By doing this, you help shift those goals-based conversations to help guide the conversation across different life stages because all phases in life are impacted by health. When you shift the conversation to focus on longevity and health, you can better understand what is going on with the client and the client’s family to help you better protect their assets based on these risks.

Three Key Challenges when Planning for Life

The first is longevity optimization. From there, you work your way into eldercare planning and that big lingering fear, which is out-of-pocket healthcare expenses.

Regardless of how they perceive their health today, most say their retirement goal is age 65, regardless of whether they had good or poor health. When asked how many years they perceive their retirement lasting, the average answer for those in excellent health and good health was 20 years of retirement, or age 85. As you started to go down to fair and poor health, you see those numbers decrease. People in fair health expect they will live about 18 years in retirement, and people in poor health expect 14 years, or age 79.

This matters because all of them are underestimating how long they are potentially going to live. Other research shows that most Americans in the U.S. will grossly underestimate their life expectancy. The average male and average female in the U.S. have a 50 percent probability of living to age 87 if they are a man, and age 90 for a woman, or as a couple, one of them might live to age 94. People guessing between ages 79 and 85 could potentially be putting their plans at risk. It is a difficult conversation when clients are stuck on thinking that they do not need their plan to go out that long.

Regardless of the person’s perceived health or how they classified their health today, what does that mean in reality? From fair health, to poor health, to good health and excellent health, all of them plan to retire at 65. But the reality is that most people end up retiring much sooner than they were planning. Sixty-six percent retire earlier than their goal of age 65.

Thirty-eight percent of Americans today are forced out of the workplace earlier than they plan because of ill health or having a health issue. Seventeen percent of people have to retire sooner than they plan because they have to step in and provide caregiving for a loved one.

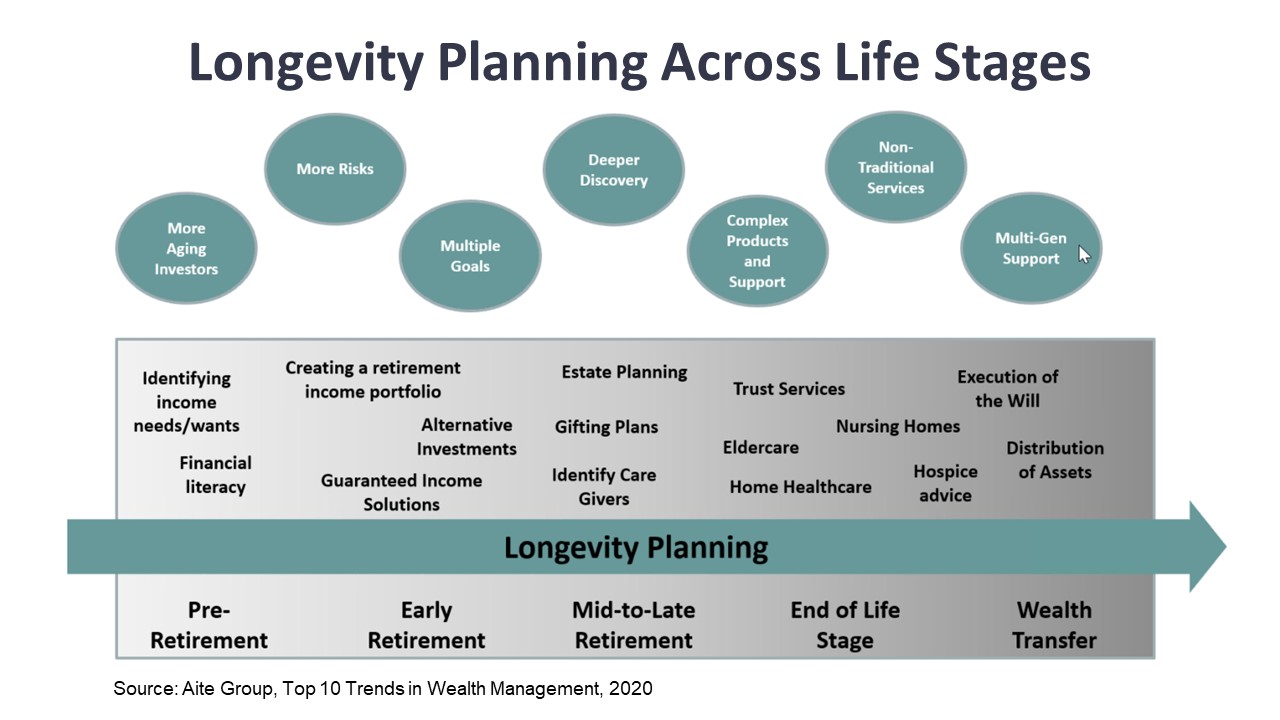

What does this all mean for you if you are thinking about bringing longevity planning into your practice? It helps you reach across the life stages. And once again, the Aite Group put together this information. It illustrates very well the opportunities advisors have to position themselves as a longevity planner at all different phases from pre-retirement through to that end wealth transfer with clients and their households.

