Yet, other products do not have fee drag and are not taxed in the same way other annuities are taxed. You cannot paint the broad brush of an annuity based on what one annuity does; and yet, it is done every day in marketing campaigns and by folks that want to dismiss annuities as a bad idea.

I want to contrast annuities to mutual funds. How many types of mutual funds are there? We do not categorize mutual funds as one segment. We recognize that there is a variety of different types of mutual funds and ETFs. We recognize that there are good mutual funds and bad ones, yet we do not paint the brush of negativity with the word “mutual funds” in a similar light that we do the word “annuities.”

Our goal in this article is to recognize the broad formation and the contract structures that exist with annuities.

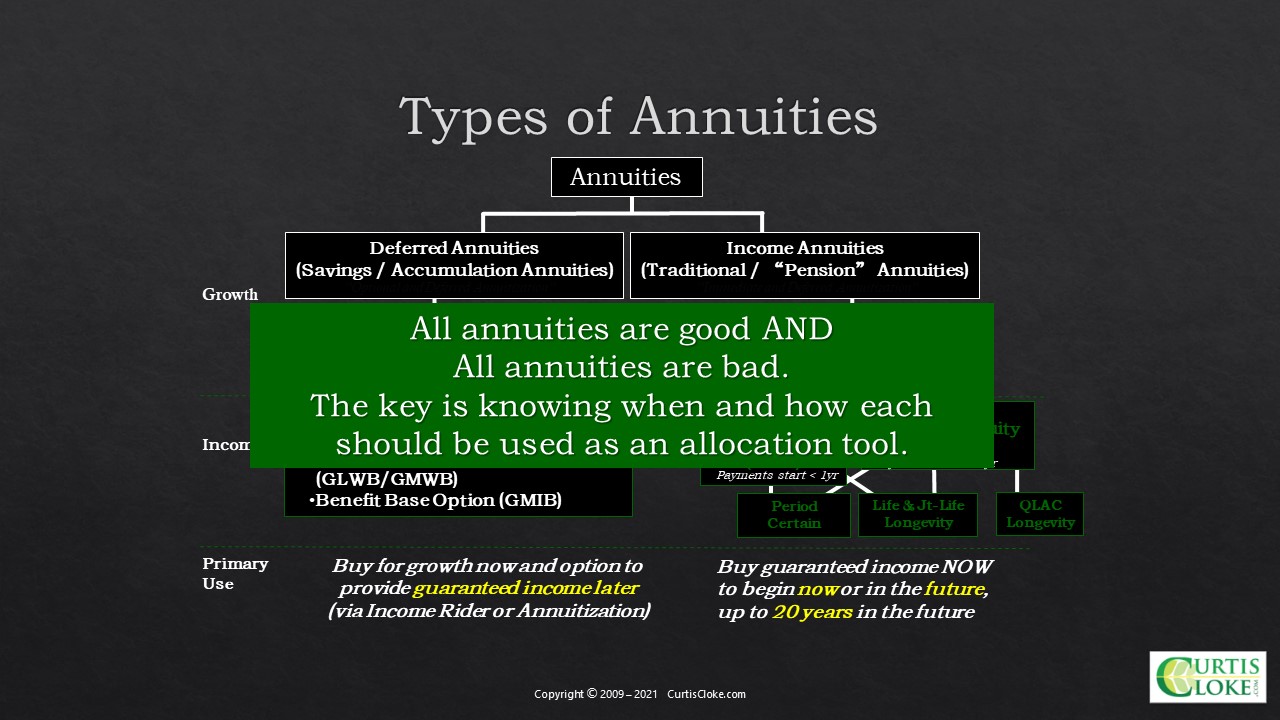

Types of Annuities

All annuities are good, and all annuities are bad. The key is knowing when and how each should be used as an allocation tool. Also, there are growth annuities that are intended for growth and annuities that are intended for income.

There are two main categories or subsets annuities. They are deferred annuities, which are savings and accumulation annuities; and income annuities, which are traditional income-producing products, or they could be like pension annuities. The only other category that we are not going to focus on today is structured settlement annuities.

Underneath deferred annuities, there are three basic chasses. There are variable annuities, there are indexed annuities, and there is a variety of different terms: fixed index annuities and other terms that we have heard for that. Then there is a fixed rate annuity. Two different types are pretty common.

