The other important age is 64½. We try to have a conversation with every single client when they’re 64½ because, at age 65, most people know that you have to do something with Medicare.

Parts A, B, C and D of Medicare

We don’t want to get too far into the specifics of Medicare because it all changes depending on which product you have, whether it’s Medigap or Medicare Advantage.

Medicare Part A covers people at the hospital and generally has no cost to enrollee. As long as you worked 40 quarters or ten years and paid your taxes, you don’t pay for Part A.

Medicare Part A does not cover long-term care expenses. Please talk to your clients and tell them Medicare is not going to solve their long-term care needs. It’s an excellent opportunity for you to bring up this topic. Many people have asked me, “Well, everything’s covered, right?” I have to say, “No, if you’re in a nursing home, you’re not going to get coverage through Medicare beyond a certain number of days.” Medicare not covering long-term care is a huge shock to many people.

Medicare Part B is for when you go to the doctor, have surgery, or have outpatient procedures. It’s pretty straightforward. Medicare pays for 80 percent of procedures, and the enrollees are responsible for the other 20 percent.

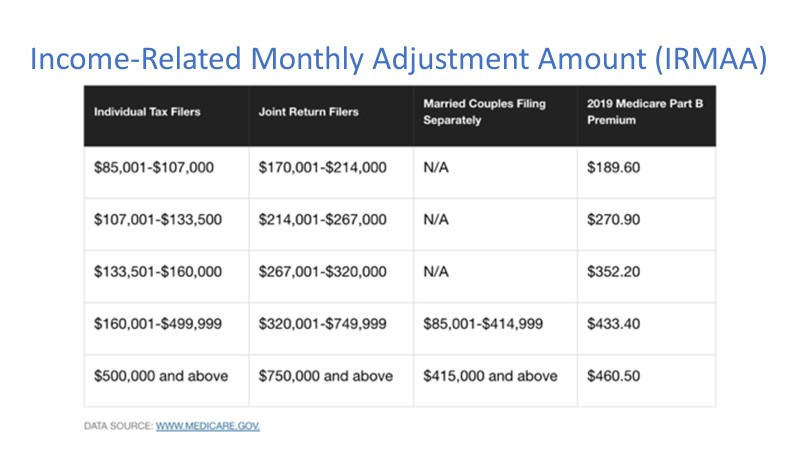

There are two IRMAA surcharges, one for Part B and one for Part D, which is drug coverage. Check out the charts below. You can see that for a client within a joint spousal household that is taking in $300,000 in modified adjusted gross income, their Medicare Part B is going to cost them $352 each per month versus the typical $135, so this is a big deal for many people. People that make more money get mad about this.

Examples of mental biases include:

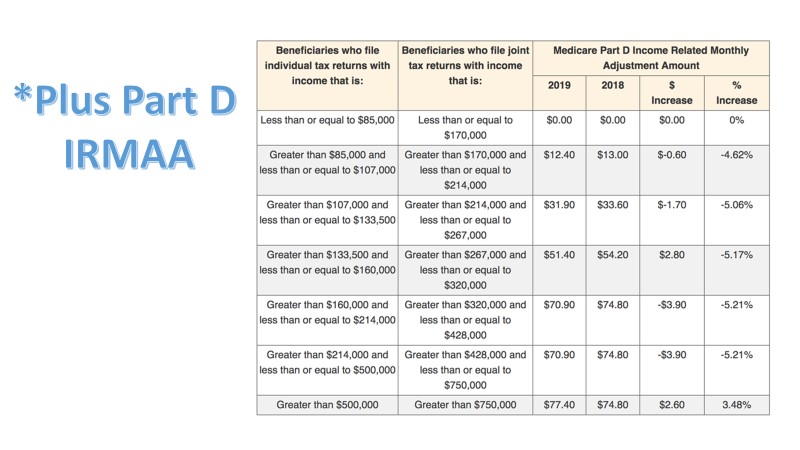

There are two different situations where IRMAA or modified adjusted gross income comes into play. Below you can see that for drug coverage, that same couple that’s making $300,000 would be paying an additional $51 for Medicare Part D.

