There are many of them, so we’ll focus on the four primary risks here – retirement risks that we need to manage when creating a retirement income plan.

- The risk you will outlive your savings is longevity risk.

- Inflation risk is that your expenses increase faster than your retirement income over time.

- Health and long-term care costs could become your largest expense.

- Investing risks and your investments’ income and real values fluctuate or decline over time.

Let’s take a closer look at these four primary risks and what you can do to manage them.

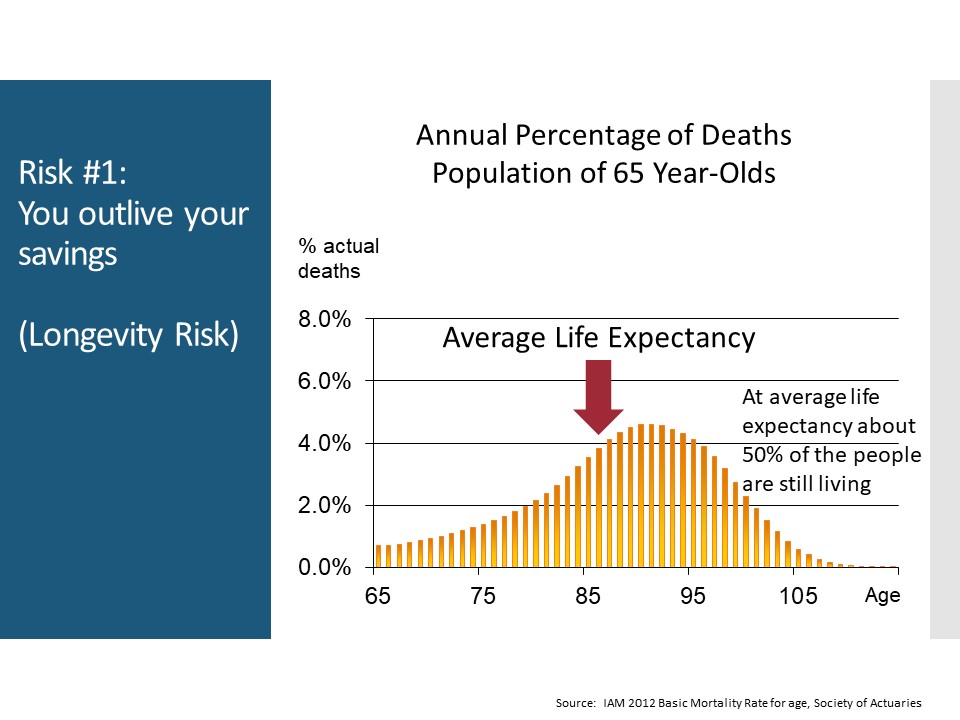

The risk of longevity

This bell-shaped curve represents the percentage chance of dying at a certain age if you’re 65 today. We see that while the average life expectancy for a 65-year-old is approximately 87 years of age, only 4% of the people died when they’re supposed to be based on the average. But at the average life expectancy, about 50% of the people are still living. Remember that averages are acceptable for statistics but are based on groups of people. They have nothing to do with you or me when planning for retirement or other needs.

So, how long should we plan to live in retirement? This is a critical question that everybody needs to evaluate on their own. But today, one thing’s certain. People live longer, and most, if not all of us, should be thinking about planning to live 10 to 15 years beyond the average life expectancy. You need a cushion because if you live long, you’ll have it. If you don’t need the cushion, then your children can have it.

A 65-year-old male has a 95% chance of living to age 70. A female has about a 96% chance of making it to age 70. For a couple both age 65 today, there is almost a 100% chance that one of them will make it to age 70. At age 85, which is close to an individual’s average life expectancy, there’s more than an 80% chance that one of a couple will still be alive. At age 95, there’s about a 30% chance that one of the couple will still live. Those are pretty good odds.

