One option to increase retirement income sustainability is to add a source of retirement income that cannot be outlived. In a 2001 article for The Journal of Financial Planning entitled “Making Retirement Income Last a Lifetime,” Ameriks et al. concluded that adding annuities to a retirement nest egg reduces portfolio failure rates, which is the risk of running out of money during your lifetime.1 Their analysis found that withdrawals from a retirement portfolio “can be sustained with more certainty for longer time periods, by adding the risk-pooling characteristics of an immediate annuity to the overall retirement portfolio.”

Does that conclusion still hold over time, when many of the underlying conditions have changed? Some 15 years later, in this article we revisit the question of whether the benefits of including a lifetime income annuity in a retirement plan persist in the current economic environment.

Specifically, we evaluate the merits of purchasing an annuity with part of the retiree’s nest egg in an environment characterized by low interest rates and, in turn, low(er) annuity payout rates (than in 2001), using annuity quotes obtained from CANNEX.2 We measure the benefit of partial annuitization by using a conceptual “retirement income frontier” that traces out the trade-offs between the sustainability of a retiree’s lifetime income and her expected financial legacy, using the framework put forth by Milevsky.3

“Annuitizing a Portfolio:” What and how?

First, let’s review what is meant by “annuitizing” (part of) a portfolio. In this article, we mean taking a portion of retirement savings and using it to purchase a single premium income annuity, or SPIA. While the SPIA is often overlooked in retirement income planning, it can provide a tremendous boost to the overall sustainability of a client’s retirement: for a one-time premium, in return the SPIA provides a lifetime of income. (Thus it functions much like a workplace defined benefit pension.)

When contemplating both retirement income and income annuities, the SPIA is frequently shunned – by clients and advisors alike – despite the benefits it can offer, because the purchase decision is irreversible and thus the asset, although it produces income, is illiquid. This point of view, however, sidesteps both the mortality credits that retirees acquire from pooling their assets, which provide a greater yield than products with similar levels of guarantee; and the lifetime nature of the SPIA income, which provides a hedge against an unknown and potentially longer-than-expected lifetime. Ultimately, while a reliable source of retirement income may be replicated with investments in fixed income products, a SPIA nevertheless provides a higher income than what is typically available from other non-pooled, non-life- contingent assets or products. In fact, given the relative advantage that the SPIA can offer to retirees, the low take-up of lifetime income annuities by retirees is known as the “annuity puzzle”– a riddle which has been discussed at length by both academics and practitioners for decades.

Retirement Portfolio Sustainability: Does adding a SPIA (still) help?

In this article, we will explore the impact of adding a SPIA on our client’s Retirement Sustainability Quotient (on one hand) and her Expected Financial Legacy (on the other). It is the trade-off between these two outcomes – increased sustainability or increased financial legacy – that is traced out by our conceptual retirement income frontier.

Our analysis assumes that the client has her financial assets consolidated in either (a) a managed account, defined as a portfolio of stocks, bond, ETFs, mutual funds or any combination thereof, or (b) some combination of managed account plus SPIA, in which the annuitized portion mimics a pension to provide lifetime income starting at retirement. We further assume that our client has a good grasp on what her future income needs will be, on an inflation-adjusted basis; that her spending needs will grow at a constant 2% per year, and that she chooses to manage inflation risk by purchasing a cost of living- adjusted SPIA. Further, in assessing our case study client’s retirement income plans and when the client has a combination of a SPIA and portfolio assets in a managed account, in our analysis the account withdrawal is coordinated with the annuity payment to match the desired spending amount.

We define retirement income sustainability as a function of first, the fraction of income annuitized and secondly, the “lifetime ruin probability” of the managed account. The lifetime ruin probability, in turn, is defined as the probability the investment portfolio will be exhausted (that is, fully depleted) while the retiree is still alive.

