Starting a conversation about aging or becoming unable to manage incapacities is challenging for planning for extended and long-term care. Today I’m going to offer you a framework: 3 Simple Steps. I hope they will help you kick-start critical conversations as a professional. I also hope they will help you expand your role since the three steps create relationships with multiple generations in families and friends of the families. Anyone who is going to be involved in caring for someone they love.

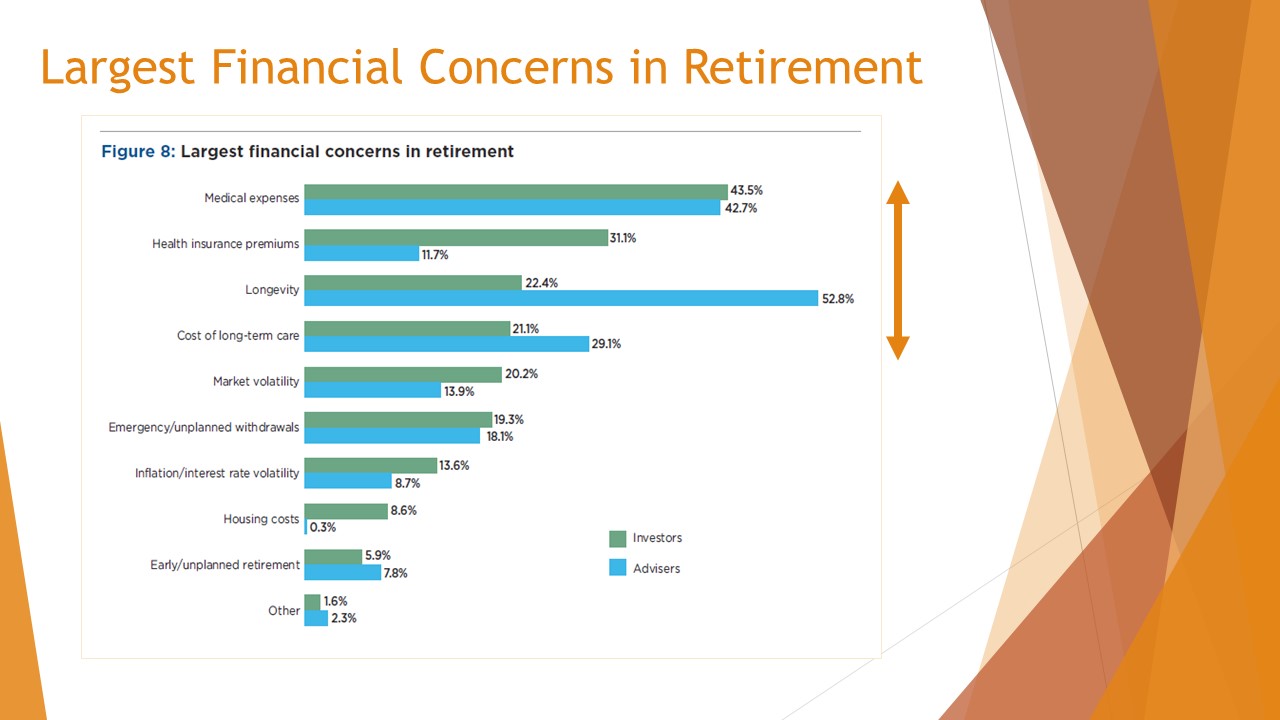

The Largest Financial Concerns in Retirement

This graph shows the largest financial concerns in retirement. The cost of long-term care is listed as one of the largest financial concerns in retirement (number four). The three above it are also intricately linked to long-term care: medical expenses, health insurance premiums, and longevity. All of these things start to become very evident as we get into the aging process and the issues that come along with it.