And if one of you does get there, who is it most likely to be? Yes, women do live longer than men typically, but that’s not a guarantee. Nevertheless, did you know that 73% of women age 85 and older are widows? And 2/3 of Americans over age 65 living in poverty today are women. But since we don’t know for sure who will die first, you need three plans. One for if you both live longer than expected, which of course, is the plan you want. But also, you need one for if he dies first, and also if she dies first. And realize that when a spouse passes away, expenses don’t get cut in half.

The risk of inflation

In this case, we’re looking at an individual or couple whose expenses in year one of retirement are $60,000. Over a 30-year retirement at just 2% inflation, their expenses come very close to doubling: they’re $106,000 after 30 years. And if inflation happens to be at 3% – and by the way, inflation for retirees typically is higher than when you’re working because typically healthcare costs at 3% inflation are $60,000 – their expenses more than double to $141,000.

Over time, inflation works against us precisely in the same way that compounded interest works for us during the accumulation years. In this case, however, the longer you have inflation working against you, the harder it works against you due to the compounding effect of inflation. It happens a little bit each year but begins to add up over 25 to 30-year retirement. So, when it comes to your retirement savings, it’s essential to be thinking more about preserving purchasing power than conserving capital.

Healthcare and long-term care costs

Forty percent of men 65 and older will need long-term care during their lifetime; it’s 58% for women. And the average number of years men will need long-term care is 1.5 years; 2.5 years for women. So, only about half of the people need long-term care, but I guess you have to ask yourself if you’re willing to flip a coin to determine if you’ll need it or not. And although the average need for long-term care is less than three years, those with related cognitive needs and who are otherwise physically healthy may require long-term care assistance for five to 10 or even more years.

You could do everything right, but without a long-term care plan, your savings could be wiped out in a short amount of time. If you’re single, that may not be as big a concern as those who are married, but everyone should want to have some control over their long-term care needs.

Assisted living base rates in the United States today are $48,612 a year. Home healthcare, if you have somebody coming to your home to take care of you is $23 an hour. And for a long-term care facility, the average semi-private room costs just a little over $90,000, getting close to $100,000 per year.

