As soon as you start to take money out of a portfolio, it becomes essential to look at the sequence of returns, particularly when weak or negative returns occur. There are going to be adverse events in the early years. There’s going to be some in the late years.

Let’s consider a very simple example to illustrate. Think about a portfolio with a value of $100, or as many more zeroes after that as you’d like, because this entire concept scales irrespective of the size. Suppose in that first year, the portfolio loses 20 percent, so at the end of that year, it’s worth $80. Again, there are as many zeroes after it as are necessary. If no draw is taken, it will require a 25 percent gain in the next year or even a series of years to return to its original value of $100. If, on the other hand, a $5 draw is taken at the end of the first year after that 20 percent loss, it leaves an end value of $75.

Therefore, it would require a 33 percent gain in the next year or next few years to return to its original value of $100. The point is that taking any money from a portfolio that has gone down makes it that much harder for the portfolio to recover. If there is a series of these, it can lead to the portfolio becoming exhausted prematurely. In fact, that’s what led to the famous four percent rule because, on average, a portfolio does much better than four percent. Because there are downturns and the four percent rule was developed in the concept of drawing money from the portfolio every single year, whether there were upturns or downturns, the amount was always the same adjusted only for inflation.

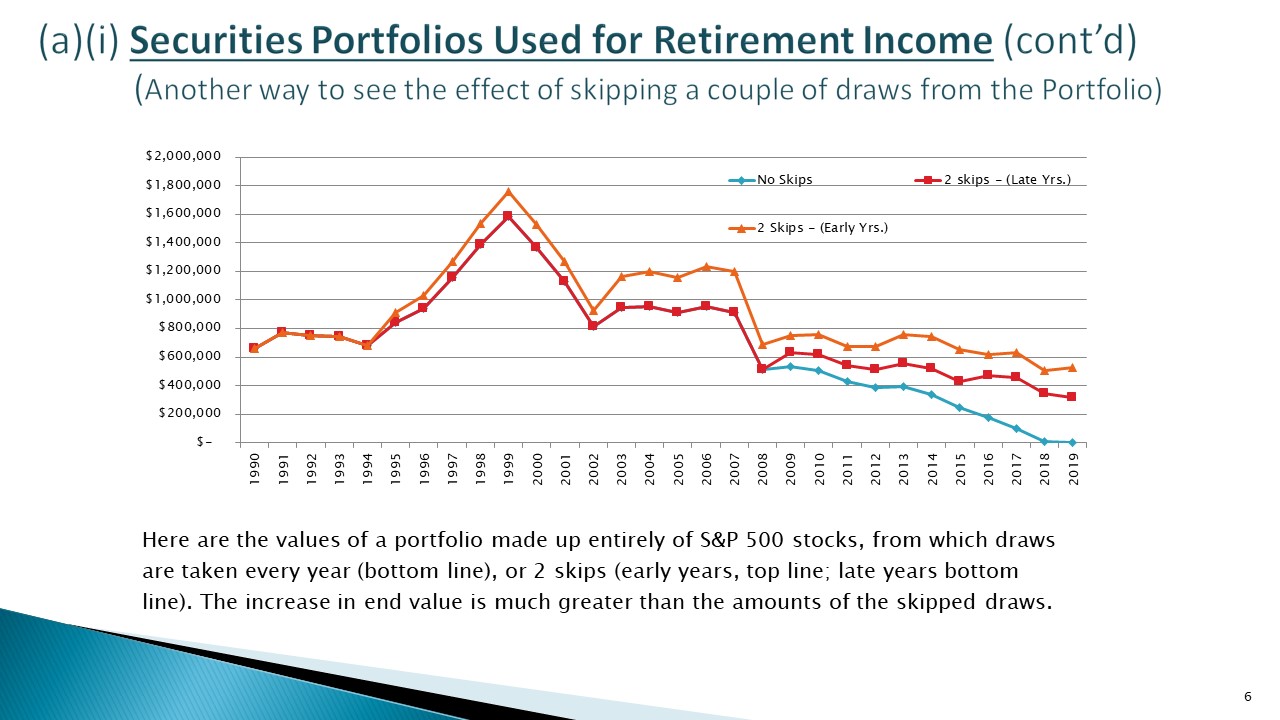

Now, let’s look at a more complicated example. Here’s an example of a $750,000 portfolio invested in the S&P 500 over the 30 years from 1990 to 2019.

