This article will cover purchasing a brand-new home without any mortgage payments, which is probably one of the better uses of the reverse mortgage. Not many advisors or consumers know about it. There are a couple of reasons for that.

One of them is just that the realtor market doesn’t know about the HECM (Home Equity Conversion Mortgage) for purchase product at all. Many still think about traditional mortgages or traditional financing. Many are already affiliated with lenders or mortgage brokers that they have worked within the past and don’t have affiliate relationships with reverse mortgage companies. It can be a compelling way of allowing clients to right-size into their new home with no future mortgage payments.

What Changes Have Been Made in the Reverse Mortgage Market?

In 2010 it was very much of a wild west in the reverse mortgage world. The program has always been well-intentioned by the government to support American’s retirement, such as Social Security for retirement income and Medicare for medical coverage. The reverse mortgage is the government’s way of supplementing and tapping into additional assets for homeowners that they can borrow later on down the road for retirement.

The problem is that when the government first created the reverse mortgage back in 2010, there were minimal rules: if you were 62 and over and you lived in a home, you would qualify for the reverse mortgage. Unfortunately, this attracted a lot of bad actors from all sorts of spectrums. Homeowners, loan officers, and lenders abused the program. The government stepped in and implemented strong protections in 2013, 2015, and 2017. They also strengthened the underwriting process of the program.

If you could imagine back in 2010, out of all mortgage products in the market, HECMs were the only ones that had no underwriting guidelines for any income and credit. Clients were applying for the program when they had a bankruptcy the day before, or they were in foreclosure. Those kinds of clients would be extremely high-risk for any mortgage product out. One of the legacy issues we have is that if you read stories about the reverse mortgage program about people being foreclosed, a lot of those clients were very, very high-risk and probably should not have been associated with a mortgage product at all. Unfortunately, back then, we had to allow all clients into the program, so it attracted many subprime households who probably shouldn’t have been in the program.

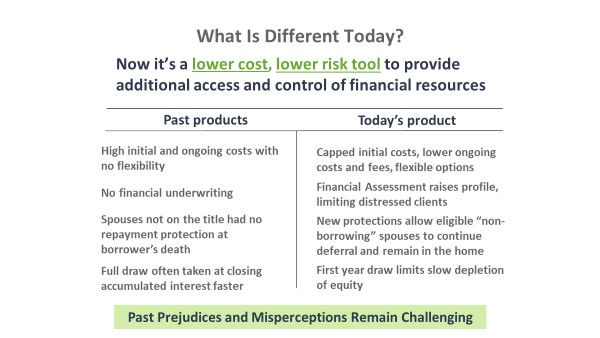

In the past, the HECM had a high initial and ongoing cost with no flexibility. It was a fixed rate lump sum distribution where all the money was accessed right away. That led to an interesting behavioral issue. For many sub-prime borrowers, it was almost like winning the lottery. What do you read about lottery winners? They win a million dollars, and then two years later, they go broke.

The same sort of thing happened in the reverse mortgage world where many of these people were already sub-prime. They were very tight on their cash flow. They got the reverse mortgage for a very short-term band-aid, but they didn’t have a sustainable plan in place. One of the most significant changes was in 2015 when the government implemented very common-sense guidelines to turn the program into a long-term sustainable tool. If you were to go through the underwriting process with me or any other reverse mortgage company, one of the key things you will hear is whether or not this reverse mortgage is sustainable for the client.

We do evaluate and implement income and credit guidelines that allow the borrower to demonstrate and prove that they have a long-term plan in place. In the past, we had no financial underwriting. For today’s product, we do have a financial underwrite that assesses their income and credit. It just raises the overall credit profile of clients.

It’s still a very lenient program. It’s never been the intention of the government to make people not qualify. But it does remove the bottom 10% who probably need to find alternative forms of housing or assistance to get them through retirement. The reverse mortgage would only be a temporary band-aid.

Another past issue was that spouses that were not on the title of the home or the reverse mortgage and had no repayment protection, and this led to some very tragic circumstances. Sometimes this was self-imposed by the borrower where they voluntarily remove the younger spouse. With reverse mortgages, we use the ages of the borrowers to determine how much they qualify. Guess what happened? When the older spouse passed away, the younger spouse was not on the title and didn’t have access to any of the funds in the reverse mortgage program. They were literally and metaphorically kicked out to the curbside.

In 2013 HUD made sweeping changes to the program to implement spousal protections across the board. We now have to include spouses in the computation of the program. The younger spouse can continue to live in the home over their lifetime as long as they keep up with the other terms like living in the house, payment of property taxes, and homeowner’s insurance. HUD (Housing and Urban Development, a federal agency) also did a good thing by extending those protections to grandfather in all those who wrongly experienced these situations. We shouldn’t see these legacy issues anymore when it comes to these particular situations.

Finally, the old HECM product required full draws of the loan at a fixed interest rate of around 5% so that they would amortize pretty quickly. With today’s product, we more often recommend the variable rate, which allows more flexibility in taking the funds out. Many clients are offered the credit line option, which leaves all the funds in the credit line until the borrower taps into it.

