Most retirement decisions require more active decisions than we make regarding saving and investing. Even Social Security requires an active decision about how to spend and when to claim from ages 62 to 70.

But even at age 70, Social Security doesn’t automatically turn on, which is very weird, as you don’t get any benefit from deferring past age 70. Social Security, in fact, knows that there are people over 70 who have not claimed Social Security benefits.

We haven’t learned about it, and we haven’t experienced retirement, so we don’t know a lot about it. Thus, Americans are not well-informed about retirement income planning.

The American College recently released a new retirement income literacy survey. It found that 81% of Americans failed a retirement income literacy quiz, with an average score of 42%. Why? Because we learned about saving, not spending. We have yet to retire. We haven’t lived through it. We need to gain experience with retirement income planning. Even though our family and friends can give us some insights into retirement, they are not the best resources for us regarding income, claiming decisions, and distributions.

Even if we look back at our grandparents or parents, they probably lived a very different retirement than we are going to live. This causes behavior bias against spending and retirement. We become fearful of it. We self-insure much risk. We don’t spend what we could spend because we don’t have the knowledge, comfort, or expertise to do that.

The 2023 American College Retirement Income Literacy Survey found a high correlation between increased knowledge about retirement income planning, retirement confidence, and access to a financial advisor. This is a correlation, not a causation-type finding.

What is Retirement Income Planning?

I describe retirement income planning as trying to hit a moving target in the wind. The targets are your and your client’s individual financial goals. We can’t create a great retirement income plan in silo, in a vacuum. We must know the goal: How much we want to travel, what we want to give back to our community and charity, our alma mater, and our grandkids. What’s the legacy you want to leave behind?

Why is the goal moving? I don’t know how long you’re going to live or how long you’ll be in retirement, whether one day or 40 years. The challenge of trying to create a fixed amount of income over an uncertain period of time is what makes the calculations and planning around retirement income so challenging.

There’s wind because there will be things that push us off course: changes in public policy, tax law, inflation, and the market. Our own goals might change.

The Four Percent Rule estimates that you’ll adjust your annual spending for inflation. We know that’s not how spending works, and that’s not how inflation works.

When inflation goes up, we prioritize spending, and eventually, spending and inflation come back down because we don’t just keep spending on the same things. Inflation actually drives behavior to spend differently.

For someone with $1 million, it’s the difference between $40,000 (4%) or $60,000 (6%) in income. When you have $1 million, you think, “I can’t spend an extra $20,000.” Suddenly, we can only spend 6 percent if it feels sustainable. Here’s the thing. There are many ways to get there. Six percent is a sustainable withdrawal rate as long as we take a more adaptive approach.

From a retirement-income approach standpoint, if your income is between $150,000 and $250,000, 60% can be your target replacement ratio. If your income is between $20,000 and $100,000 a year, your target income replacement is close to 80%.

So, based on how much income you make during your working years when your income is higher, you typically need a lower replacement ratio in retirement. It’s a very back-of-the-envelope view. It’s not helpful when we get into an individual plan. The 4 percent strategy, again, one of the most useful, important findings we’ve had in retirement income planning, taught us much information about the sequence of returns risk and gave us a guideline for distributions. Still, it should be something other than what we rely on too much individually. Why? Because we don’t live our lives like the 4 percent model suggests. It’s not how we react. It’s not based on reality. It is a simplistic model that used the technology at the time, but it is super important from a finding standpoint.

Another retirement income approach is what I call my grandparents’ strategy, which is still alive and well today. You all know someone who wouldn’t spend down their principal. What did they spend in retirement? They spent whatever their bonds, CDs, dividend stocks, Social Security, and maybe their pension paid out, and they didn’t spend anything else.

In fact, many people use this approach today. JP Morgan Chase spending data shows that millions of Americans live like this, and they’re very fearful of spending down principal. They self-insure. They’re afraid of this risk. Why? Because they’re afraid of failure. But retirement isn’t about success or failure.

In all these other scenarios, you could run out of money 20 years into retirement, fail retirement, or succeed in retirement. Retirement is not pass/fail. It’s not success or failure. We don’t want to use success or failure language anymore.

We Need Different Ways to Measure Retirement Success

Failure rates, in and of themselves, ignore the magnitude of failure. You live for 30 years in retirement, and you’re one dollar short on the last day of your life. Many people would say that’s a successful retirement. Still, with today’s focus on success rates as an indication of retirement success, it’s considered the same failure as someone who runs out of money in retirement on day two.

