The Basics of Health Savings Accounts

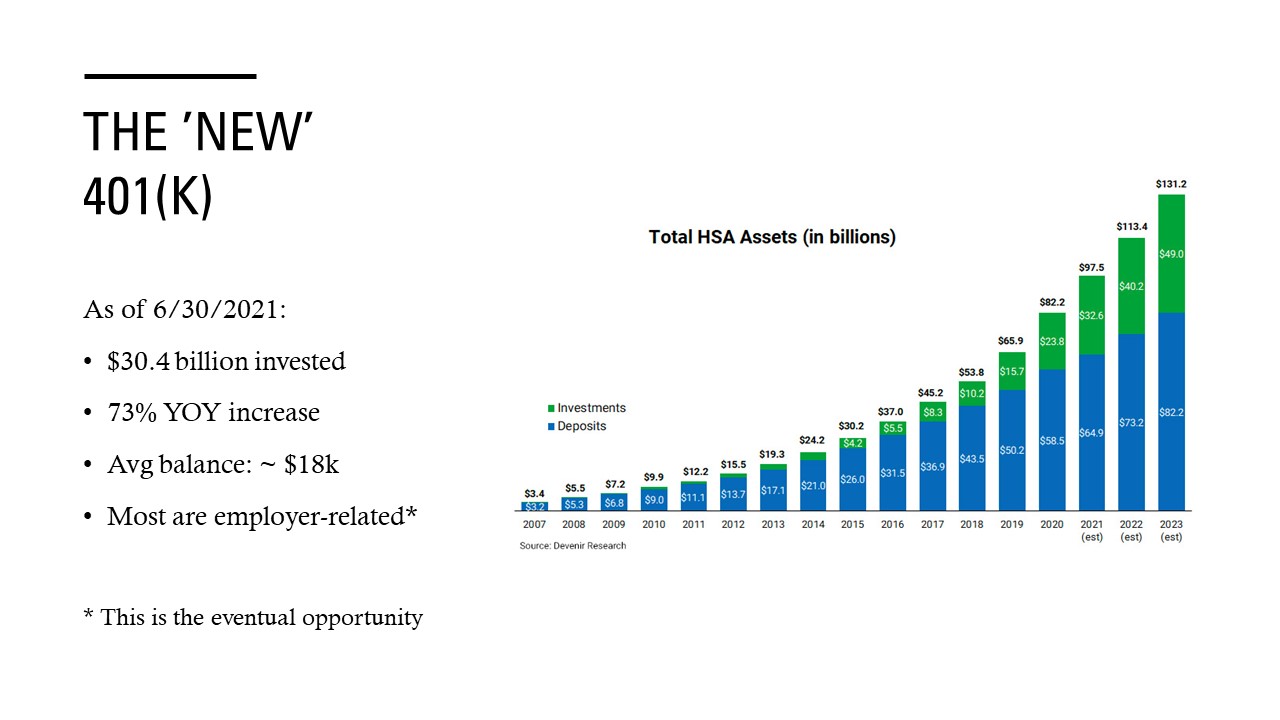

HSAs are not necessarily a huge place to get revenue from an investment fee perspective for advisors. But the asset growth in HSAs is growing exponentially, and every time I update this slide, the numbers get even more significant.

There was a 73% year-over-year increase in funds in HSAs in the past year. Of course, some of that is due to investment growth in these numbers as of June 30, 2021, so that might be a little lower due to market movements in invested funds. Many of these are employer-related contributions. This leads to an opportunity when folks leave their companies or even before they leave their companies because one of the things about health savings accounts that is different from 401(K)s is that they are fully portable at any time.

A plan participant can still be enrolled in an HSA eligible plan, contribute through their paycheck, and still move their HSA assets to an outside provider from the provider that their employer set up for them. This is something I was regularly engaged with when I was employed.

A Review of Medicare Enrollment Rules

We are going to review the Medicare enrollment rules as they apply to HSA eligibility and cover how to contribute to HSAs past the age of 65. I have several case studies that we’ll cover later that are based on questions I have received. I published an article on this topic last summer, so people regularly find me on the internet and send me very personal questions.