The lowest line of the three lines represents no skipping of draws. Every year, the same amount of money (6% of the portfolio’s value) was taken, adjusted only for inflation. Notice that by 2018, which is before the end of the 30-year retirement, it had run out of money.

The top line shows that if we skip two draws, particularly in the early years, at the end of 30 years, there is nearly $600,000. The middle red line shows that if we skipped two draws in the later years, there is a remaining value at the end of 2019 of about $300,000.

Now, the point is, of course, that if somebody is retired and they skip one of the annual draws from the portfolio, they’ve got to live on something. What do they live on? Well, as it happens, the title of this article is housing wealth. And if you take a draw from a reverse mortgage credit line then, what will happen is that you’ve got the money to live on, and you let the portfolio recover. The amount of money left in the portfolio grows at the portfolio rate, in contrast to the cost of drawing on a reverse mortgage credit line is an interest rate, which is lower over time than the value of the portfolio’s growth.

The famous four percent SafeMax rule was developed by William Bengen back in 1994. It covered a whole raft of 30-year periods using actual portfolios, unlike this example that I just gave with a pure stock portfolio invested in the S&P 500. Bengen used various mixed portfolios from about 40 percent stock/60 percent bonds on up to about 70 percent stocks and 30 percent bonds. He found that if you drew four percent initially and then adjusted that draw for inflation over all of the subsequent years, that the portfolio didn’t run out of money.