Medicare Options

Everyone gets the “Medicare & You” handbook when they turn 65. It boils down to two choices. Clients can choose from Original Medicare where you pair Medicare with a drug plan and the Medigap plan, or they can choose a Medicare Advantage plan. There are still some employer-sponsored retiree coverages available today. However, for most people, Original Medicare and Medicare Advantage are going to be their options.

Medigap

Medigap is often called “Medicare supplement.” Private insurance companies are the ones that provide Medigap, so they simply pay secondary to Medicare. It’s something where if you have a Medigap policy, it’s great for people that travel – snowbirds – because you can go to any facility around the country, as long as they take Medicare.

These products are pretty straightforward. They’re just designed to pay what’s leftover from Medicare. So, if Medicare pays 80 percent, this plan will pay 20 percent, and your client walks out with no hospital bills when they have procedures done. You do have to have separate drug coverage with Part D. That is also by private insurance, and that pairs with Medigap.

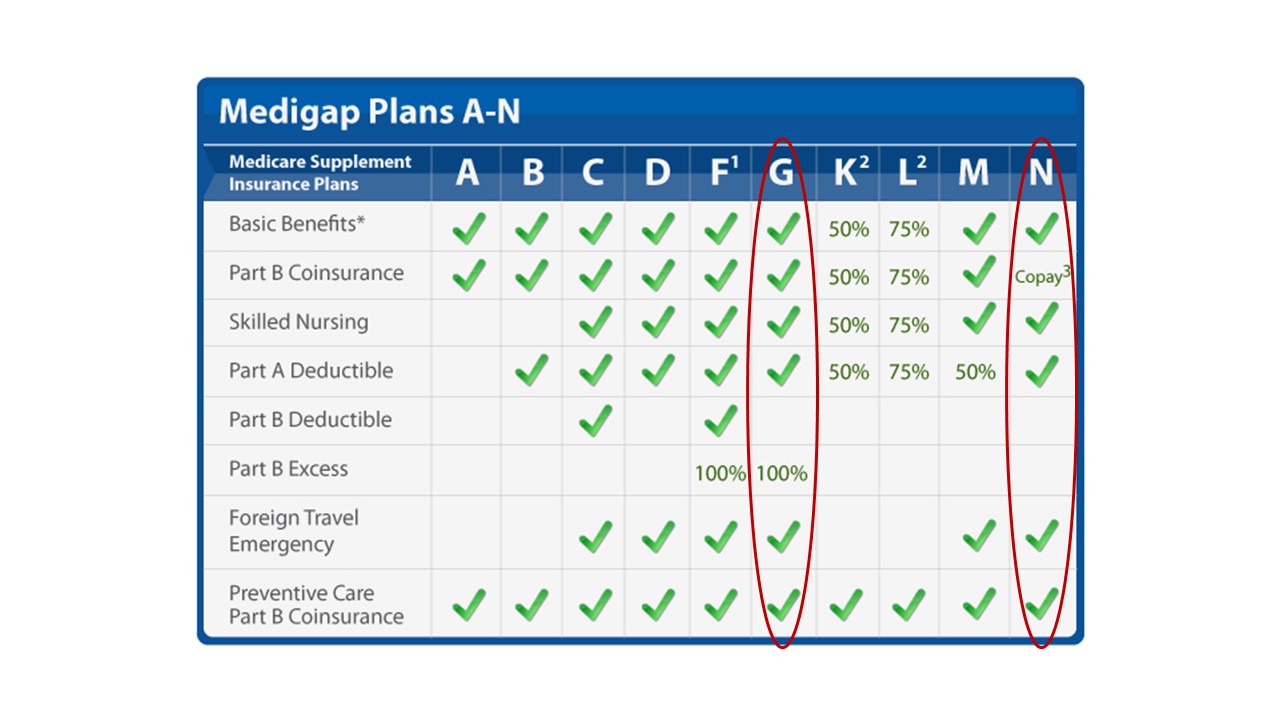

There are standardized plans with Medicare: A, B, all the way to N, and they’re all standardized, so if you have a Plan G with one company, like Blue Cross, it’s going to be the same as a Plan G with a company like Aetna, so it actually makes the comparison very easy. Again, Medigap pays after Medicare, so you have to find a facility that takes Medicare, and you’re good to go.