Mathematically, the Retirement Sustainability Quotient (RSQ) takes the following form:

RSQ = (1 − p)(1 − fSPIA ) + fSPIA = 1 − p(1 − fSPIA )

where p represents the ruin probability and fSPIA represents the ratio of the annuitized income to the client’s desired income.

In the above equation, we are measuring retirement sustainability as the weighted average of the success probabilities (“success” defined as the cases in which the retirement income portfolio is able to support the desired withdrawals during the client’s lifetime). Note that the annuity, by its very nature, has a ruin probability equal to zero (assuming no default risk of the insurance company); while the investment account has a “non-zero” ruin probability.4

As everything in finance, there is always an economic trade-off – and the added retirement sustainability that is produced by annuitization comes at a cost that we can view through the prism of the client’s “Expected Financial Legacy,” which is the wealth that is available to be left to heirs.

We define Expected Financial Legacy (EFL) more formally as the expected value of the funds left over upon the retiree’s death, measured in today’s dollars. More precisely (and technically), our client’s EFL is calculated by aggregating the present value of the probability-of-death-weighted account balances over time. Here we note that portfolio account balances may veer below zero; implying that the client, instead of leaving a financial legacy, is instead borrowing funds in retirement (possibly from the people who would otherwise be heirs!). In our examples, when borrowing is required we assume the cost is equal to the long-term interest rate – but we caution the reader that in the extreme (and in real-world scenarios), borrowing may not be available or the cost may be higher than our assumptions.

Together, the two concepts of Retirement Sustainability and Financial Legacy form a frontier that helps us to better understand and model the income sustainability and financial legacy trade-off introduced by the inclusion of life annuities in the client’s retirement portfolio.

Methodology: Modelling Legacy and Sustainability along the Retirement Income Frontier

Now, on to our model. In our case study, given the illiquid nature of the SPIA, and the irreversibility of the SPIA purchasing decision, we limit the allocation to SPIAs to be no more than 30% of our client’s

initial wealth. With the remaining (non-annuitized) portfolio, we consider three kinds of asset allocation models: conservative, balanced, and aggressive.

We also consider two approaches:

- Approach 1: SPIA + No Change to Asset Allocation (“SPIA + No Change”)

In approach one, we assume our client maintains their asset allocation (whether conservative, balanced or aggressive) even after purchasing the annuity. That is, we do not adjust the allocation of the managed assets in response to the annuity purchase.

- Approach 2: SPIA + Modified Asset Allocation (“SPIA + Modified Portfolio”)

In our second approach, we proportionally adjust asset allocations within the client’s managed account such that entire retirement portfolio conforms to the overall risk profile of our retiree (whether conservative, balanced or aggressive), taking the allocation to the SPIA into account. This means we change the asset allocation of our client’s investments once the client has purchased an annuity, viewing the annuity purchase as a bond-like allocation on the balance sheet.

In our analysis, we use a stochastic modelling approach which incorporates two separate sources of uncertainty (namely, market returns and remaining lifetime) to explore how adding a single premium income annuity to a range of “traditional” investment portfolios affects both retirement income sustainability and financial legacy. (Although our focus is on the single premium income annuity, or SPIA, we note that a similar analysis could be carried out with other types of income annuities, such as deferred income annuities, or even variable or fixed indexed annuities.)

While the Retirement Sustainability and Financial Legacy calculations we are interested in can be carried out using Monte Carlo simulations, we chose instead to use the numerical and analytic methods that are available in QWeMA NumeRIcs®, a set of analytic tools which equip financial specialists to explore and solve questions in retirement income planning.5

From a technical point of view, for our analysis, market dynamics are stochastically modelled and we assume that asset returns are normally distributed – and thus asset prices follow a lognormal distribution. Finally, in modelling remaining lifetime for our client, we utilize the Gompertz-Makeham Mortality model calibrated to RP2000 actuarial tables for calculating retiree life expectancy that are readily available from the Society of Actuaries.6

In our case study, we chose a client who is a 65-year old healthy female retiring immediately. She desires to spend 5% of her initial wealth annually, adjusted in subsequent years for inflation, which we assume is 2%. As noted earlier, we consider three asset allocation models to perform our analysis, namely:

- Conservative Portfolio: 30% Equity and 70% Fixed Income

- Balanced Portfolio: 60% Equity and 40% Fixed Income

- Aggressive Portfolio: 70% Equity and 30% Fixed Income

All calculations are performed on an initial wealth value of $1 which allows us to scale the client’s legacy value by her initial wealth.

