The S in HSA stands for savings.

Most of us grew up in the time of flexible spending accounts (FSA), where you made an educated guess as to what your out-of-pocket expenses were going to be, but you didn’t want to overshoot it because you had to use it or lose it. However, an HSA is money that’s yours. So, I like to try to frame it as more of a 401(k). Once you put money in, it’s yours forever whether you switch out the plan, whether you leave the company, whether you need it, it’s there.

Emphasizing the S is the key to framing health savings accounts that even many healthcare providers still need to figure out. I went for my annual visit a couple of weeks ago, and even my doctor said, “Well, you can use your HSA to buy a spinning bike.” I said, “Maybe, but why would I do that?” She said, “Well, you have to use it up before the end of the year.” I responded, “No, that’s your FSA.”

The one thing that really trips people up, and one of the most frustrating things for me as a practitioner, is that HSAs are complex, and the IRS has not done a good job of making them less complicated. Some of the rules are just really annoying and frustrating. I am a founding member of the Plan Sponsor Council of America’s (PSCA) HSA committee. We advocate very strongly to make HSAs simpler, but for now, to deposit money into a health savings account, you must be enrolled in a high deductible healthcare plan (HDHP). This is the most confusing for people because they think of the HSA as paired with HDHP. When they roll off the HDHP, they feel like they must spend their HSA assets down. I did this very thing until I learned more about the HSA. I piddled away some savings that could have been there in the future when I ended up having some significant health expenses in my 40s.

Once you enroll in Medicare, you’re no longer eligible to make deposits to an HSA. So, that can come in as a useful planning tool for clients who are planning to retire or maybe even are working past the age of 65 and thinking, “Oh, I should just go ahead and enroll in Medicare Part A just to make sure I don’t screw anything up.” The caveat is that if you want to keep funding your HSA, you can’t have any other coverage. This often confuses people because you can have money in an HSA, and you can spend it at any time no matter what your coverage is, but you just can’t put more money in unless you qualify.

We all know that HSAs are triple tax-free, but what that really means is that you can even make lump sum contributions to your HSA up until the tax filing deadline. Many people will set their HSA deposit amounts at open enrollment, not realizing that they can switch it or add more to it after-the-fact. It’s more like an IRA in that regard, but the biggest thing is that it’s a deduction. While it’s in there, it grows tax-free, so it’s like a traditional IRA or a traditional 401(k). And upon withdrawal – if it’s for qualified medical expenses – it’s also tax-free.

For 2021, the contribution limits are $3,600 for individual coverage and $7,200 for family coverage. If you’re 55 or older – not 50 – you get an additional $1,000 catchup contribution per person. The big thing to know here is that if you are two spouses over age 55 on the same plan, the second spouse needs to open their own HSA to contribute $1,000.

Advanced Facts and Health Savings Account (HSA) Strategies

You can use your HSA to pay long-term care insurance premiums for the rest of your life. If nothing else, over funding the HSA up to the maximum amount and letting that money build up to provide long-term care insurance might be enough of an incentive to offer your clients.

Another asset retention opportunity is that most clients and retirees tend to be withdrawing money from their IRAs to pay for retirement healthcare. If they have an HSA – even if you are not holding it – they can use their HSA to pay for these things and keep their money in their IRA with you.

You can use your HSA to reimburse yourself for Medicare Part B and Part D premiums, which many people don’t realize. Medicare premiums – as you probably know – come out of your Social Security check. Still, you could make a $145 per month withdrawal from your HSA and use your Social Security check or your end of year tax form from the Social Security administration as your receipt to show that you’re reimbursing yourself for that year’s premiums.

Many people don’t know this, but you can move your HSA even while you’re actively contributing. When I discovered with a previous employer that my HSA was portable, I went to my HSA provider once a year and did an indirect rollover of my HSA to a better HSA provider. It’s kind of like the IRA indirect 60-day rollover rule.

If you’re helping your clients with portability of their HSAs, make sure you have them check into any fees. Not all providers work this way, but once a year, you can do a rollover to an investment account if the intent is to building investment funds.

The other thing to understand is you can spend your HSA dollars on any tax dependent. A married couple might be on different healthcare plans. The husband has an HSA; the wife does not. Let’s say the wife works for a firm that has a great PPO plan with very few costs, so she stays on that plan. The husband uses the HSA and has the kids on his plan.

The husband can put $7,200 into the HSA for the family and even spend it on the wife, even though she’s not on the plan. She is a tax dependent. This also includes parents. If any of you or your clients have elderly parents who have moved in with you and become taxable dependents, you can use your HSA to pay for their medical expenses if they’re on your tax return.

There is a one-time IRA rollover provision. Every HSA holder has a once-in-a-lifetime opportunity to rollover IRA money into their HSA up to the annual limit to pay for an expense. This is only applicable if you had somebody who had an HSA that hadn’t been funded. Maybe they put in $30 a paycheck. Then they end up with a considerable medical expense that they don’t have any cash for anywhere else to cover it, and they’re thinking about taking an early distribution from their IRA. It’s better to roll it over to the HSA and then pay it out of the HSA for a tax-free distribution. You can only do this once, and you can only do it up to the annual limit, so it’s not a huge opportunity, but just something to know.

