What is Medicare?

Let’s start with the two main parts of Medicare: Medicare Part A and Medicare Part B. Medicare Part A covers your hospital visits, skilled nursing, mental health, Hospice, etc.

If your client or spouse has worked 40 quarters, which is ten years, and they’ve paid their FICA taxes during that 40-quarter requirement, they don’t pay anything extra for Medicare Part A premium. They prepay those premiums through their FICA payroll taxes. But if they have not met that requirement, Part A can cost over $400 a month.

Medicare Part B covers most of what people need when it comes to their healthcare. Part B covers doctors’ visits, lab tests, therapy, durable medical equipment, etc. In 2020, most pay $144.60 a month for Medicare Part B. It can be less if your client is on Medicaid, but it can also be more if your client has a higher income.

If your client had a modified adjusted gross income in 2020 – the premium is based on their taxes – of $87,000 or more as an individual, or $174,000 or more as a couple, they will pay more for Medicare Part B. The more they make, the more they pay. That said, there are ways to appeal income surcharges. I think it’s vital as an advisor to understand how these income surcharges work because the way you recommend retirement distributions can impact how much Medicare costs them.

Medicare usually only covers 80 percent of healthcare expenses, and individuals are responsible for the remaining 20 percent – Medicare doesn’t pay 100 percent of their healthcare costs. There are some exceptions, including the fact that Medicare will cover 100 percent of preventative services approved through the Affordable Care Act. However, everything else is essentially covered by the 80/20 rule.

Medicare Supplements and Medicare Advantage Plans

For that reason, we have both Medicare supplements and Medicare Advantage Plans. Those are the plans that come in to help cover that 20 percent that Medicare does not cover to reduce your clients’ healthcare risk once on Medicare. This is where I think Medicare gets confusing.

What most people don’t know is that there are two different Medicare program choices. People get to decide which program they want to provide their Part A and their Part B services. The first program is called Original Medicare, also known as traditional Medicare. The second program is called Medicare Advantage, also called Medicare Part C. To understand the differences between the two programs, let’s talk about how each one works.

The federal government administers Original Medicare and negotiates prices with the doctors and the hospitals. It includes both Medicare Part A and Medicare Part B. Under Original Medicare, you can see any doctor or hospital across the entire country that accepts Original Medicare.

Studies show that about 95 percent of doctors in our country accept Original Medicare. When people are on Original Medicare, they can see any doctor across the entire country who accepts Original Medicare. Now Original Medicare generally does not include coverage for prescription drugs. But there is one exception.

Medications that must be administered by a medical professional, such as chemo at the doctor’s office, other injections, must be covered by Medicare Part B. But all other prescriptions that people get from their pharmacy are not covered by Medicare Part A or B, but instead covered by Medicare Part D drug plans, which are standalone plans offered by independent insurance companies. Also, as I mentioned before, when you’re on Original Medicare, it only covers 80 percent usually of medical services, and people are required to pay the remaining 20 percent if they only have Part A and B.

However, this is where supplement, also called Medigap, insurance comes in. Most people on Original Medicare will get a Medicare Supplement plan to cover nearly most of the 20 percent that Medicare does not cover. Medicare Supplement plans only go with Original Medicare. They never go with Medicare Advantage.

What is Medicare Advantage?

Now let’s talk about Medicare Advantage. One of the critical differences between Original Medicare and Medicare Advantage is that Medicare Advantage is administered by private insurance companies approved by Medicare to offer the benefits. It’s the Blue Cross Blue Shield, Humana, United, Aetna; all those companies out there have Medicare Advantage plans.

These private companies are the ones negotiating prices with the doctors and the hospitals. While Medicare Advantage plans must offer all the same coverage as Original Medicare, they can determine which doctors and hospitals you can see since they are the ones negotiating prices. Most Advantage plans work like HMOs or PPOs.

Advantage plans might offer extra benefits, like drug coverage, free gym membership, extra vision, or dental services. Please also note that Medicare Advantage plans have co-pays and co-insurance, and they can also have max out-of-pocket costs, which in 2020 can be up to $6,700 a year for in-network providers.

There’s another critical thing that you should be aware of when it comes to these programs. One of the main reasons people regret their decision is that they didn’t fully understand this difference. I can’t go into all of the differences, but let’s go into one in a bit more detail. It has to do with the doctors that you can or cannot see through each program.