The capital market parameters used in our model are based on J.P. Morgan Asset Management’s 2016 Long Term Capital Market Assumptions.7 Specifically, we chose U.S. Large Cap equity returns and U.S. investment-grade corporate bonds for the equity and fixed income returns, respectively. We assumed the long-term borrowing cost was 2.5%.

Tables 1 and 2 summarize the capital market assumptions used in the case study and the return and volatility assumptions for our three (conservative, balanced and aggressive) portfolios.

Table 1. Capital Market Assumptions

| Asset Returns & Volatility Assumptions | ||

| Fixed Income | Return | 4.5% |

| Volatility | 6.5% | |

| Equity | Return | 8.1% |

| Volatility | 15.5% | |

| Correlation Coefficient | 26% | |

| Portfolio Management Fees | 1% | |

| Long Term Discount Rate | 2.5% | |

Table 2. Portfolio Return (Net of Fees) & Volatility of Returns Assumptions

| Annual Return | Volatility of Return | |

| Conservative Portfolio | 4.6% | 7.3% |

| Balanced Portfolio | 5.7% | 10.3% |

| Aggressive Portfolio | 6.0% | 11.5% |

With these assumptions in place, we are ready to examine how adding an annuity (specifically a SPIA), in varying proportions, to our client’s portfolio impacts the sustainability of her retirement income, and her expected financial legacy. We’ll start with the conservative asset allocation, then move on to the balanced and aggressive portfolios.In our analysis, we consider the impact of an annuity purchase on the client’s retirement sustainability and financial legacy if she annuitizes up to 30% of her initial wealth – and we calculate and display the outcomes for no annuitization, and annuity purchases using 5%, 10%, 15%, 20%, 25% and 30% of her initial wealth. (In this way, we can evaluate the differences in outcomes from annuity purchases of varying amounts, up to our cap of 30%.) For the annuity purchase, we have used the average of the A.M. Best’s A++ rated quotes, obtained from CANNEX, for a healthy 65-year-old female annuitant. This gives us a quote of $410 per month ($4,920 annually or 4.92% on the $100,000 purchase) for a $100,000 purchase, indexed at 2%.8

For each allocation, we first show a table that displays numerically how varying the portfolio allocation to different combinations of investments and a SPIA impacts the sustainability of the retirement income as well as the expected financial legacy for our client, both without making changes to the original allocation (“SPIA + No Change”) and with modifying the investment allocation to ensure the holistic or overall allocation conforms to the client’s conservative, balanced or aggressive risk orientation (“SPIA + Modified Portfolio”). We then graphically display the legacy and sustainability results for our combinations of portfolio plus SPIA, along the conceptual retirement income frontier we described earlier – showing how “no change” and “modified” portfolio allocations have varying sustainability scores (the “RSQ”). Finally, we present a chart that shows the sustainability and legacy outcomes for each combination of investment portfolio and annuity purchase, both with and without portfolio modifications.