Here is a chart that we show that talks about the benefits of Medigap. Plan G and Plan N are the way to go when it comes to Medigap. If you have clients with any other plan, that should raise a red flag to at least look at their options.

Pros of Medigap plans

The biggest one is the freedom to choose doctors. There’s no network. Many times, people ask, “Do you take Blue Cross? Do you take United Healthcare?” With Medigap, it’s as simple as saying, “Do you take Medicare?”

You can go anywhere you want. You can go to the Mayo Clinic if you wish to receive specialty treatment. If you’re going to go to MD Anderson for your specific cancer, you can travel from Michigan down to Texas and get the care you need with no questions asked. So, that’s a huge one, especially for people who have a lot more saved in retirement and want to travel or just want the best care possible. Who doesn’t want the best care possible?

Also, going back to the best care, you get the best coverage. Your costs are going to be the lowest with Medigap as far as your out-of-pocket expenses go when you go to the doctor. You usually only spend up to $185 per year when you have medical procedures, and this makes budgeting easier. I always say Medigap is like leasing a car. You pay a little more upfront, but you know what’s coming as far as payments and as far as maintenance.

Medigap has guaranteed renewable contracts. As long as you pay your premium, you keep the plan. If you don’t want your doctors changing in and out of network, or you don’t want your benefits changing, you get a Medigap plan when you’re 65. You keep paying the premium until you’re 95, so that plan is not going to change for you. The price can go up, but the benefits are not going to change, so this is huge for people. The only way it can change is if your company goes out of business, which I’ve only seen happen once. It gives you security.

Medigap gives you more of an a la carte-style feel, and that means you can pick a drug plan that’s perfect for you to go with the best Medigap plan, so it’s not all a bundled package because your Medical needs might not fit your prescription needs. You may have many prescriptions and not go to the doctor a lot, or you may go to the doctor all the time, but you’re only taking low-cost, generic medications.

So, this makes it able to customize. You can pick from 30 different plans out there, find the best plan for you every single year, and then you’re good to go. It does not change your medical coverage in any way if you want to change your drug coverage.

Cons to Medigap Plans

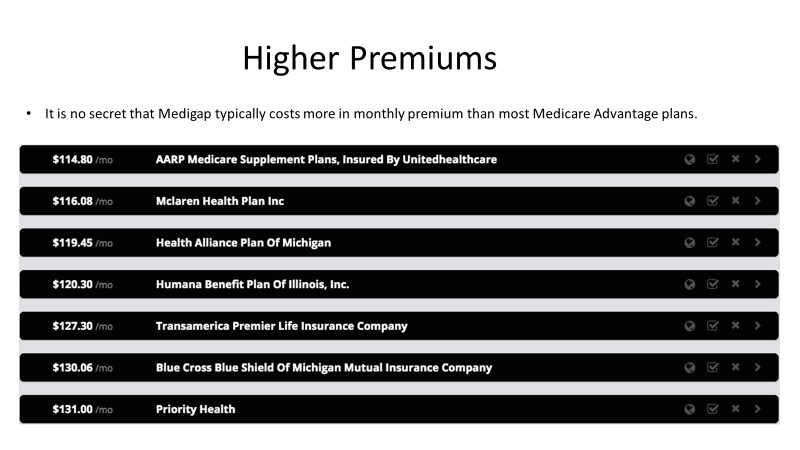

The first one is probably the most straightforward, which is there are higher premiums. It’s no secret that Medigap is typically a higher monthly premium than Medicare Advantage plans.

The higher premium comes with Medigap, where you can see here the baseline plan. These on rates in Michigan for a 65-year-old. You’re looking at about $115 minimum per month when it comes to Medigap, whereas Medicare Advantage can go all the way down to zero. You have probably seen the advertisements on TV – “Call us now to talk about a zero-premium plan.” Those ads are talking about Medicare Advantage. Medigap premiums start in the hundreds of dollars, and it changes based on your location, your age, and your gender.

