The following is an excerpt from the August 2016, GAO Report to Congressional Requesters, “401(K) PLANS: DOL Could Take Steps to Improve Retirement Income Options for Plan Participants”.

Why GAO Did This Study

As 401(k) plan participants reach retirement they face the challenge of making their savings last for an unknown lifespan, and many 401(k) plan sponsors do not offer options to help participants with this complex task. GAO was asked to review any related challenges and potential changes to help plan sponsors and participants. This report examines, among other things, barriers that deter plan sponsors from offering such options, and the defaults that exist for participants who do not choose a lifetime income option. GAO administered a non-generalizable questionnaire to record keepers, conducted a non-generalizable survey of 54 plan sponsors, and interviewed a range of stakeholders.i

What GAO Found

Workers relying in large part on their 401(k) plan in retirement may not always have a feasible way to make their savings last throughout retirement. Responses to GAO’s non-generalizable questionnaire from 11 401(k) plan record keepers— entities that manage participant account data and transactions for plans— showed that most plans covered by the questionnaire had not adopted products and services that could help participants turn their savings into a retirement income stream (referred to as lifetime income options in this report). Responses to the questionnaire represented more than 40 percent of all 401(k) assets and about a quarter of plans at the end of 2014. GAO found that of the plans covered by the questionnaire, about two-thirds did not offer a withdrawal option — payments from accounts, sometimes designed to last a lifetime—and about three-quarters did not offer an annuity—arrangements that can guarantee set payments for life.

Concerns about legal risks and record keeper constraints may deter many plan sponsors—typically employers that provide 401(k) plans and establish investment and distribution options—from offering lifetime income options. The Department of Labor (DOL) issues regulations and guidance for plan sponsors and is responsible for educating and assisting them to help ensure the retirement security of workers. For example, DOL has prescribed steps plan sponsors can take to satisfy their fiduciary duties (i.e. act prudently and in the best interest of participants) when selecting an annuity provider for a 401(k) plan. However, according to industry stakeholders GAO interviewed, those steps are not often used because they include assessing “sufficient” information to “appropriately” conclude that the annuity provider will be financially able to pay future claims without definitions for those terms. Without clearer criteria to select an annuity provider, fear of liability may deter plan sponsors from offering annuities.

Further, GAO found that a mix of lifetime income options to choose from is not usually available. DOL provides an incentive in the form of limited liability relief to plan sponsors who, among other things, provide participants at least three diversified investment options. However, no such incentive exists for plan sponsors offering a mix of lifetime income options. Without some degree of liability relief, plan sponsors may be reluctant to offer a diverse mix of lifetime income options to their participants. Lastly, stakeholders told GAO that record keepers may make only their own annuities available to the plans they service. DOL provides guidance on selecting service providers, but it does not encourage plan sponsors to seek choices from their service providers, which may prevent plans from having appropriate annuity options available to offer participants.

What GAO Recommends

GAO makes seven recommendations to DOL, including that it clarify the criteria to be used by plan sponsors to select an annuity provider, consider providing limited liability relief for offering an appropriate mix of lifetime income options, issue guidance to encourage plan sponsors to select a record keeper that offers annuities from other providers, and consider providing RMD-based default lifetime income to retirees.

1. Clarifying the safe harbor from liability for selecting an annuity provider by providing sufficiently detailed criteria to better enable plan sponsors to comply with the safe harbor requirements related to assessing a provider’s long-term solvency.

Industry associations and other stakeholders told us that concerns

Industry associations and other stakeholders told us that concerns

about legal liability are the primary barrier deterring plan sponsors from offering annuities to participants. Of the 54 plan sponsors responding to our survey, 39 did not offer an annuity, and 26 of them said their decision was influenced by the resources required to obtain liability relief. In 2008, DOL promulgated a “safe harbor” rule that sets out procedures 401(k) plan sponsors can follow to satisfy their fiduciary duties when selecting an annuity provider. To obtain fiduciary relief under the safe harbor rule, for example, plan sponsors must perform an analytical search for annuity providers and consider the provider’s ability to pay claims in the future, in addition to the costs and benefits of the annuity. According to the rule, plan sponsors and other fiduciaries following the safe harbor when selecting an annuity provider fulfill their fiduciary duty and should, therefore, not be subject to corporate or personal liability for that selection.

