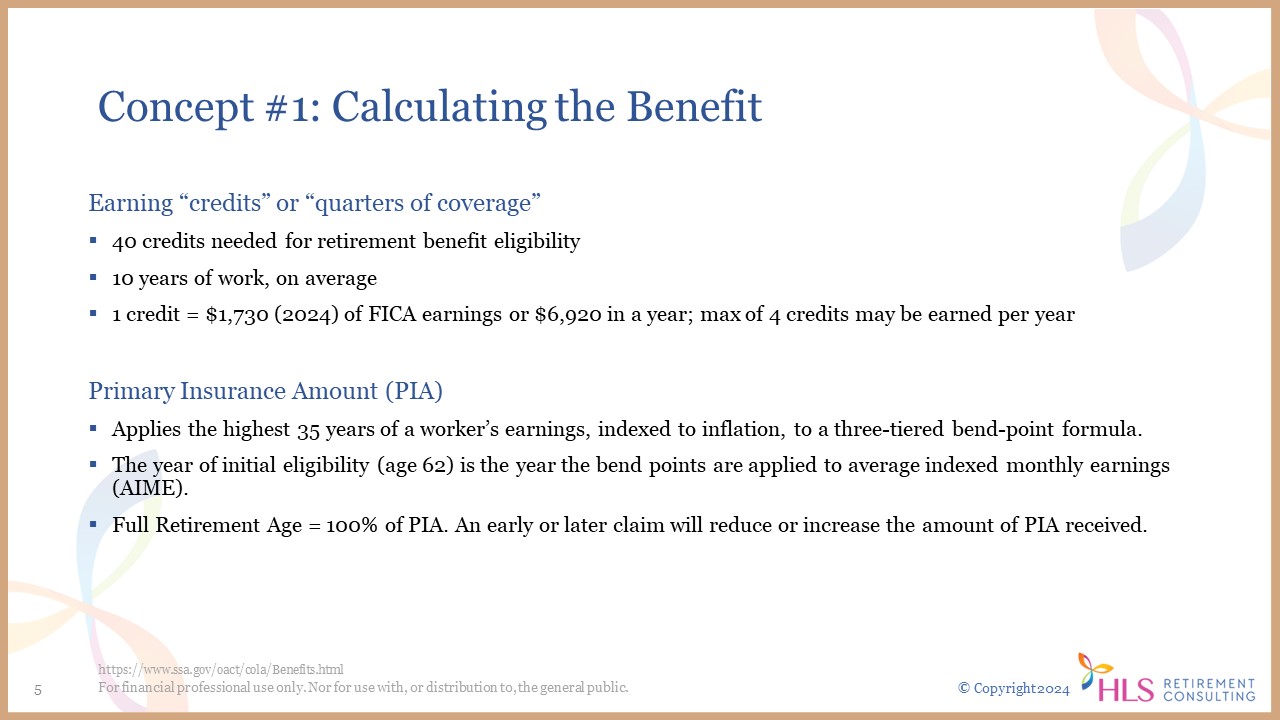

This year, one credit is $1,730. So, if you work throughout the year, you must earn $6,920 to earn four credits. You can earn them at the beginning of the year, and once you have earned your four credits, you have earned the maximum four for the year. You can stop counting once you have done this over the past ten years and earned 40 credits.

That leads us to a very significant term, which is called PIA, or Primary Insurance Amount. That is the basis on which your Social Security benefit revolves. You will see the term “Survivor PIA,” you will see PIA as it relates to retirement benefits, and you will even see PIA when we are talking about spousal or ex-spousal benefits because someone’s PIA is how a spouse or ex-spouse will benefit as calculated. You need your ten years on average, but the PIA is based upon your highest 35 years of earnings indexed for inflation, and it is based upon a three-tiered bend-point formula.