The Super Health Savings Account (HSA)

How the Super HSA works is essentially it takes advantage of or addresses the fact that you must be a taxable dependent to use somebody else’s HSA dollars.

For people who have college students who are over the age of 19, you probably know you can’t claim them as a dependent anymore on your tax return. You may be able to get deductions for tuition you pay on their behalf, but you don’t get that little tax deduction like you used to. But they can stay on your plan up until they’re 26.

When I worked at Financial Finesse, I spoke with many early-career employees who opted to stay on their parents’ plan just for simplicity. They didn’t feel like figuring out open enrollment. They weren’t sure about staying in-network. They were still transitioning into adulthood, so they stayed on their parents’ plan. The issue is that they can’t use their parents’ HSA dollars.

The good news is that they can open their own HSA because they’re enrolled in a high deductible healthcare plan. Families with children between the ages of 19 and 26 who are still enrolled on the healthcare plan can contribute an additional $3,600 (2021). If you have a client who may be looking for some tax planning opportunities from a family perspective, they have up until April 15, 2021, to fund an HSA using the 2020 limit of $3,550, and the child would get the tax deduction because the HSA is in their name.

This strategy is not as useful for parents, but at the end of the day, the family with parents that are over 55 and one child could save up to $12,800 in an HSA.

Another key planning strategy with HSAs is that there is no time limit for distribution reimbursements from your HSA. Suppose you have clients who have accumulated a lifetime of medical expense receipts, and they’ve kept that money in their HSA. In that case, it can be a powerful way to distribute money tax-free even without a lot of medical expenses in retirement. This is often an objection that people will put forth about overfunding an HSA. “Well, what if I’m super healthy? What if I don’t need it in retirement?” You can still use it, and there are ways to do that.

In the HSA rules, the age of 65 is crucial. At that point, you can withdraw HSA money without penalty. This is where you can overcome that objection of “What if I don’t need all this money?” You’re talking to a 30-year-old who says, “I could have $600,000 in my HSA by the time I retire. What world am I going to live in that I’m going to need $600,000 for medical expenses?” At age 65, you can tap that money just like it’s a 401(k), but if you happen to need it for things like long term care, medical expenses, or Medicare premiums, then it’s tax-free. If you withdraw money from your HSA before 65 and you don’t have a qualified medical expense to support it, then there’s a 20 percent penalty. In that case, you’re better off raiding your retirement savings account versus the HSA.

Examples of Different Coordination Strategies

Let’s start with someone at the beginning of their career. Let’s say they have the option to contribute to a 401(k) and make an HSA contribution.

The first dollar they contribute to these accounts should be the first year they’re enrolled in an HSA. You need to put at least $1 in to start your eligibility to use it. People make a common mistake because they open their HSA, enroll in a high deductible healthcare plan, don’t put any money in their HSA, and then have a medical expense. Technically speaking, they’re thinking, “Oh, I’ll just put the $150 of my medical bill in my HSA and reimburse myself.” They’re not eligible to use their HSA for medical expenses even if they’re not on a high deductible healthcare plan in the future.

If people save more than their match in their 401(k) and not maxing out their HSA, without any change to cash flow and, in fact, an increase in cash flow, you need to dial back to just the match in the 401(k) and then max out your HSA. For example, if you’re putting 10 percent into your 401(k) but you only get a match on the first five percent, shift that five percent of pay into your HSA. Not only is there no change in your cash flow, but you are going to see even an increase in your net pay because HSA money is a deduction from your FICA as well. A 401(k) is only a federal and state tax deduction. HSA money comes out before we even withhold for Social Security and Medicare.

Now, why does this make sense? First, the main reason people tap their 401(k)s and IRAs early and pay a 10 percent early penalty in taxes is because of medical expenses – unexpected, crippling medical expenses. Why not have that available in a tax-advantaged account versus a tax-deferred account where you have penalties for early withdrawal? This only makes sense if you can let your HSA dollars accumulate and invest most of your HSA money similarly to the 401(k).

Now once you’re saving in your 401(k) to the match and you’re maxing out your HSA, then if you have extra dollars, it makes sense to return to the 401(k) or – depending on the plan – fund an IRA or a Roth IRA. That will depend on the availability of different tax planning mechanisms through workplace plans.