Stakeholders we interviewed indicated that the safe harbor for selecting an annuity provider is not helpful and the primary challenges stem from the requirements that plan sponsors appropriately:

- Consider information sufficient to assess the ability of the annuity provider to make all future payments under the annuity contract.

- Conclude that, at the time of the selection, the annuity provider is financially able to make all future payments under the annuity contract. Plan sponsors must also periodically review the appropriateness of the conclusion over time as the provider continues to issue annuity contracts.

To facilitate the availability of annuity options in 401(k) plans, the 2005 ERISA Advisory Council Working Group on Retirement Distributions and Options recommended DOL change sponsor responsibilities for selecting an annuity provider. The Pension Protection Act of 2006 (PPA), required DOL to promulgate regulations clarifying the fiduciary standards applicable to the selection of an annuity contract as a form of distribution for a DC plan. In 2007, in the preamble to the proposed safe harbor rule, developed in response to the PPA requirement, DOL stated that plan sponsors had frequently cited their fiduciary liability as a reason for not offering an annuity spend down option. However, by DOL’s own estimates, the safe harbor was unlikely to make plan sponsors substantially more willing to offer annuities because it estimated when it proposed the rule that the safe harbor would increase the share of participants offered an annuity by only 1 percentage point.

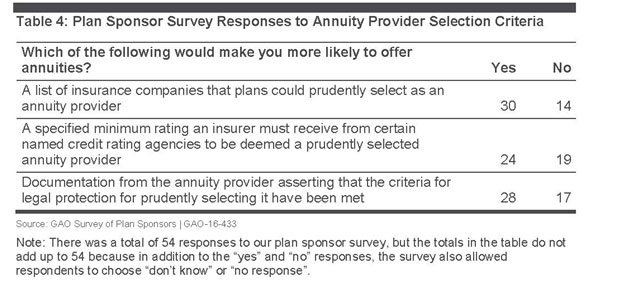

Assessing the future financial health of an insurer can be a difficult task for a plan sponsor, and many plan sponsors responding to our survey indicated they would be more likely to offer an annuity if the benefits of the safe harbor were more readily attainable. Members of Congress in both parties introduced legislation that would have, among other things, amended ERISA to permit plan sponsors and fiduciaries to rely more heavily on state regulators when selecting an annuity provider. Additionally, the Director of the Federal Insurance Office told us plan sponsors should not be expected to look at an insurer’s annual report to assess its financial liabilities or know more about an insurer than the research and metrics a rating agency or other entity might make publicly available. Officials we spoke with at the National Association of Insurance Commissioners (NAIC) also told us the safe harbor should have verifiable criteria. For example, the plan sponsors responding to our survey who did not offer annuities responded that any single criterion provided would make them more likely to offer them, as shown in table 4.

DOL is responsible for educating and assisting plan sponsors to help ensure the retirement security of workers and their families. However, the annuity selection safe harbor can only translate into increased retirement security if it is used, and it does not provide sufficiently detailed criteria that plan sponsors feel they can use to obtain the liability protection it offers. The safe harbor requires plan sponsors to consider “sufficient” information to “appropriately” reach a conclusion about the annuity provider’s future solvency without defining the terms “sufficient” and “appropriate.”

In 2010, a DOL official told us the agency was considering addressing industry concerns that plan sponsors have to second-guess state insurance regulators to assess insurers’ financial viability, and in 2014, DOL published information indicating that it would be developing proposed amendments to the safe harbor to provide plan fiduciaries with more certainty that they have discharged their obligations when contracting to provide an annuity option. DOL officials told us one advantage of revising the annuity selection safe harbor would be that it could provide greater clarity for plan sponsors and thus lead to more annuity options for participants. NAIC officials mentioned a standard proposed by an association of insurers, which would include, among other criteria, that the insurer be licensed in at least 26 states. RFI responses from two participant advocates suggested that annuity providers should also be licensed in states with strong regulatory protections. A DOL official told us that because the ERISA standard of prudence requires plan fiduciaries to exercise some degree of judgement in making the annuity provider selection, it precludes development of a simple and easily verifiable checklist. However, clarifying how to comply with the annuity selection safe harbor to the greatest extent possible may help encourage plan sponsors to offer plan participants an annuity option.