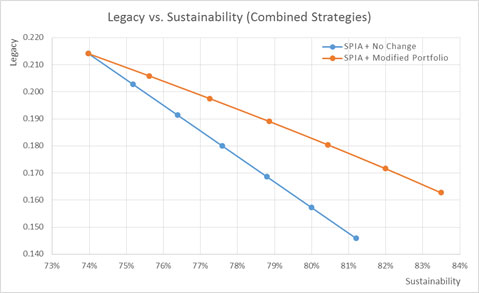

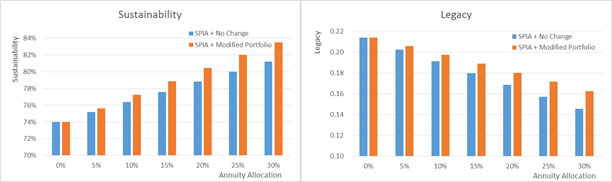

Table 3. Results for a Conservative Portfolio

| Allocations to Investment Account & SPIA | SPIA + No Change | SPIA + Modified Portfolio | ||||

| Investment Account | SPIA | Retirement Sustainability | Financial Legacy | Retirement Sustainability | Financial Legacy | |

| 1 | 100 % | 0 % | 74.0 % | 0.214 | 74.0 % | 0.214 |

| 2 | 95 % | 5 % | 75.2 % | 0.203 | 75.6 % | 0.206 |

| 3 | 90 % | 10 % | 76.4 % | 0.191 | 77.3 % | 0.197 |

| 4 | 85 % | 15 % | 77.6 % | 0.180 | 78.9 % | 0.189 |

| 5 | 80 % | 20 % | 78.8 % | 0.169 | 80.4 % | 0.180 |

| 6 | 75 % | 25 % | 80.0 % | 0.157 | 82.0 % | 0.172 |

| 7 | 70 % | 30 % | 81.2 % | 0.146 | 83.5 % | 0.163 |

Figure 1. Comparison of SPIA + No Change vs. SPIA + Modified Portfolio: Conservative Allocation

Figure 2. Sustainability & Legacy vs. Annuity Allocation (Conservative)

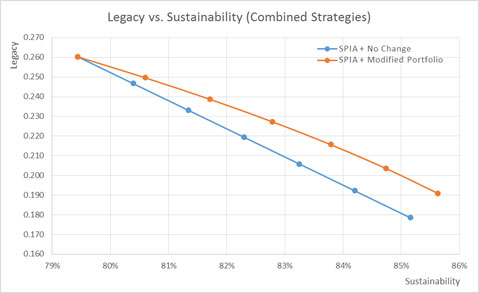

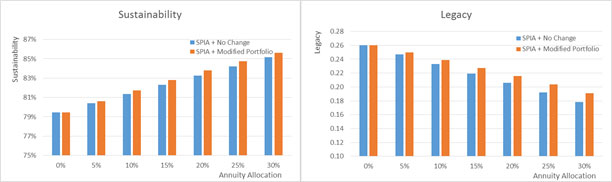

Table 4. Results for a Balanced Portfolio

| Allocations to Investment Account & SPIA | SPIA + No Change | SPIA + Modified Portfolio | ||||

| Investment Account | SPIA | Retirement Sustainability | Financial Legacy | Retirement Sustainability | Financial Legacy | |

| 1 | 100 % | 0 % | 79.4 % | 0.260 | 79.4 % | 0.260 |

| 2 | 95 % | 5 % | 80.4 % | 0.247 | 80.6 % | 0.250 |

| 3 | 90 % | 10 % | 81.3 % | 0.233 | 81.7 % | 0.239 |

| 4 | 85 % | 15 % | 82.3 % | 0.219 | 82.8 % | 0.227 |

| 5 | 80 % | 20 % | 83.3 % | 0.206 | 83.8 % | 0.216 |

| 6 | 75 % | 25 % | 84.2 % | 0.192 | 84.7 % | 0.203 |

| 7 | 70 % | 30 % | 85.2 % | 0.178 | 85.6 % | 0.191 |

Figure 3. Comparison of SPIA + No Change vs. SPIA + Modified Portfolio: Balanced Allocation