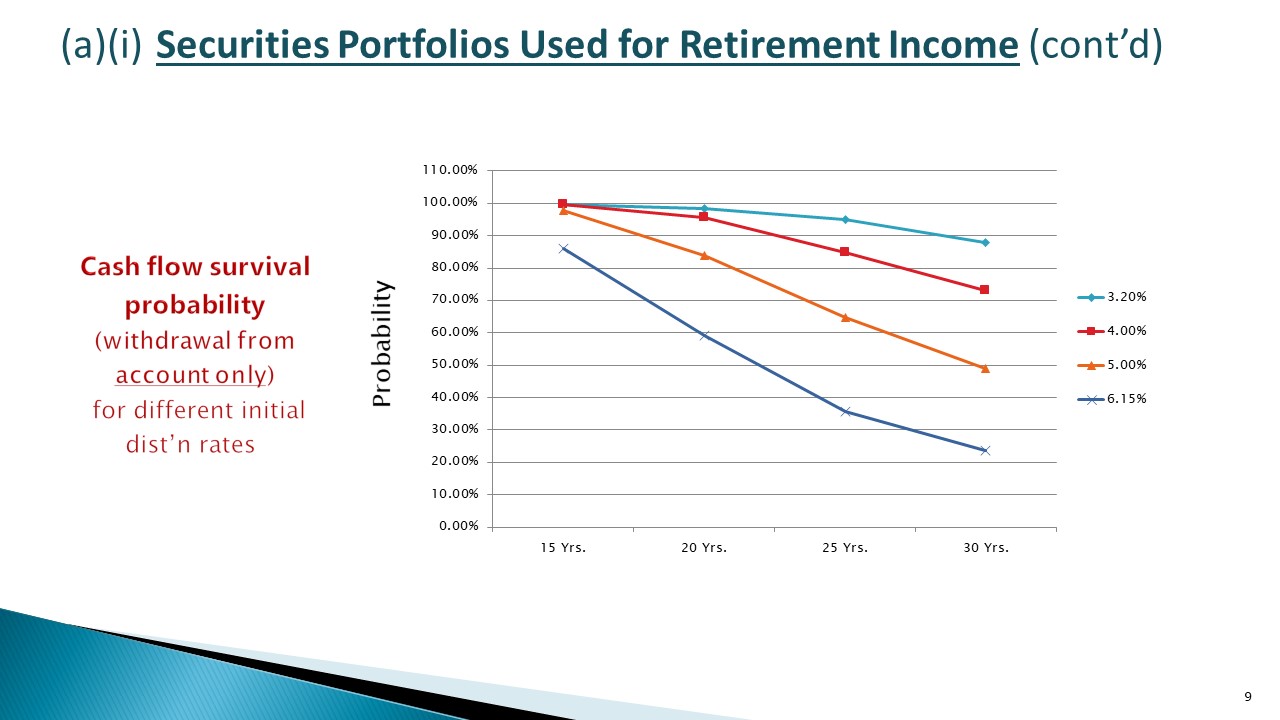

Suppose we do mathematical modeling with a Monte Carlo simulation using today’s projected investment returns. In this case, we find that to achieve a 90 percent probability of success, you can only take a 3.2 percent withdrawal to be absolutely safe when drawing exclusively from the portfolio. That’s the point. If you draw exclusively from the portfolio, you’ve subjected yourself to the sequence of returns risk because you’re withdrawing even when the portfolio is down. That leads to cashflow exhaustion or at least enhances the probability of cashflow exhaustion.

Suppose you take an unsafe approach, meaning increasing with today’s projections from 3.2 percent to 4 percent or from 4 percent to 5 percent using Bengen’s data. In that case, you find that you increase the probability of cash flow exhaustion in fewer than 30 years from 10 percent up to 30 percent. Below depicts what happens if you’re taking cash flow at various initial percentages and after that doing nothing but inflation adjustment.

So, whether the portfolio goes up a lot, up a little, down a lot, down a little, you’re only adjusting the cash flow for inflation. And the reason for thinking that way is that it’s for constant purchasing power. The top blue line after 30 years has a probability of about 90 percent success. That means that cash will flow at a constant purchasing power in 90 percent of the scenarios, which means a 90 percent probability. If, however, you increase the cash flow to four percent of the portfolio – that is, the initial draw and then adjust that for inflation – then you’re down to about just a little above 70 percent of the probability of cash flow survival for 30 years. At 6.15 percent, we’re down to about a 1 in 4 probability of cash flow survival.

That’s a terrible way to retire, risking that you’ll run out of money three times out of four.

The conventional wisdom for dealing with the risk of that exhaustion is when the portfolio is exhausted, use home equity. Use a reverse mortgage as a last resort. It’s what I call a wait-and-see approach. Because after all, if you’ve got a one out of four chance of making it, maybe you don’t want to take the risk of digging into the house equity.

A better strategy might be an active strategy or a coordinated strategy that enables the retiree to avoid drawing on the portfolio when it’s had negative or weak investment performance, especially in the early years of retirement. One way to do that is to draw instead on a reverse mortgage credit line each time the portfolio’s investment performance was negative or weak. I published an article in 2012 and another article in 2017 with more variation testing this strategy.