2. Considering providing legal relief for plan fiduciaries offering an appropriate mix of annuity and withdrawal options, upon adequately informing participants about the options, before participants choose to direct their investments into them.

According to researchers we spoke to, participants should have multiple lifetime income options because no one solution works for everyone. Treasury officials told us that participants can benefit by combining options to diversify their sources of lifetime income and help them manage multiple risks in retirement. For example, participants could use a portion of their savings to purchase an annuity and leave the balance invested in their plan for a withdrawal option.

A variety of products and services could be offered in the plan environment to provide participants with a mix of annuity and withdrawal options. For example, managed payout funds provide for automated withdrawals, and annuity providers offer a wide variety of guaranteed income options. Furthermore, plans can also offer participants access to an online annuity shopping platform, and with it, comparable information on multiple products from multiple providers.

However, there is no agency guidance available to help plan sponsors minimize their legal risks when offering participants a mix of annuity and withdrawal options within a plan. The current safe harbor for the selection of an annuity provider is available to plan sponsors only offering an annuity product from a single annuity provider. Based on our analysis, a plan sponsor could increase its risk of legal liability for each option it offers. For example, a plan sponsor that offers an in-plan annuity increases its risk by adding withdrawal options. Of the 12 plan sponsors responding to our survey who did not offer withdrawal options, 8 responded that the fiduciary responsibilities for managing participant assets in the draw-down phase influenced their decision.

The results of our record keeper questionnaire indicate that most plan sponsors are not offering a mix of lifetime income options. In contrast, plan sponsors are required to diversify the plan investments they offer. In addition, when 401(k) plans permit participants to exercise control over their investment choices and, among other things, offer participants a broad range of investment alternatives, plan sponsors or other fiduciaries are not liable for any losses that result solely from a participant’s exercise of that control.

DOL has not provided an incentive for plan sponsors to provide participants a mix of lifetime income options and information about them. EBSA’s mission is to assure the security of the retirement, health, and other workplace-related benefits of America’s workers and their families, and without lifetime income options in workplace 401(k) plans, those benefits may not remain secure throughout retirement. Accordingly, DOL is engaged in an initiative with Treasury to encourage plan sponsors to offer prudent lifetime income options. Currently, each additional lifetime income option plan sponsors offer potentially exposes them to additional legal risk, unless that option is an annuity selected in a process pursuant to the safe harbor for annuity selection.

DOL has not established a process plan sponsors can use to prudently select an appropriately diverse mix of annuity and withdrawal options offered to participants. Consequently, DOL has not determined the types of products—such as those on an online annuity shopping platform—that might appropriately be included in such a mix. DOL officials told us the decision to offer any lifetime income option is still a fiduciary one, and that even if they provided such relief, plan sponsors would still have some fiduciary responsibility associated with providing participants lifetime income. However, if plan sponsors and others are protected from liability when participants exercise control choosing among lifetime income options in a way comparable to how they are protected when participants exercise control in choosing investments to accumulate retirement savings, sponsors may be more likely to offer a mix of lifetime income options from which participants can choose in their plan.

3. Use a record keeper that includes annuities from multiple providers on their record keeping platform.

One of DOL’s roles is educating fiduciaries on how to carry out their responsibilities, which include selecting service providers. DOL’s guidance in its Meeting Your Fiduciary Responsibilities publication recommends that, to ensure a meaningful selection, plan fiduciaries should survey a number of potential service providers before hiring one, but the guidance does not specifically include or discuss consideration or adoption of annuities or lifetime income options. The guidance specifies that diversifying plan investments—which can include annuities—and paying only reasonable plan expenses for service providers and plan investments are among a sponsor’s fiduciary responsibilities.

DOL also underscores the importance of plan fiduciaries’ responsibility to compare potential providers’ services to appropriately assess their reasonableness. However, DOL’s guidance does not encourage plan fiduciaries to use a record keeper that supports products from competing providers. While factors like cost and business affiliation may prevent some record keepers from supporting a variety of products, DOL officials told us participants would benefit from their plans having the ability to access non-proprietary products along with proprietary products. We previously recommended that DOL provide guidance to plan sponsors that addresses, among other things, the importance of considering multiple providers when choosing a managed account provider, and the importance of requesting from record keepers a choice of more than one provider. By considering similar guidance encouraging plan sponsors to use a record keeper that supports competing annuity product providers on its platform, plan sponsors could be more likely to find options that serve their participants and adopt them.