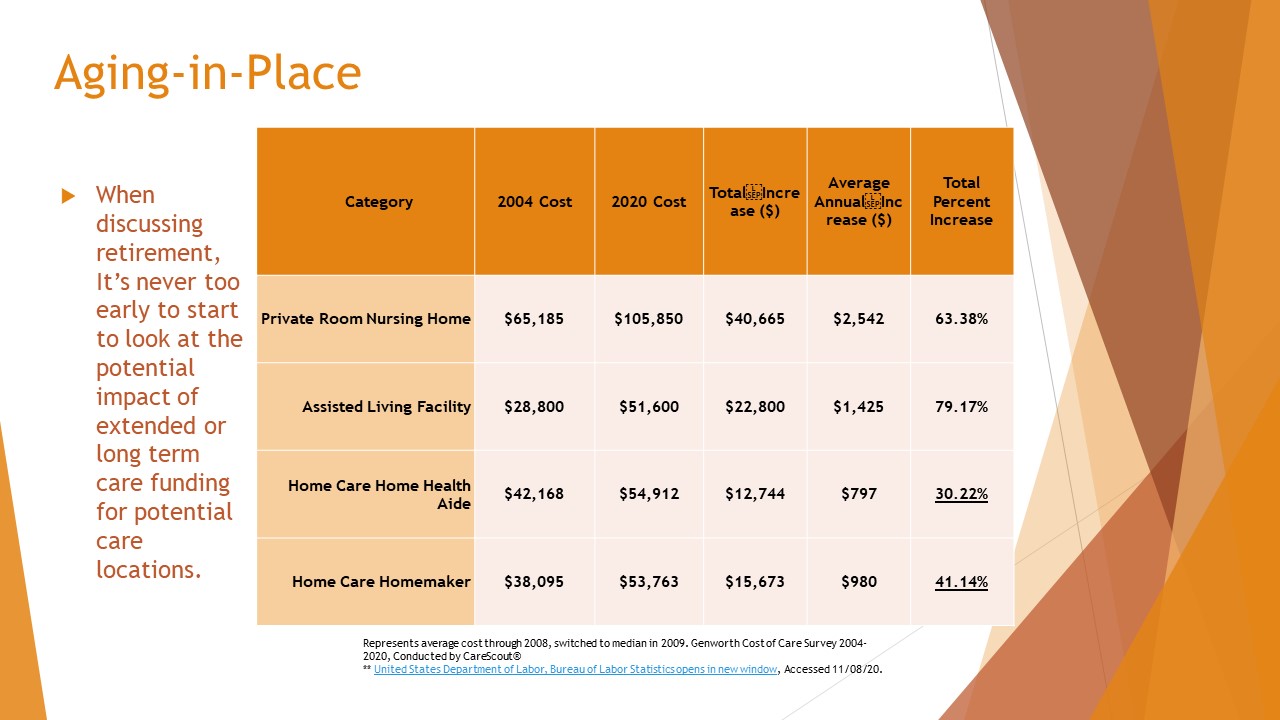

Having seen what we saw during the pandemic, everyone wants to age in place. Everyone. We must include in retirement planning the impact of trying to fund long-term care.

This slide compares the last 15 years’ change in cost. There has been almost an 80% increase in the cost of assisted living facilities in the last 15 years. Take a look at the increase in home care/home health aide cost. Everyone wants to age in place. How will they manage that if the cost for home healthcare aides has increased 30 percent in the last 15 years?

Home Care Homemakers help people manage all of the things involved in aging, such as medication management and paying bills. Those costs have increased a little more than 40 percent since 2004. Do we think that that is going to change?