You probably know that there is no cost when you enroll in Medicare Part A. Turning age 65, as long as you are eligible for Medicare according to the work rules, you can enroll in Part A. Many people do that to ensure that they do not have issues with late enrollment, even if they choose to work past 65.

Medicare Part B is the part where there is a premium involved. If you miss the window to enroll when you are eligible and enroll late, there are lifetime penalties for that late enrollment. Depending on when you figure out that you messed up, there could be a gap in coverage because there is an annual enrollment period. Messing up and missing the enrollment date does not qualify you to enroll immediately; you will have to wait. There is a risk of getting this wrong.

Many people are disappointed to learn who will want to continue contributing to an HSA past 65. If you are already collecting Social Security, you are automatically enrolled in Medicare at age 65 or later. For folks who are still working but have reached their full retirement age from a Social Security perspective and decide to start collecting that additional income, they must understand that they are automatically enrolled in Medicare. Therefore, you are no longer eligible to contribute to a health savings account. Some of the calculating contributions and eligible contributions to HSAs can get complicated or confusing, and frustrating.

To defer Medicare Part B, you must have other qualifying coverage in place. Qualifying coverage generally means an employer-based group health plan for an employer with 20+ employees. I had a question on that this week. This person owns the company but has less than 20 employees. What is the rule there? The rule is more about the plan itself. Most health insurance plans say that if there are less than 20 participants and any participants are eligible for Medicare, they need to use Medicare as their first coverage. I referred this question back to the health insurance plan since this was a growing company that anticipated having more than 20 people in the plan sooner than later.

Generally speaking, if you have health insurance through your job and work for a larger company, or your spouse does, and you are on that plan, you can defer Medicare Part B until you lose that coverage. One thing that comes into play that people are often taken by surprise about is the idea of creditable coverage, which refers to the prescription drug coverage under Part D. You must be enrolled in Part B to be eligible for Part D. You would enroll in Part D for prescriptions if you were not on a Medicare Advantage plan.

But if you are looking to defer coverage to contribute to an HSA, you need to check to make sure that the prescription drug coverage provided by your plan is like what a Part D would offer. That often can be the thing that disqualifies the ability to defer Medicare coverage. Many HAS-eligible plans do not have creditable coverage for drugs. To answer whether you have it, you need to call your plan, and they should know whether or not the drug coverage is considered “creditable.” That is a technical term. If you have creditable coverage and you are in an employer-based health plan, you can defer Medicare Part B as long as you have that coverage.

One type of coverage that does not qualify is COBRA. Sometimes folks will retire and go onto CPBRA for a little while or even plug the gap between figuring out self-employed insurance as I did myself. However, COBRA coverage is not qualifying coverage in terms of deferring Medicare Part B without penalty. Most self-employed insurance does not qualify as qualifying coverage, nor does individual coverage through the Exchange. For folks who are self-proprietors and purchasing their health insurance through the marketplace, when they turn 65, they will need to enroll in Medicare or get a job with a larger company.

Can You Contribute to a Health Savings Account (HSA) Past Age 65?

Say you have a client who would like to continue contributing to your HSA past the age of 65 and has qualifying coverage in place. HSA rules say you cannot contribute any other funds to a health savings account if you have other coverage behind that qualifying “high deductible healthcare plan.” If you are enrolled in an HSA-eligible plan, which is the only coverage you have, you can contribute to an HSA. But if you have any other coverage, you are not allowed to put additional funds into your HSA.

This includes Tricare. It includes non-limited purpose flexible spending accounts (FSA) and even if you have a spouse who elects coverage into an FSA. A non-limited purpose FSA is where you could use your flexible spending account funds for anything. However, a limited-purpose flexible spending account is a great pairing for an HSA, a flex spending account that you can defer tax-free income to pay dental and vision costs and get those tax-free outside of HSA coverage. If you have a limited purpose FSA and an HSA that you are contributing to and have hit your deductible on your health savings account, then you can use your FSA for medical expenses.