Another con to Medigap is that you much purchase separate drug coverage. You see it when people feel overwhelmed by everything that comes with Medicare. We tell them you have to go to Social Security, sign up for Part A, get Part B, then you need Medigap, then you need a drug plan, and then you need dental coverage. Sometimes, people want the one-size-fits-all package. It doesn’t exist, but they think that’s the package they’re getting with Medicare Advantage, whereas with Medigap, they don’t want to look at a new drug plan every year and have a different medical card for the pharmacy.

So, this is something that comes up. I always tell people, whether they’re an advisor or client, that they shouldn’t make healthcare decisions based on having an extra card in their wallet, but at least know that it can be a struggle for people.

There are also no additional benefits when it comes to Medigap. Generally, Medigap policies never cover long-term care. There is not going to be a policy that somehow combines Medigap coverage with long-term care.

Compared to Medicare Advantage plans, Medigap doesn’t cover vision and dental. So, your routine vision and dental when you go to get your glasses, your eyes checked, your contacts, or if you go to get your teeth cleaned – that is not going to be covered by Medicare, and because Medicare does not cover it, it’s not going to be covered by Medigap either.

The biggest reason people stray away from Medigap aside from just the price, is they’re not going to get YMCA for free and can’t get their teeth cleaning paid. Frequently, this comes as a shock to people, so they’ll just say, “Well, this Plan Zero covers all of that, so I’m just going to go with it.”

Medicare Advantage

Medicare Advantage plans are, without a doubt, the more heavily marketed plan, and there are a couple of reasons.

The government pays insurance companies to offer Medicare Advantage plans. The government doesn’t want the risk on their books of having people on Original Medicare, so instead, they tell the insurance companies they’ll give them a lump sum or monthly payment to offer Medicare Advantage plans, so they don’t have to deal with the fluctuations of health and healthcare costs. Medicare Advantage plans love it because they know what’s coming in and know what benefits they can provide for that price. It tends to be the more lucrative option when it comes to insurance companies and their revenue.

We have talked to COOs and CEOs of large insurance companies, and we’ve even had one say, “Medigap is better coverage, better for the client, but Medicare Advantage pays the bills.”

So, what is Medicare Advantage (MA)? It’s usually called “Part C.” This is just a marketing thing. It’s not a part of Medicare in any way. It just fits in with the A, B, C, and D, but really, what happens with Part C is that you are no longer enrolled in Original Medicare. Instead, your Advantage plan takes over your medical coverage and drug coverage. It wraps it all into one package.

MA plans are an all-in-one or bundled alternative to Original Medicare. They are offered by private insurance companies, and members must reside in the plan’s service area. So, these plans are more of the HMO/PPO variety that most people are used to, and coverage will be where you live. For example, metro Detroit has specific plans where you can’t go outside of metro Detroit. It’s a smaller HMO plan. It gives you richer benefits for the sacrifice of the larger network, but know that again, it works similarly to under-65 health insurance, so it feels comfortable for people.

If you’re coming from a Ford plan as an employee, and you have a deductible, copays, coinsurance, and you can go to see a physical therapist, and then you go to Medicare Advantage and have the same copay at the doctor, max out-of-pocket, and deductible, it’s structured a lot like under-65 insurance. Again, it bundles everything into one, so they do include drug coverage, even at the zero-premium price, and then they offer the additional benefits beyond Original Medicare that we talked about, like dental, vision, hearing, and gym membership. Who knows what will be added next?

A quick story on that – I saw one yesterday doing training for next year, and the company is going to do a service called PAPA, where they send college students to elderly enrollees’ homes, and they just cook for them, clean for them, and do whatever, so they’re really doing everything at this point to try to differentiate their plans. I thought that was interesting – sending college kids to hang out with the elderly. We’ll see how that goes.