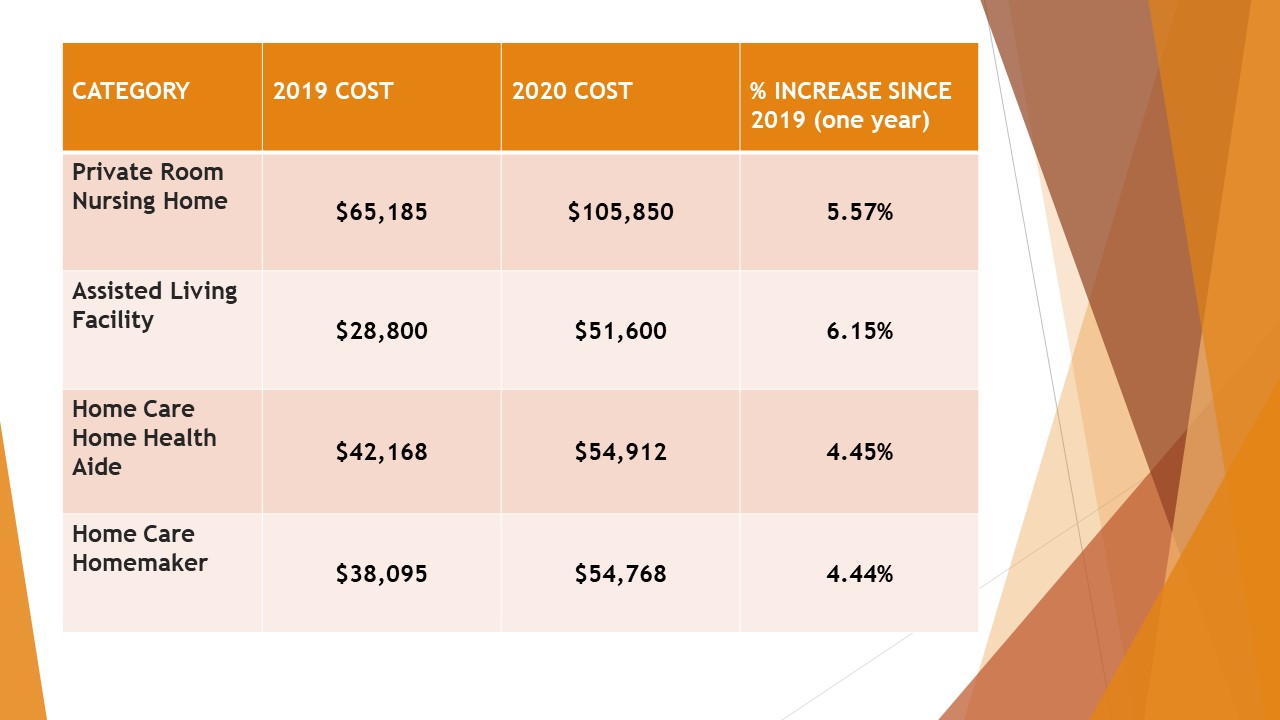

Let’s look at the increase in costs of just this one year, 2019 to 2020. Specifically, see what’s happening with assisted living facilities. The bottom line, aging in place is going to be expensive.

Ask your clients their thoughts about where they expect to retire. How far are they going to be from family and friends? Are they going to be able to afford an assisted living facility or a CCRC (continuing care retirement community)? What exactly do they have in mind? How many physical limitations will they have?

Longevity is Redefining Retirement

Let’s now address the effect of longevity because here is the crossroads between long-term care, extended care, and retirement planning. The increases in longevity are genuinely unprecedented. I recently saw John Hancock’s Vitality research; Vitality is a wellness program. With 50 years of research and data, they have concluded that while people live longer, they’re not necessarily living healthier.

Funding longevity in retirement is a significant cost of retirement. Extended and long-term care absolutely must be included in planning, and it should also include long-term care.

The question is: Are your future clients involved? Will your client become what I call a presumptive generational caregiver?

We will go through a book I wrote (available on Amazon) that uses a story. The main character, Jody, is typical of most caregivers. Her parents are living in their home. Her dad is in pretty good shape; her mom is more wobbly and not all that steady on her feet. Jody is the on-call caregiver.

We will go through a book I wrote (available on Amazon) that uses a story. The main character, Jody, is typical of most caregivers. Her parents are living in their home. Her dad is in pretty good shape; her mom is more wobbly and not all that steady on her feet. Jody is the on-call caregiver.