Elder Care Planning

The reality is that two out of three people require elder care at some point in their lives. Often the disconnect is not thinking or believing or understanding that they will potentially need care.

Sixty-five percent of parents agree, and their adult children agree, that they should be having conversations to discuss their parents’ wishes as a family. Who is going to provide care? Is there a financial component for those adult children? Even though both agree that this conversation is necessary, 72 percent disagree on the level of detail. Eleven percent of kids are walking away from the conversation, feeling that the conversation did not go into the depth needed.

This is a great opportunity as the adviser to position yourself between the household, between the parents and those adult children, and help them facilitate that conversation. Show them how through the planning you are doing with the parents that either this is taken care of or if there is a need for the adult children to step in to help them understand that. The reality is that when adult children and parents walk away from these conversations, a quarter of those adult children walk away believing that they will have no responsibility for their parents and 97 percent of the parents believe they will not need their help. Reality is different.

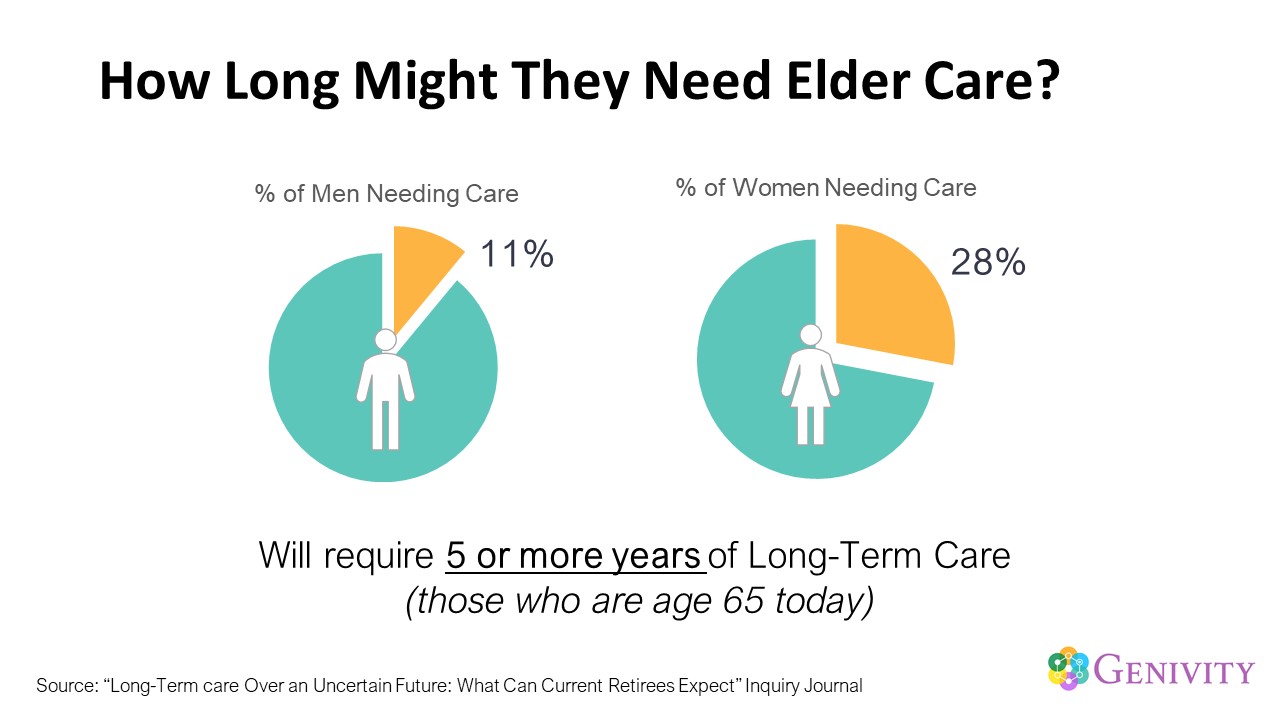

Often people wonder that when it comes to elder care, do they need to plan for it, and for how long? The average numbers are well-discussed. What is the probability of a client needing more extended levels of care? For people aged 65 today, the need for five or more years of long-term care is much lower for men at around 11 percent, but for women, up to 28 percent of women will need five or more years of care.