Pros of Medicare Advantage Plans

There are lower premiums with Medicare Advantage plans. The average is $30 per month. You can compare that to premiums in the hundreds for Medigap, but for many plans, most of the marketing is geared toward zero-premium plans. These do include prescription coverage, so you can pay zero per month and get drug coverage included. I’ve even seen some plans that have a much narrower network and scope, and they’ll be a zero-premium plan that comes with drug coverage, and they give you a rebate toward Part B. You can even pay $30-40 less for Part B in addition to having a no-cost plan to go with it.

So, the lower premium is by far the most significant enticement. Going back to the complexity and the simplicity, Medicare Advantage plans come with one card. I’ve talked to insurance agents who say, “Well, you’ve got to agree that it’s better just to have one card in your wallet.” It’s a convenience thing, but don’t make your healthcare choices based on one card, two cards, or three cards. Just know that it is something out there that people hear that is enticing.

Medicare Advantage also makes it easier for payments, so you don’t have a bunch of payments coming from a drug company or a Medigap company. It is all wrapped into one.

The other big thing is the additional benefits. It’s prevalent for dental, vision, hearing, and gym memberships to be covered with Medicare Advantage plans. Many people think, “Okay, I can go to the dentist, I can have crowns, fillings – Whatever it may be, I’m going to be covered if something happens to my teeth.” That’s really not the case. Routine dental and vision are covered, so you can typically get one or two cleanings, one or two x-rays, and maybe a filling for the year, and then, for vision, you usually get a free exam, and you might get $100 toward glasses or contacts.

In Medicare and Medicare advertising, you might see “coverage” or “covered by this plan.” All “coverage” means is that it has some form of coverage. It doesn’t mean it’s completely covered. If you tell me something is covered, like dental, in my mind, I say, “Okay, great, it’s totally covered,” but really, it just means you’re giving me some form of coverage. So, you have to dive deep into these plans and understand what “coverage” means.

I’ve had other HMO plans where they have a limited, narrow network, and the sales rep is saying, “Well, you have nationwide coverage. It’s an HMO, but you can go anywhere.” And then, you look down at the asterisk, and it says, “If you go out of network, you pay 50 percent of the cost.” So you have coverage everywhere, but what kind of coverage is that? If you have a client that has to get the premier treatment at MD Anderson, 50 percent of a $50,000 bill – it’s coverage, but it’s not good coverage.

There’s also limited discrimination for pre-existing conditions. You can be denied Medigap coverage based on having pre-existing conditions. With Medicare Advantage plans, you can simply switch every year, and you can do that without the potential of being denied as long as you don’t have end-stage renal disease (kidney failure).

Pre-existing conditions are the big thing for people if they already have a Medicare Advantage plan. If they have a lot of pre-existing conditions, it’s important every year to look at the new options out there and see which plan will fit best. You can have cancer and switch Medicare Advantage plans. You cannot switch to Medigap, but you can switch from one Medicare Advantage to another Medicare Advantage.

Cons of Medicare Advantage

The biggest con is limited networks. They are HMO/PPO-style plans. They are becoming a little bit broader, where some of the PPO plans will give you almost identical coverage outside of the network compared to inside the network, but there is cost-sharing involved. There is a difference between the actual out-of-pocket spending when it comes to Medicare Advantage plans versus Medigap.

Medicare Advantage Plans are yearly contracts with insurance companies, so consumers have to agree to see medical providers in their insurance plan in an approved network. Insurance companies offer that “At this reduced price, we will give you medical coverage and additional benefits. You have to agree to see our doctors.” It’s really that simple as to what Medicare Advantage plans are.

Medicare Advantage Plans leave you exposed to HMO plans. If you have to go out of network, it can be hard to coordinate as well for people who travel outside the service area. There are new some snowbird-specific plans, but just because you’re a snowbird doesn’t mean you’re only going from Michigan to Florida. You may take a trip elsewhere that is not part of a specific plan, so if you have somebody committed to traveling, that’s a big reason to stray away from the Medicare Advantage side.