Generally speaking, if you have a limited-purpose flex spending account and an HSA, the best practice is to put the maximum account into the health savings account. Do not touch that money if you do not have to, and use the flex spending account for what you estimate in dental and vision costs. That would include contact lens solutions, glasses, regular dental care, dentures, and anything applicable to those two types of services. That would allow you to have even more tax-free income for your anticipated medical expenses.

Beyond that, of course, the other coverage that cannot be in place for you to not contribute to an HSA is Medicare. The rule of thumb that we have had in practice basically since the beginning of Medicare was to go ahead and sign up for Medicare Part A on your 65th birthday just because it is generally offered at no cost. However, this needs a caveat if you have an enrollee covered in an employer-based plan that is HSA-eligible, they want to continue funding their HSA, and they are already enrolled in Medicare.

For example, let’s say someone is age 66. They enrolled in Medicare on their 65th birthday because that is what they heard you are supposed to do. Then their employer decides to offer an HSA-eligible plan for employee healthcare. That individual may choose to enroll in Part B, or they can continue that employer-based coverage. They just cannot fund their health savings account. It is not that you cannot have coverage under an HSA-eligible plan after you are enrolled in Medicare; you just cannot put another dollar into your HSA.

Clearing Up a Few Misconceptions

That is really what a lot of the misconceptions go into this. There are many nuances about remaining eligible to contribute to the HSA beyond age 65, and I want to clear up a few other things that are often misunderstood.

- Enrolling in Medicare only disallows further contributions to your HSA. That does not mean you cannot have coverage; you can still use funds in your pre-existing HSA to cover your eligible medical expenses. A best practice for HSAs is to allow those funds to accumulate. Ideally, you would invest them for tax-free income and then use them to fund your retirement healthcare expenses.

- One interesting thing that many people do not realize about HSAs is that you can use them to reimburse yourself for Medicare premiums. Once you are on Medicare, if you have funds in an HSA and then pay Part B and maybe Part D premiums, you can take money out of your HSA tax-free to reimburse yourself.

- You can also use your HSA for most long-term care insurance premiums and long-term care costs. If you have an insurance plan that you are funding to cover eventual costs, most of those qualify for HSA eligible costs. Then, of course, any healthcare expenses that would include hearing aids, dental care, and many things that are not necessarily covered by Medicare or tend to be higher medical expenses for retired folks can be covered tax-free by your HSA.

- If you have healthcare expenses, i.e., larger ones like adding ramps to your home or upgrading your shower with bars that can help the taxpayer qualify for the medical expense deduction, you do not get to double-dip if you pay for it with your HSA. Most people do not even qualify for the medical expense deduction anymore on their tax returns because they are not itemizing. This is another way to make those expenses tax-free.

- Finally, many people do not realize that once you are 65, you can take money out of your HSA for any purpose and just pay taxes on it. If you take money out of your HSA before you are 65 for non-medical expenses, there is a 20 percent penalty. Once you are 65, if you have excess funds saved and you do not have any medical expenses to support withdrawals, and you need some money out of your HSA, it is more like a 401(K) or a traditional IRA where you can just take the funds out and pay taxes on them. I do not see that happening much because most people have earmarked their HSA for medical expenses, and you do not know until the very end whether you will need those for medical expenses.

As we get some of the folks who are early in their career and really maximizing the HSA opportunity and possibly amassing six figures or more in an HSA, we may see more of those distributions coming about in the future. Some people are concerned about socking money away into a health savings account specific to medical expenses. Hopefully, this alleviates some of that concern about access after age 65.

The Six-month Lookback Rule for Enrolling in Medicare

The big issue here is not just that enrolling in Medicare discontinues the ability to fund a health savings account. The big issue is a six-month lookback rule for folks who have deferred their Medicare enrollment. This is where I get a lot of panicked emails from consumers.