Market risk

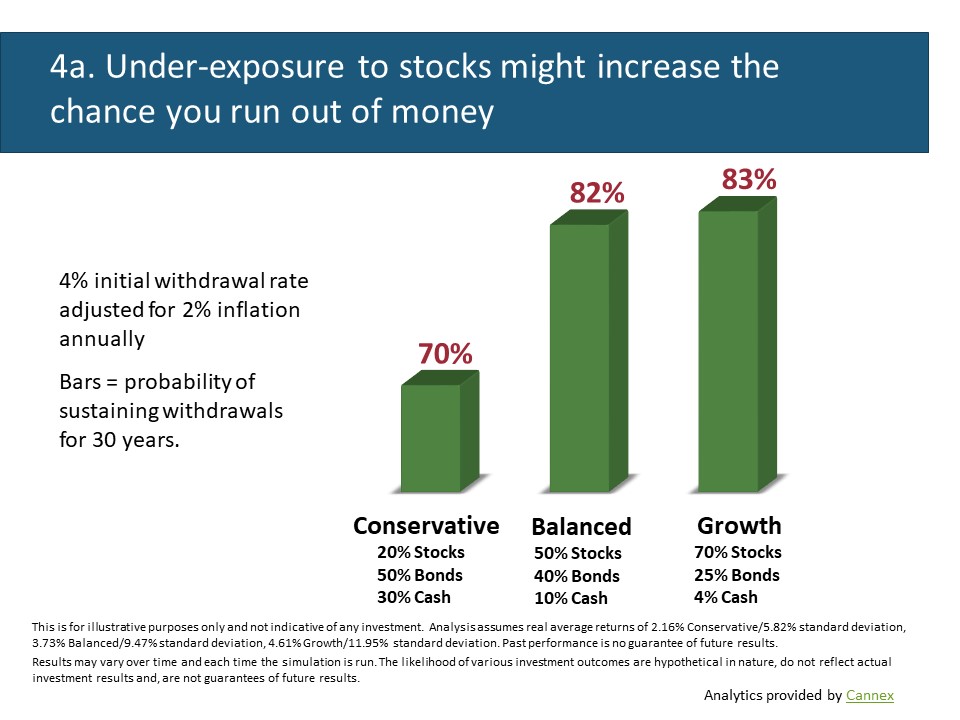

Underexposure to the stock market and experiencing losses in the early years of retirement can impact your retirement income plan.

A systematic withdrawal plan or SWP is where we start by taking 3% or 4% from savings in the first year of retirement and then increase that amount every year for inflation. It may be sustainable over a 30 to 40-year retirement, depending upon your equity allocation. To state the obvious, the higher the initial withdrawal rate, the lower the chance of sustainable lifetime income.

For example, assume you take an initial withdrawal rate of 4% of the portfolio adjusted for inflation. On $100,000, the initial amount taken in the first year would be $4,000, and that dollar amount would be adjusted for inflation each year after that. Again, we’re using a 2% assumption for inflation. The bars show the probability of savings lasting 30 years when invested in a conservative, balanced, or growth portfolio, going from left to right. When looking at the conservative portfolio, lower returns and inflation has a more significant impact on your ability to beat longevity risk, and savings only has a 70% chance of lasting 30 years.

But when investing in a balanced portfolio, there’s an 82% chance of the portfolio lasting 30 years. Of course, the challenge is that to increase the chance of success, you need to assume more short-term market risk. You can see that when investing in the growth portfolio, there’s only a 1% increase in the percentage chance that savings will last 30 years when compared to the balanced portfolio (83% compared to 82%). So, this tells us that, at some point, further increasing a portfolio’s market risk would not be very helpful. The one thing about a SWP is that regardless of how we invest, there are no guarantees.

How Much Will I Need in Retirement?

How much you spend in retirement has the most significant impact on how long your savings will last. Studies show that the average American today should replace 75% to 80% of their income when they retire.

If we assume your pre-retirement income is $60,000, let’s assume we’ll replace 80% of your income so you may spend $48,000 a year in retirement. That may sound like a good and easy way to determine your retirement income needs, but unfortunately, it’s not very helpful. The problem with this approach for determining the most crucial retirement planning question you need to answer is that, again, it’s based on an average. A person or couple who currently makes $150,000 may only need to replace 60% of their income, and a person or couple who makes $30,000 may need to replace 100% of their income.

So, by going through a budgeting process, you’ll be able to come up with the best answer to how much you’ll need in retirement. It’s critical to do this. Otherwise, it’s just a guess, and if you guess wrong, you won’t realize it in the first five years of retirement but instead in the last five years when it’s too late to do anything about it.