The Differences Between Medicare Supplement Insurance (Medigap) and Medicare Advantage Plans

As I mentioned earlier, with Original Medicare, people can see any doctor or hospital that accepts Original Medicare. In contrast, with Medicare Advantage, people can usually only see doctors in their network. Depending on the doctors your client currently sees, or they want to see in the future, they should easily fit best into one program or the other.

But here is what usually happens, which is why people regret their decision. Usually, an insurance company will come to your client, or they’ll see them on the television. Most of the time, they encourage people to send out for a Medicare Advantage plan first. And they do this because it makes insurance companies a lot of money, which they openly share in their financial reports. Since Medicare Advantage plans are very profitable for insurance companies, they spend more on advertising. They put more perks in it to entice people to join. But the reality is they don’t always share the full story. They don’t always share the co-pays, the high max out-of-pockets, and they don’t always share the doctors you can or cannot see, which is the most important thing.

How Medicare Insurability Rules Work

Many people approach their Medicare decision, and they say, “You know what? I’m just going to pick the cheapest plan. I’m healthy,” or, “I’ll get the plan with the gym memberships, or dental and vision coverage. And when I need something different, I’m just going to change plans later.”

The fact is that Medicare rules don’t let people just change plans whenever they want. It is crucial to understand how these insurability rules work because it impacts how your clients pick their program.

If your client needs to switch programs in the future, it is easier if you first join Original Medicare, and then you can more easily go into Medicare Advantage later. It is much harder, if not impossible if you first join Medicare Advantage and go back into Original Medicare.

Here is why. When it comes to Medicare Advantage plans, they really can’t turn anyone away. If your client applies for a Medicare Advantage plan during an approved period, and they don’t have, say, end-stage renal disease, they have to accept you. While technically, Original Medicare can’t turn people away either, supplement – also called Medigap – insurance companies can turn people away.

Remember how I said Original Medicare only covers 80 percent of most expenses, and either the individual or the supplement plan pays the remaining 20 percent? Well, this is where it gets tricky. When people first join Medicare, they have a six-month window where they are automatically eligible to join any supplement plan of their choice. They can join these plans, whether they are healthy or sick.

They can have Stage IV cancer, diabetes, lung issues, heart issues, autoimmune issues, be on depression medicine, and the Medigap insurance companies are required to accept them during this six-month window. Medigap insurance companies cannot charge them more for any of the pre-existing conditions. However, once this six-month window expires, these guaranteed-issue rights expire also.

So, after the six-month window, in most states, to switch letters, join a new plan, switch companies, any of those things, the company can and will ask for the individual’s health history. They can deny coverage if they’re unhealthy or if they don’t want to cover them for any reason. Therefore, it’s hard, if not impossible, to switch programs after someone first joined Medicare.

Most people don’t realize that they’re in the wrong plan until they’re sick, and once they’re sick, it’s usually too late to switch. So, again, what I’m saying here is that if your client first joins Medicare Advantage and they later decide they’d rather be in Original Medicare, they may not be able to switch.

The only way people can easily switch is if they’re completely healthy and insurable. Suppose they’re not healthy, while they can still join Original Medicare, they likely will not be approved for a Medicare Supplement plan. So they are now responsible for 20 percent of their medical bills, which can quickly bankrupt them.

How to Help Your Client Decide Which Medicare Program Best Fits Their Needs

For your client to decide which program fits them best, they should look at:

- What Medicare their current doctors accept

- If they were to get sick, who their future doctors might be

- What Medicare future doctors might accept

- If your client is traveling or living in multiple states and how that might impact the program they pick

- Look at the costs and the risks of each plan to see which one ultimately best fits your client.

If your client ends up going down the Medicare Advantage route where they talk to their doctors, they all accept Medicare Advantage, they’re completely fine with that, there are four things that they should be doing to identify the right Medicare Advantage program.

- First, find out which doctors they can see on that plan. Kaiser is unique, where you can usually only see doctors inside of the Kaiser network. But other plans can have exceptions.

- Look at all the costs: the premiums, the deductibles, the co-pays, the max out-of-pocket, both in-network and out of network.

- Look to see how well that plan covers your client’s medications. There can be thousands and thousands of dollars in medication cost differences through different plans.

- And then also look at the fine print of the document.

Each plan has about a two- to three-hundred-page “Evidence-of-Coverage” document, where they will outline particular fine print, as they’ll only cover 20 percent of the cost of chemo until they reach their out of pocket limit. There are little things that should be looked at before finalizing any Medicare Advantage plan.

