Yield and How That Corresponds to Returns in The Future

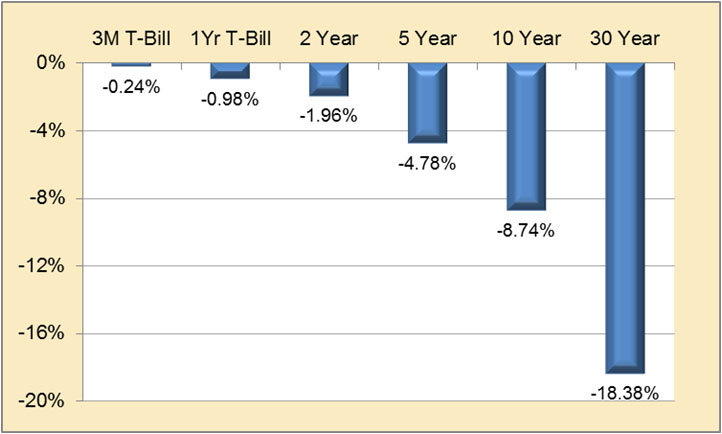

This chart is for a 1 percent instantaneous rise in interest rates broken out by maturity for three month Treasury bills, one year Treasury bills, all the way over to thirty year Treasury bills. What you see is that a 30 year bond can move quite a bit for movement in rates.

Estimated Losses for a 1% Rise in Rates

To give you an idea, from April to August of last year, longer term interest rates moved about 1 percent higher. This is just the loss on price. This doesn’t add back in the yield that you’re receiving. But the yields, obviously, are currently pretty low, so they’re not going to put a big dent in here.

The duration on a 30 year bond would be about 18 years, which means the price will move about 18 percent for a 1 percent rise in rates. Ironically, the lower general interest rates move, the higher the duration of the bonds, so the more susceptible they are to movements and interest rates. So at a time as we are in currently, we see durations on bonds as long as I’ve ever seen them in my career at the same time as interest rates are at the lowest point they’ve ever been in my career, sort of a double whammy.

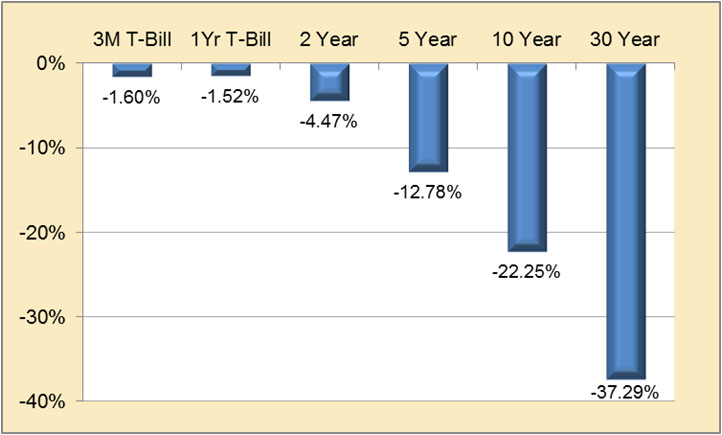

This is just straight math. We can run it through a bond calculator, put in moved yields 1 percent, and come up with an exact number. So estimated losses moving to 2004 rates the last time interest rates really backed off quite a bit. Can you see that 30 year number –negative 37 percent?

Estimated Losses Moving to 2004 Rates

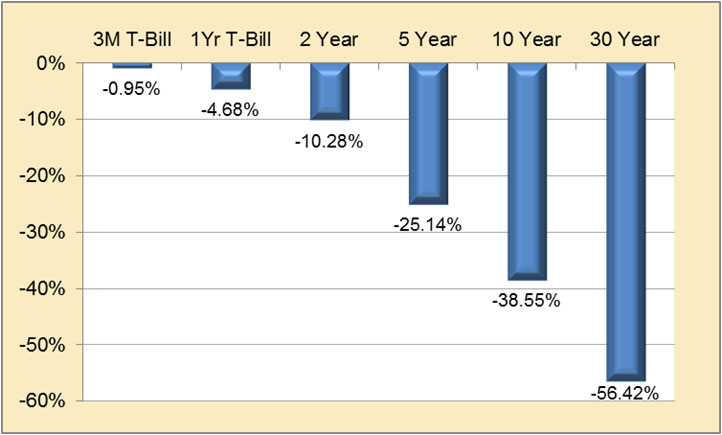

Again, this is an instantaneous change to give you an idea of how susceptible prices on bonds can be to movements and rates. In 1994, really, the last time we had a large movement in interest rates, interest rates rose a little over 3 percent with a -56 percent return on the 30 year Treasury.