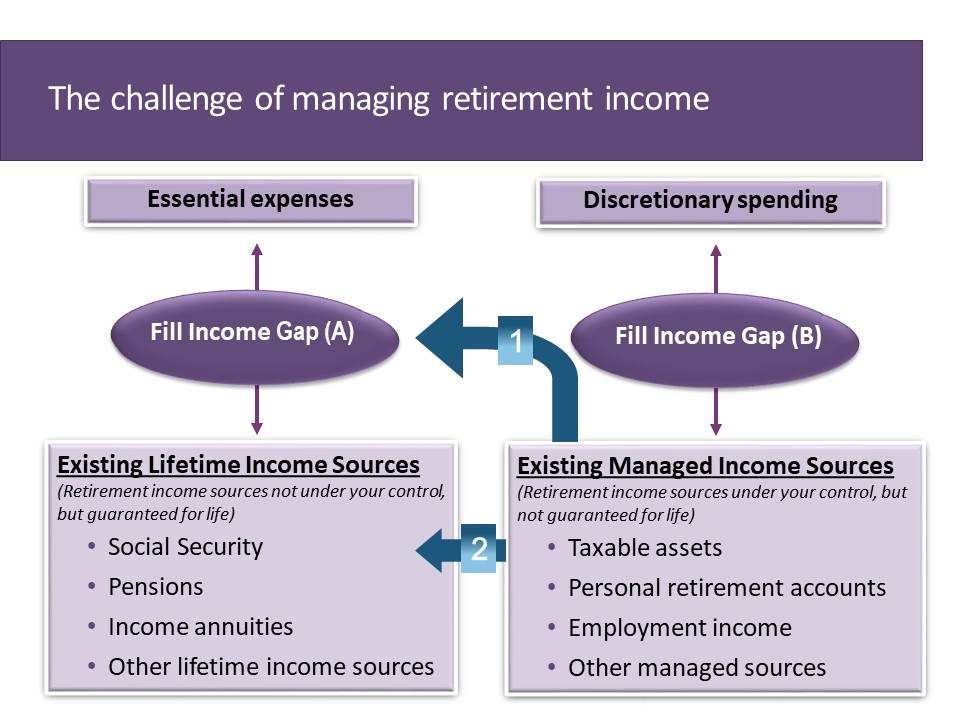

This is an important slide because, more than anything else, it helps us understand how to create a retirement income solution. It starts by taking budgeting for retirement one step further by breaking down your expenses into the two categories of essential expenses and discretionary or lifestyle expenses.

If you don’t have enough lifetime income sources to meet your essential needs, then the first challenge is to fill “Gap A,” as indicated on the slide; and you fill that with other lifetime income resources.

Once we have a plan to fill “Gap A,” we need to see if we have a “Gap B,” which is the gap that may exist between our discretionary or lifestyle spending goals and the rest of our nest egg, which may include your 401(k), IRAs, other savings and investments you have. For a while, as you transition into retirement, it may also include employment income.

If after that you have filled “Gap A” but still have a “Gap B” when you’re getting ready to retire, you have an essential question to answer, which is, “Do you want to retire now with the savings you have or save more to have the retirement you want?” The answer to that question determines what you do next.

As you determine your income needs in retirement, keep in mind that you may have different phases of spending patterns. For most retirees, determining how much you will spend in retirement doesn’t mean figuring what you’ll need in the first year of retirement and then plan on the same spending increase for inflation each year. If you think about it, retirees typically spend more in their early years of retirement because they’re, again, traveling and checking things off their bucket list. We call these the “go-go years,” and it’s when your discretionary expenses typically are going to be at their highest. At some point, however, although you maintain a high degree of activity, spending slows down, and you enter what we call the “slow-go years.”

And then, for the latter stage of retirement, you will become less active as health and other issues impact your mobility, and you’re in the “no go years,” which doesn’t mean by the way you can’t have a “go-go” moment once in a while. It is also important to realize that in the “no-go years,” if there are higher than expected health or long-term care costs and you have not managed those risks, your total inflation-adjusted expenses could be higher than they were in the “go-go years.”