One thing that we have seen with our analysis here at Longbridge Financial is that the more money clients take out at the time of closing, the more they accelerate their draws in the next two years. It turns out that if clients take out just $10,000 right away, they tend to burn through all their cash within the next two to three years. A client who leaves their funds in the credit line tends to have those funds last for a longer period of time. The credit line option or even the monthly income option is a better sustainable way of thinking about the reverse mortgage, especially for middle-income Americans who are looking at it for a longer-term planning tool.

Reasons to Consider Using a HECM for Purchase

Many retirees in America are carrying a lot of debt into retirement. Some are still carrying student loan debt that they acquired either from their children or grandchildren. Mortgage debt is usually the most significant source of debt that clients carry into retirement. For those ages 60 to 64, about 38% carry a mortgage. For those ages 65 to 74, about a quarter are still paying off a mortgage. Part of this is due to the effect of the Great Recession in 2008 that led to much refinancing in 2010 and 2011 after the stock market crashed and pushed interest rates very low. Pretty much everybody at that time refinanced if they could to lock in the lower interest rate.

However, they restructured the mortgage to a new 30-year term, so for a lot of people they have a mortgage that may outlive their own life. That means they’re sort of beholden to that mortgage payment for as long as they live. The reverse mortgage gives these clients the flexibility to make that payment or not make that payment. At the heart of the reverse mortgage, and this is probably the simplest way that I can explain the program, is that it is just like any other mortgage with flexible payments, meaning that if you refinanced your existing mortgage over to a reverse mortgage, you could continue to make normal mortgage payments if you chose to do so. In addition, you can still write off the mortgage interest deduction like any other mortgage.

However, if a client gets into a bind and needs to skip the payment, they can with no penalty and just catch it up the next month or not at all. Whereas with a traditional mortgage, if you miss that payment the mortgage company will start to impose penalties or start the foreclosure proceeding. The very structure of the reverse mortgage gives flexibility to borrowers and reduces the foreclosure risk to seniors by not having a required payment for the mortgage interest and the mortgage principal. Clients can take money out of the reverse mortgage, pay the mortgage down, take money out, and again pay it down. Behaviorally, we have discovered that 90% of clients, when given a choice, don’t want to make any payments at all. But some clients do make payments on the reverse mortgage either as interest-only or a fully amortizing payment to pay down the balance.

The interest rates on reverse mortgages are in line with the broader mortgage market. Also, academic research is showing the advantages of using a reverse mortgage in a responsible manner. Proper use can lead to more legacy wealth left over for the children, and it can substantially increase the success rate of clients getting through retirement. It is especially useful for clients in the middle America range that have less than one million dollars saved for retirement.

What is the HECM for Purchase program?

Within the world of reverse mortgages, the purchase program is probably one of the hidden secrets. I was able to pull 2017 data from the top eight or nine states from HUD, which is the last full years’ worth of available data. About one of every 20 reverse mortgages are a HECM for Purchase.

Reasons to consider a HECM for Purchase for your clients include:

- When clients want to right-size their house.

- You also want to be looking at the HECM approaches when a client doesn’t want to pay all cash for their new home. This will also help them preserve their portfolio.

- If clients may not have long-term care or they may not have enough assets to buffer through what I like to call ‘shocks’ such as their car breaking down, to home renovations, to medical expenses. Every client should have a couple hundred thousand dollars (depending upon where they live) to help absorb those shocks over their lifetime.

- The client’s estate does not necessarily need to live in the home, especially once the parents pass away. When the reverse mortgage gets triggered by the parents moving out or passing away, the children will have to make a decision on the debt at that time.

When not to look at the HECM approaches:

- Just like any other mortgage, there are closing costs, mortgage interest, and HUD mortgage insurance that will eat up some in the home a little or a lot depending on how long the clients live. It can also make moving difficult because the equity has been reduced by the reverse mortgage, so they may not have a lot of equity rollover into another home.

- Children may not be able to live in the home once the parents die because the children will have to decide how to pay off the debt, and they may not be able to refinance at that time, or they may not be able to pay off the mortgage on their own.

- There are also ongoing obligations by property taxes, homeowner’s insurance, and home maintenance.

- There are property restrictions on condos and coops. More specifically, for condos, it does need to be FHA approved.

How to use a HECM for Purchase to create a sustainable living situation

The HECM purchase allows clients to right-size into a home in a single financing transaction. In the past, clients financed their retirement home using a traditional financing tool, with 20% down and 80% financed. Then a couple of months later, they financed into a reverse mortgage, experiencing two sets of closing costs when they could have used the HECM purchase directly to buy into the home. It also makes home equity more accessible.