First is the MYGA, which represents a multi-year guaranteed annuity. That would be like a CD alternative. If you buy a three-year MYGA today, you might earn 2.1% on a three-year rate, which beats the banks by about one percent or 80 basis points. A MYGA is a multi-year guaranteed annuity. What you see is what you get. You get the same rate all three years. Many have a 5% or 10% liquidity provision and then s 30-day window of freedom at the end of the three-year or the five-year, whatever the term is.

Then there are traditional fixed annuities. There are too many variations of that product to describe here. There is a new type of variable annuity called structured annuities. There are a whole bunch of categories under each of these basic types.

Underneath deferred annuities intended for savings and growth are alternative income and death benefit riders that one can layer on, so you can have withdrawal benefit riders like a GLWB (Guaranteed Lifetime Withdrawal Benefit), GMWB (Guaranteed Minimum Withdrawal Benefit), or a GMIB (Guaranteed Minimum Income Benefit). They all work quite differently in terms of how they generate and produce income. All these benefits generally charge some kind of fee drag to allow you to have a guaranteed lifetime income or joint lifetime income on top of whatever the other charges of the annuity are if any.

A primary use for these products is to buy growth now and an option to provide guaranteed income later via an income rider or via an annuitization. That represents the deferred annuity category.

The second category is income annuities. There are immediate income annuities, which we know as a SPIA. For tax purposes and content purposes, SPIAs must start within 12 months. There is a specific tax reason why this is the case.

The second category is deferred income annuities (DIA). I discovered this particular product in 1999. At the time, it was called a deferred SPIA. I actually coined it as a SPDIA: single premium deferred income annuity. That name didn’t take off, so we changed and shorted it to DIA. We were the first firm to name that product in the industry.

Payments with a DIA for tax purposes must start after a year. You must delay payments for more than a year, but you can delay that up to 20 years, for example. There is much flexibility between when you purchase it versus when income starts.

With a SPIA, we all know you can buy a period certain payout. You can buy a five-year period certain, a one-year delay and a five-year period certain, a one-year delay and a 10-year period certain. There is much flexibility with period-certain payouts. You can buy a lifetime or a joint lifetime.

The fallacy I repeatedly hear is that insurance companies only allowed you to turn on a DIA for longevity purposes. They would not allow you to do period certains, so the “DIA” was perceived as only a longevity annuity. I hear it coined in articles and all kinds of material, but it is absolutely the most inaccurate thing said about a DIA. Everything you can do with a SPIA, you can do with a DIA. As a matter of fact, from 1999 until 2009, the only thing I did with DIAs was laddered period certains as compared to doing laddered bonds. I found some interesting things in my analytics, testing fee drag and tax drag differences between retaining a present value for a future income stream. That was the most powerful thing. But we must stop calling a DIA just a deferred longevity product. It is a flexible product with a multitude of uses, and it is not limited by longevity only.

The third subset of DIAs called the QLAC (Qualified Longevity Annuity Contract). It truly is a longevity product. What is interesting about QLACs is they are brand new; it is the newest type of annuity we have. The Treasury approved it in July of 2014. The purpose of a QLAC is to buy guaranteed income to begin now or in the future, such as in 20 years.

By the way, there are some products where you can buy a QLAC on a young child. Buy it today and turn it on 30, 40 years from now. I do not know anyone who has ever done that. I have bought it now and delayed up to 20 years. That is the measure by which I will describe this today. Just expand your mind on possibilities.

Age 59½, 10% Penalty Tax Tips and Traps

I mentioned that with SPIAs, you must start the income within 12 months, and with DIAs, you had to start after 12 months. Non-qualified SPIAs do not generate a 10% penalty tax for the taxable portion of the excluded income payments paid before age 59½ for either a short-term period certain or a lifetime income stream. SPIAs for this purpose have a unique tax treatment. Not many advisors know this.

Everybody believes that if you take any gains out of an annuity before 59½, you will naturally pay a 10% penalty tax. This is simply not correct. For non-qualified DIA contracts, however, you do generate a 10% penalty tax for the taxable portion of the income payments paid before 59½ for a short-term period certain, but you do not pay that penalty tax for a lifetime income stream. There is a difference. The reason for this is because for tax purposes, a deferred income annuity that delays more than a year is taxed almost identically to a deferred annuity. Because a deferred annuity is not an income annuity, you can turn it on for a lifetime, have taxable income distributed before 59½, and have no penalty tax. Same with a DIA.