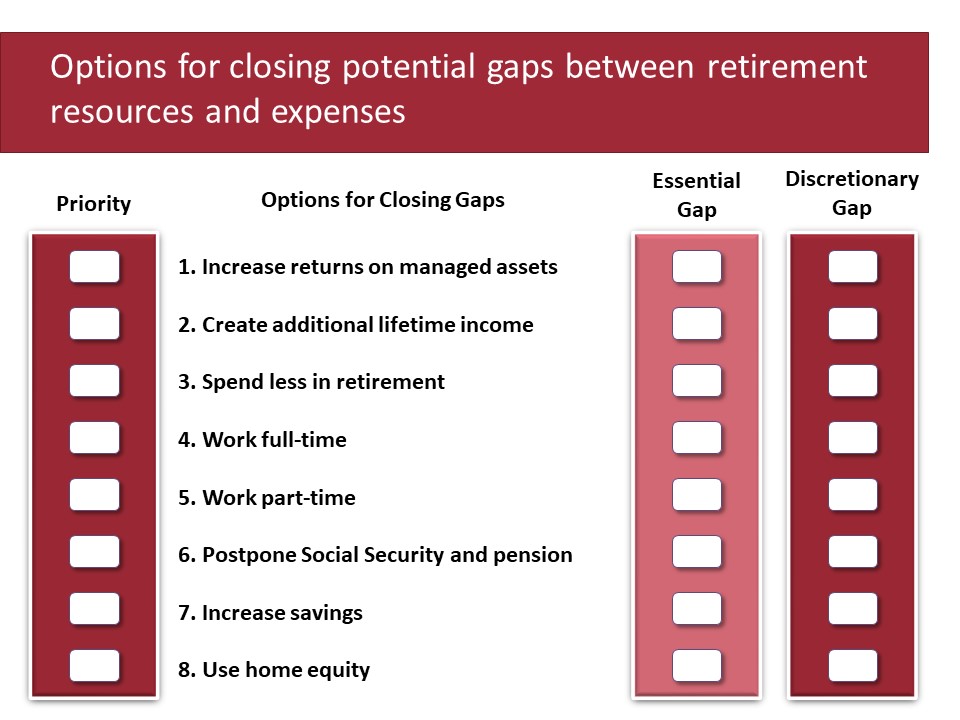

Options for Closing Retirement Income Gaps

You may have gaps between your essential needs and lifetime income sources or between your discretionary needs and managed income sources. Here are the eight options to consider for closing retirement income gaps. Once you determine which options are on the table and off the table, you can then determine how to prioritize them and use them to fill essential and discretionary needs. In many cases, it’s going to be a combination of options that you need to consider and adopt.

Option one is to increase returns on managed assets. Although it would be difficult to fill a five or 10-year income gap by just adjusting how we invest our retirement resources, it’s always going to be a good place to start. Many retirees like to avoid the stock market in retirement, and I get it; they want to preserve everything they earned and not take risks. But as we saw earlier, underexposure to stocks might increase the chance that you run out of money. By trying to avoid the short-term risk of the stock market, the tradeoff is that you’re just trading stock market risk for longevity, inflation, and maybe even a little healthcare cost risk. The key is to find the right balance in your investment portfolio to manage all the risks and give you the best opportunity for success over a 30-year retirement.

Option two is to fill gaps is to create additional lifetime income. As we saw earlier, when looking at the importance of using lifetime income sources to fill essential needs, one option for creating lifetime income was an annuity. So, how does an annuity work? Well, it’s a lump sum investment typically with an insurance company, and then the insurance company will send you a check every month for life. But the payments stop upon the death of the owner or the joint annuitant. Why do they work? Some people live longer than others, and those who live longer receive the unused investment of those who die earlier.

Annuities work just like your life, car, and homeowner’s insurance. All insurance allocates premium payments for those who don’t experience a risk to those who do. In this case, we’re insuring against longevity risk, and people who don’t live as long help provide lifetime income to those who live longer. In this case, the tradeoff is if you happen to be one of those who die earlier, you may not get back all the money you invested in your annuity. For that reason, many people don’t like annuities. But remember that we need to plan for if we live longer more than if we die earlier.

Also, there are other advantages to using an annuity to create lifetime income for essential needs. Generally, you can safely receive more money annually for a dollar annuitized than what you could take if you managed it yourself. And the insurance company must keep paying you even if you live so long that your initial investment runs out.

Option three for closing income gaps is to spend less in retirement. Do you want to retire now with the savings you have or save more to have the retirement you want? It comes down to either decreasing your spending goal so that you can retire earlier or continuing to work so that you can keep growing your nest egg.