The bend-point formula is indexed to or based upon the year someone reaches initial eligibility or turns 62. Their highest 35 years of earnings as of the year they turn 60 are indexed, and then all years after that are taken at face value. If the Primary Insurance Amount is equivalent to what someone would collect at full retirement age, you get 100% of your Primary Insurance Amount.

Whether or not you collect that is based upon the timing of your claim. So, if you file early, it is reduced monthly. If you file later, as late as age 70, it is increased by delayed retirement credits. The PIA is an important number.

How do you calculate 100% of the benefit at full retirement age? You first look at someone’s entire earnings history under Social Security and adjust all of those numbers for inflation. Remember that age 60 and beyond are not adjusted.

A common question is, “Well, once I claim the benefit, do they still look at my earnings? Absolutely. If those most recent earnings continue, if it bumps out one what was counted for the highest 35, it will be used. So, every year someone earns something, Social Security will recalculate the PIA. Once those highest years have been selected and indexed, those are used in the recalculation of the PIA.

Now, what if someone has a zero in some of those years? Well, guess what? They do not just say, “Well, we will just use the 20 you have;” they will substitute zeros. This is where this becomes a valuable conversation. Zeros are added from missing years in that 35-year calculation.

Once you have 35 years, or if you do not, zeros are substituted for the highest 35 years where you had no earnings. You divide that by 420, the number of months in 35 years, and that becomes your average indexed monthly earnings.

You apply a bend-point formula to this. I do not want you to get into the weeds about the bend-point formula; know it is used when someone turns 62. I want you to focus on the ties. The first tier pays 90% of the income in that tier, the second tier pays 32%, and the third tier pays 15%.

I’m sure you’ve heard that Social Security is designed to replace a higher percentage of lower-wage earners’ income. For example, someone whose average indexed monthly earnings is $1,000 a month will get 90% of their pre-retirement earnings replaced, while someone who has higher earnings will have less replaced. Social Security is intended to replace about 30 to 40% of pre-retirement income.

Let’s say someone has an average annual income of around $24,000 throughout their career. Per the bend-point formula, Social Security will replace 65% of their earnings. For someone with an average monthly income of $10,250, Social Security will only replace 33% of their income. So, how do we take all of this mumbo-jumbo about the PIA and the bend-point formula and use it with clients?

Remember, zeros are substituted for any missing years in this calculation. So when clients want to know how to increase their Social Security because they might have been in and out of the workforce taking care of children or aging parents (the sandwich generation), tell them that even part-time work can increase their PIA. These are the honest conversations you have by understanding this. Encourage them to work at any level. Any level is going to be better than a zero.

Sometimes, a dependent spouse says, “It is not worth it for me to work, so I will just wait. I will get the spousal benefit, which can be as much as 50% of the higher earner’s PIA.” The problem with that is it can be a competing interest because now the rules have shifted, and I will get to that later, in that the higher wage earner has to file for benefits before the dependent spouse can file.

The higher wage earner should consider waiting longer so that it produces a higher cash flow while they are both alive and a higher cash flow for the survivor. However, for the dependent spouse to file, the higher wager must have filed. So, encourage a dependent spouse who might be either very low earning or shy of the credits needed to collect their independent retirement benefit to work enough to earn those credits. If they have earned at least some benefits, let them file and have the higher wage earner file later. So that is something to consider.

However, make sure they understand that for any year that they work, Social Security will be recalculated, and if that presents a higher PIA because that most recent year increased their PIA, they will see that benefit increase the following year. It takes a whole year to come into effect, but they will see it. People ask how accurate a Social Security statement’s benefit estimates are. First of all, they are in today’s dollars. Secondly, they are most accurate the closer you get to the benefit projection date. It is assumed that someone will earn the most recent year of earnings for the rest of their career until Social Security is informed otherwise.

Business owners generally report very low W-2 earnings. If they are an S corporation, they generally report lower W-2 earnings to avoid employment taxes. Then they come to you later and say, “Uh-oh, I barely have any Social Security.” So, you always want to be mindful of that, especially when they are in their 50s. If you discover they have negligible Social Security benefits, how can you test how much they should consider putting in to bolster that retirement benefit?