These are yearly contracts, so they’re not guaranteed contracts like Medigap. It’s not where you pay your premium, and you get to keep your plan forever. You have to go year to year with your decision, whereas with Medigap, you have the budgeting and planning picked out for decades instead of the year-to-year decision.

Another disadvantage is that physicians and hospitals can and do terminate agreements in the middle of the year. I’ve seen plenty of headlines in July or August that the so-and-so healthcare system is no longer taking so-and-so’s Medicare Advantage plan. I saw one in Florida that no longer takes United Healthcare plan, and if you have that United Healthcare plan, you have to pick a new doctor for the rest of the year. You can’t change your plan just because your doctor is no longer in-network, so that’s a big thing about which people don’t technically think.

Again, government funding is tied to Medicare Advantage plans. If Republicans are in office, it’s usually funded more. If they’re not, it’s funded less, so you never know what’s going to happen with year-to-year funding.

Medicare Advantage plans own the right to tell you where you can and cannot receive care (managed care). If your doctor says you have to have a procedure done at a specific clinic, your Medicare Advantage plan has every right to say, “How about you try this first?”

If it’s a top-of-the-line procedure with an endoscope that’s going to be minimally invasive, your Medicare Advantage plan can say, “Yes, that’s great, but we want you to try this option first, where it’s more exploratory, and we need actually to open you up.” So, it’s not always up to you as the consumer or end-user where you can or cannot seek care because your Medicare Advantage plan may not allow it.

We commonly find people who are on a Medicare Advantage plan and have been healthy for two years. Then, they need a knee replacement, and they get that knee replacement done with their Medicare Advantage plan, and they do not understand at the time that all of a sudden, they’re going to start paying $40 per session for physical therapy. That’s problem No. 1 – they’re not prepared for one month costing $500 – but No. 2, the carrier can come back, and they often will and do cap how many treatments that person can have for physical therapy. So, with a knee replacement, they might give you seven sessions because that’s managed care – they can tell you you’re stopping at seven – whereas if you’re back with Original Medicare and Medigap, you might have 22 sessions.

There are also higher out-of-pocket costs. With Medicare Advantage plans, instead of the $185 deductible and cap, you’re looking at up to $6,700 as the max out-of-pocket with a Medicare Advantage plan, and this does not include prescriptions. Many people think prescriptions are covered in the $6,700. You could have a bunch of procedures, rack up bills for $6,700 for the year, and also have another $5,000 in prescription costs.

The exposure to the high deductible of Medicare Advantage plans is huge for people. Usually, I will say most plans are about $5,000. They don’t go to the max – $6,700 – but just know that is possible, and that’s just for 2019. We don’t know what it is for 2020 yet. It makes budgeting difficult, like getting a lower-cost car and hoping that nothing terrible happens.

There’s less flexibility with coverage options, so again, you do get the bundled approach, where it has the drug coverage and the medical coverage built-in, but what people don’t realize is that you can have the same doctor forever, but your medications are rarely ever going to stay the same for your whole retirement. If you have a medication that is no longer covered by your plan, you have to switch to a different Medicare Advantage plan.

When you do that, you also have to change your doctors and your network because again, it’s a bundled approach that includes everything, so your medications could determine what plan is covered by your doctor, or your doctor could leave your plan, and you may want to follow your doctor, and then the new plan may not cover your prescriptions as well. So, again, you can’t customize it. You have to find what’s best for you, but you’re not going to see the highly customizable option that you would with Medigap and separate coverage.