Options four and five are to retire later or work part-time. Just remember that if you decide to continue working during retirement, you must ask yourself if work will be available and will you be able to continue working. One study found that the percentage of workers planning to work in retirement is 74%, but only 25% of retirement age people were still working.

Our sixth option for closing potential income gaps is postponing Social Security and pension benefits. In this example, we’ll evaluate the Social Security decision, but many of the same considerations apply to those with a pension. Social Security benefits can still start as early as age 62 and be delayed to as late as age 70. The amount received relates to your full retirement age, or FRA, which today is going to be age 66 or 67, depending upon when you were born. If a retiree’s FRA is age 67, they will receive 30% less than their FRA amount if they start their benefits at age 62, and 20% less at 64.

The key factors to consider are certainly health and longevity risks. Another factor is the breakeven point between the total income received if you took less starting at age 62 versus waiting until your full retirement age. That breakeven point is around age 78. In other words, if you start Social Security at age 62 and receive $14,000 per year for 16 years until age 78, it will be very close to the same amount you’ll receive if instead you start benefits at age 67 and receive $20,000 per year for 11 years until age 78.

If you tell me when you’re going to die, I’ll tell you when to start Social Security benefits. If only it were that easy. Did you know that if you were born after 1943, you could receive an 8% increase in monthly benefits for every year you delay taking Social Security benefits past your FRA up to age 70? This can make a big difference because you would now receive $24,800 a year at age 70 versus $20,000 at age 67. By the way, there’s no benefit to taking Social Security benefits after age 70. You wouldn’t want to wait later than that.

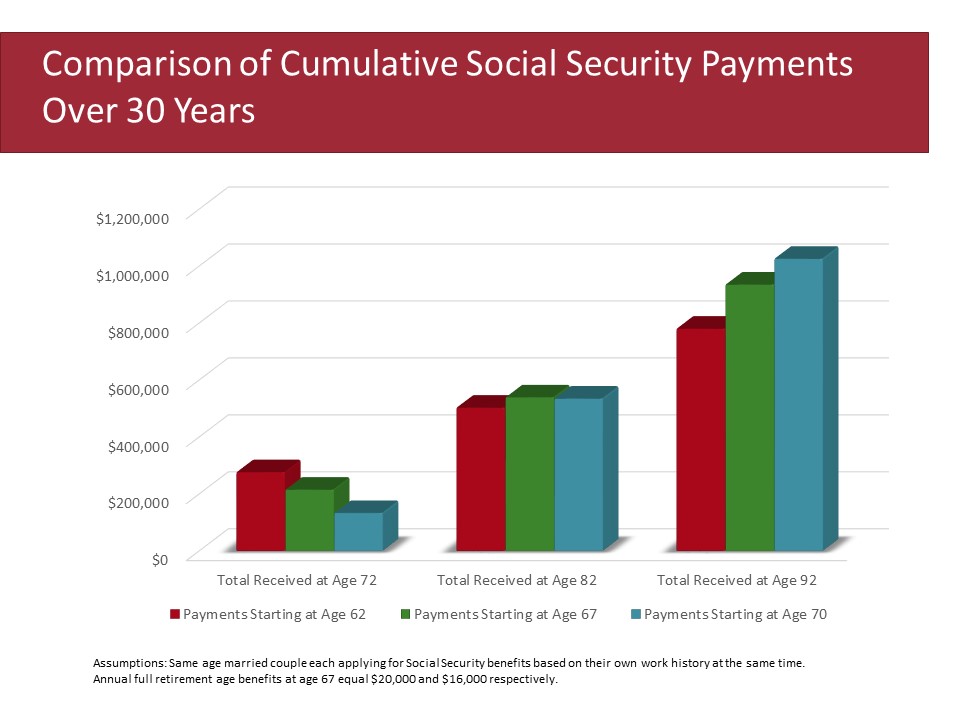

The decision for when to start Social Security benefits can be rather complicated, but – and this is important for most people – delaying Social Security can probably have the most significant impact on filling income gaps. Let’s look at an example. The red bars represent the combined totals of a couple with a full retirement age of 67 receive from Social Security if they started their benefits at age 62. The green bars are the totals received if they started at 67, and the blue bars are the total they received if they waited until age 70 to start.