A little-known tool I recommend is the “Plan for Retirement Tool,” available through your online Social Security record. If you have a business owner who says, “Well, what if I report higher or lower earnings?” You can put all those scenarios into modeling potential benefits. So, if I just went in and said, “What if this person makes zero for the rest of their career, how does their benefit change?” “What if they make $75,000 or $50,000 a year?” Then, you can download the results.

This is a good way to test scenarios for business owners who want options. What if they say, “Well, how about if I shift income to my spouse, who also works for the business?” Or someone can say, “Well, what if I go to work full-time to earn my credits?” These are valuable ways to work with clients to help them see what different amounts of earnings will do for their benefit.

Concept #2: (Living) Spousal/Ex-Spousal Benefit Eligibility

Let’s now discuss spousal and ex-spousal benefit eligibility compared to survivor benefits, two things people need clarification on.

Often, people ask, “Can I file for spousal or ex-spousal benefits and let mine roll up?” That is called a restricted application. It rode off into the sunset on January 1, 2024.

Why? Because the people that were eligible for that had to have been born before January 2, 1954. Why? Because the Bipartisan Budget Act of 2015 gave that a shelf life until this year, those individuals had to have been born before January 1, ’54, and they all turned 70 by January 1 of this year. The flip side of that strategy was the file and suspend strategy. The file and suspend strategy has a very short shelf life. It expired on April 16, 2016, after the Bipartisan Budget Act came out in 2015.

These strategies allowed the higher wage earner at full retirement age to file and immediately suspend their benefit, allowing a dependent spouse or even dependent children to collect benefits during that suspension period while the higher wage earner was earning delayed retirement credits. That went out of the window in 2016, but people are still confused. So, the first thing to know is that the restricted application is no longer a thing. How are benefits payable now that these strategies are gone?

Since the file-and-suspend strategy is gone, the higher-earning spouse has to file, period, for the spouse to collect spousal benefits. For currently married spouses, that is the deal.

Now that the restricted application is gone, it is not that someone who has earned a retirement benefit can never collect a spousal benefit. Still, it means that everyone falls into a “deemed” filing category. If you file for a retirement or a spousal benefit, you are deemed to file for both simultaneously. To simplify, that means that if I am entitled to a Social Security retirement benefit, it will always be paid before an auxiliary benefit under my spouse’s or my ex-spouse’s record.

In other words, Social Security always wants to pay workers’ own benefits before they pay benefits under their spouse or ex-spouse. Makes sense. We are not talking about survivor benefits here (but will later on); we are only talking about living. Social Security will compare the two benefits and say, “Okay, you have a retirement benefit, but this produces a higher benefit under your spouse, so we are going to go ahead and pay you the spousal excess on top of your benefit.”

What is the maximum spousal benefit? For a living spouse or ex-spouse, it is 50% of the higher wage earner’s PIA. Remember that the PIA is the crux of everything. That is 100% of the benefit at full retirement age. That is what you need to know. So, you need to know the full retirement age benefit of the higher wage earner. You take half of that. That is the maximum amount a spouse or ex-spouse can get, so you should compare that with their own full retirement age benefit. So, it is reduced if the dependent spouse takes the benefit before their full retirement age. People get confused by that.

People ask, “Well, what if the higher wage earner takes it at 70? Is it 50% of that?” I hope you’re saying, “No, it is not 50% of that.” Or “What if the higher wage earner files at 62? Is it 50% of that? No, it isn’t. It is always 50% of the higher wager’s primary insurance amount. Whether or not the dependent spouse gets that much depends on when the dependent spouse files for it. The reduction always follows the claimant, regardless of whether it is their own or a dependent benefit. There is a big difference; if you can get that, you are light years ahead of many people because it is confusing.