But with a SPIA, this particular provision is waived. It is a unique tax treatment to SPIAs only, and only applies to non-qualified assets. DIAs with a delayed income for a date of deposit are treated as a deferred annuity for tax purposes, unlike SPIAs, which are taxed differently. Not many folks realize this particular point. When doing short-term income bridges, the benefit of using SPIAs over DIAs is sometimes the tax benefits of a high exclusion. This allows a much smaller portion of the asset to be held hostage to generate that short-term sphere of income. In low-interest rate markets, a larger block of assets must be held hostage to generate yield, where you could have a lot more of that portion focused on growth.

Qualified SPIAs and qualified DIAs also do not generate a 10% penalty tax for the taxable portion of income payments paid before age 59½ for all lifetime income streams, regardless of whether it is an installment payment, a cash refund, or there is a variable COLA adjustment to the income payments. Even though 72(t) and 72(q) reference substantially equal payments, there are COLAs that you can buy, such as a one percent COLA, two percent COLA, three percent COLA. All of these are still be within the category of substantially equal payments. This is an alternative to the 72(t) options that exist.

72(t) Regulations Tip and Traps

For qualified SPIAs and qualified DIAs, a five-year period certain income from ages 55 to 60 does not qualify for substantially equal payments under 72(t) as a carve-out from a larger sum of qualified assets.

I hear of advisors starting with maybe a $200,000 IRA account. They think they can take a smaller piece of that $200,000 and then do a five-year period certain payment on a piece of it. Then they grow the rest of the remaining assets between ages 55 and 60, thinking they have met 72(t) because there are two succinct and separate accounts for tax purposes. This strategy does not work for 72(t) whatsoever. All qualified accounts may provide Form 5498 for market value tax documents, but the income provided by the income-only annuity only satisfies the RMD requirements for that particular SPIA or DIA.

The IRS does not provide for any offset of income payments provided in excess of the 5498 fair market value for the SPIA or DIA. No offset of excess RMDs is allowed for other non-annuity IRA or non-annuity IRA RMDs, even though the 5498 exists. Here is the reason. All annuity contracts approved for issue to be sold in 2006 and after were required to provide a 5498 fair market value to the IRS that included SPIAs and DIAs. SPIAs and DIAs approved for issue to be sold before 2006 were not required to provide the 5498 fair market value to the IRS.

This happened because in 2006, the IRS became aware of death benefit rollup variable annuity contracts. They realized a death benefit to an heir could be $200,000 with the rollup, but the account value might only be $50,000. The client was getting a Form 5498 RMD based on the $50,000 of cash when they could be 90 years of age, die the next day, and the heirs would get $200,000. So, the IRS formulated a special RMD for those products based on the present value, based on age, and based on a formula of the death benefit.

In an effort not to miss any correct 5498 filings, they just simply said all annuities that are qualified must produce a Form 5498. Consequently, you could have an income annuity, a SPIA, or a DIA that does not provide a Form 5498, and you could have some that are providing 5498s. Some tax professionals and others will call me and say, “The income on Box 7, Code 7 of the 1099 is much higher than what the RMD fair market value requires, so cannot we take less from the non-annuitized IRA assets and take an offset?” The answer is, technically, you cannot do that. We can offline have more discussion about this, but that is not allowed given the current IRS Service Regs.

Let us talk just a minute about the QLAC annuities. Qualified longevity annuity contracts were approved for issue by the U.S. Treasury in July of 2014. It allows for 25% of your IRA assets to be invested in a QLAC up to $135,000. A QLAC can be turned on for income at any time. This concept is a point that is missed. Most people think it is age 85. The QLAC Regs allow you to turn it on as early as 72, which now meets the RMD age consequently, but you can delay it and start it anytime you want between ages 72 and 85.

Based on the case study of the client you are working with, there may be reasons why income may want to start at ages 73 or 75 or different ages. You have much flexibility as to when you turn it on the income. Even after you buy QLAC contracts, a lot of them allow you to change the start date to five years later or five years shorter. If you choose a middle ground like age 80, you have maximum flexibility to recast when that starts if you are not sure when you have a gap of income. Just be aware that this feature does exist. QLACs allow for joint lifetime payouts, in addition to just single life. They also allow for a cash refund.