Notice that at age 72, the total amount received when starting benefits at age 62 still beats the totals from age 67 or 70. That makes sense because if they waited to age 70 to start, at age 72, they’ve only received benefits for two years. But at age 82, in the middle, things start to change. They’ve passed that breakeven point at about age 78, so the total received by waiting to start at age 67 is more than if they started at 62. Because delaying benefits until age 70 gives them so much more per month than if they started at 62 or 67, the blue bar to the right shows a total amount received at age 92 of almost $1,000,000 compared to a little more than $900,000 for the green bar. They will receive less than $800,000 for the red bar, again, showing if you started at age 67 or 62, respectively.

The seventh option for closing potential income gaps is to save more for retirement. If you remember to think of your savings as last in, last out, meaning that the last money you save before retirement will be the last money you spend later in retirement or the money your children will inherit. For example, if you saved $50,000 from age 60 to age 65, it may grow to as much as $135,000 at age 80. That amount could go a long way toward filling future potential income gaps in the “slow-go years.”

Our last option for filling retirement income gaps is tapping into home equity. For most people, their biggest asset is their home, especially when their mortgage is paid off. One question to ask yourself is to consider downsizing your home either at the time of retirement or in the future. If that answer is yes, let’s assume you have a $500,000 home with no mortgage; if you downsize to a $300,000 home, that could free up $200,000 for your retirement spending goals. Some may also decide to rent after selling their home so that they don’t have the responsibility for ongoing maintenance, or to give them the flexibility to move again later if needed. The third way of tapping home equity today is to obtain a reverse mortgage.

Essentially, a reverse mortgage is exactly what the name implies. Instead of paying the bank a monthly payment and increasing your home’s equity, the bank pays you monthly, and your equity decreases with each payment. Many are reluctant to use home equity for living expenses. But for those who want to stay in their family home and find themselves running short on resources later in retirement, a reverse mortgage can be a wonderful option for creating needed income. Going back to the idea of selling your home and downsizing, a certain kind of reverse mortgage will also help you buy a new residence with the reverse mortgage, freeing up some of the proceeds from the sale of your prior home for retirement expenses.

Using a reverse mortgage is also another way to think about paying for potential long-term care needs of one spouse while allowing the other spouse to continue living in the home. Certainly, there are fees to consider when purchasing a reverse mortgage. But one of the benefits is that some reverse mortgages are federally insured so that when you leave your home, you never have to pay the bank more than its value.

How to Create a Retirement Income Plan

When it comes to creating a retirement income plan, figuring out how to convert retirement resources into income is where the rubber meets the road.

Remember we talked about a systematic withdrawal plan or SWP for withdrawing funds from your managed asset sources. We start by taking 3% or 4% of your savings in the first year of retirement and then increasing that amount annually for inflation.

To create more lifetime income for essential needs, we also talked about the benefits of using an annuity to fill “Gap A.” Something else to consider is that it’s not an either/or decision. Just like when we want to diversify our investments when saving for retirement, it’s probably a good idea to think about how we can diversify our retirement income plan by using a combination of both a SWP and an annuitization to help us get the best of both worlds. Let’s see how that might work.