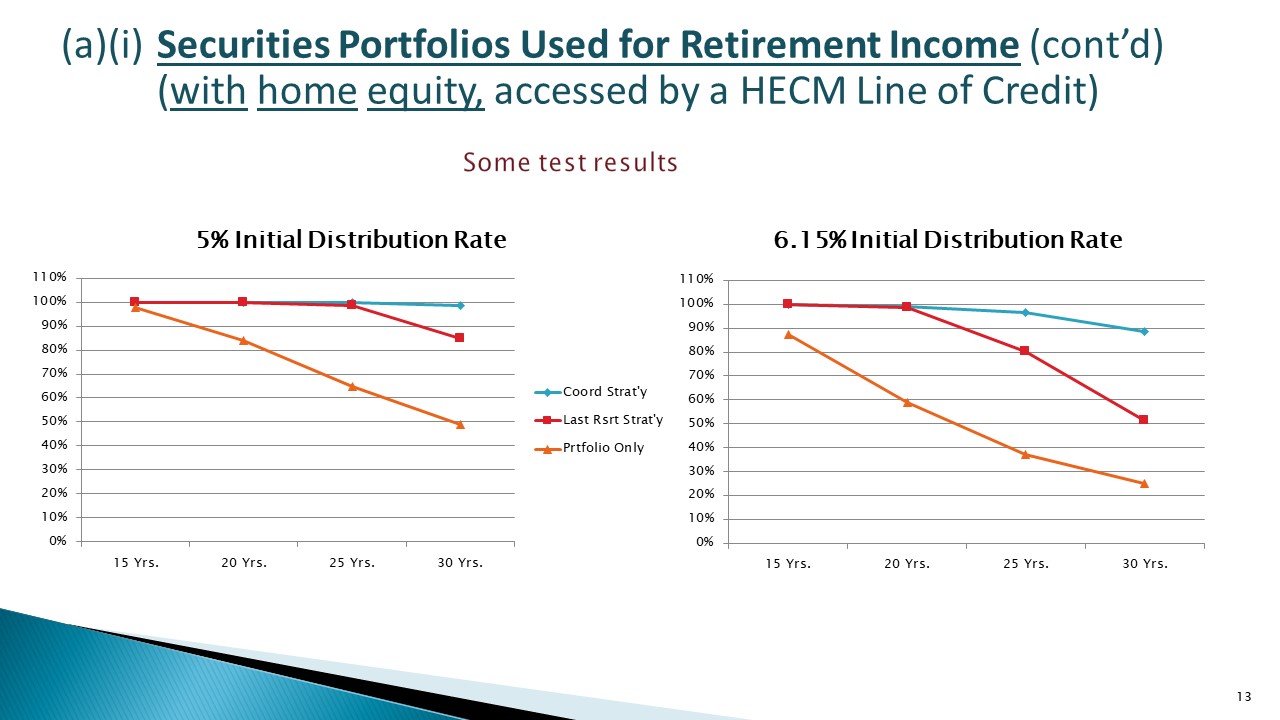

We ran two spreadsheets simultaneously that are identical in every respect, except the timing of the draw on the portfolio or the reverse mortgage or HECM credit line (home equity conversion mortgage). It’s the most widespread, most widely used kind of reverse mortgage. We used a portfolio value equal to $750,000, which is also the initial home value. The composition of that portfolio is 60 percent stocks and 40 percent bonds because that tends to be a bit more stable and more widely used.

We found that if we use a coordinated strategy and a five percent initial distribution rate adjusted annually for inflation, there is a one hundred percent likelihood that the portfolio will last (blue line on top) even after thirty years of distributions.

In the graph on the right, if we go up to a 6.15 percent distribution rate, there is a ninety percent probability that a coordinated portfolio and the home equity strategy continue to provide as much cash flow and constant purchasing power as which we started. If we use the last resort strategy, there is a 50/50 chance of success. And if the portfolio alone is drawn upon, even with this kind of portfolio at a 6.15 percent initial distribution rate, we only have roughly a 1 out of 4 chance of the cash flow making it.

Obviously, there’s a tremendous advantage in using the coordinated strategy. Moreover, there is a tremendous increase in the amount of cash flow. It’s twice as much as the 3.2 percent rate if you’re drawing on the portfolio only.

To recap: Where the initial home value is close to the initial portfolio, that’s the one-to-one ratio, and the coordinated strategy is used, an initial draw rate of six percent of the portfolio value will provide about a 90 percent probability of cash flow survival. That’s a terrific result. That’s twice as much as the portfolio alone in today’s returns environment. Other initial draw rates can also provide a 90 percent probability of success with other home-to-portfolio value ratios.

The most important thing, especially for financial planners and their clients, is don’t think of it as set it and forget it. If appropriate, be prepared to adjust spending levels. It’s easier to make minor adjustments early than major revisions later.

Replacing a Conventional Mortgage to End Mortgage Payments

Let’s now look at someone who retires with a mortgage balance on a conventional mortgage. About 30 percent of people who retire owning a home do so with a mortgage, which is a significant portion of many people’s income.

Let’s say a retiree retires with a remaining mortgage balance of $200,000 on a home worth $700,000 and 15 years to go, or 180 months of payments. Let’s assume payments are $1,568 a month. Over 180 months, these total to more than a quarter of a million dollars, or $282,000. A retiree can use a reverse mortgage to refinance an existing debt into a non-recourse loan with deferred payment.

A typical retiree in their late 60’s can get a reverse mortgage in the amount of about a 45 to 55 percent range of the house’s value depending on age. This retiree then qualifies to refinance their existing $200,000 mortgage into a HECM with available proceeds of about $350,000.