The six-month lookback rule says that you are deemed to be enrolled in Medicare Part A up to six months before the day you apply to enroll. If you enroll on your 65th birthday, it starts the first of your birthday month. If you apply after that, it starts the month after your 65th birthday. But the six-month lookback does not go before you turn age 65. If you are age 67 and you apply for Medicare because you are getting ready to retire, they deem you enrolled in Medicare Part B six months before the date of application.

Things can get sticky because that is when your eligibility for HSA contributions discontinues. Many people do not become aware of this rule until they enroll in Medicare. If you are applying for Medicare at age 65½ before, then you just need to stop HSA contributions on the first of the month of your 65th birthday. Still, after that, it is six months from the date of your application. This is a crucial thing to know about making sure you are not making ineligible contributions to an HSA, leading to penalties and unnecessary taxes.

Let’s take a look at an example here. We have a person who has elected to retire on September 30, 2022.

Say someone is age 67 and wishes to start Social Security the day after they retire on October 1. Most people in a similar situation will apply in August to ensure that they are enrolled and that everything is set to go before they retire on September 30. Since that application date is in August, they are deemed enrolled in Medicare Part A on September 1, which means that there is the six-month lookback rule that deems them enrolled in Part B on March 1. The six-month lookback rule means you are enrolled in Medicare Part B six months before the application.

For 2022, that means you would only be able to contribute to your HSA for the months of January and February. This is based on the individual contribution, which would be a maximum of $4,650. Two-twelfths of that are $775. This person might not realize until maybe the following tax year when they file their taxes that they over-contributed, and they might instead stop their contributions on October 1.

They made six months of ineligible contributions that they might need to remove some funds. However, many people do not realize that the timing of their contributions is based on the calendar year. I had somebody doing $100 a month into their HSA, so they were not necessarily maxing out, but they had contributed or made payroll contributions beyond the six-month lookback. They were deemed enrolled in Medicare on April 1, and they had contributed in May. There was much panic about what do I do with this money?

But when we did the math, they were still within not making more than they were allowed to contribute for the year. If this person does not exceed the $775 total they can contribute for Tax Year 2022, it does not matter when that money goes in. One way to allow this client to make maximum contributions to their HSA while still having Medicare enrollment and coverage start as soon as they retire is to wait until September, allowing for one more month of HSA contributions.

If there is funding available, another option is to take advantage of the eight-month window to sign up after retirement. This special enrollment period for initial enrollment and deferred Medicare says that you have up to eight months after your employer coverage ends to apply without penalty. The six-month lookback period starts upon the date of application. If you apply six months after September 30, you will have your lookback to October 1, and then it will be all the same. That would require some funds on hand because you would not be starting Social Security until six months later. But there is a way to maximize the funds beyond just the typical rule of thumb and practice of getting all these applications ready to go before retirement.

Most folks prefer to have the application done and their coverage in place before leaving work. That makes perfect sense from a psychological perspective; most people are just going to not max out their HSA. But just a reminder that it can be delayed if maximum health savings account funding is a primary goal. But let us take a look at a more complicated scenario when a six-month lookback period takes us to the prior tax year. We have somebody who wants to retire at the end of April 2022. Same circumstances, age 67, wants to start Social Security the day after retirement..

They apply in March to make sure their first Social Security check is deposited on May 1. They are deemed enrolled in Medicare as of April 1, which is what the lookback takes them to October 1 for Medicare Part A, which is the prior tax year. The maximum contribution for 2022 to their health savings account is zero. They also have a limit on their 2022 contributions to the nine months out of the year that they were eligible since they are technically enrolled in Medicare Part A on October 1. What if they made a full 2021 contribution? There is a fix for that, as long as it is taken care of in a timely manner.

Using the previous example, let us say your client did contribute the full $4,600 that a 2021 individual aged 55 or older could contribute. Applying for Social Security in March of 2022 would make their Medicare Part A enrollment day October 1, 2021. This means they were only eligible for HSA contributions for nine of the 12 months, so they had three months of ineligible contributions made. Just a reminder also that the six-month lookback is only for clients over 65.