That said, most people in our country are on Original Medicare. Original Medicare is more work upfront. In my opinion, when our clients’ doctors accept Original Medicare, it’s worth it because they can see their doctor. I think of Original Medicare as an all ala carte menu. There are Medicare Part D plans and Medicare Supplement plans, also called Medigap plans, to choose from.

With Original Medicare, people can customize a plan to fit them best, the coverage they want, and at the cost they want. Original Medicare includes Medicare Part A and B and does not include prescription drug coverage. Once your client confirms they want to be on Original Medicare, the next step is to pick out a Medicare Part D drug plan.

When you first look at these prescription plans, they all look very much the same. But prescription plans have little details that make a huge difference in cost. For this reason, it is incredibly important for people to get the right Part D drug plan.

Here is how Medicare Part D drug plans work. First, Medicare determines the types of medications that every plan must cover. Now some plans will include extra medications, but they’re not required to do so. Now once this list is released, insurance companies go to the drug companies to negotiate prices. Depending on how good a deal the insurance companies get, it will put the drugs in different tiers. There are usually five different tiers, with the first being the cheapest and the fifth being the most expensive.

So the right plan for your client depends on many factors, including the medications they take, the tier their medication falls into, the premiums, the deductible, their preferred pharmacy, and whether or not your client hits a donut hole or even catastrophic coverage levels.

This is a high-level overview of Medicare Part D. There are three other things that I want to share with you that most people are not aware of, and it can be hard to find out on your own.

- Medicare Part D drug plans have prescription penalties. Medicare rules say by the time you turn 65, you must have a creditable prescription drug plan, and if not, you’ll face penalties.

Most people are on medications, so it’s usually a no-brainer to just get a Part D drug plan. But there are quite a few people out there these days that don’t take any medications. If your client is in that boat where they don’t take any medications, be aware that if they don’t have a creditable drug plan, either for a Part D plan or included in their Medicare Advantage plan, they will be penalized. The penalty isn’t huge, but it’s still a penalty that applies for the rest of your life.

- Medicare Part D plans also have high-income IRMAA (income-related monthly adjustment amounts) surcharges. So, IRMAA surcharges mainly impact what your client pays for Medicare Part B, but it will also impact what they pay for their drug coverage as well.

- Part D plans change every single year. These plans do not have insurability rules so that everyone can change plans every single year. Your client must review his or her plan every single year during open enrollment.

- Here’s how it works. By October 1st of every year, every single Part D plan must announce the new plan details for the upcoming year. Your client then has from October 15th through December 7th to review those plans and change plans for the upcoming year. This is the only time that most people can change Part D drug plans during a year, so it’s essential to get this right. During this time, you can change things like premiums, add or drop medications, add or drop pharmacies, or change the tiering of the medications’ price. We are currently in this process right now of doing our clients’ annual reviews for them. Our average savings every year per client are between $800 and $900.

People often ask me, “Well, Emily, which is the right Medicare Part D drug plan?” It’s like a giant game of cups. There is no good plan; there is no bad plan. But there is a plan that will fit you best. It’s just all about finding that red ball every single year. Most couples will be on different medication plans because they have different medications. Again, it’s all about finding out what ultimately fits you best.

Picking Out a Medicare Supplement Plan

A Medicare Supplement Plan is sometimes called a Medigap plan because these plans fill the 20 percent gap that Medicare does not cover. These supplement plans only go with people who are on Original Medicare. If your clients have chosen to go the Medicare Advantage route, they will not have one of these plans.

I highly recommend that people on Original Medicare pick a supplement plan out when they first join Medicare. Supplement plans are critical to reducing what someone pays out of pocket for their healthcare. Original Medicare pays 80 percent. If someone does not have a Medicare Supplement plan, they are paying more or less 20 percent of their health care cost. None of us know what the future holds. For that reason, I highly recommend that people plan for all scenarios and choose a plan when they first join Medicare that they’re comfortable having when if they were to have health issues.

A few weeks ago, we received a call from Kate, a 30-year-old teacher, and she was calling on behalf of her dad, who’s on Medicare. He was recently diagnosed with end-stage renal disease, which is luckily covered by Medicare, and the treatment includes dialysis and possibly a kidney transplant. While it’s great that Medicare covers the treatments, it is not great that her dad did not get a Supplement insurance policy when he first joined Medicare.