As so often happens, when people begin to feel the effects of poorer health and aging, they become more dependent. What was just a phone call now becomes an on-site caregiving responsibility. You have to drive over and help them with certain things. Maybe they don’t want to drive long distances on a highway. Maybe they need help going to the doctor. It’s very gradual.

There is also an “on a flight” caregiver. When my mother needed care, my sisters and I all lived in different states, and none of us lived where my mother needed care. We became “on a flight” caregivers. And if you think that that doesn’t interrupt funding retirement, maybe you haven’t had the experience yet.

In 2017, caregiving provided was worth about $470 billion, according to AARP. Can you imagine how much is being devoted to caregiving not only in terms of money but of hours?

What is the real issue? The real issue is starting the conversation with clients. Right along there with them, I don’t want to talk about aging and needing help, etc. I have created a book that is a story because storytelling is telling. You, the advisor, can step into the role of a moderator, sometimes a mediator (unfortunately), sometimes a facilitator, or a guide along the way so that as they’re looking at retirement, you bring up the subject. Frankly, it is a fiduciary responsibility. You are helping them with investments, retirement planning, and insurance. You also need to mention extended and long-term care planning because it impacts so much of their lives.

How to Start Conversations with Clients that Address Extended and Long-Term Care

How are you going to start these conversations? When starting the conversations, you must be aware that caregiving, extended care, or long-term care is never done in isolation. While people retire from work, they do not retire from their families, and they may find that their family will have to help them through this.

This is beyond just a math problem. We already looked at the rising costs for aging in place or going in a facility or, frankly, needing nursing care. But it’s more than that. In my book. Jody is caught up and is already the on-call caregiver, and she’s heading straight towards being the full-time caregiver.

Why haven’t they started the conversation? Parents often aren’t sure how to approach it without sounding as if they do not want to share this situation. Maybe they’re in denial. Jody isn’t starting the conversation, but she wonders if her parents are even sharing the current needs, let alone where they’ll be in the future, or if they even have plans.

The rest of the family doesn’t know how to discuss this either. They’re seeing the impact on Jody, and they don’t want to sound invasive. In addition, Jody has two children. The two children don’t want to say to their mom, “Well, don’t you want to talk about this?” Because they don’t want to have Jody think that they’re being critical.

What’s the reality of what’s happening to Jody? Almost all caregivers wind up impacting their work on their career. So many will also wind up being forced into giving up work entirely.

In Jody’s case, it is her children who notice that not only is their mom now out of the running for her promotion, but she’s not eating right. She has given up going to the gym. She is not visiting with her children, and Jody has young grandchildren. But Jody is caught. She’s the sandwich generation, and the sandwich generation is now becoming a club sandwich because it’s four generations involved in extended and long-term care.

We’re starting to realize how many people retired early during the pandemic, and we weren’t anticipating this number of Baby Boomers to retire. We all know that when they retire, it starts to impact the retirement plan. Whether you’ve worked with them as to whether they’re going to retire or not, it falls on the retirement plan to support it.

I don’t have to tell you that the caregivers may be sacrificing years of future earnings and contributions to the investment accounts you manage, to the retirement plans you have so carefully put together, to the insurances that you thought they would purchase or ladder as they got older.

An early retiree making $80,000 per year forgoes about $80,000 in savings over a decade. By the same token, they’re now missing out on the 5 percent of salary contribution to the employer-sponsored plan. If they were also earning a retirement match that now they’re not, that just exacerbates the entire thing.

So now you have clients who are retiring. If your client isn’t the one retiring, they have retired parents. Again, it’s a trickle-down effect.

3 Simple Steps Provide a Planning Framework for Consumers/Clients to Seek Advisement

Planning for extended and long-term care is a generational problem. I went into some detail about each generation in the book because, as we know, where you come from determines how you interpret and how you learned words. Each generation learned things according to the environment they were in. There will be many boomers who are going to live a long time and who are going to depend on either Gen Xers or Millennials and Silents who will depend on Boomers. That means when you’re talking about extended and long-term care, you will have to learn to work with all of these different generations.