What is the required length of marriage to receive benefits on the higher earner’s record? Currently married spouses have to be married for one year for spousal benefits to be considered for living spousal benefits. For survivors, it is nine months.

If divorced, you must have been married for at least ten years to access living and survivor benefits. In the case of living ex-spousal benefits, you also have to be unmarried. So, you could have been married in between, but you have to be unmarried to be eligible for living ex-spousal benefits while your ex is alive. So, you could have gotten married, but if you get divorced again, you can claim those benefits again if the benefit is higher than your own retirement benefit.

The other slightly different requirement for ex-spousal benefits is if the ex-spouse still needs to file for benefits. However, there is still potentially a way to get ex-spousal benefits, which is called an “independently entitled ex-spouse.”

That means I do not have to go knocking on my ex’s door to find out if they filed if I know that the divorce occurred two years before my claim and my ex is at least 62. That way, without finding out if they have filed, I can say, “Well, I know those things to be the case, so then I can still file for an ex-spousal benefit.” Again, provided that it is more significant than any benefit I may have earned under my own record.

So, let us look at an example so that you get this deemed filing thing under your belt. Say Seth has a PIA of $3,600, and wife June has a PIA of $2,000. So, the maximum spousal benefit under Seth’s record is 50% of $3,600. That is pretty simple. June will forfeit the spousal benefit. Why is that? Because the spousal benefit of $1,800 is less than her benefit of $2,000, so in no circumstance will she collect a spousal benefit because her own PIA is greater than half of Seth’s. But what if Seth waits until age 70 to file and collects $4,464? Can June collect 50% of that amount, or $2,232?

June’s benefit is capped at 50% of his PIA. So, the fact that Seth waits until 70 to file does not give her 50% of that. However, it does give her the right to inherit it. If he dies before her, then she does benefit from him waiting until 70 to file, and that is why the claiming age decision of the higher earner is incredibly important. So, inherit it at death, but not during lifetime.

Let us look at another one. Susan is 65, has a PIA of $3,300, and is waiting until 70 to file. Husband Jake just reached his full retirement age with a PIA of $1,000. So, we know that the maximum spousal benefit is 50% of Susan’s PIA, or $1,650. We know in this case that Jake’s PIA is less than the spousal benefit, so we know there is an opportunity here for him to collect a spousal benefit. So, if he files now, what is he entitled to collect?

I hope you are thinking, “Well, because Susan has not filed yet, he is only entitled to his benefit of $1,000.” But a few years from now, he will get a spousal boost or spousal excess when she files for her benefit. So, he will continue to receive his $1,000, and then he will get the additional $650 when Susan files for her benefit, representing the sum of the two that is bringing him to the greater spousal benefit amount. Remember, she has to file for her benefit before he is entitled to that extra amount.

Concept #3: The Annual Earnings Test

Help your clients avoid withheld benefits or overpayments by asking one simple question. Every time you deal with someone who says, “Well, I am considering filing before I reach full retirement age.” Your very first question should be, “Are you working?” because right now, Social Security, if you have read anything in the media, has a massive overpayment problem to the tune of $23 billion outstanding in overpayments, a lot of which is based on applicant’s, or recipient’s or beneficiary’s changes in their income.

They do not know what they do not know, so they file for benefits. They either do not report that they are working, or their circumstances change while claiming benefits early, and they need to tell Social Security. Then it catches up with them. The IRS communicates with Social Security and then they are in overpayment status. It is not fun. So, you want to make sure you ask if they are working, and if so, you need to ask them how much they are making.

Every year, the limitation on earned income changes. You only need to be concerned about this until they reach full retirement age, at which time in the month that they reach full retirement age. Let’s say someone is working and also collecting Social Security and is under full retirement age for the entire year. The 2024 earnings limit is $22,320. Let’s say they exceed the earnings limit by $10,000. Social Security divides that excess by two and then divides their monthly payment into the excess amount. Social Security will then say, “We will not pay you benefits for x months until the excess is paid back.” That is if they hear about it beforehand. If they do not hear about it, they will return to you later and say, “Well, it took us two years to find you. We have paid you ten months of excess benefits, so now you owe us $20,000.” So, you want to be very careful about that.