Kate called to see if there’s any way that we could help them get financial coverage of some nature because she knew that 20 percent of the cost of his dialysis would quickly go through all of his savings. Based on the government rules, the government won’t step in for extra help until he has no money left to his name.

However, it’s too late to get a Medicare Supplement plan. He missed that chance. But, there are still some options that are a bit more complicated because he does have end-stage renal disease. If he simply would have gotten a supplement plan when he first joined Medicare, he could have avoided this huge financial risk now and the stress it’s causing on both him and his family.

Again, if your client goes down Original Medicare route, please encourage them to pick a supplement plan out when they first join Medicare. These are the plans that have the insurability rules. When someone first joins Medicare, they have a six-month window where they’re automatically insurable, and the companies must accept them no matter what their health conditions are.

But once that six-month window expires, in most states, the companies can and do ask for their health history whenever they apply for a new plan, a different letter, a different company, any of those things. Therefore, it’s so important to get it right.

Now with Medicare, there are always exceptions. New York State allows people to move between Medicare Advantage and supplement plans without any medical underwriting. And so, if you have a client in New York State, these rules are different. You will see that the plans in New York State are much more expensive than any other state.

Washington State has a rule where you can move between certain supplement letters without underwriting. So, there are some states like that. There are about five or six states that have rules like that. But most states have standard insurability rules.

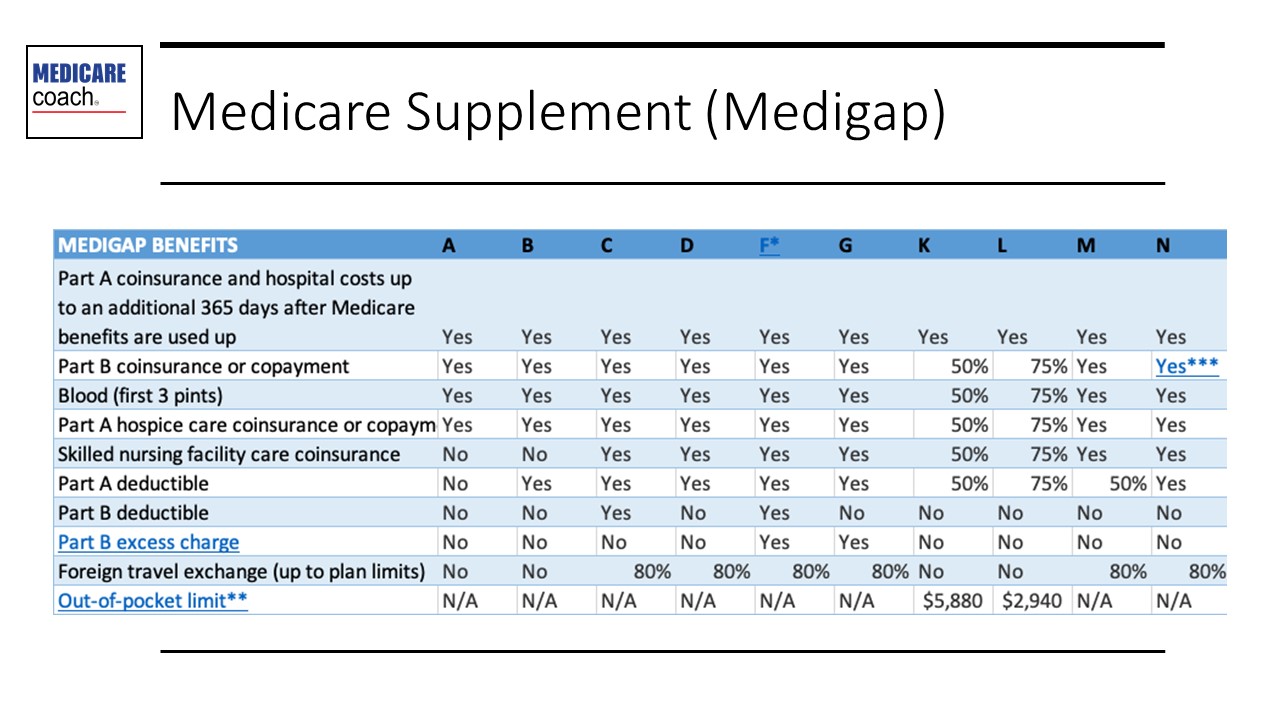

The first step to picking the right supplement plan is choosing a letter. On this chart is the current letters that are offered in most states across the country. Please know that if your client lives in Wisconsin, Minnesota, or Massachusetts, they have their supplement plans, so they won’t have these options. But the other 47 states and territories will have these letters.