They do not allow for installment payment, but they allow for COLAs. Not many folks understand this. I cannot think of a single QLAC we have ever done that has at least a cash refund on it. The only time a cash refund might not be utilized is if I am arbitraging life insurance purchases along with the income annuity. Then, in this case, I might then do a life-only QLAC. But I do not know of very many clients who would be okay with meeting a MAC truck the day after purchasing a life-only QLAC and kissing that money to their heirs goodbye.

Finally, the IRS allows QLACs to be converted to Roth IRAs, but most carriers do not allow for this change in their administration features for servicing QLAC contracts. Let me pause here for a minute.

Mark Iwry was the second-in-command at the Treasury when the QLAC was approved in July of 2014 to be sold. This approval was before any QLAC product had been developed. It was not highlighted as a benefit in the Regs.

However, the Regs were written so that a QLAC, just like any other qualified account, can be converted, as long as it is the entire contract, over to a Roth. Most carriers that develop these products decide when they develop them what administration allowances they are going to provide to service that product. I have only in my career found one company that was willing to do Roth conversions. We have also converted qualified DIA contracts to Roths.

But because of this possibility and the fact that there may be new developments later, and with all this new thought process, inflexibility of administration possibilities could occur. So, I recommend you consider splitting the QLACs into smaller chunks if there is an opportunity to convert before the income start date to a Roth. The present value of each QLAC would have to fit whatever bracket bumping level you do not want to go over without causing higher taxes from having one QLAC versus many. So, you want that flexibility. This flexibility is magic.

Remember, you can do a QLAC to start in 20, 30, or even 40 years. There is no age limit. The earlier you do it, the more present value there is for RMDs that are pushed further out.

Income Strategies With DIAs

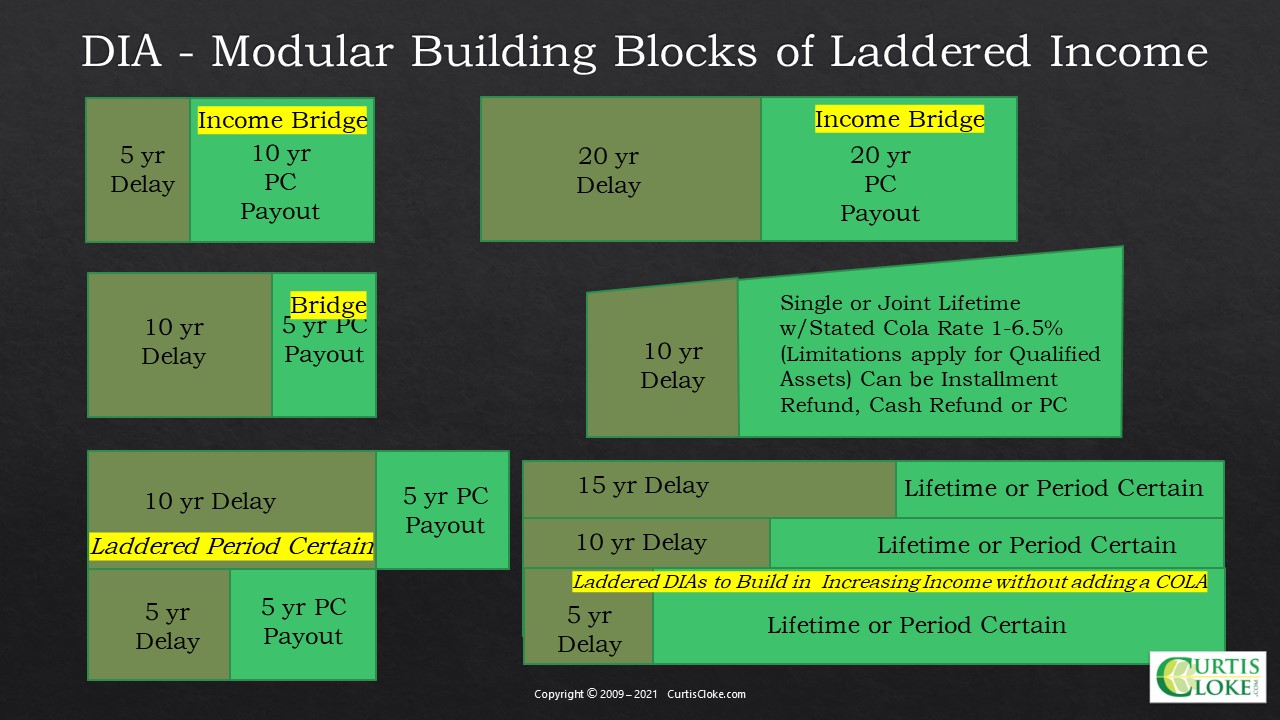

Many folks have not thought about DIAs as I am about to share because they think they are a longevity-only product.