There are many ways to look at the average or magnitude of failure. Often, our past science relied on historical returns, which help predict future returns, but they need to guarantee that the way things mesh up together will be different in the future than we have seen. Last year’s first quarter was a very good example of that. We had never experienced the bond and stock market react like that together ever. It was the worst first quarter we had ever seen. That doesn’t mean that historical data isn’t useful. Software firms such as MoneyGuidePro and eMoney allow you to enter your own market assumptions.

Where do we get happiness from spending? That’s often also ignored in four percent distribution approaches. We assume a person should spend the same amount every year, and that’s a good thing. But it probably doesn’t align with happiness. Where do we get the most benefit for every dollar spent?

Retirement is not binary. It’s not success or failure, and neither is life.” And we don’t typically, as Americans, fail in retirement. If you look at Americans, they are very resilient. They are very adaptive. It’s not about IQ and a magic savings number. It’s about AQ, adaptive ability quotient. And what we do in retirement, when we’re running out of money or overspend in a year, we adapt. We cut back on spending. And we’re able to then make assets sustainable. We might not have lived the life we wanted to because we didn’t do the right amount of planning or planning ahead of time, but we adapt. And that’s what life is about. It’s about adapting.

Most retirement income plans that face a shortfall today can be sustained by making small adjustments to the plan. Sometimes, that means adjusting our spending, cutting back in certain areas, delaying Social Security, or working for six months longer. Very small, adaptable changes can make a huge difference. Pushing back retirement for two years would eliminate most of the retirement income shortfall projections in this country.

I’m not saying that this is doable for everybody, but we’re talking about making minor adjustments and, moving away from this language of success or failure and moving to more of an adaptive-based approach. “What’s the risk that we are going to have to change our spending over time?” is the conversation that I think we need to get to as an industry and a profession.

Retirement Income Approaches

You’ve probably all heard about safety-first, systematic withdrawal, and bucketing approaches to retirement income. They’re all a little bit different. I think that we should learn the best things from all three approaches and combine them.

Systematic withdrawal approaches are helpful. They tell us what some sustainable approaches are. They tell us that the sequence of returns risk is really impactful to our plan, and it helps us manage around that. The safety-first approach tells us, “Look, there are expenses we need: healthcare, housing, food. I can’t ignore these. So, I have to have some baseline of income out there.” A bucketing approach says, “We should align our assets to their uses.”

This all leans into the concept of mental accounting, where we treat assets differently based on their nature and origin. We do this with money all the time. In retirement, Americans do the same thing. Why? We were told that our savings should be put aside, that this is the most important thing we could ever do, and we don’t like spending it down.

So, when we get to retirement, and we’re told that we need a distribution strategy to spend down our income, we’re being told to give up on this thing that we attached much meaning to. But if we can come up with that bucket approach, it gives a story and a meaning around the assets that we have, such as our cash might be for Year One of retirement; our fixed income sources, such as annuities, fixed indexed linked annuities, TIPS, or bond ladders can be used to generate income in the midterm. Then, we can put our equity and growth assets in the bucket to obtain further income.

How we project retirement spending and how much we actually spend in retirement don’t match up. They’re very different. When we apply this type of testing to how people live their lives, it’s almost 25% better than expected, which means sustainable withdrawal rates are probably a lot higher than we think they are. By just adapting to the way that people actually live and spend their money in retirement, we can go from a four percent to almost five percent withdrawal rate.

But are you willing to adjust to this? Can you adjust for year 30 by cutting back a little bit in year 13? All of a sudden, it starts changing the conversation. The conversation becomes not about the risk of failure but the likelihood that we will have to adapt to retirement and change our spending. Most people are willing to cut back, and they feel like they can. We should have the conversation about, “What can we cut back on, and can that help us make this more sustainable? What is the risk that we might have to cut back on our wants, needs, and some of our spending for a couple of years?” That’s really the conversation.

Retirement Management means giving Guidance – Not Scores.

The way we have looked at retirement success and failure, static spending, and the four percent rule was based on the technology we had at the time. We were running these scenarios out of Excel sheets on desktops that had one percent of the processing power we have today. The reality is that technology has moved forward. We can run more complex scenarios, and over the next five years, we’re going to have much better technology and solutions from a financial planning and income standpoint than we had even a decade ago.