There are lots of letters when it comes to Medicare. There is Medicare Part A, which is hospital insurance. There is Medicare Part B, which is medical insurance. There is Medicare Part C, which is Medicare Advantage. Medicare Part D is a drug plan.

Please don’t confuse those parts, letters, with these above supplement letters. Medicare Part A and Supplement Plan A are two very different things. Supplement plans differ based on what they cover, and they also differ based on their premium. Premiums range anywhere from about $30 a month to over $200 a month.

A woman came to me a few weeks ago and said, “Now, Emily, I did my own Supplement research, so I don’t need your help there. I just picked the most expensive Supplement plan because I assumed that that was best.” It literally made me cringe because the plan she picked was not the best. It’s expensive because no one’s in it. It will cost her a lot of money, and she already missed her six-month window, so I can’t undo that.

So your clients must get that right letter when they first join Medicare. People often ask me, “Emily, which letter is best?” It depends. Most of the married couples that I work with end up on different letters because they have different health issues; they have different doctors; they have different health concerns; they’re different people. Medicare is a very individual decision.

Some supplemental plan companies are adding extra perks like gym memberships, or extra vision and dental, which can be valuable. I don’t recommend people decide when it comes to Medicare on those factors, but it can be a factor to be aware of when adding extra coverage for your client at a lower cost.

Once people decide which letter fits them best, they need to determine which company they want to provide them in that plan. When looking at companies to purchase a plan through, look at things like the history of the rate hikes, how contracts are priced, the company’s financial stability, the customer service, and things like that. We capture these things in our Medicare Supplements Scorecard to be able to compare companies against companies easily.

You can’t always tell from their name or from their public image which really is the best. There are dozens of companies in each state who offer Supplement plans.

What You Can Expect in Medicare Costs

What your client ultimately pays will be based on where they live, their income, their health conditions, their doctor considerations, etc.

With Original Medicare, most of your clients will pay nothing for Medicare Part A. At least for 2020, most of your clients will pay $144.60 a month for Part B. Again, if they have a higher income, they are also subject to IRMAA surcharges.

In most states,

Medicare Part D drug plans have a premium from about $6 a month to $150 a month. These plans also have co-pays, so what your client pays for drug coverage will depend on their medications, their pharmacy, their plan, all of those good things.

The final cost of Original Medicare is supplement coverage. In 2020, these ranged anywhere from $23 a month to around $250 a month. The maximum out of pocket on most of those plans is around $2,340 a year. This will give you an idea of what you should be planning for when it comes to the Original Medicare route based on how the current environment looks.

The second path is to use Medicare Advantage plans. You’ll have the same, likely zero, cost for Part A. You will likely have the $144.60 a month for Part B and then the Medicare Advantage plan, where their premiums go anywhere from zero a month to a couple hundred a month. Medicare Advantage has a vast range of premiums. The critical thing to look at is they do have co-pays. They have a maximum out-of-pocket of up to $6,700 for in-network doctors, and they usually include drug coverage.

Strategies to Help Your Clients Prepare for Medicare

There are a few things that you can be doing with your client as early as 60 to help them prepare for Medicare.

- Identify your clients who are over age 60 or if they haven’t retired yet and are not on Medicare today. Help them think about the doctors they’ll want to see; how it will impact the Medicare program that they pick, whether they are with that doctor now or might be in the future. This could be a Mayo Clinic, an MD Anderson, or a EuroMed. One of our good family friends had Stage IV lung cancer, and he went to a Euromed facility. He’s now completely cured of cancer. But Medicare is not accepted at all there. So, if your client says, “I want to go to a place like Euromed” that doesn’t accept any Medicare, then that could be an extra planning line for their retirement. But having those conversations now can help you understand what you’re planning for in the future.

Also, ask your client early on:

1. If they have any other health insurance we should be looking at

2. Whether they are working past 65 and still have an employer plan

3. Whether they came from a corporation or a union which has a retiree plan

4. Whether they have VA benefits, TRICARE for Life, or ChampVA.

Understanding the healthcare options that your client has outside of Medicare is essential to consider before you assume that they’re going on Medicare.