Comparing Medigap and Medicare Advantage

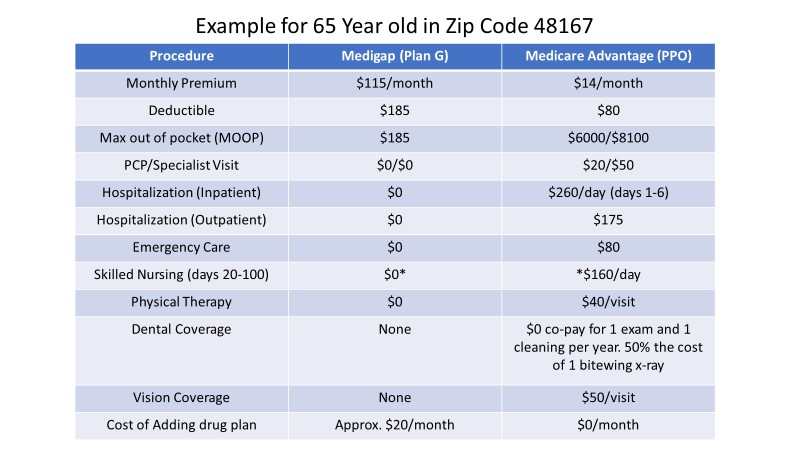

Here’s the pricing for a Medigap plan, Plan G, and a Medicare Advantage plan using metro Detroit in Michigan as an example. It’s a pretty good example of what is available nationwide.

You can see that Medigap is $115 a month, and Medicare Advantage is $14 a month. The big difference is the out-of-pocket spending with Medicare Advantage plans where the max out-of-pocket is $6,000. If you have to go to physical therapy, it costs you $40 every visit. There are a bunch of various copays, even if you’re hospitalized. If you’re hospitalized for six days, you’re paying north of $1,200 with Medicare Advantage, whereas Medigap covers everything once you meet the deductible of $185.

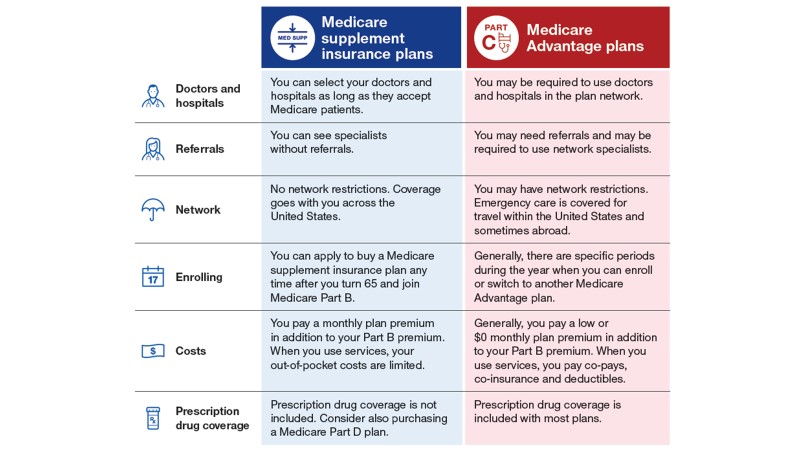

Here is another chart that compares the differences between coverage of Medigap and Medicare Advantage plans.

Everyone’s health can and will change. I always tell people to buy the plan that’s going to fit them for 20 years, not what’s going to fit them for two. We had a person earlier this year who was in perfect health, wanted Medicare Advantage, felt good about it, and wanted the extra benefits. After we talked to her, she realized that she would like to go with Medigap after all. Two months later, she had a heart attack and had other issues where she could have never been able to get a Medigap plan if she had gone with a Medicare Advantage plan from the start. So, things can and do change. You have to plan for the long term, not the short, just the same as with financial planning.

Remember, the government is funding the carrier to the tune of $1,000 a month per person. The carrier wants to turn around and sell it to a bunch of people, thus the push with Silver Sneakers, the dental coverage, and all the related perks.

Healthy people want to buy a Medicare Advantage plan because it looks fantastic. For Medicare Advantage plans, be aware that agent compensation is double what we are paid for signing somebody up with the Medigap contract. So, in our state, if someone enrolls in a Medicare Advantage plan, we get $482 from the carrier. If we put them with a Medigap policy from the same carrier, we get $240 as our agent commission.

If it’s good for the government to put people into Medicare Advantage, it’s good for the carrier to get them to Medicare Advantage, and it’s good for the agent to get them to Medicare Advantage, it typically is not good for the consumers. It’s critical to understand that if you follow the money trail, you can understand better why it’s portrayed the way it is and why many people walk away with Medicare Advantage.