Estimated Losses Moving to 1994 Rates

We get a lot of fixed income reports with a lot of doom and gloom, and people don’t want to hear about it. Fixed income still isn’t the best place to necessarily hide in this environment.

A Look Back in History

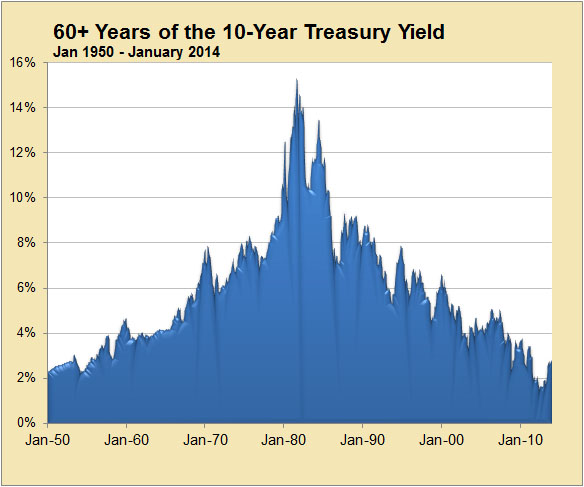

I think it’s good to go back in history to get an idea of where interest rates have gone over time. Below, we’re looking back over the last almost 65 years. You’ll notice from 1950 to 1981 or so for 31 years, interest rates basically moved right up.

Historical 10-Year Yields

Since that time, interest rates have basically fallen almost back to the levels that we saw back in 1950. You’ll notice that throughout the last 31 years or so, we’ve had areas where interest rates have fallen, moved back up, fallen, moved back up, and fallen, a little bit choppy.

But what it tells you the picture is is that times when rates were falling was when the economy was slowing. The Fed was able to lower interest rates to allow people to refinance their debt. Then as the economy took off, they raised rates back up. Again, towards the next recession, they took rates down again and so forth throughout the last 31 years. What you’ll notice is we have lower lows as they put interest rates lower each recession and lower highs as well as they didn’t raise interest rates up to the previous level. This has been a great environment not only for us but certainly for the Fed.

If they know that they can lower interest rates and the market knows that they can lower interest rates and that they will lower interest rates at the first sign of trouble, the market was able to see a lot of support behind itself without the Fed actually making a move. Even prior to their movements of cutting rates all before 2008, they had a pretty good control over the economy. Obviously, this is going to be more of a problem going forward when you don’t have as much room. Certainly, you don’t have any room currently. What we’ve noticed is from 1950 to 1981, recessions happen with much more frequency than they’ve happened over the last 31 years.

In fact, they happen every 4 years or so for that first 31 years, and they’ve happened every 7 or 8 years for the last 31. So we would anticipate that with the situation where interest rates are currently that the Fed is going to have a more difficult time keeping recessions from occurring. They should occur with more frequency.

How Well are Investors Compensated for Assuming Risk from Credit Instruments Today?

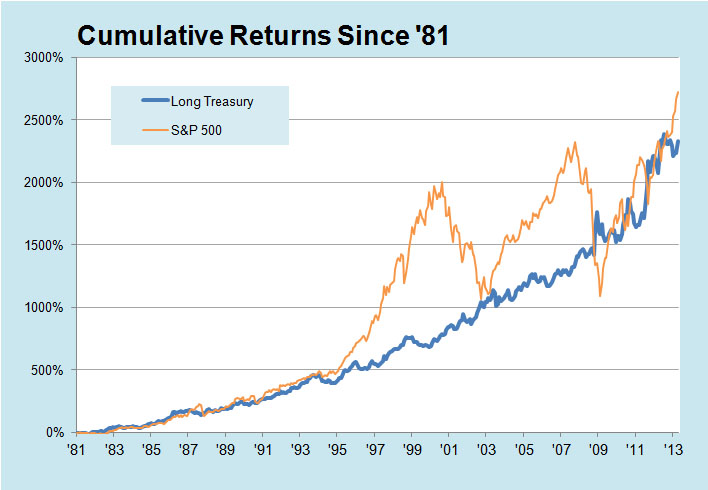

Here are the cumulative returns since 1981 just to give you an idea of how strong returns have been in the bond market because interest rates have fallen and the prices have gone up.