During my career, I noticed that if consumers had any knowledge about extended and long-term care, they tended not to talk about it or would walk away if only one solution were offered. So, I broke down the process to talk about care into three steps. Frankly, it doesn’t matter which step you start with, whether you start helping them create a care guide, a care squad (which is inclusion for people in the family), or a care planning team.

Let’s talk about Step One: The Care Guide. Life can only be understood backwards, but it must be lived forward. Family members may not remember what you said as an advisor, but they will remember how you made them feel. The process of suggesting that they create a care guide is a perfect ice breaker. Why? Because when you talk to them about the care guide, you’re not just talking about healthcare.

For Jody, she needs to determine if her parents have a do not resuscitate (DNR) order in place. She needs to find out the family’s history and find out if their wills are up to date. The care guide is far more than just what is your current medication.

What is Jody gaining? She’s gaining insight into her family’s medical history on both sides of the family. This can be a non-invasive exercise because they don’t have to share everything. In my book, one of the granddaughters helps the grandfather put it all together, but he holds back a certain amount, and Jody is aware of that. The grandfather has the option to share some of it with just his advisor and maybe his daughter – preferably the three of them.

So, why are you, the advisor, helping with this? It’s a caring conversation, and it uncovers facts and influencers for various generations of the families who will face retirement and who need to start to plan.

What about Step Two: The Care Squad? What do we work for, if not to make life less difficult for each other? That’s the “what if” conversation. In the book, I shared that in planning for parents, sometimes – as in the case with my husband – he was made the executor of his mom’s trust. Long story short, he didn’t consult with the brother. He and his brother were at odds quite often. As a result, they’re still not speaking with one another.

The Care Squad is designed so that when an incident occurs – and I assure you in the book, an incident occurs – instead of everybody panicking and running in directions and starting to be counterproductive, it pulls everybody into a role. When you give people a role and responsibility when there is an extended long-term care incident, everyone benefits. Jody won’t be the only caregiver. We saw during the pandemic how overwhelmed many caregivers (the Jodies of this world, the Gen-Xers who were trying to help people who were in care facilities) were and how overwrought they became. Planning for the Care Squad will avoid that. For you, the advisor, you will get to know the generational family members.

In the case of Jody, they brought in a friend – Jackson – because he has been a lifetime friend and can be there in case Jody needs help with her husband or with her father. So, it’s not necessarily just family members, and remember, we defined family in varied ways.

By familiarizing yourself with other family obligations, you can pose specific questions. The book has many questions that you can ask to help make you comfortable bringing up the topic with clients. Unless you can start the conversation and guide it along, it’s not going to be as well incorporated into their retirement plan as it needs to be.

What about the Third Step: The Care Planning Team? “Fight for the things that you care about, but do it in a way that will lead others to join you.” Ruth Bader Ginsburg. This is the discovery conversation. Let’s say you’re not a specialist in this area, so you want your client to be able to read through a story. In this story, Jody assigns to the various care planning team members, her children, her husband, herself, and her father because she needs her father to buy into whatever solution they discover. This step will help your client create a care planning team and review the different available options.

As your clients discover options, you guide, moderate, and facilitate these discussions. You’re not selling them anything. You’re not saying, “Here is the solution.” Ultimately they might say to you, “You know? That’s interesting, and that could work for me. Let’s look more into that.” You would respond with, “Yes, well, that’s a good idea because frankly, the devil is in the details. We need to look at the details. These are just overviews.”

I have included tools, research, links, and sidebars to help individuals and families see you as part of the team as you’re doing these overviews,

When you’re working through this with them, or they’re working through it, and you’re in touch with any one of them, they start to tell you their preferences, and you start to see how they envision growing older. This is a retirement issue. How do you envision yourself? This is all about behavioral finance and how people can envision their future self.