Circling back to that adult children conversation, who will be there to care for your clients? Seventy-two percent of parents, regardless of thinking if there is a financial impact on their kids, believe that one of their children will be the person who can be the go-to person they can count on. Forty percent of those children have no idea that their parents think – are counting on – them to be the ones to do it. Siblings need to understand who is going to be that lead caregiver. This is an opportunity for you as the advisor to speak with your clients because the lead caregiver is often the alpha child in the family. Knowing whom that identified person is and establishing that trusted relationship can help move the needle if you think about wealth transfer, family dynamics, and family relationships.

Out-of-pocket Healthcare Costs

Baby Boomers’ health fears are clear. Fifty percent of high-net-worth pre-retirees are terrified of healthcare costs and what that will do to their retirement and financial well-being. Almost 40 percent of Boomers are unsure whether their advisor is knowledgeable about this issue, so they are not bringing it up to them. So, this is your chance to engage in these conversations and let your clients know that this is an important conversation area and that you are there to help them understand and address it.

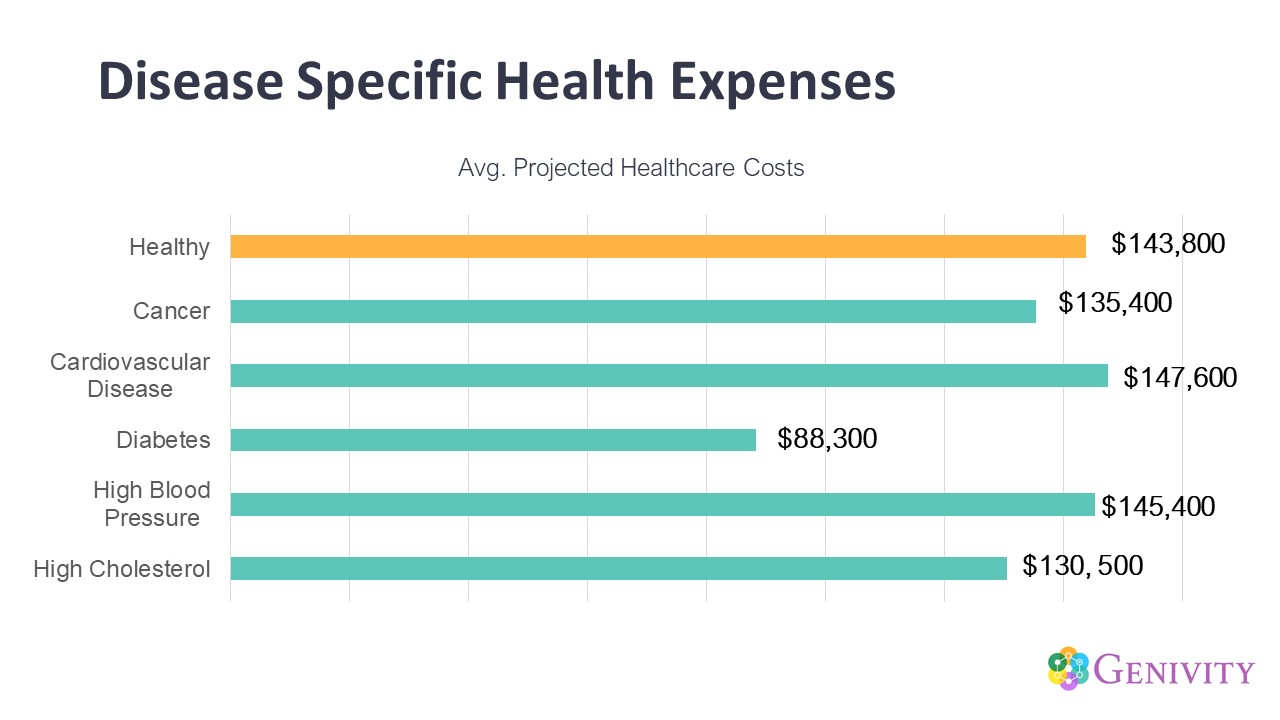

What does “addressing” it mean? Fidelity does some great research about the expected average annual healthcare expenses for a couple. But no client is average, and no couple is average. When you start looking at different health conditions, health, in general, is not average. Healthcare costs in retirement can look different based on your health risk or the health condition you have today. There is a wide range between cancer, cardiovascular disease, and diabetes. We tend to see shorter life expectancies for people with diabetes.