We ran long Treasuries for that time period. This is through the end of 2013. On average, long Treasuries, on an annualized basis, returned over 10 percent versus an S&P 500, which returned just shy of 11 percent, approximately the same returns. This cannot happen again. I’m not so sure about the stock market, but certainly to get 10 percent returns is impossible. Interest rates would have to fall negative and continue to move negative, and that’s not going to happen. So a lot of people’s asset allocation plans look at history. They’re looking at bonds. They’re looking and saying hey, I’m going back 30 years. But not necessarily a realistic time period to look at if you’re trying to extrapolate forward what you expect bond returns to be.

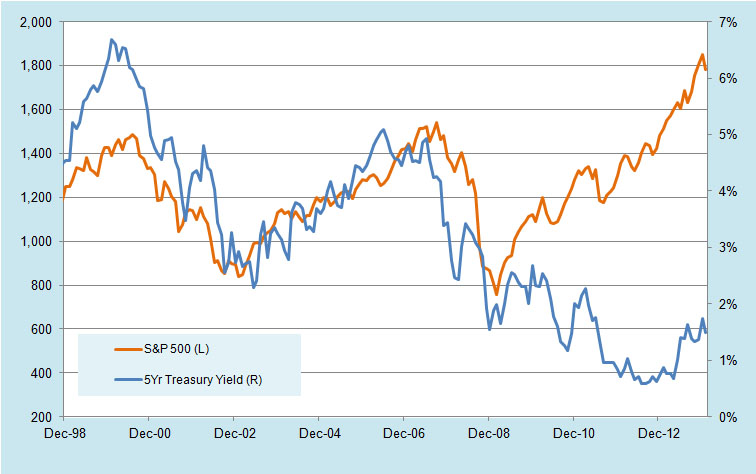

Something is not right with this picture. Typically Treasuries, Treasury yields and the S&P 500 tend to move in the same direction.

It makes sense that as the economy slows in ’06 through ’08, interest rates are falling at the same time the stock market is falling. Then as the economy recovered in 2009 forward, the stock market has really taken off, but interest rates have continued to fall. A rare occurrence. The Federal Reserve is certainly doing this on purpose to continue to add stimulus to this economy as much as they can.

But this division here has to bother them somewhat. So, something has to change. Either equity prices have to fall to justify where yields are, or yields need to start rising and probably fairly quickly when they do start to rise.

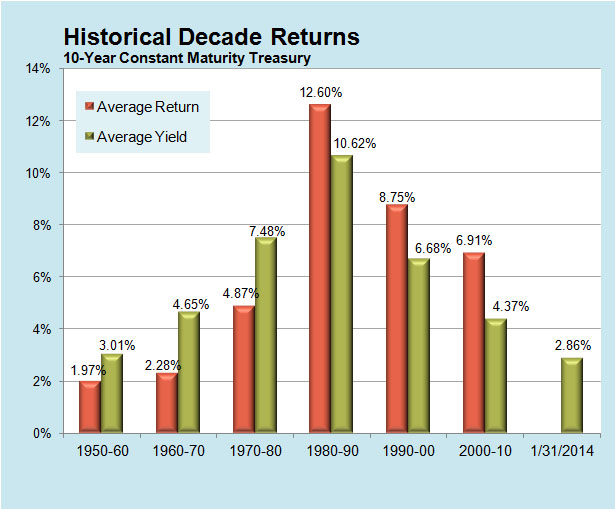

I thought it would make some sense to pull out some actual returns to give you an idea of the difference in returns given rising interest rates versus fallen interest rates. So this is strictly the 10 year Treasury over this time period. There are two bars for each ten year timeframe.

The orange bar is the average return for ten year Treasuries during that time period. The green bar is average yield. In the first 31 years you’ll notice that the yield is higher than average return. The reason for that is you’re going to get the yield on the bond less a little bit because there was a decline in the dollar price as interest rates rose. I highlight 1950 to 1970 because the average return there was just slightly over 2 percent, even though yields were averaging 3.75 or so versus current yield (as of January 31, 2014).

But even as of today, the 10 year is yielding about a 2.70%, yielding less than they did from 20 years from 1950 to 1970. We can anticipate the returns; we say returns are probably going to be around 2 percent to 3 percent over the next 5 to 10 years. This is a significant reason why. So again, compared to 1980 to 2010, the average return was higher than the average yield. Again, reflecting as interest rates fall, you get the yield plus a dollar return on the principal price and some pretty hefty numbers that people had gotten used to over that time period. Signs of what is to be done.