4. Offer participants the option to partially annuitize their account balance by allowing them the ability to purchase the amount of guaranteed lifetime income most appropriate for them.

Industry stakeholders and Treasury officials indicated that many plans lack partial annuitization options, which means many participants who have access to an annuity option through their plan must either

Industry stakeholders and Treasury officials indicated that many plans lack partial annuitization options, which means many participants who have access to an annuity option through their plan must either

annuitize their entire account balance or none of it. Agency officials and industry stakeholders have said that allowing participants to partially annuitize their account balance helps participants to combine multiple lifetime income options and purchase only the amount of annuity that they need.

Partial annuitization also allows participants to purchase an amount of annuity that makes sense for their situation in consideration of not only their plan savings but also income sources outside the plan, such as from Social Security or the resources of a spouse. Research has also shown that when offered, partial annuitization increases both the percentage of people who annuitize and the average percentage of balances that are annuitized. An industry stakeholder noted the increase in the purchase of annuities through the Federal Thrift Savings Plan (TSP) after partial annuitization was introduced. When the TSP began in 1986, the annuity option was an “all or nothing” choice. In 2004, TSP amended the plan to include partial annuitization and saw an increased use of annuities. For example, although the take up of TSP annuities in general remains low, more participants annuitized after TSP introduced partial annuitization. According to the insurer that has been the exclusive annuity provider to the TSP since its inception, 784 annuities were purchased in 2003. From 2004 to 2008, after partial annuitization was implemented, the number of annuity purchases—including partial or full annuitization—increased to an average of 1,645 per year, a 110 percent increase in the number of participants annuitizing at least a portion of their account balances. In addition, the insurer noted that the average purchase amount of annuities increased 60 percent from $66,000 to $106,000.

Treasury noted one of its goals is to make it easier for plans to offer participants a combination of retirement income options that avoid an all-or-nothing choice. However, 401(k) plans are not required to offer partial annuitization and our interviews with industry stakeholders and agency officials indicate that plan sponsors are not incentivized to offer partial annuitization and may not be aware of the benefits to participants. Recent collaborations by Treasury and DOL have tried to encourage plans to allow participants the ability to combine multiple options to receive their retirement benefits. For example, the actions taken by Treasury approving the use of QLACs and by DOL facilitating the use of deferred annuity contracts embedded within a target date fund have made it easier for plans to offer partial annuitization options. However, partial annuitization is not encouraged broadly through general guidance applicable to all 401(k) plans, such as DOL’s Meeting Your Fiduciary Responsibilities publication. Agency officials have told us that many plans continue to frame annuity purchases as an “all-or-nothing” choice even though one Treasury official said that there is nothing prohibiting plans from offering partial annuitization. With DOL guidance encouraging plans to allow partial annuitization and enabling their participants to purchase the amount of annuity that they need, participants will be able to make annuity purchases that are most appropriate for their individual circumstances and support their lifetime income needs.

5. Consider whether a contract with a service provider ensures future service provider changes do not cause participants to lose the value of their lifetime income guarantees.

Another deterrent to plan sponsors offering annuities, according to representatives of annuity providers, is the possibility of plan participants having to lose lifetime income guarantees when the plan sponsor changes service providers. To serve the best interests of participants, plan sponsors may at times be required to change service providers, including annuity providers and record keepers. Plan sponsors have a legal obligation to establish and follow a formal review process at reasonable intervals to decide whether to continue to use a service provider or look for replacements. However, lifetime guarantees—insurance policies offering lifetime income—can be difficult to transfer.

When participants contribute over time to a guaranteed lifetime income product such as a deferred income annuity or a GMWB, they are purchasing both an investment product and a guarantee of lifetime income. Purchasing an annuity in small amounts over time can have certain advantages, such as managing interest rate risk. When the plan sponsor changes record keepers or annuity providers, the investment will transfer, but the lifetime income guarantee may not. Some products might charge a guarantee fee of 1 percent or more every year and, as such, there is the potential for participants to have committed substantial resources to the guarantee before losing it due to a service provider change.