Key Takeaways

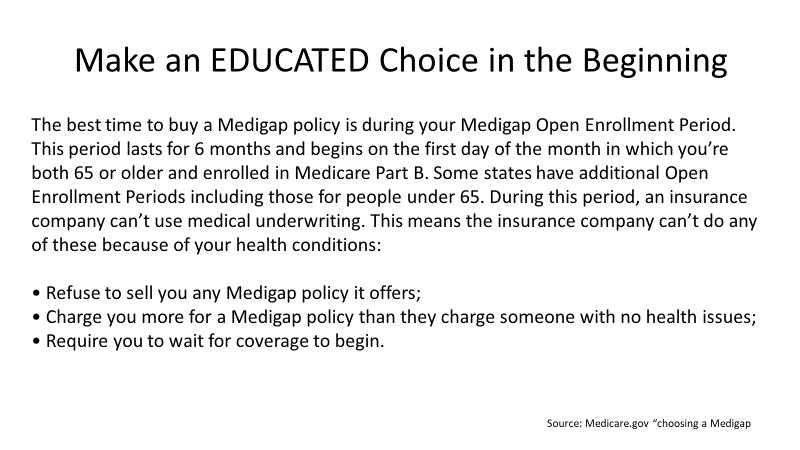

The biggest key takeaway is to make an educated choice from the beginning. Again, this is also from Medicare.gov. Please read this and understand it for your clients, or have your clients read it. When you first start Part B of Medicare, whether you’re 65 or when you retire, you have six months to take any product with no health questions. After that, you are not guaranteed to get a Medigap plan without health questions for the rest of the time you’re on Medicare.

If you have cancer and you’re being treated actively, and you start your Part B, you can get any plan without any questions asked. It’s going to cover you entirely, you’re going to have most of your out-of-pocket expenses covered, and you won’t have to worry about those bills.

Now, on the flip side, if you get a Medicare Advantage plan because you are healthy and you don’t really care about the out-of-pocket expenses, in two years, if something happens then, and you want a Medigap plan, you simply cannot get one. Many people don’t realize this. They say, “I thought Obamacare did away with pre-existing conditions.” It did, but not for Medicare, so you can and will be denied Medigap plans if you have certain pre-existing conditions, which can be as extreme as Alzheimer’s or even as mild as mini-strokes or diabetes. If you take insulin, that can stop you from getting coverage from a lot of Medigap plans with different insurance companies.

All this is why we talk to people at 64½, so they know at least that pre-existing conditions are a vital consideration when it comes to choosing a Medicare plan when they turn 65 or when they start Part B. Consumers out there just aren’t getting this information. How would you like to be the consumer coming back four years later after a cancer diagnosis, realizing that you never saw this from your agent four years ago? This is why we do this.

When you’re talking about which is right for your clients – Medicare Advantage or Medigap – it is something that none of us can tell you or that even the client can tell you based on their needs. Medigap does provide very comprehensive coverage; there’s no doubt about it, but it’s just not going to fit everybody. Some people have a higher risk tolerance, whether it comes to financial investing or Medicare. People might want a lower payment, and they might want to take the chance with out-of-pocket spending, or they’re fine having limited networks.

Bring up IRMAA. Please talk to your clients about how their modified adjusted gross income impacts their cost on Medicare. If your client does have a higher net worth and they’re stuck with a higher IRMAA surcharge, know that it is appealable. If you retire and you have a life event that lowers your modified adjusted gross income, you can appeal your IRMAA surcharge, and many times, it is successful.

Find a broker that specializes in Medicare. Medicare agents and Medicare brokers have to go through rigorous training and testing to make sure they’re certified to sell Medicare products. It’s not just a standard health-licensed agent. You have to find somebody who knows what they’re doing, understands the differences between the two products, and can talk to your clients, not only about the products, but also the penalties associated with Medicare and when and when not to sign up. It’s not as simple as going to talk to somebody who can sell Medicare. So many people dabble in it; not many people focus on it. Very few agencies do only Medicare. It’s just a gateway to talk about other products. A lot of Medicare agents out there get in the door with Medicare, and then move on to sell products that make other commissions.