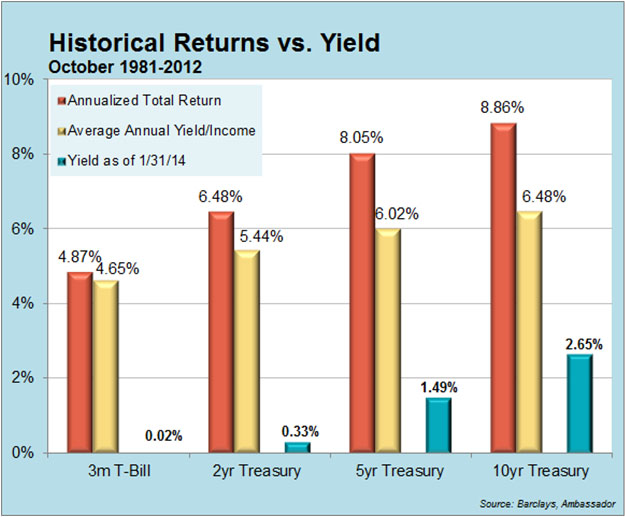

So we ran some similar ideas of what we just did, but breaking it out by shorter maturity Treasuries as well. Again, comparing 1981 thru 2012, and focusing on the total return versus the annual yield, the three month T bill price doesn’t move a lot because it’s so short in maturity. The yield and the return are pretty close to one another, then they separate and get higher as you get out into the longer maturities. Again – this is as of January 31, 2014 – what the current yields are to give you a comparison of how much lower they are relative to history.

What is the Fed’s Plan to Get Things Back on Track?

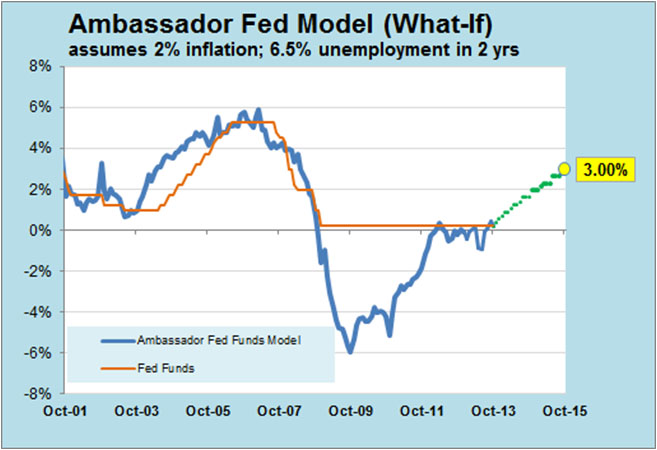

We run what we call our Ambassador Fed funds model and then run it relative to the Fed funds rate. The Fed funds rate is a short term cash rate, overnight borrowing rate for banks that the Federal Reserve really uses to control interest rates.

This is basically what the Fed is doing. They’ve tried to control inflation for the last 31 years. By getting that under control, they got the market to agree with the fact that the Fed had the economy under control. Now, they need to go after unemployment, a much bigger problem in this environment where the last three recessions, this one being the worst, where the recoveries have been very poor for employment. Each time that happens, it’s gotten worse and continues to be a major drag on this economy. So we think they’re looking at that side a little bit harder than inflation.

In fact, they wouldn’t mind to see a little higher inflation here. Inflation is a great help to an over-indebted economy, as well as over-indebted consumers. But when we’re talking about inflation, we’re talking about wage inflation, not food and gas and oil inflation. Those things hurt. They’re really watching wage inflation, and there are some reasons to believe why wage inflation could pick up here in the near term. But again, they’re not worried about that currently. They’re really concentrating on trying to get that unemployment rate down as much as they can.

A couple of comments about what the Fed is up against: They are hurting savers. They are hurting bond investors and people who are trying to find safety at the expense of trying to get this economy moving. They understand that, and they also know that they’re helping out higher risk products such as junk bonds and even the stock market. It bothers them that they feel strongly that that was needed to be done in order to keep this economy from really falling apart. We mentioned deflation, and that was the big concern in 2008, that inflation is a great help to an indebted people. Deflation is just the opposite, an absolute killer for an economy that is over indebted. So that’s why they’re keeping interest rates at zero. Until they see some really strong inflation, we anticipate that they’re going to keep rates low as long as they possibly can.