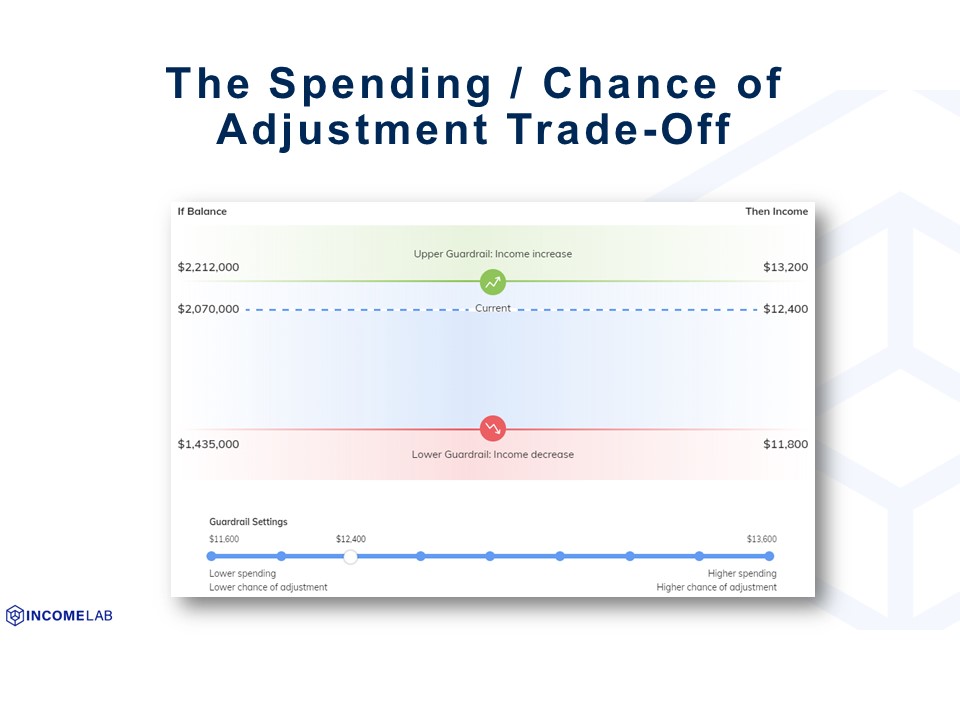

Below is a screenshot from Income Lab, which can implement this adaptive-based spending approach and create guardrails. It’s just one program out there that talks about guardrails.

This idea of an upper and lower guardrail around your retirement income portfolio essentially says, “If our spending and assets stay within these two guardrails, we’re okay.”

That’s a lot of what clients are looking for. Remember, we’re trying to take their fear and uncertainty and give them hope and clarity back. While staying within this spending range, they know they’re okay. But we can spend more money if our assets hit the upper guardrail value. Clients might choose to spend less money, but we will give them permission to spend more money and know that this is still on a sustainable path. Or, if we hit the downside guardrail of account balance, that means, “Look, our funded ratio is dropping too low. We need to adjust.” And that means we need to cut back spending for some time.

And so, you can see current spending and current assets. If our assets hit the upper guardrail, we can increase spending. If our assets hit the lower guardrail, we decrease spending. So, as we’re bouncing in between those ranges, all of a sudden, we know that everything is okay.