If the existing $200,000 conventional mortgage is refinanced into a HECM, it eliminates the monthly payment obligation. That’s already a terrific help to cashflow drain. Then, it provides access to an additional HECM line of credit of $150,000, which can be used to manage the sequence of returns risk throughout the distribution phase of retirement. Obviously, in this case, where $200,000 of the $350,000 is already used up in making a loan payoff, the advantage that’s available to help deal with the securities portfolio is far less, but it’s not absent.

If the reverse mortgage is the remainder of the original purchased mortgage or a refinancing, then that portion of the reverse mortgage is considered acquisition indebtedness. Any indebtedness secured by the home that is not acquisition indebtedness is called home equity indebtedness. Under the 2017 tax law, interest on home equity indebtedness is no longer deductible. Interest on acquisition indebtedness is still deductible to a lesser extent than before but still deductible.

In other words, you don’t lose the acquisition indebtedness character of the conventional mortgage if it had such character by refinancing it into either another conventional mortgage or a reverse mortgage. In this case, the interest that accrues on that portion of the loan is deductible when paid. Generally, it’s deductible when paid if there aren’t other complications involved.

The other portion of the reverse mortgage, that is the $150,000 portion reserved as a line of credit, creates home equity indebtedness. Under the 2017 tax law, the interest on that indebtedness won’t be deductible.

Downsizing to Eliminate Debt and Increase Income-Producing Investments

Let’s say Joe is 70 years old. Joe’s wife passed away a few years after they refinanced their home. The debt on the home is now $400,000. Upon the passing of Joe’s wife, the household income diminished by $1,200 a month, making the monthly mortgage payment difficult. Joe is going to downsize and sell his home worth $950,000. After real estate commission, he will net $893,000 and pay off the $400,000 existing mortgage, ending his mortgage payments of $2,350 a month. Think of the savings in cash flow!

Joe buys a new home for $625,000. He makes a down payment of $275,000, and he gets what’s called HECM for purchase reverse mortgage to finance the rest. A HECM for purchase is a reverse mortgage that you can use to facilitate purchasing a new home. This leaves $218,000 of the cash remaining from the sale of his home to invest or for home improvement, and his $2,350 monthly mortgage payments are wiped out.

Assume he generates a five percent return on the $218,000 or about $900 a month in income. This means a net monthly increase in cash flow of about $3,200, or $39,000 a year. That’s a fantastic improvement, and it’s because he was able to downsize and use a HECM for purchase reverse mortgage.

Let’s look at the tax issues here. In this case, if the home is sold after substantial appreciation, there is capital gain. If the seller is a couple, which is not Joe’s case, the capital gain exclusion is $500,000. If the seller is a single individual, the capital gain exclusion is $250,000. So, that’s important to note because it was, in our example, a $900,000 house. There was likely quite a bit of capital gain. But only a portion of it is subject to capital gain tax because you get a $250,000 exclusion. Moreover, the capital gain rate is lower than the ordinary income rate. He may have to pay some tax, but it’s not likely to be a big hit.

The reverse mortgage loan that pays the portion of the purchase price is acquisition indebtedness. The accrued interest on the acquisition indebtedness will be deductible when paid.

Using a Reverse Mortgage with Silver Divorce

There are many scenarios in which a reverse mortgage can facilitate asset division in silver or gray divorce. People over age 50 are the only cohort that continues to experience an increased rate of divorce. Younger people seem not to be divorcing as much or at least not increasing the rate of divorce.

I published the following illustration in the Journal of the Society for Divorce Financial Analysts. Luke and Laura are divorcing, and they own the home free and clear. Laura wants to keep the home. From the home, each party is entitled to $350,000. They want to follow a scenario that does not require them to come up with a whole bunch of cash, so Laura obtains a HECM refinance in the amount of $350,000 to purchase Luke’s interest.

All the mortgage payments are deferred until Laura permanently vacates the home, so it doesn’t impact her cash flow. Luke receives the $350,000 and uses that as a down payment using a HECM for purchase for a new home. His new home will cost $635,000, so his down payment is $285,000, and the HECM for purchase pays the remaining $350,000.