Ways to Protect Fixed Income Portfolios as We Go Forward

Maybe not over the next six months, but certainly sometime over the next two or three years, if we don’t take off, we’re certainly due for another downturn. Low rates cannot last forever. There are a number of reasons for that.

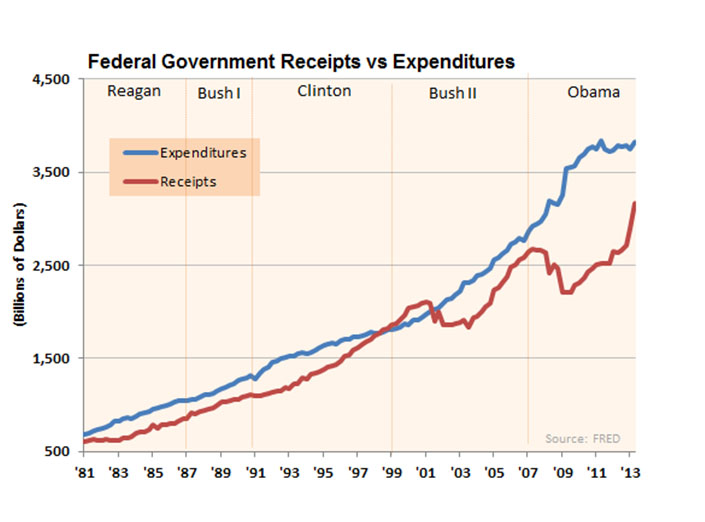

First and foremost is the budget deficit. The higher the deficit goes, the more we have to borrow, the more difficult it is to keep interest rates low. Back in the late ‘80s, we heard about bond market vigilantes that were pushing up interest rates during that time period.

So this is definitely a problem for not just the US government but governments throughout the world. Since I ran some numbers on expenditures and receipts, pretty easy numbers to pull up, and I ran it back to 1980 and split it out by president, not to make any political statement here, but just to show that really both sides are causing problems.

The biggest problem really started in 2000. We were on a similar trajectory back in ‘80s to the late ‘90s. In fact, receipts moved ahead of expenditures right in the early 2000s. We enjoyed a little bit of surplus. Receipts have stayed on the same sort of path.

In fact, they’ve picked up quite a bit here recently. They’ve stayed on a similar path all the way through that time period. Whereas expenditures really started to take off in 2000. So we’ve had both a Republican and a Democrat in office as expenditures have continued to soar. As much as people argue about that ’08 increase under the current administration, it’s actually come back down and back to that same trajectory. The problem here is that regardless of what we do, this is going to be tough to pull that expenditure level down primarily because of the aging of demographics in society and what we’ve promised.

We talked about the deficit. It’s ironic that one of our ̶ I don’t want to call them enemies ̶ but somebody who is not necessarily on our side, is the one that we sold the majority of our debt to. There are major reasons why China can’t just outright sell our bonds.

But certainly, if we do rattle their cage sometime in the future, I would expect to see a headline that says that the Chinese are stating that they might be looking into the fact of selling some of our Treasuries. They don’t even have to do anything. They just have to make a statement, and interest rates will back up. So that’s always something to keep in the back of your mind.

Interest rates can’t go much lower, so there’s only one way they can move up; and they’ve stayed here for almost four years now. It’s going to be tough to keep them down here for another four.

What you think you’re getting in protection, you might be better off being shorter on maturity overall. We think it’s going to trickle up inflation much more quickly. Rhe answer is to think differently. You can’t think about bonds the same way as you have for the last 31 years. It’s not just a yield plus a little bit. It’s going to be yield minus a little bit.

Current yield is a very good proxy of future returns. It’s going to be close. In fact, after about six years with yield on your bond today is about what you’re going to get. Six years forward give or take about a percent. So if somebody wants to know what do, you think you’re going to return to the bond market over the near future, you look at the current yield. The future of rising interest rates is bad for bonds.

The yield compensation for taking credit risk is at all-time lows. We think that’s a serious problem. We don’t understand why you’d try and grab a little extra yield with all that downside risk that’s attached to it. The Fed still does not know what to do and is certainly concerned. Shorter maturities will protect portfolios better than TIPS. There’s some great research out there on TIPS if you want to do some more on your own.