Once someone hits the year they are going to reach full retirement age, they have a higher earnings limit, and they only have to worry about it from January until the month of their birthday. The earnings limit for the year you reach full retirement age is $59,520 in 2024, and then the excess withholding is only a third of the excess. Remember, starting the month you reach full retirement, and beyond, we do not have to worry about this.

A common question I get is, “What earnings count?” It is only the applicant’s earned income; it is not the spouse’s earned income. You do not have to worry about pension income, IRA income, rental income, or dividends. W-2 income, self-employment income, and benefits are withheld up front. They need to understand that when they go into this. Now, it is not that the benefits are lost. Once they reach full retirement age, if they have had benefits withheld, the benefits are restored in the manner of taking those missed months and recalculating their benefit as if they had applied for benefits that many months later.

If someone had missed out on ten months of benefits over time, at full retirement age, their benefit would be recalculated as if they had claimed ten months later. They do not get a lump sum back; they get it added to their benefit in a monthly way at full retirement age as if they had claimed ten months later. If Social Security is not informed of the excess earnings, they will come looking for you and present an overpayment notice, which is not fun. I have worked with many clients who have gotten them, unsuspecting people who needed help understanding, and it can be an overpayment for many reasons. It is usually an earnings problem. It could be that they had a non-covered pension and received benefits they should not, but often it is an earning issue.

Always ask about working when people are claiming benefits or considering claiming benefits before full retirement age. Some say, “Well, I have made $100,000 this year. I am going to retire in September. Does that mean Social Security will not let me file until the following year?” That is not the case. A special rule exists called the monthly earnings test for situations like this.

Social Security will say, “Okay, if you plan on retiring mid-year, then we will disregard all of your earnings from January through August if you are going to retire in September. You can get your full monthly benefit in September, provided you do not earn more than the monthly equivalent of the annual number for the rest of the year.” So, if the 2024 earnings limit is $22,320, you divide that by 12 for a monthly amount of $1,860, and you cannot earn more than that per month for the rest of the year.

Any benefits due to excess earnings are withheld in the first months of the year. For example, Jim is 64 and expects to earn $35,000 in 2024. If he files for benefits now, he will get a permanently reduced benefit because he is filing at 64, but he has $12,680 of excess income over the $22,320. When we divide that by two, he received $6,340 of excess benefits, which he is not entitled to because of his excess income.

So, Social Security will withhold the $6,340 excess in the following year’s first four months. They take that $6,340 and divide it by his monthly income benefit. Say it comes to 3.38 months. They rounded it up so they would not have to pay him for four months, and his Social Security benefits would start again in month five. Every year, he needs to report to them what he thinks his earnings will be so that they do it proactively instead of reactively. You do not want your clients to get overpayment notices. The other thing is that if someone relies on Social Security for a steady income stream, it is not a good idea because they will not get benefits for part of the year.

As said earlier, benefits previously withheld will be repaid at full retirement age. Even if the filer is under the earnings cap or retired and their spouse continues to work, you need to make them understand that “Yes, you are under the earnings cap, but if you have a spouse who is working, it is likely that you are going to pay taxes on a portion of your Social Security benefits.”

There are alternate ways to bridge income so we can avoid that, and because you are taking a permanent reduction in addition to the fact that taxes will probably take a bite out of it on some level, too. I did mention already that in the fiscal year 2023, there are $23 billion in outstanding overpayments, so this is a critical issue that you need to make sure that your clients are aware of when they are considering filing early.

Concept #4 – Widow(er) Benefit Eligibility and the Survivor Switch Technique

Let’s discuss widow and widower benefit eligibility and the survivor switch technique.