Representatives of one service provider told us that in general it is difficult to transfer annuities among annuity providers because it is difficult for providers to absorb the risk of another provider’s insurance products. For a product with a lifetime income guarantee to transfer from one record keeper to another, the new record keeper’s platform must either have the capacity to support the annuity product, or use third party software to allow a link to product information on the platform. Representatives of one annuity provider told us that given the complexities in effectively managing such a situation and the confusion about whether those efforts would be successful, many plan sponsors may be reluctant to offer annuities.

According to examples provided by industry officials, options needed to protect participants already exist, whether by refunding, preserving, or transferring their lifetime income guarantees, and some annuity providers and record keepers have taken steps to preserve participant benefits when plans change record keepers or annuity providers. For example, an association of defined contribution plans’ record keepers has developed common data standards for tracking annuity products, which are intended to simplify the transfer of annuity data among record keepers. In another example, one annuity provider representative offers participants a refund of fees if they lose their lifetime income guarantee, returning to them some value that could replace the lost lifetime income. Further, another annuity provider representative told us his company paid the lifetime income guaranteed by another annuity provider’s product, effectively transferring the annuities from provider to provider. An additional approach to preserving such benefits would be to allow participants to roll over their 401(k) plan annuity into an IRA version of the annuity provider’s product in the retail market if it would otherwise be lost. However, such distributions would move some 401(k) plan benefits while leaving others, increasing the likelihood of participants having to manage benefits in multiple places, which we previously reported can be challenging for participants.

DOL has not issued guidance encouraging plan sponsors to consider whether a service provider contract ensures future service provider changes do not cause participants to lose the value of lifetime income guarantees. While options to prevent lifetime income guarantee loses may exist, it is not clear how widespread they are in practice. However, by following such guidance from DOL, plan sponsors could make such options more widespread by requesting them, and they may be more willing to allow participants to accumulate in plan annuities in the future, if they are confident that a service provider change will not amount to a benefit reduction for participants.

6. Include participant access to advice on the plan’s lifetime income options from an expert in retirement income strategies.

Participants we surveyed in coordination with a research organization cited obtaining advice as a key step in selecting lifetime income options offered by a 401(k) plan. We asked participants to check all the steps they would take to assess what lifetime income options are right for them, and almost 50 percent of respondents reported they would seek advice. Our surveys also found that participants preferred to obtain financial advice through their plans as opposed to other sources. We asked participants to select from a list the types of individuals they would consult in selecting among a plan’s lifetime income options. Fifty-nine percent of respondents selected a financial adviser provided by the plan. In comparison, fewer than 40 percent of respondents selected a tax professional or lawyer (39 percent) or a financial advisor outside of a plan (about 36 percent).

Despite broad recognition of the need for participants to consult an adviser on lifetime income options before they make any decisions, industry research indicates only a minority of plan sponsors make advisers available to plan participants. In a 2013 survey of more than 600 plan sponsors, less than one-third reported offering access to any kind of advice to participants.80 One industry stakeholder told us plan sponsors are reluctant to provide access to investment advice, in part because of concerns about the costs. One survey reported this is true even though participants can get advice on withdrawal options through their plan for less than half the cost they would pay on their own. Lawyers representing 401(k) plans told us they counsel their clients against providing access to advice because of legal liability.

DOL officials told us it was a good idea to encourage sponsors to offer participants access to investment advisers in-plan, though sponsors should diligently vet prospective advisers before they are allowed to make open presentations to participants. However, in DOL’s publication Meeting Your Fiduciary Responsibilities, plan fiduciaries are not encouraged to provide access to an investment adviser knowledgeable about lifetime income strategies. Despite the absence of such guidance, some plan sponsors have already ensured that their participants have the chance to speak with an investment adviser about their plans’ annuities and withdrawal options, enabling participants to talk to professionals before they leave their plan or make a decision that can jeopardize their retirement security. Without guidance about the importance of providing their participants access to an adviser at the point of retirement to discuss in-plan lifetime income options, plan sponsors may continue to not offer such a service.

7. Consider providing RMD-based default income–plan distributions as a default stream of lifetime income based on the RMD methodology–beginning, unless they opt-out, when retirement-age participants separate from employment, rather than after age 70 ½.