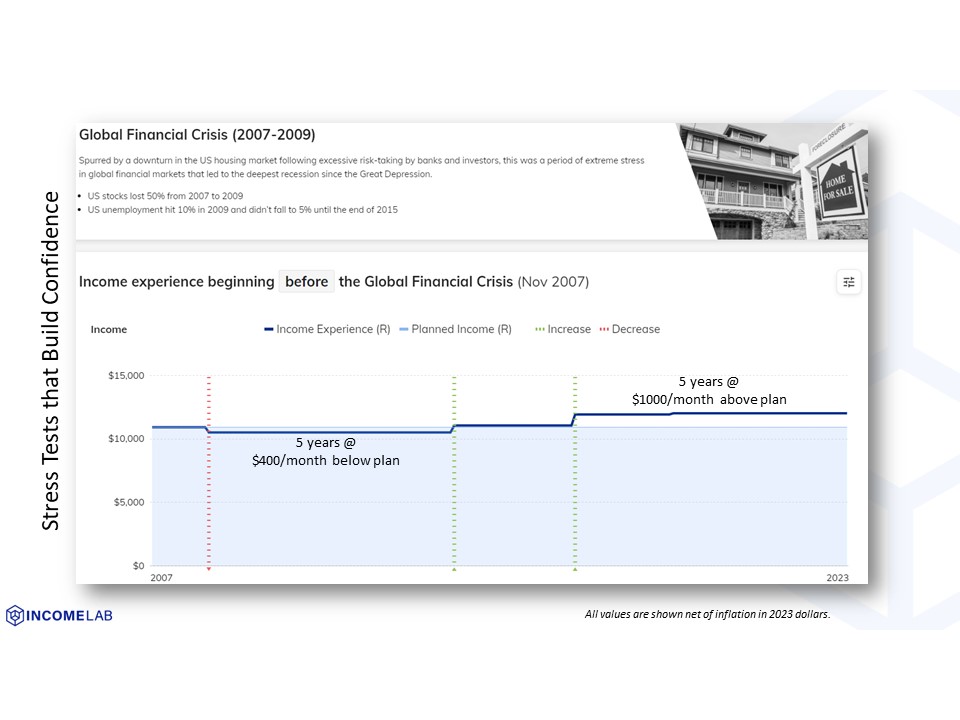

You can look at the global financial crisis and see how a portfolio might be impacted from a guardrail approach. But what you saw is that you wouldn’t have to cut back for very long, and then you would actually have a situation where the income goes back up by more than that after cutting back for a bit.

You might have to cut back $400 a month for five years, below what you were hoping to spend for five years. And in that situation, everything recovered. We know the story. The market then went up, and we could actually increase spending. From 2012 to 2023, we could spend an additional $1,000 per month above plan.

So, total spending over this now almost twenty-year period increased despite retirement, basically, in the financial crisis, by taking an adaptive and guardrail approach to spending. And so, why am I bringing all of this up? Looking at success and failure is not how we live our lives.

Our goal is to build clients’ confidence and tell them they are okay. Adaptive-based and a risk of changing your spending are much healthier ways in conversational pieces to approach this with clients, instilling more confidence in them than a success or failure metric, with fixed spending, with assumptions that don’t align with reality. We will see more and more changes to this approach over time.

How Do We Put This into Practice?

We should treat retirement decisions and conversations with our clients like change management.

If you think about this, the decision to retire and move into retirement is a perfect change management situation. We are going from this pre-retirement stage, where we are saving and generating our income from work to this decision to retire and then to a retiring stage to figure out how to distribute the income. Some of it might be really abrupt, which is change management, too.

ADKAR is a popular change management approach that says, “What is the process of change management, that a client becomes aware that they have to go through the change? They have a desire to go through the change; they have knowledge about it, and they have the ability to do it.” We reinforce this over and over because it’s not just a linear path. It’s going to adapt and change. We’re going to have to reinforce this process as we move through it.

So, we can learn a lot from change management as financial service professionals, such as, “Are we helping our clients be aware of the issues? Are we helping them to have a desire to make the changes they’re going to need to make that they know this will take?” They understand that small changes to their plan can make a 6 percent withdrawal rate more sustainable over time. Do they have the ability to put these things into place, which is often why they come to you to help with the ability to do this?

The last time NASA went to the moon, they were off track about 98% of the time. But they landed within seconds of when they projected to be there. Why? Because they planned to be off track. They planned to make constant adjustments. And so, when we look at retirement income planning, if we start the conversation with our ability to adjust, we’ll make this more sustainable. All of a sudden, we’re changing the conversation dynamic. That becomes part of the mindset and plan we set up early in the conversations.

It’s not about failure. It’s not the risk of adapting, a risk of cutting back in some areas, like your charitable contributions, eating out at restaurants, and shopping for new clothes. If the client is willing to adapt, we can make this plan sustainable and get to the moon on time. We can get to your retirement outcomes if you are willing to be flexible. It doesn’t have to be tremendous, but can we work six months longer? That’s equivalent to saving 1 percent more yearly for the previous 30 years. Can we work for a year longer? EBRI (Employee Benefit Research Institute) has shown that working a year longer is the equivalent of about 7.7 percent more inflation-adjusted income throughout the course of retirement

Those are small changes on the front end. Can we cut spending by five percent and suddenly make this sustainable? Not forever, but for three to five years in case the market and funded ratio drop? Because of the change in technology, there can be a significant change in how we have these conversations, which can enhance our clients’ confidence that they will be okay throughout retirement.