Being a healthy individual has one of the higher-projected healthcare costs in retirement. Many people think that because they are healthy, that means my healthcare expenses will be a lot lower. The reality is that this is not the case. In retirement, you will see higher healthcare costs for healthy individuals because they are living longer and will need to pay for healthcare longer. They will also be doing more preventative health care.

What Does Genivity’s HALO Measure?

How do your clients think about their family’s longevity? How do you incorporate that into their plan? From there, then you can plan for elder care and then future out-of-pocket healthcare expenses. This leads to what we do at Genivity, which is to help advisors help their clients understand in a personalized way how health and longevity can impact their finances.

The standard way of estimating longevity is to use an actuarial table, which does not create the personalization level needed as it is a population-based average. By creating personalization and matching the individual client to people similar to them, we can help create better data and assumptions to plan future healthcare expenses.

We create a digital experience for clients built around grounded science, sound research, and data. This drives everything behind the algorithms that create a very individual personalization for each client.

Advisors can use our interactive digital assessment directly with their clients and prospects to help those concerned about longevity and health understand their risks. It is designed to take the client less than five minutes to complete.

In the typical client scenario, we start with background information to establish a baseline for calculating their personalization. Depending on how the client answers, different questions will reveal additional questions to create even more personalization. Each question along this path directly impacts the outputs in our results.

The second phase of the assessment focuses on the most critical lifestyle factors that can impact how long you live. Many people think that their genetics are their destiny, which is a big misconception. The reality is that lifestyle and environment play a huge role in how your health progresses and whether different diseases you might have a genetic risk for come to fruition.

Exercise is incredibly important, and smoking has the most significant negative impact on longevity, which is probably no surprise. Diet has a smaller impact. Alcohol is probably one of the more complicated calculations because depending on how much you drink and your age and gender, that can be a positive or a negative at different phases of your life.

The last component is emotional support. Who is in your care circle? This has an incredibly strong tie to future longevity. For clients who do not as strong as a network, this can be a great area to help them try and optimize their life for creating these connections.

In the health section of the assessment, we start by understanding their healthcare mindset. How are they utilizing the healthcare system today? Because if they are lower utilizer, their out-of-pocket expenses will be a little bit lower; if they are a higher user of the system, they’ll experience higher heathcare costs.

We also look at health conditions, which are important for you to think about in your client conversations. The 15 most common chronic health conditions in the U.S. have a strong family-history component to it, so we want to understand their risk from their immediate family level as well as for themselves.

Once someone answers yes to a question, we get more personalized from there. We look at Alzheimer’s and Dementia. We look at diabetes. We look at heart disease, and we look at a stroke.

You can use this in your practice without HALO because understanding clients who have a family history of these risks can tell you if it is a first-degree relative, meaning their parents or their siblings. This significantly increases their probability of having that disease. Costs will be different based on different diseases. But understanding that can help you start to understand where their future costs could go and what are some of the steps to take.

Then we start tying things back to their retirement goals. We create personalization of cost based on the state that they want to retire in. In the last part of our assessment, our algorithm has already done an initial risk assessment of the client.

Your client can complete the assessment in the privacy of their own home, which is great during COVID for digital engagement, or it is something that you can do either screen sharing or together side by side. We focus on their longevity health span and helping them get into the frame of mind of living longer than they might expect.

A Case Study with Jane and John

Jane and John are pre-retirees. Jane makes $75,000 a year; John makes $250,000. They both want to retire at 65 and in Florida.