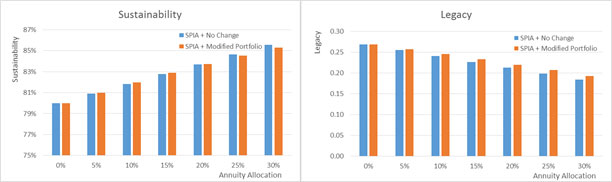

Figure 4. Sustainability & Legacy vs. Annuity Allocation (Balanced)

Table 5. Results for an Aggressive Portfolio

| Allocations to Investment Account & SPIA | SPIA + No Change | SPIA + Modified Portfolio | ||||

| Investment Account | SPIA | Retirement Sustainability | Financial Legacy | Retirement Sustainability | Financial Legacy | |

| 1 | 100 % | 0 % | 80.0 % | 0.269 | 80.0 % | 0.269 |

| 2 | 95 % | 5 % | 80.9 % | 0.255 | 81.0 % | 0.257 |

| 3 | 90 % | 10 % | 81.8 % | 0.241 | 82.0 % | 0.245 |

| 4 | 85 % | 15 % | 82.8 % | 0.227 | 82.9 % | 0.233 |

| 5 | 80 % | 20 % | 83.7 % | 0.213 | 83.7 % | 0.220 |

| 6 | 75 % | 25 % | 84.6 % | 0.199 | 84.5 % | 0.207 |

| 7 | 70 % | 30 % | 85.6 % | 0.185 | 85.3 % | 0.193 |

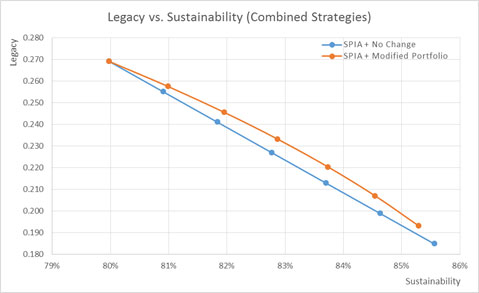

Figure 5. Comparison of SPIA + No Change vs. SPIA + Modified Portfolio for an Aggressive Allocation

Figure 6. Sustainability & Legacy vs. Annuity Allocation (Aggressive)

Results and Discussion

After this analysis, what have we learned? Here is the main takeaway: when annuities are added to a portfolio, the sustainability of a client’s retirement income plan is increased – both when the asset allocation within the investment portfolio is unchanged, and when the asset allocation is modified to match the client’s overall risk profile.

Additionally, when the client purchases an annuity and her portfolio is modified to match her overall risk profile (the “SPIA + Modified Portfolio” cases), both the legacy and sustainability of her strategy are improved – whether the investment allocation is conservative, balanced or aggressive. This result is explained by the fact that annuity allocation, acting as a portion of the fixed income allocation of the retirement portfolio, allows our client to take more upside exposure (more equities) within her managed account.

Taking this specific point further, we note that when the client has an aggressive investment portfolio, beyond a certain annuity allocation the “Modified Portfolio” strategy does not provide any additional benefit over the “No Change” strategy. (See the allocation of 10% to annuities in portfolios three and four on Table 5, and note the sustainability and legacy scores for these two portfolios.) This is explained by the fact that at a certain point, taking additional risk within the investment account exposes the client to significant downside that cannot be overcome by further annuity purchases – as that will move the client away from an overall aggressive investment profile. Note that given our assumptions and parameters, the highest sustainability scores are obtained by annuitizing 30% of the initial portfolio while adopting a balanced portfolio allocation and modifying the portfolio to take the annuity allocation into account (Table 4), and from annuitizing 30% of the portfolio while adopting a conservative portfolio allocation without modifications (Table 5) – both give an RSQ score of 85.6%.

Finally, the analysis presented so far is for a female aged 65. How do the results change at earlier or later ages? In Table 6, we show values for a female age 60, and age 70; compared to our original 65- year-old client.