The earliest age at which retirement benefits are available for spousal and ex-spousal benefits is age 62.

A widow or widower collecting survivor benefits can remarry at age 60, so it does not prohibit a survivor benefit from being paid. That is important. When talking about ex-spousal living benefits, if that ex is collecting benefits under an ex’s record and gets remarried at any time, those benefits will stop. Still, survivor benefits will be payable to a surviving spouse or surviving ex-spouse of the deceased as long as that remarriage does not occur until age 60 or later.

I tell advisors they need to be mindful of the fact that age 60 is critical for the remarriage of widows and widowers. Why is that? Well, a survivor benefit can be as much as 100% of what the deceased was receiving, whereas a spousal benefit is capped at 50% of PIA. That is a big difference, and you need to be mindful of this in your planning and your discussions with them.

The age widow benefits are as much as 100% of what the deceased was collecting at the time of death or entitled to collect at the time of death, so the claiming age decision of the higher-earning spouse is critical to survivor cash flow. Suppose that higher wage earner waits until age 70 to collect their benefits. In that case, the lower-earning spouse, if they are the survivor, will benefit from that decision at death because the 24 to 32% in delayed retirement credits that the higher-earning spouse earned by waiting is inherited by that surviving spouse.

Now, I say as much as 100%. Benefits might be reduced by as much as 28½% % if the survivor files at 60. If they are eligible between 50 and 60 because of a disability, it is not reduced any further; it is only reduced by 28.5%.

How is it reduced? Remember, the survivor benefit, like every other benefit, is reduced based on when the claimant, in this case, the survivor, takes it. The benefit is always based on when the survivor takes it. What happens if the deceased dies before they ever claim a benefit? You will get different answers if you call Social Security. From experience, they are in dire straits and trying to train new people. They have a hiring freeze, and they have a bunch of attrition. Make sure you are aware of this.

If they die before full retirement age and never claim, the survivor PIA is equivalent to their full retirement age as of the date of death. If they die after full retirement age but before 70—say they were planning on waiting, and they never got there, and they pass away—their survivor PIA is what their date of death benefit would have been had they claimed. So, the survivor benefits from the delayed retirement credits they earned or never had the opportunity to claim.

What is the survivor switch technique? This is something that Social Security usually will never tell a widow or widower who comes into file for survivor benefits. (You cannot file for survivor entries online, by the way. You must either make a phone appointment or go into the office.) The survivor switch technique is for an individual entitled to both a survivor benefit and a retirement benefit. They do have a choice. They can choose to file for the lower benefit first and switch to the higher benefit later, regardless of their age. It is essentially a restricted application strategy that they can do at any age.

For example, I could be a survivor and say, “Well, I am going to take the widow’s benefit at age 60 and hold out and take my retirement benefit at age 70 since my retirement benefit can continue to increase.” Social Security generally does not inform a widow or widower that they can do this. They essentially deem the person without the person even knowing. (See this link to this information on the Social Security website.)

Let’s look at an example. Mary turned 66 in February. Her husband Ryan passed recently. At the time of his death, he was collecting $2,000 a month in Social Security benefits. Mary had not yet filed. Her full benefit at her full retirement age is $1,800. What are her options?

If you look at this at face value, his benefit is higher, so she could file in June, which would be her survivor’s full retirement age, and collect 100% of Ryan’s benefit. Social Security would say, “Well, Ryan’s benefit was higher than yours. In June, you have reached survivor full retirement age, so take his.” What that “just take his” means is that they have deemed her. They pay her own $1,800 full retirement age benefit plus the additional $200, and then she goes on her merry way, not knowing the difference.

What is her other option? She could have said, “No, I want to file for Ryan’s now. I want to hold my own application for my benefit out of the scope of this application because I know, without any cost-of-living adjustment, that if I do that and wait more or less four more years, my benefit will outpace it. So, I will take my benefit of $1,800 a month plus 40 months of delayed retirement credits at age 70, and it will be worth $2,280 a month.” These are the things your clients don’t know they are entitled to unless we advocate for them and educate them.