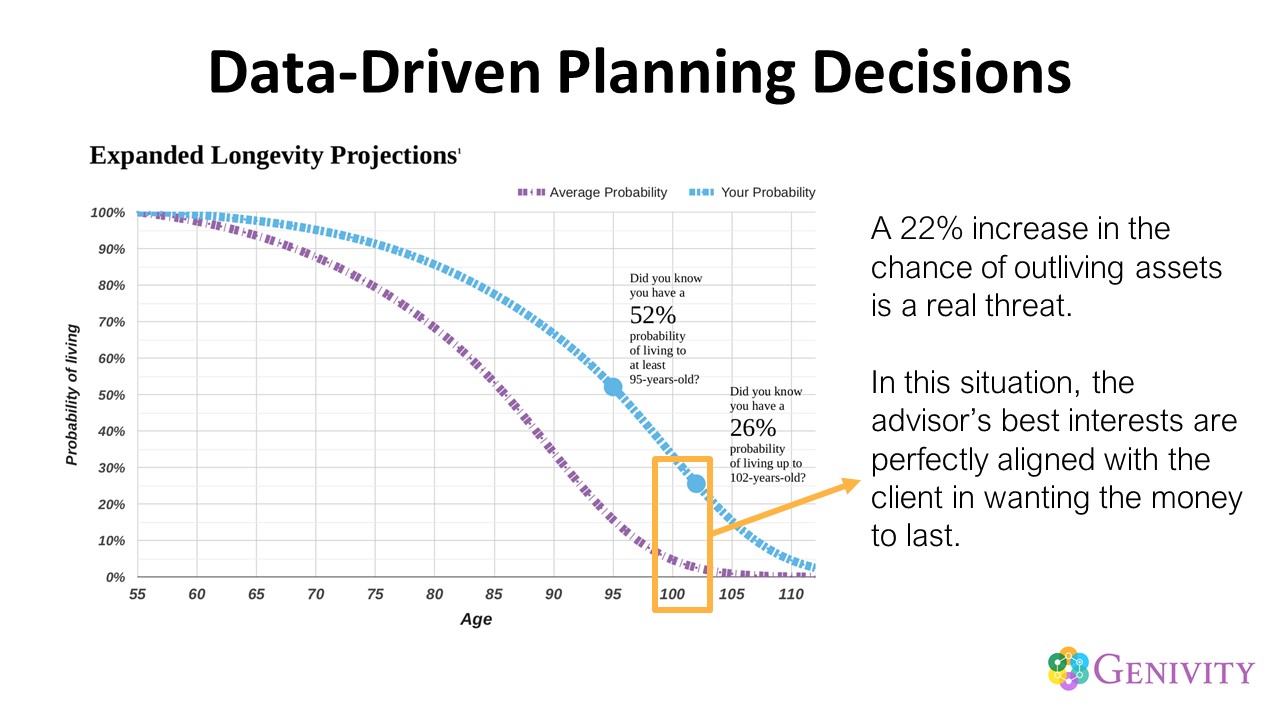

Jane has an incredibly healthy lifestyle. She has several family members that have had extended longevity. From her longevity healthspan, we can see that she has a 50 percent probability of living to be aged 96 or older, so she is already well on that high average. But let us look a little bit deeper at her projections.

The blue line on this chart is Jane’s personalized probability. Now we match her to women just like her, same ethnicity, family health-risk profile, and lifestyle choices. You can see where this starts to make a pretty big difference.

In this case, is she has a 26 percent chance of living age 102. The average woman has approximately a three percent probability of living that long.

This is where you can step in to see where she feels most comfortable from a risk perspective. How far out would she feel comfortable moving the plan and the decisions around that to help her meet these goals? This is also a great way for you to sit on the same side of the table in an unbiased way to discuss different investment decisions.

Now let’s look at John’s profile. John has a few opportunity areas that he could optimize. John does not like exercising. He hates his fruits and veggies. He likes to live life his way. But he does have a family history of heart disease. So far, he has been a pretty healthy guy, but we know that some risks are lingering for him that could create some financial issues.