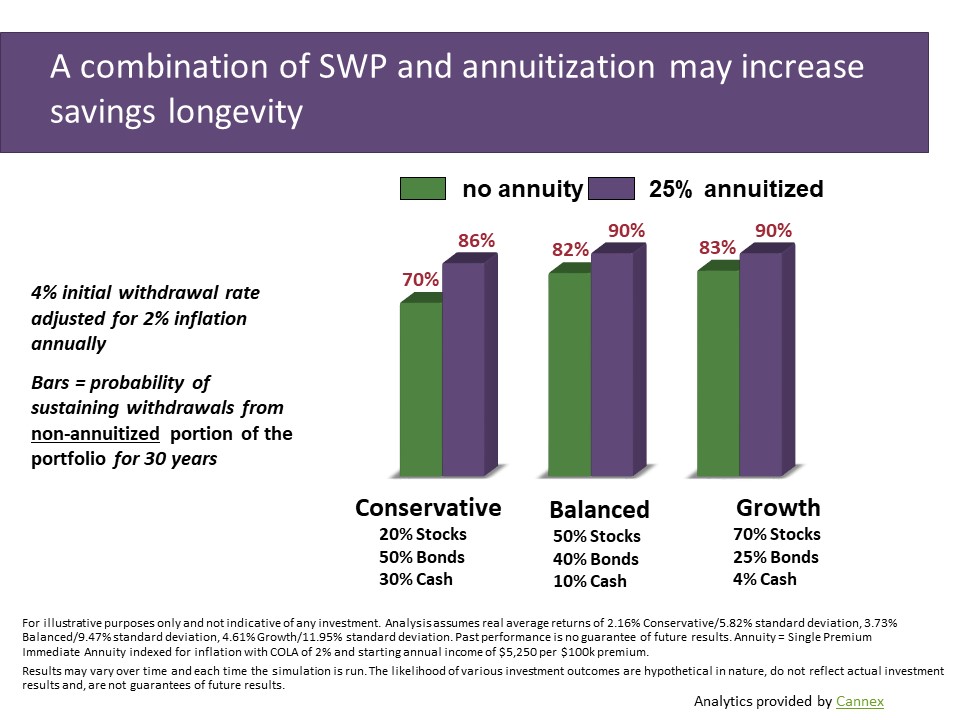

In this slide, the green bars indicate the percentage chance of various portfolios lasting 30 years when using an initial withdrawal rate of 4% and adjusting for 2% inflation.

The purple bars show that by purchasing an income annuity with 25% of the savings, we have created a guaranteed income source to pay for essential needs, and we have also potentially increased the percentage chance that remaining non-annuitized savings will last 30 years. How can that happen? Well, remember that in addition to creating a source of lifetime income, another advantage of the annuity is that you can safely receive more money annually for a dollar annuitized than what you could take if you managed it yourself.

So we’re getting a higher percentage of income than 4% from the annuity, and therefore we can take less than 4% of the remaining savings. As a result, when looking at the conservative portfolio, we see that there’s a 70% chance that the portfolio will last 30 years without the annuity. But when adding the annuity to the mix, you have a source of guaranteed income created with 25% of the savings, and the rest now has an 86% chance of lasting 30 years. We’ve now created a bar that says there’s a 100% chance that at least some of my savings will last 30 years.

For retirees whose only source of lifetime income is Social Security, and they are concerned about stock market risks, annuitizing a portion of the portfolio can dramatically increase how long the rest of their savings might last. Even the growth portfolio benefits, though not as much. And in this case, the percentage chance of savings lasting 30 years goes up from 82% to 90%. Again, as before, there’s not much additional benefit for taking the additional risk of the growth portfolio.

Key Takeaways

Retirement planning is not one-size-fits-all. Your specific plan for making sure you don’t run out of money before you run out of breath will require an evaluation of your particular facts and circumstances to determine what potential combination of retirement income solutions is best for you.

It’s impossible to predict what will happen over a 30-year retirement. Undoubtedly, not everything is going to go as planned. Therefore, after retirement begins, you’ll want to make sure you periodically review your plan and adjust as needed. Each of these events listed – and others – can significantly impact your retirement plan’s success. Remember that there’s no “set it and forget it” button when it comes to retirement plans. Retirement can truly be the best time of your life if you plan for it to be.

Remember, goals without actions are just dreams; action without goals just passes the time. But goals with action is what changes your life.