Table 6. Results for Additional Ages (Monthly SPIA income F60 = $353.60 and F70 = $472.05)

| Age | Investment Portfolio Asset Allocation | Product Allocation | SPIA + No Change | SPIA + Modified Portfolio | |||

| Investment Portfolio | SPIA | Sustainability | Legacy | Sustainability | Legacy | ||

60 |

Conservative | 100.00% | 0.00% | 85.7% | $0.344 | 86% | $0.344 |

| 95.00% | 5.00% | 85.8% | $0.322 | 86% | $0.324 | ||

| 90.00% | 10.00% | 85.8% | $0.300 | 86% | $0.304 | ||

| 85.00% | 15.00% | 85.9% | $0.278 | 87% | $0.284 | ||

| 80.00% | 20.00% | 86.0% | $0.255 | 87% | $0.264 | ||

| 75.00% | 25.00% | 86.0% | $0.233 | 87% | $0.244 | ||

| 70.00% | 30.00% | 86.0% | $0.211 | 88% | $0.223 | ||

Balanced | 100.00% | 0.00% | 88.1% | $0.376 | 88% | $0.376 | |

| 95.00% | 5.00% | 88.2% | $0.352 | 88% | $0.355 | ||

| 90.00% | 10.00% | 88.3% | $0.329 | 88% | $0.333 | ||

| 85.00% | 15.00% | 88.4% | $0.306 | 88% | $0.311 | ||

| 80.00% | 20.00% | 88.5% | $0.282 | 89% | $0.289 | ||

| 75.00% | 25.00% | 88.5% | $0.259 | 89% | $0.267 | ||

| 70.00% | 30.00% | 88.5% | $0.235 | 89% | $0.244 | ||

Aggressive | 100.00% | 0.00% | 88.1% | $0.382 | 88% | $0.382 | |

| 95.00% | 5.00% | 88.2% | $0.358 | 88% | $0.360 | ||

| 90.00% | 10.00% | 88.3% | $0.335 | 88% | $0.338 | ||

| 85.00% | 15.00% | 88.4% | $0.311 | 88% | $0.315 | ||

| 80.00% | 20.00% | 88.6% | $0.287 | 88% | $0.292 | ||

| 75.00% | 25.00% | 88.6% | $0.263 | 88% | $0.269 | ||

| 70.00% | 30.00% | 88.7% | $0.240 | 88% | $0.246 | ||

70 |

Conservative | 100.00% | 0.00% | 85.7% | $0.344 | 86% | $0.344 |

| 95.00% | 5.00% | 86.9% | $0.331 | 87% | $0.333 | ||

| 90.00% | 10.00% | 88.2% | $0.319 | 89% | $0.323 | ||

| 85.00% | 15.00% | 89.4% | $0.306 | 90% | $0.312 | ||

| 80.00% | 20.00% | 90.6% | $0.293 | 91% | $0.300 | ||

| 75.00% | 25.00% | 91.8% | $0.280 | 93% | $0.289 | ||

| 70.00% | 30.00% | 92.9% | $0.267 | 94% | $0.277 | ||

Balanced | 100.00% | 0.00% | 88.1% | $0.376 | 88% | $0.376 | |

| 95.00% | 5.00% | 89.1% | $0.361 | 89% | $0.363 | ||

| 90.00% | 10.00% | 90.1% | $0.346 | 90% | $0.350 | ||

| 85.00% | 15.00% | 91.1% | $0.332 | 91% | $0.337 | ||

| 80.00% | 20.00% | 92.0% | $0.317 | 92% | $0.323 | ||

| 75.00% | 25.00% | 93.0% | $0.302 | 93% | $0.309 | ||

| 70.00% | 30.00% | 93.9% | $0.287 | 93% | $0.295 | ||

Aggressive | 100.00% | 0.00% | 88.1% | $0.382 | 88% | $0.382 | |

| 95.00% | 5.00% | 89.0% | $0.367 | 89% | $0.369 | ||

| 90.00% | 10.00% | 90.0% | $0.352 | 90% | $0.355 | ||

| 85.00% | 15.00% | 91.0% | $0.337 | 91% | $0.341 | ||

| 80.00% | 20.00% | 91.9% | $0.322 | 91% | $0.326 | ||

| 75.00% | 25.00% | 92.9% | $0.306 | 92% | $0.311 | ||

| 70.00% | 30.00% | 93.8% | $0.291 | 93% | $0.296 | ||

Our results confirm that including a SPIA into an individual’s retirement portfolio improves retirement sustainability. This improvement is obtained through a reduction in the lifetime ruin probability of the investment account as the portfolio is not burdened with higher withdrawals and is thus more sustainable. That said, this improvement comes at a price, which can be observed through the reduction in client’s financial legacy.

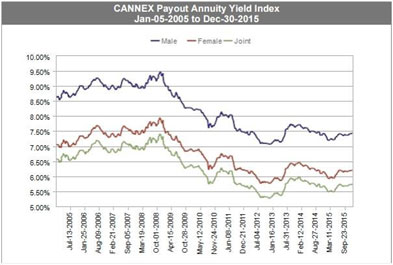