- How might the retirement distributions that you’re recommending impact what they pay for Medicare? Medicare premiums change every single year based on the previous two years’ income. If your client plans to take a lump sum of money out for a new home or a child’s wedding or something of that nature, understand how the Medicare rules work. I’m not saying you should make a recommendation based on these income requirements. I am saying that it’s good to be aware of Medicare’s income limits so you can at least make informed recommendations.

- Talk to your clients about whether they should be delaying Medicare. Different factors go into deciding whether your client joins Medicare at 65 or whether they delay it. I know that this sounds silly because people assume that you must join Medicare at 65. But that’s not the case. And if your client incorrectly joins Medicare at 65, it can be a huge waste of money.

The Medicare rules say that when you turn 65, you either must be on Medicare or covered under an acceptable health insurance plan that meets Medicare rules. Now, if you don’t meet one of these two requirements, you will face lifetime penalties. For your retired clients, if there’s no other form of health insurance past age 65, then, yes, they should be joining Medicare. But most people today are working past 65, have some health insurance, or their spouse is working past age 65.

There are specific rules that a plan must meet to delay Medicare without penalties. It’s important to understand that this rule does exist and decide what makes sense. For most employer plans to meet Medicare rules, they must meet all three of these requirements.

- The first one is, do you have health insurance of some type through a company? Obamacare does not meet this rule. COBRA does not meet this rule. Medi-Share plans don’t meet this rule. VA makes you join Medicare. TRICARE for Life or ChampVA requires Part A and B. There are some nuances. My point is just because they have a plan, it does not mean that it meets Medicare rules. So be aware of this.

- The employer providing health insurance must have 20 employees or more, and if your client is disabled, the employer must have 100 employees or more. If the employer providing health insurance does not meet this rule, then your client must join Medicare.

- Does the employer plan have creditable prescription drug coverage? Creditable means the plan, on average, covers prescriptions as well as or better than Medicare. The company’s benefits person is legally required to confirm this every single year for your client.

If your client meets all of these requirements, they can delay Medicare.

I would say that before you finalize that decision, compare the employer plan vs. Medicare. A client of mine was going to work until at least age 70. But we found that she could save $16,000 by leaving her employer plan and joining Medicare instead. I have other clients, especially with high incomes, who were better off on their employer plan for as long as they possibly can. Again, just know that there are different situations where you’re better off on Medicare, and others where you’re better off on your employer.

- Find out if your client’s spouse is working past 65. If they have a retiree health plan, evaluate how good the retiree plan is, or are they better off on Medicare? Usually, the tipping point is that if a retiree or employer plan has a premium, monthly premium of $250 a month or more, you’re almost always better off on Medicare. It can depend, though, but that’s about where the tipping point is.

Just because your client or spouse has an employer plan or a retiree plan, it does not mean that that one is truly best for them. I have seen some really bad plans out there offered by employers, by retiree plans, and people just assume that they should take that coveted employer or retiree plan because they’ve worked their whole lives for it; but it’s not always best for them. It’s a stern message to deliver, but it’s an important one to talk about before your client finalizes anything.

Key Takeaways

- Most of the changes and decisions happen when your client first joins Medicare. If your client is already on Medicare, please recommend that they review their options every year during Medicare’s annual election period. There can be huge changes, especially in Part D drug plan, so this is another reason to meet with your clients every September. Remind them that the Medicare enrollment period is coming up to make sure they take advantage of it.

- Please look to see if the income distributions you recommend create temporary increases in your client’s income that might result in them paying more for Medicare.

- Help your client think of the doctors they want to see once on Medicare, or after age 65, and the corresponding Medicare program and cost implications that will impact their retirement planning. Remind your clients of Medicare insurability rules.

- Finally, if your client is already on Medicare, make sure they review their plan every year.

For anyone who’d like to know more about the Medicare Coach, have us help your clients. Our signature offering is a Medicare Enrollment Concierge Service. It’s a done-for-you service that includes a four-part process that will take your client from the very beginning, no matter where they are. It could be simple; it could be complex. It takes them through the entire process to ensure that they’re making the right decision, the right timing, the company, the right plan, and all of those details to truly ensure they’re protecting their healthcare rights and retirement savings. This is where we use our expertise – when it comes to Medicare with both the rules, the insurance companies, all unique things to guide your client to help them save money and save time.

Ideally, clients start our concierge six months before they ever join Medicare, so there’s time to be thoughtful and thorough with this important decision. Most of the clients who join our service save time, hassle and ultimately gain peace of mind that they’re doing the right thing regarding Medicare.