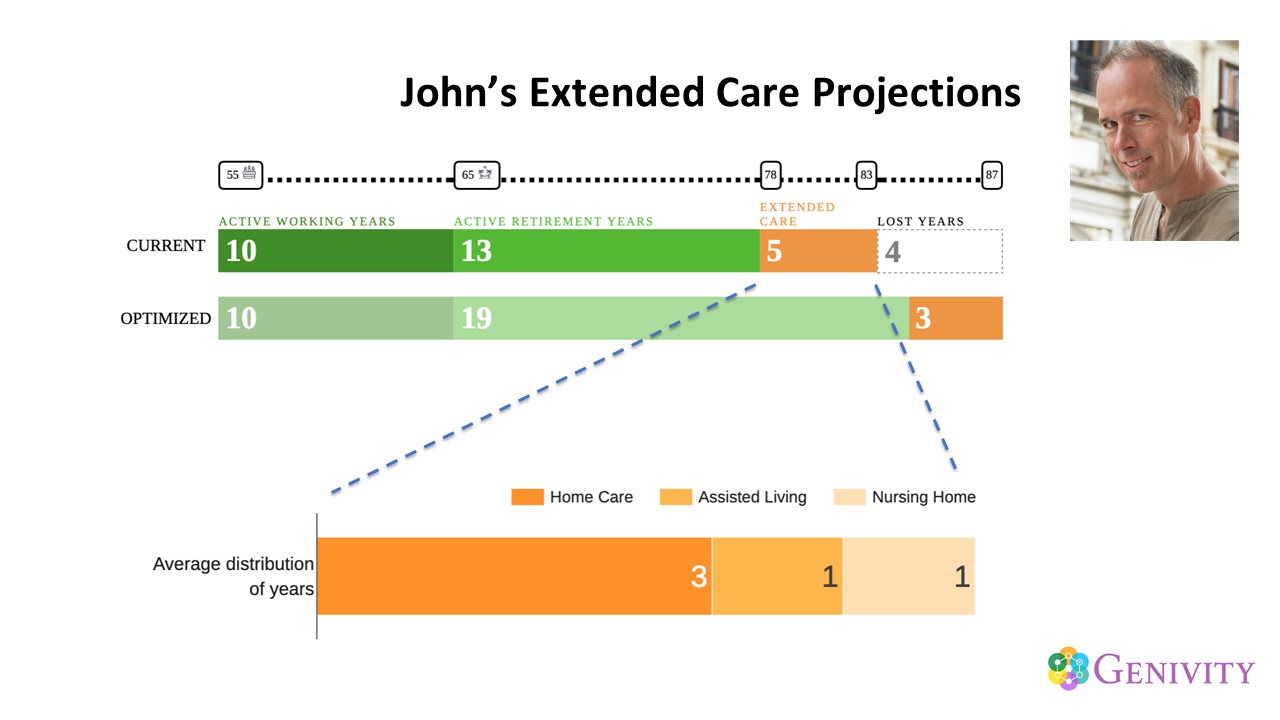

Let’s take a closer look at John’s personalized longevity health span. The first line is what his longevity healthspan is today. We are projecting for him 13 active retirement years once he retires at 65, with around five years of increased levels of slowing down. And he has some opportunity years to optimize if he made some lifestyle, exercise, and diet changes.

Below this is the optimized scenario. If John made changes today, he could have six more active years to spend with Jane and possibly reduce his slow-go years down to three. Also, he has further optimized his life expectancy.

So what about the slow-go years? HALO takes those five years and breaks them out in distribution around how many years of more home-based care is he likely to need, where possibly Jane takes care of him before he needs more stepped-up levels of care. We project three years of home-based care before needing to step up to some level of assisted living or home healthcare, and then later, a level of nursing home support.