Since this person is 67, the six-month lookback period takes them back to October 1. The maximum that they could have contributed in 2021 turns out to be only $3,450. To avoid a penalty that could last the lifetime of the HSA, the client just needs to request a withdrawal of the $1,150 excess contributions by the April tax filing date. If you make a corrective request, you do not have to pay a penalty for those excess funds. This is typically a form that most HSA providers have on their websites. I accidentally made overcontributions to an HSA, and it was straightforward to pull it back.

If this client had put their $4,600 all in through a payroll deduction, then pulled that $1,150 out, they would have $1,150 in additional taxable income for 2021. They would get a 1099-SA from their provider to tell them what to include on their tax return. But suppose they are more like me, where maybe your HSA is outside of your employer, or you are making manual contributions where you, as the HSA account holder, log in and make a direct deposit. In that case, the deduction from your taxes does not even happen until you file your tax return. In this case, there would be no tax consequences to withdrawing those excess contributions.

Another case study is for a couple where a spouse is retiring and enrolling in Medicare. In this case, the working spouse is the younger spouse, age 63.

When the retired spouse turns age 65 and enrolls in Medicare, they are still on the working spouse’s workplace plan as a backup to their Medicare. How much can the couple put into their HSA? The working spouse can do up to the maximum individual contribution for 2022. But because the retired spouse has other coverage, you cannot make a contribution based on their coverage.

Assume that the retired spouse enrolling in Medicare would then drop off the working spouse’s plan and reduce the premium if that is a concern since most don’t need double coverage. But there is a case where you might want to keep the spouse in Medicare on the healthcare plan, which would allow the working spouse to contribute up to the family maximum. The amount you can put in your HSA is based on your coverage amount and not necessarily on the other members of your family’s eligibility to contribute, which is an interesting fact. Let us look at that in a different way that helps better explain what I am saying.