Generational Extended and Long-Term Care Planning

Above are extended and long-term care planning options for healthy people, such as Jody’s son. Jody’s son has two children. His wife isn’t working outside the home, and she’s taking care of their young children. He has a limited budget, and he discovered there is term insurance with an accelerated benefit endorsement rider. Considering that he rides a motorcycle, which completely freaks his wife out, he wanted to have the adviser look into what that would be for him.

Jody’s son is two generations down from where we started helping with the grandparents. The whole idea is that once you get the conversation started by using any of the three steps, you start to not only grow your practice but think of Jody as your client or Jody’s parents as your clients. You are starting to secure their retirement plan because you’re looking at these various options with them, and hopefully, this is going to be something that they come to you and say, “What about this?” You may have to increase your professional network to be able to help. But isn’t that a good thing, not a bad thing?

What if your client has some health issues or budget concerns? Some people just don’t want insurance. They come to you, and they say, “Look, if we invest, then I think I can cover this.” Somewhere along the line, the advisor said to Jody, “Okay, but right now, what if we had to invade your stock portfolio? Is there a good time?” When the market is high and it’s earning well, do you want to pull it out? When the market is low, do you want to pull it out or let it sit, and maybe you’ll recover? But at any rate, do you want to have to do that?

What about the tax implications of suddenly having to invade investments or funds that were growing for retirement, and now all of a sudden, boom, they’re not growing. We all know that changes not only the numbers but the stress level is also terribly impacted by the sudden need to invade investments or retirement funds.

And as we saw earlier, Jody passed up a promotion, which will impact her retirement, especially long term.

What if the parents are genuinely impoverished? We can’t disregard that Medicaid is there. We can’t disregard that there are community, state, and county services that could also be an answer for certain clients, depending on the situation and what the family feels comfortable with.

How to Help Your Clients Not Tear Their Family or Retirement Plan Apart

If extended and long-term care isn’t your area of expertise, please consider sharing the book because in it we offer overviews, links, and resources for the currently available extended and long-term care options. You can get a great deal of insight just from reading the story, but it does mean that if you send this book off to a client, you have brought up the topic.

At this point, if they don’t want to go ahead with it or find that it is not a conversation they want to have with you, well, you tried. As a fiduciary, you certainly took on the responsibility of the impact that extended or long-term care could have on the planning that you’re doing, and you took steps.

Remember, it doesn’t matter how or in what order you use any of this. You’ve broadened your knowledge. Hopefully, you’ve become a generational advisor, and you have helped your client avoid tearing their family or their retirement plan apart.

For most of us, and certainly, for those who help plan retirement, the tricky part is that life doesn’t stop while they’re caught up in caring and juggling their own life. It’s dynamic and ever-changing. No matter how they define caring, no matter how they define family, no matter how they define advice, this book will help them understand that you’re there for them and that there isn’t just one path to security. They may not only put their retirement at risk, but certainly, the impact on those who are caring for them is a big theme that pervades the book as well.

My primary objective of the three simple steps was to offer an easy-to-follow, easily adaptable process to help secure retirement. Stories can simplify complexity, and generational stories allow your clients to identify with characters. Suppose they don’t want to talk about their situation. Let them talk to you about what they saw in the book, how they felt about it.

Successful fiduciary relationships ensue when clients see you as a critical driver and the moderator of a plan. The three simple steps can be used in any order and tell you that if they start with stage two, they’re a little hung up on creating a Care Guide and talking about medical things. Explain to them that a Care Guide doesn’t have to be medical. It can be about their retirement plan and things that can affect their retirement plan.

All in all, each step is your clue and your cue to integrate your value proposition, offer guidance, and put the best solution in place for generations to come.

There are a couple of resources that I wanted to mention. I am the Executive Director of the Limited & Extended Care Planning (LECP) Center. I’d love to have you reach out to me. We have conversations, and we have blogs. We are very much into social media. We do interviews. All in all, it’s a center where we have information that we hope will help you, and we have the legislative working group housed there as well.