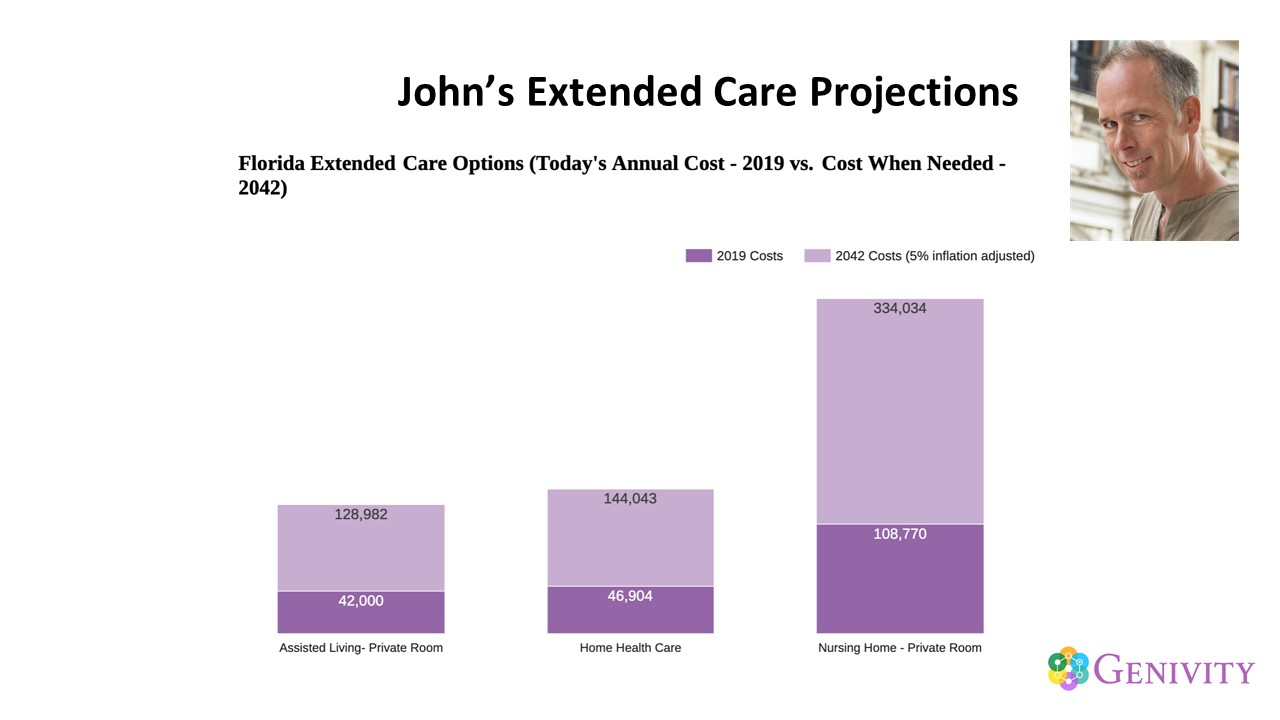

We then estimate costs in today’s dollars and future dollars with inflation, with different care levels so that John and Jane can come up with a scenario that makes the most sense for them.

As an advisor, this provides the information you can then input into your planning software to create more personalization for both Jane and John.

Key Takeaways

There is no avoiding it. At some point in our lives, we will experience a health crisis. That could be our own or a loved one. There is no escaping that this will happen and the impact it can have.

Suppose you wait until a health crisis happens. In that case, there may not be time to have these difficult conversations around health when there is no longer an opportunity to look at alternative solutions to help them plan and prepare. You want your clients and their adult children to know that you are the first person to call when a crisis like this happens because you will help them then figure out the financial parts of it and how they are going to take care of it.

As someone who personally has gone through a health crisis with a loved one, having that open and ongoing dialogue with an advisor long before a crisis happens made all the difference. This creates a loyal next-generation client for you.

Health is the one thing that will bring a family to their knees and stop everything and bring them together regardless of wealth level. While families can be funny about how they talk about money or what they are willing to talk about as it relates to money, health tends to be the area that is more of a uniting factor for them. This is a way for you to be that connector across the different family members.

I hope you understand that the future of goals-based financial planning must include planning for health. I would like to see that talking about health and planning for longevity – just like in the medical world where we talk about the standard of care for treatments – becomes the standard of care for goals-based financial planning. This approach is something you can actively incorporate into your practice and use as a key way to differentiate yourself from your competition.

Part of that planning for life and planning for health needs to include longevity, as people are living longer. There is no escaping this part of it. Longevity planning is your key to having a positive conversation about how a client wants to spend those active years in retirement and celebrate the things they have been able to accomplish and do. Health and longevity are facts. None of us are escaping them. You can approach them from two sides: from the more scary aspect that we are all going to be facing this, or once you understand and start thinking about longevity and health, it allows you to plan for what you want to accomplish in life.

Whether that means retiring earlier or retiring later, or so they have more time to achieve the things they want to do; whether it is making those lifestyle changes today, so they have a more active retirement, or they have greater longevity … all of this helps you help clients understand what they can do to achieve their retirement lifestyle goals. This is an empowering conversation to make people feel good and shows the value of the strategies you have been putting in place for them.

Dr. Coughlin from MIT’s AgeLab does much wonderful research about longevity and the impact on health and financial planning. He wonders if financial advisors can fulfill their fiduciary responsibility to clients today without an intimate understanding and knowledge of their health aspects that impact their physical and financial lives.

By starting these conversations, bringing them into your plan, you can put that stake in the ground that shows clients how you are different, shows prospects why they should be working with you, and helps set your practice up for this next phase of holistic planning.