Here is another example. Edward is 62. He recently filed for his $ 1,610-a-month retirement benefit. His PIA was $2,300. Margaret, five years his senior and a physician (this is based on a real case), was collecting $3,200 at the time of her death. She was obviously the breadwinner in this situation. What are his options? If he went in right now, Social Security would say, “Well, you are going to lose your lower benefit, but hers is higher, so you can go ahead and file. We will file now, but you are under your full retirement age. You are only 62, so you will continue to collect your $1,610, but we will pay you the reduced amount of the survivor benefit, which is $755, for a total of $2,365.”

Or he could do nothing. This is an option. If he is properly advised and says, “Well, can I wait until I reach my full retirement age and take 100% of her $3,200 for the rest of my life?” That is an option, too. He is not forced to take it right when she dies. The only time he is forced to do that is if he is already a dependent spouse.

If he were taking a dependent spousal benefit, then yes, Social Security automatically switches him. But if he is not, he does not have to do it right away. So, if there is another way to bridge income between now and when he turns full retirement age, then absolutely do it because by waiting, he can collect $3,200 for the rest of his life.

The point is that there are options that Social Security generally will not offer. They are not in the business of providing advice of any kind, so your client has to know their options before reaching out to Social Security.

Be aware that survivor benefits are subject to the annual earnings test if claimed prior to FRA. For some reason, people often think they are not, but they are. Even mother’s and father’s ben fits taken before full retirement age are subject to it. It is generally not advisable to collect Social Security benefits if some will be withheld, especially if someone is counting on those benefits for monthly income. However, this is the one time when I say, “Hey, take it while you can,” if the idea is to take survivor benefits for a finite period of time.

Say I am a widow at 62, or even 60, but I am earning not so much that it totally wipes out my ability to take a survivor benefit but let us say it does withhold benefits for a few months of the year. I say take it anyway. Why? Because I will only get it for, let us say, eight or ten years, depending on how old I am, before I switch to my retirement benefit. Take it because you are not going to get it for very long. Then remember, when you hit full retirement age, they will recalculate it, and you will get a little bit more until you reach age 70. So, take it. It is better than nothing.

Again, if the survivor benefit is taken before full retirement age, the benefit will be reduced because it is taken for a longer period of time. You always want to seek solutions to bridge income while the lower benefit is claimed. If they do that survivor switch thing, you must say, “Okay, we will hold out for a higher benefit.” So, think of solutions to bridge income to preserve the ability to do that. Some people may need help to do that, but if they can, always look for bridge solutions.

Remember, you want to compare the survivor benefit at full retirement age because it cannot increase. Once someone dies, that survivor’s PIA number is not going to increase. You want to compare the survivor benefit to their own benefit at age 70 because theirs can increase, but the survivor PIA will not after full retirement age. Which one is higher? That is the one you want to hold out to take. For the lower one, take it earlier.

Concept #5: Minimizing Taxes and IRMAA Surcharges

Many people are surprised to learn that they might have to pay taxes on a portion of their Social Security benefits, which were established as part of the 1983 Social Security amendments. These tiers have never been inflation-adjusted, so more people are pushed into a situation where their Social Security benefits are at least partially taxable.

The way to determine whether or not someone is subject to tax on a portion of their benefits is to take their Modified Adjusted Gross Income (modified means we are not counting the taxable portion of Social Security yet). So, MAGI plus half of their Social Security benefits for the household and dividing it by two, plus nontaxable interest such as tax-exempt interest, is what is called your combined or provisional income.