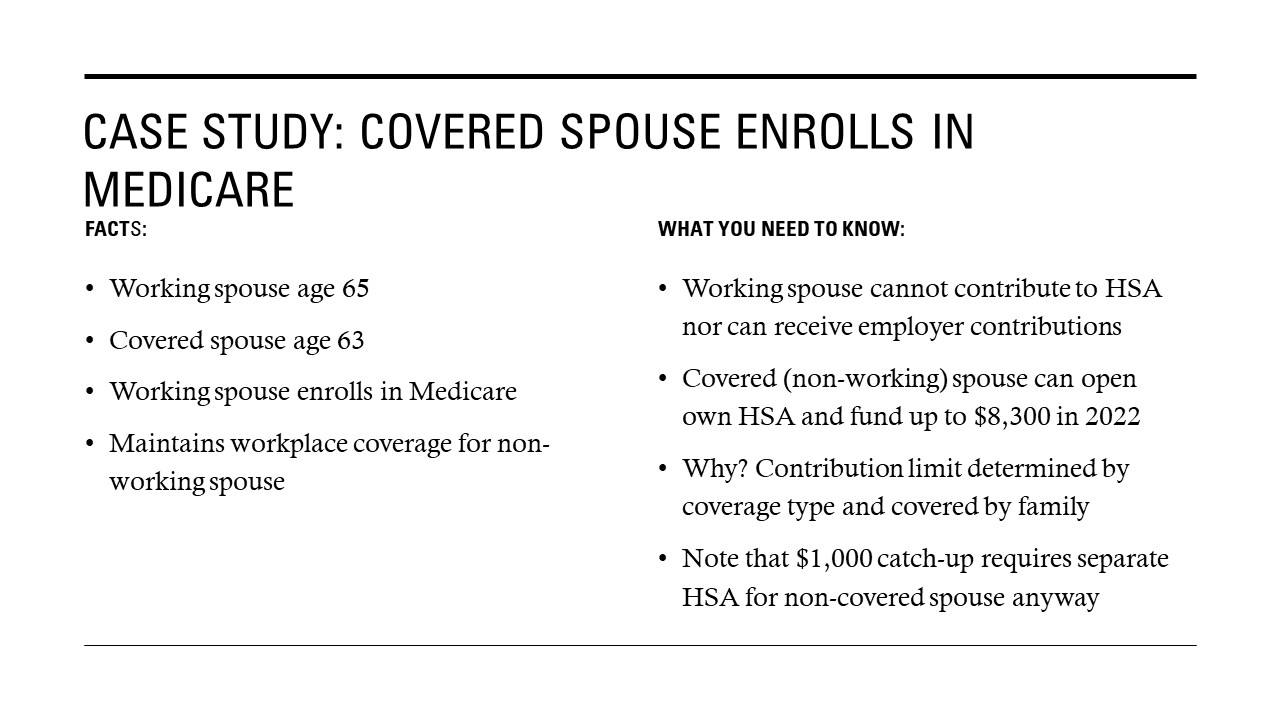

What happens when the facts are flipped, and the covered spouse enrolls in Medicare? Let us say the working spouse is 65, and they have a younger spouse who is 63, who is also on the plan. The working spouse wants to enroll in Medicare. But they maintain their workplace coverage for the non-working spouse to continue to have health insurance until they are 65. This is common for folks married to a younger spouse who is not working and does not have coverage.

Assume that the retired spouse enrolling in Medicare would then drop off the working spouse’s plan and reduce the premium if that is a concern since most don’t need double coverage. But there is a case where you might want to keep the spouse in Medicare on the healthcare plan, which would allow the working spouse to contribute up to the family maximum. The amount you can put in your HSA is based on your coverage amount and not necessarily on the other members of your family’s eligibility to contribute, which is an interesting fact. Let us look at that in a different way that helps better explain what I am saying.

What happens when the facts are flipped, and the covered spouse enrolls in Medicare? Let us say the working spouse is 65, and they have a younger spouse who is 63, who is also on the plan. The working spouse wants to enroll in Medicare. But they maintain their workplace coverage for the non-working spouse to continue to have health insurance until they are 65. This is common for folks married to a younger spouse who is not working and does not have coverage.

You might have somebody work a couple of years beyond age 65 so that their spouse can have coverage. In this case, the working spouse cannot contribute to the HSA, and they are also not allowed to receive any employer contributions. Employers will often make contributions to their participants’ plans to encourage enrollment in this type of plan or provide additional compensation in a tax-favored way. But when you enroll each year in an HSA-eligible plan, the employer will ask if you have other coverage, including Medicare. So, it is a box you will probably have to uncheck or note so that the employer does not make contributions for the working spouse.

This is an area where, if it happens, maybe the spouse just does not check the correct box on their enrollment and then gets employer-based contributions. Then you would have just to make that ineligible contribution withdrawal and have it included in taxable income. It is not a super-emergency situation but knowing that they cannot get further employer contributions or contribute to their own HSA.

But the non-working spouse can. How much could they put in? The working spouse would put the family amount into their own HSA, and the covered spouse could do another $1,000, but they would have to contribute it into an HSA outside of work. While the working spouse is no longer eligible to contribute to their own HSA, we would assume that the covered, non-working spouse would already have an HSA in their name established that they would have been using to put their $ 1,000 catch-up contributions. They would just shift into contributing $8,300 for the family contribution and their own catch-up for 2022 into their own account.

Key Takeaways

- Deferring Medicare enrollment past age 65 does make sense when you want to continue funding your HSA through an eligible employer-provided plan.

- The six-month lookback for Part A Medicare enrollment must be considered in the year of retirement or enrollment in Medicare, especially for folks who are retiring in the first half of the calendar year because that often drifts back into the prior tax year.

- Any ineligible contributions must be addressed before the April tax filing date.

- A spouse who enrolls in Medicare on an HSA-eligible plan may affect contribution amounts. It depends on who is covered and what level of coverage is elected. If it is just two spouses and the non-working spouse is just dropping off of the plan to enroll in Medicare, it becomes individual coverage. Beyond that, it is generally still family contribution amounts, and just the Medicare-enrolled spouse cannot make the catch-up contributions as well.