This leaves him $65,000 remaining for future income or home improvement. The result is that both parties remain homeowners, and neither party incurs a monthly mortgage payment obligation. Neither party has to draw on any income-producing assets, so they don’t get hit with the tax if they drew the money from a 401K account or a rollover IRA. There is no capital gain tax or sales fees incurred. And Luke increased the value of his investment portfolio or has extra money for home improvement.

Why is there no capital gain tax? Let’s assume that house was purchased for a whole lot less. Now, one-half of it is purchased by one of the parties, Laura, from Luke. In the Internal Revenue Code, there is a special exception for situations between spouses in several situations, particularly in the context of divorce. One would suspect that Luke might be hit with a capital gain tax. But because of the special exemption in the code, there is no tax.

Additional Tax Strategies with Reverse Mortgages

The interest accrues on a reverse mortgage debt for many years. As we all know, it’s not deductible until actually paid. That’s because most borrowers are cash method taxpayers. It’s often the case that reverse mortgage debt is paid following the homeowner’s death who is the borrower. Sometimes, the homeowner borrower leaves the home permanently while still living, and the reverse mortgage debt is then paid. So, we’ve got two situations to consider. Leaving home horizontally, which means following death, or vertically, which means going somewhere else.

Let’s point out some critical values. Over the typical 10-to-25-year duration of a reverse mortgage, the amount of accrued interest allowable as a deduction can be in the tens of thousands to hundreds of thousands of dollars. It really does build up. The rules that determine the amount of interest allowable as a deduction depend on whether the reverse mortgage loan itself is properly characterized as acquisition indebtedness or as home equity indebtedness.

If the coordinated strategy is used and people are reasonably careful during their retirement years, there is likely to be ample income available against which to use the deduction. So, when they pay off the debt, that’s when the income deduction is taken. The deduction for accrued interest on acquisition indebtedness can be used against any income to the extent allowable.

If the homeowner borrower does not have enough other income to be offset by that deduction but does have a 401(k) account or a rollover IRA, they can take a distribution which would be then entirely tax-free. It warms the heart of a tax lawyer to think that the money in question has never been taxed and never will be taxed because the reverse mortgage interest creates the deduction that makes that money deductible when it went into the 401(k). The earnings in it were tax-exempt because it’s a tax-exempt entity. And when coming out, the income that would be taxable is offset by the deduction for the interest that accrued. Then, we have a complete legal avoidance of the tax.

If not taking out the money, they can do a Roth conversion. That can make tax-deferred money never taxable. It’s a terrific thing to keep in mind when the interest is deductible, which means that the interest is based on acquisition indebtedness. An important point to note, though, is that the distribution or Roth conversion must be accomplished in the same year that the interest is paid off because the deduction cannot be carried forward or backward like business operating loss.

The above strategy is for when the borrower leaves the home permanently while still living. Now, we’ll go to the situation where the borrower dies, and the interest is then paid off by the heirs using IRS regulation, 1.691B-1, which allows what’s called a “deduction in respect of a decedent.” The idea is, typically, the estate doesn’t have enough earnings to benefit from the deduction. Following the language of this regulation, to pass the home to the adult child(ren) or the beneficiaries of the 401(k) account or the rollover IRA because then they can sell the house, pay off the mortgage, and with that payoff is the interest deduction. The interest deduction, of course, is the offset against what they have as income.

Key Takeaways

We’ve shown the effect of skipping a few distributions from a securities portfolio and replacing the income withdraws on a buffer asset such as home equity. Cash-value life insurance can also be used in this context. It’s important to remember that skipping a few distributions from a securities portfolio early on can make the portfolio last a whole lot longer because the amount that stays in the portfolio grows at the portfolio rate. The cost of replacing it with draws from a reverse mortgage line of credit, or the cost of borrowing, is an interest rate. The interest rate tends to be less in the long run than the growth rate of a balanced portfolio.

The second item we looked at was replacing a conventional mortgage. Using a reverse mortgage to replace a conventional mortgage substantially reduces cash flow needs during retirement, particularly for retirees who want to age in place.

We’ve also shown how to downsize or change location using a reverse mortgage for purchase can reduce cash outflow and provide additional funds to invest for additional cash inflow in retirement.

And finally, we’ve shown that using a reverse mortgage can provide liquidity for the division of assets in a silver divorce. The result is that less cash is needed for housing than without the reverse mortgage.