Once you know that figure, then you compare it to the threshold. So, if your client is a married couple and their MAGI comes to $32,000 or less, there is no tax hit for them. If their MAGI is somewhere between $32,000 and $44,000, then as much as 50% of their Social Security benefits are exposed to taxes. Now, this is not a cliff regime, but as much as 50% can be exposed, and if they are over $44,000 in income as a couple, as much as 85% is exposed to taxation.

Only so many retirement income sources do not hit the line of provisional income. According to Social Security, roughly 40% of income beneficiaries pay federal income tax. That number will continue to rise, especially as these numbers never change and as all of these proposals hit on how they will fix the insolvency issue. Unlike the earnings test, a spouse’s earnings and other income sources hit MAGI, such as pensions and your IRA distributions. All those things go into the taxation of benefits, unlike the earnings test, which only looks at earned income.

What are the sources of income that do not increase provisional income?

- If they can start putting money into a Roth, qualified Roth distributions do not hit the bottom line.

- Health savings accounts. I am a big advocate of health savings accounts. If they have a high-deductible healthcare plan, start max funding that thing early. It has a trifecta benefit: It comes in pre-tax, it grows tax-deferred, and monies can be withdrawn tax-free for qualified expenses. Since it comes out tax-free, do not use it while they are working; hold on to it to offset medical expenses in retirement.

- Loans from a cash-value life insurance policy come out tax-free.

- Qualified charitable distributions (QCD) from IRAs. If you do not know about them, you should know about them. When someone turns 70, you must start talking about QCDs because they become available at 70½. Up to $105,000 this year could be transferred directly to a qualifying charity. For each person who has an IRA—only IRAs at this point—and when they hit RMD age at 73, they can also use it to offset a portion or all of their RMD.

- Reverse mortgages are another way to access cash that is not taxed.

Minimizing IRMAA Surcharges

IRMAA is the Income-Related Monthly Adjustment Amount for Medicare premiums. Start being mindful of this when someone turns 63. Why? For those who enroll in Medicare, usually at age 65, their Medicare premiums are based upon their MAGI two years before at age 63. So, we have to make sure that any strategies we are using to diversify income from a tax standpoint are mindful of what that looks like at 63.

The MAGI situation with these IRMAA brackets is a cliff regime. For 2024, the standard monthly Medicare premium is $174.70, but if a married couple’s income tops a MAGI of $206,000, they are pushed into the next premium band, and they would instead pay $244.60 per month per person. When someone turns 63, ask, “Are you going to enroll at 65?”

So, if someone finds themselves in a higher premium band, know they will only feel the pain for 12 months. Are higher premiums for one year worth the reward of getting this into a more tax-efficient bucket?

There are exceptions for life-changing events like divorce, marriage, work stoppage, loss of income, and loss of income-producing property that can be appealed. They would have to file a form SS-44, submit it, and they will get a new determination. If it hits a married couple, they must fill out the form.

Social Security and Your Value Proposition

You do not need to be an expert to incorporate Social Security optimization services into your suite of services. I hope that these five things we covered here have given you enough to say, “Okay, now I understand why I need to know how the benefit is calculated.”

Have an educated conversation with clients about why it is important to substitute zeros during your highest 35 earnings years with at least something to increase benefits, why it might be beneficial for a lower-earning spouse to pump up their primary insurance amount by taking on some full-time work, or why the business owner might want to consider paying themselves a little bit more to boost their benefits long term. You need to understand the basics, and you need to understand how to convert that into meaningful conversation.

Remember, Social Security is experiencing a crisis of infinite proportions. There are many points of misinformation coming out of the local field offices and over the phone. It is frightening, and it concerns me because consumers need guidance. They need accurate guidance, and they need you. You are desperately needed.

I have read studies that say people are willing to leave their advisors if they are not willing or able to help them with their Social Security claiming decisions. Eighty-two percent of respondents want to talk to their financial professional about how to maximize benefits, and 78% want to discuss how to leverage other sources of income to delay filing. Seize this opportunity. Do not let it pass you up. Learn about Social Security.