In the upper left corner is a DIA with a five-year delay and a 10-year period certain payoff. We use this as an income bridge. Because we are doing retirement planning five or ten years before retirement, we can delegate dollars early and get a discount like buying a discounted bond, in the same idea, same manner. There is an accrual factor on what my withdrawal rate is to an older age, but with a present value deposited early that gives me a much higher outcome. It holds hostage capital from my fixed-income assets because usually, income annuities are bought with fixed-income assets, not growth assets. There is an advantage to this.

Another option is a DIA with a 10-year delay and a five-year period certain. Or you can do laddered period certains by doing a five-year delay, a five-year certain period; a 10-year delay, five year certain. Like an accordion, you can do a 20-year delay and a 20-year period certain payout. You can do a 10-year delay with a single or joint lifetime. You can also add a COLA.

For example, in 2009, I bought a DIA with a 20-year delay in an all-cash balance pension plan. It was not going to any have new funds added to it. It was locked in at a three percent fixed rate. I could not invest the money. It was part of my fixed-income portfolio.

I put in $52,660. It does not start income payments until July 7, 2029. When I turn it on after 20 years, I will receive five annual payments of $49,797.87. It is a 25-year contract—twenty years of delay, five years of payoff.

I went out this morning on the quoting software inside our retirement income planning software, piped in from Cannex. I wanted to see how much I would need to invest in having an annuity that started paying in January 2029 with a five-year payout of $49,797.87 a year. I would need to invest about $200,000 today to generate the same amount of income.

By the way, if this is the present value needed to produce the same income, I would have to produce an 11.4% accrual factor in the market net of fees and net of taxes to achieve the same goal.

Also, I want you to understand that if I had attempted to do this with bonds, I would have to pay income tax on the phantom income during the deferral period if I delayed with bonds. With the deferred income annuity, it is all tax-deferred. When I get to the income distribution, then I still have income taxes on the portion that is still taxable. With the income annuity, I have an exclusion ratio tax treatment. If I have trading costs and asset management fees for managing the bonds, I have none of those fees with this DIA. And this is with a commission of about two percent already included.

This is relative to the day, but not certainly at the same level. I just wanted to demonstrate the power of this. You still have the no income tax and the deferral. No phantom income tax. You could replicate the laddered idea with zero-coupon bonds, but you would still have the potential cost of trading or buying those bonds. Then you would still have the phantom income tax on the deferral period before the ladders were to mature.

You can create the same income stream with a little bit less capital held hostage to generate the income net of tax and fee drag.