One option already in place that can provide a default for participants in 401(k) plans is the provision of required minimum distributions (RMD). A plan can be disqualified under the Internal Revenue Code if they do not follow the RMD provisions. Under these provisions, participants are required to begin receiving at least minimum payments starting after the participant retires and reaches the age of 70 ½. RMD calculations based on life expectancy provide lifetime income by design. Some plan sponsors are willing to administer RMDs as lifetime income by providing the minimum distribution to the participant in the plan rather than requiring participants to take a lump sum. As a result, participants who do not proactively commit to a lifetime income strategy may still get lifetime income through a plan that complies with RMD provisions by making distributions on the regulated minimum schedule. Default income based on RMD provisions can also begin when a participant retires and is in need of income, even though a distribution is generally not required until after the participant turns 70 1/2. For example, the Thrift Savings Plan (TSP) for federal employees offers a series of monthly payments computed by the TSP based on IRS life expectancy tables.

Conclusion

DOL can take action to address fiduciary barriers that deter plan sponsors from offering lifetime income options to participants. First, most plan sponsors are unlikely to be equipped to judge the long-term viability of an insurer, yet they currently must do so under the existing safe harbor. Providing clearer criteria for making this determination likely would encourage more sponsors to seek fiduciary relief for offering annuities. Second, DOL offers fiduciary relief when savings are accumulated in an appropriate mix of investments, but it offers no such relief for plans offering a mix of lifetime income options. Extending this relief to plan sponsors could encourage more plans to make a mix of options available and, therefore, allow participants to create a better retirement strategy by selecting and combining annuity and withdrawal options.

DOL can also provide additional guidance, in its Meeting Your Fiduciary Responsibilities publication or elsewhere, for fiduciaries as they consider how their participants’ account balance will translate into retirement income. DOL guidance can encourage plan sponsors to use a record keeper that includes annuities from other providers on its record keeping platform and increase the likelihood the plan sponsor will have access to annuities that the plan sponsor considers to be in the best interest of the plan participants. DOL guidance can encourage fiduciaries to offer participants the option to partially annuitize their account balance, allowing participants to purchase the amount of guaranteed lifetime income most appropriate for them.

DOL guidance can also help plan sponsors plan for future service provider changes when offering an annuity. The fear of causing participants to lose annuity guarantees due to a service provider switch may cause plan sponsors to stay in a less than ideal service provider relationship or not offer an annuity. Guidance can encourage plan fiduciaries to consider whether a lifetime income contract could cause participants to lose lifetime income guarantees under such a circumstance before entering into the contract.

DOL guidance can also encourage plan sponsors to provide an expert in retirement income strategies for participants to talk to about the plan’s distribution options. Enabling participants to receive advice about in-plan lifetime income options given their individual circumstances will better ensure they make retirement income decisions that can be directly applied to their specific circumstances.

Lastly, DOL can encourage participants who have not chosen a lifetime income option at retirement toward income security with defaults. These participants may be less likely to take advantage of advice when offered. RMD-based default income can stretch out the account balances of these participants throughout retirement if sponsors and participants understand how they can be administered and used. Unless DOL encourages plan sponsors to consider providing RMD-based default income, many retirees who do not select a lifetime income option may continue to receive a single lump sum payout that may not be used for lifetime income.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

A copy of the full report can be found here.

For more information, contact Chuck Young, Managing Director, youngc1@gao.gov, (202) 512-4800 U.S. Government Accountability Office, 441 G Street NW, Room 7149 Washington, DC 20548

Endnote

i To better understand the adoption of lifetime income options in 401(k) plans, we administered a questionnaire to 11 401(k) plan record keepers that together accounted for approximately 42 percent of the 401(k) plan market as measured by plan assets, 46 percent as measured by participants, and 26 percent as measured by the number of plans, as of December 2014. To examine what barriers, if any, deter plan sponsors from offering lifetime income options, we conducted a non-generalizable online survey of plan sponsors through industry organizations such as PLANSPONSOR, the Plan Sponsor Council of America, the National Association of Plan Administrators and BenefitsLink. We reviewed relevant research; industry publications; and federal laws, regulations, and guidance on lifetime income options in 401(k) plans. We also interviewed industry stakeholders, researchers, and government officials—including officials from DOL’s Employee Benefits Security Administration (EBSA) as well as from the Department of the Treasury’s (Treasury) Office of Tax Policy, Federal Insurance Office, and Internal Revenue Service (IRS). We conducted this performance audit from July 2014 to August 2016 in accordance with generally accepted government auditing standards.