More broadly, this result has persisted even when interest rates and thus annuity payout rates are lower than in earlier periods, such as when the original analysis by Ameriks et al. was concluded. Figure 7 provides an illustration of annuity payout rates in the United States from January 2005 to the end of December 2015.

Figure 7. CANNEX PAY Index – United States

What is the implication for retirement income advisors and their clients? When designing retirement solutions, it helps to focus on the client’s retirement goals: is the client looking for a sustainable income, or is she interested in maximizing a potential legacy? Given that both market returns and remaining human lifetime are random, we propose the use of the Retirement Sustainability Quotient and Expected Financial Legacy (RSQ and EFL) concepts to help advisors evaluate the costs and benefits of including annuities within a retirement income portfolio. We also recommend that advisors and clients consider product allocation strategies to help determine an optimal portfolio on the sustainability-legacy frontier– a topic for a future publication.

1 Ameriks, John and Veres, Robert and Warshawsky, Mark J., Making Retirement Income Last a Lifetime. Journal of Financial Planning, December 2001. Available at SSRN: http://ssrn.com/abstract=292259

2 CANNEX specializes in gathering, compiling and redistributing comparative information and calculations about products and services offered by financial institutions, including, in the U.S., guaranteed lifetime income products such as income annuities. Go to www.cannex.com for more information.

3 See, for example, Peng Chen, Moshe Milevsky, “Merging Asset Allocation and Longevity Insurance: An Optimal Perspective on Payout Annuities”. Journal of Financial Planning, June 2003. Available at http://www.ifid.ca/pdf_workingpapers/WP2003JUN.pdf.

4 We note that our model could incorporate insurer credit ratings, or assume diversification via the purchase of annuities from various issuers. We have not included either of these as they are not central to our main message. 5 More information on QWeMA NumeRIcs is available from CANNEX at www.qwema.ca.

6 See https://www.soa.org/research/experience-study/pension/research-rp-2000-mortality-tables.aspx.

7 Available at https://am.jpmorgan.com/us/institutional/library/ltcma-2016

8 Quotes obtained on December 30, 2015 from www.cannex.com.

©2015-2020, CANNEX. All rights reserved. Republished with permission of Branislav Nikolic, Vice President of Research and Tamiko Toland, Head of Annuity Research at CANNEX. CANNEX’s mission is to provide access and transparency relating to the cost and features of retirement savings and retirement income products offered across the market. CANNEX is an independent and privately held company with operations in Canada and the U.S. that also provides research and thought leadership regarding retirement income planning. No financial institution holds any shares in the company and no CANNEX employee or shareholder receives any income from the sale of financial products. They facilitate the efficient and accurate exchange of pricing and analytics for annuity and bank products between financial institutions.