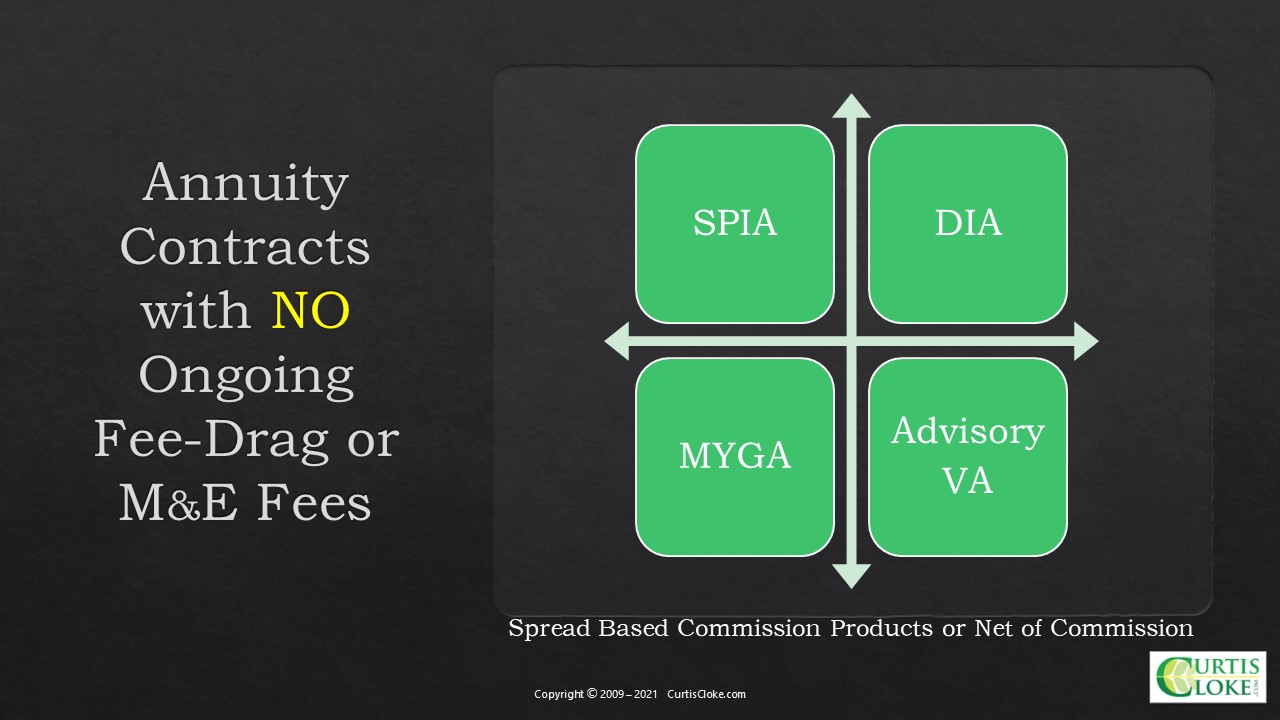

Do All Annuities Have Fees or An Ongoing Fee Drag?

The answer is no – they do not. There are annuity contracts with no ongoing fee drag or M&E fees. They are SPIA, DIA, MYGA, and advisory VA contracts. Advisory VA contracts, the good ones out there, charge a $25 annual administration fee.

You also have spread commission-based products: SPIA, DIA, and MYGA, and you have net-of-commission products. A net-of-commission product is not free; I am not sure an advisor will do the work without charging a fee to give the advice or the service they get to get net-of-commission products. They have to pay to get access to those products. They have to do that with after-tax money. If it is a qualified account, I am paying those baked-in fees in the spread, where I put in this much, and I get this much out already baked in.

Once purchased, there is no ongoing fee drags on any of these except the advisory VA, where there may be a $25 annual administration fee and whatever other fee an advisor puts on there and discloses transparently.

Key Takeaways

In retirement, we all know there are three basic retirement income strategies:

- Systematic withdrawal income plans.

- Bucket strategies, with the buckets laddered in progressive time segments of money, and

- Retirement income floor, or promised-based income floor strategies.

We built our Retirement NextGen software to allow all these to be done dynamically with tax, Medicare Part D, Social Security timing, and Roth conversion strategies. We have tested hundreds and hundreds of case studies. Eighty percent of the case studies we test are more efficient using a hybrid combination of these three approaches together than they are just doing one over the other. So, the power of efficiency is in blending it.

Also, it is the power of not having bias as to specific products, believing more products are superior. Because until we know the facts of the client’s situation, the facts of the case, we do not know what is best for the client until we know what the tools do. You would not use a crescent wrench to ratchet a nut off the end of a lug nut for a tire, and we would not use a screwdriver to use in a way that would not be appropriate for a screwdriver. We need to know what the tools do. Use the tools for the right job and collectively understand what these tools might do for the efficiency of tax, fee drag, and inflation.

I want to encourage all of us to think about these. It is just a basket of products. We need to know what the products do without biases. Annuities provide broad-line product types. Annuities may help mitigate tax drag, fee drag, inflation drag with COLAs. Annuities are financial tools that have features and benefits not available by other financial products and vice versa. The basket of products approach blends optimal planning tools that may enhance potentially better outcomes.

The true fiduciary considers and understands all product allocations without bias, no bents. Financial advisors should have no bent for or against annuities. Instead, we should consider them only as one of many financial tools in the toolbox.