Using a HECM for Purchase to Right-size

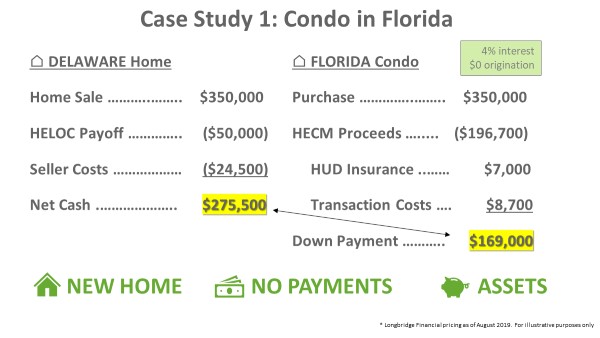

Here’s a classic example of a HECM for Purchase. The Millers want to move to Florida for warmer weather and purchase a condo. They currently own a home that is worth $350,000, owe $50,000 on a HELOC, and are looking for a condo in the same price range of what they have today.

Their financial adviser wants to investigate the HECM for Purchase Program on their behalf to see how it might fit in their portfolio. He likes how the Millers can reduce their state tax burden by moving down to Florida (which has no state income tax), and to unlock equity for future long-term care and other needs. The adviser is looking five, 10, 15 years down the road and trying to preserve as much money in a portfolio as possible.

Let’s say the Millers sell their home for $350,000 and pay off the $50,000 HELOC. Seller costs total $24,500, so the Millers net $275,500 from this transaction. This means they won’t have enough to pay cash for their new home, but they will have the ability to put in a good amount equity.

If they were to a HECM for Purchase, they could purchase their new home for $350,000. They qualify for a reverse mortgage of around $196,700. HUD insurance is 2% of the home value, or $7,000, and there are transaction costs of $8,700, so the total down payment needed from the Millers is $169,000.

This allows them to net over $106,000 that they can take out while buying a brand-new home in Florida. Also, they will not have any future mortgage payments.

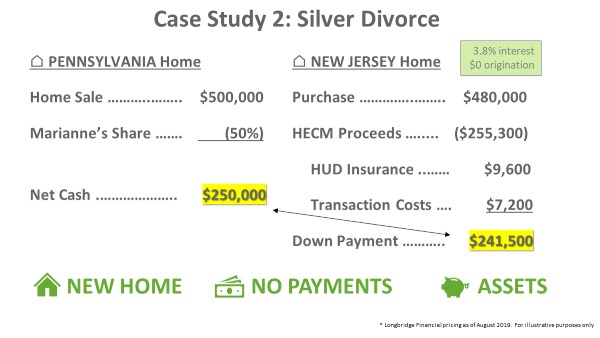

Using a HECM for Purchase with a Silver Divorce

We are starting to see more silver divorces where couples divorce after decades of marriage.

For example, Marianne, aged 68, is recently divorced. She is starting over at the age of 65. She is looking to buy a brand-new home for $480,000 close to her children.

Her divorce decree entitles her to half the value of the $500,000 home. However, the ex-husband wants to keep that home so that she will receive her half in cash. Marianne’s CFP knows that even though Marianne is entitled to another large distribution from the ex-husband’s business, one of the problems is that the business’s proceeds are illiquid, so she probably won’t see those funds for many years. Marianne, unfortunately, doesn’t have many savings under her name beside a modest $80,000 cash account, so she is looking to stretch that cash as far she can.

On the Pennsylvania home, she’s entitled to 50% of the $500,000 value so that she will receive $250,000 right away from the divorce. She found a home in New Jersey she’d like to purchase. At a 3.8% interest rate with no origination, a HECM for Purchase will qualify her for $255,300 loan, less closing costs of 2% for HUD insurance, and transaction costs such as title fees, notary fees, documentation fees, of about $7,200.

This means that she needs to put down $241,500 to buy the home in New Jersey using a HECM for Purchase, close to what she can get from the equity of her former home. She will have no payments on this new home in New Jersey, and she’s able to preserve the $80,000 of cash that she has for everything else needs.

Key Takeaways

When to use the HECM for Purchase:

- Clients want to move into their forever home and have a sustainable living situation. The HECM for Purchase is truly designed for the forever home where clients don’t have to worry about payments or the interest rate, and then when they pass away, the remaining home equity pays off the loan. To use the HECM for Purchase, at least one of the spouses needs to be 62, and they do need to meet very minimal income credit standards.

Most clients tend to be in their sixties and seventies. That’s usually the sweet spot where they can access 50% of home’s value as a loan and 50% for the down payment for their retirement home.

- The HECM for Purchase helps preserve the retirement portfolio so it can stay invested where needed.

We do have a website available just for financial advisers. We have the best of class calculators that are free for financial advisers. There’s no paywall for registration. One of them allows you to compute HECM proceeds, and it does incorporate jumbo reverse mortgages. The other one is a Monte Carlo simulation for financial modeling.

The reverse mortgage is a good long-term tool for middle America. These clients have less than one million dollars in assets, but they’re looking for a little bit more to get them through retirement. These are smart clients, they are proactive, they’ve done a good job saving for retirement, but they also know through their forecast that they’re not quite sure that everything that they have will get them through to the end. Americans are living longer than ever with good health and good medicine, so they need to plan for a minimum of 25 to 30 years through retirement. That’s a long time to prepare for when you have so many uncertainties. The HECM for Purchase can help.