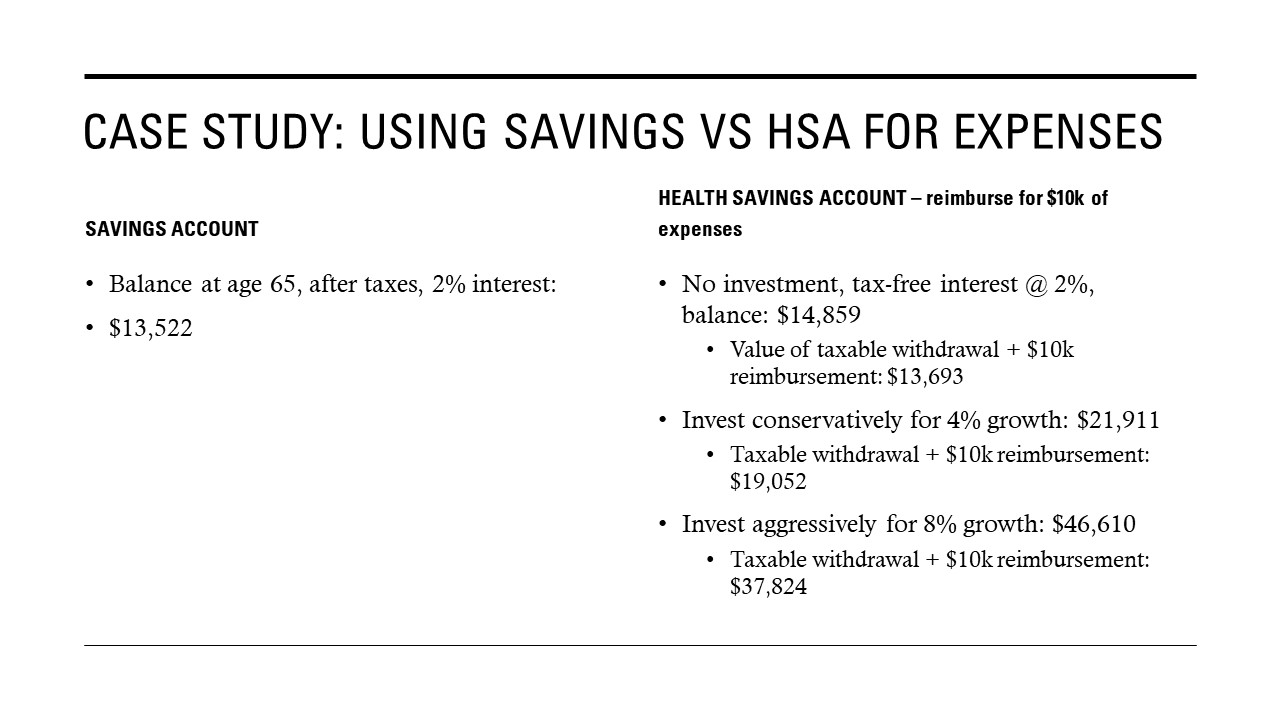

For the example below, let’s assume that a 45-year-old person is financially secure. They have emergency savings set aside, they’re debt-free, they’re at least getting their match in their 401(k), and they’ve got $10,000 in savings that is not earmarked for anything special. If these assumptions aren’t met, and they are still paying off student loans or higher interest rate debt, it would make more sense to use their HSA for medical expenses. But we’re assuming that they’re able to super fund the HSA and let this money ride for 20 years. They’re in a 24 percent tax bracket, and – throughout those 20 years – let’s assume that they have $10,000 worth of medical expenses.

So, if they were to leave that $10,000 in their savings while using their HSA to cover their $10,000 worth of medical expenses throughout those 20 years of working, at the age of 65, they’d have $13,522 in their savings account after paying 24 percent taxes on the interest that account earns.

Let’s say instead they spent their savings down and let that $10,000 stay in their HSA, and it earns, again, two percent. At the end of 20 years, they’d have $14,859 because they’re not paying taxes on the interest. Let’s say then at age 65, they want to take out the future dollars tax-free equivalent to reimburse themselves for the savings they spent on medical expenses. The remaining taxable $4,859 would be taxable, so they’ll have $13,693.

A reasonable person who will keep $10,000 in their HSA is at least going to invest it conservatively at four percent growth. At age 65, they will net out $19,052 after withdrawing the equivalent reimbursement for the future value of the $10,000 of medical expenses. If they invest more aggressively at eight percent growth, they’re looking at a net $37,000 of savings.

Here’s another example of Ben and Shelby, both age 30. Ben is in the HSA eligible healthcare plan because he wants an affordable plan. In general, the HSA eligible plan – especially in workplace plans – is the cheapest premium. He’s looking for the cheapest premium, and he’s a pretty healthy guy. His goal is to balance his current costs with his long-term goal of having some money in his HSA.

On the other hand, Shelby is in the FIRE (financial independence, retire early) movement. She is looking for a way to retire early, and her HSA will support that goal. Her goal is to retire at 55. Why 55? Because at that point, she can withdraw from her 401(k) penalty-free, and she’s got ten years to plug the gap for healthcare.

Ben saves to the match in his 401(k), then puts $2,000 a year in his HSA, which is his plan’s deductible. He’s funding just enough to make sure that he at least has enough for his deductible, and on average, he spends about $1,000 a year of that money. After a while, he decides to loosen his grip a little bit and invest in a balanced fund. He achieves four percent growth over his 35-year career. At retirement, he has about $74,000 in his HSA. Not bad for somebody who’s buying the cheap premium plan, putting money in the HSA tax-deductible to fund his current medical expenses, and having $74,000 leftover to help with retirement medical expenses.

Remember, Shelby wants to retire at age 55. She’s maxing out her 401(k), $19,500 this year, and she also is putting in $3,550 (2020) into her HSA. She invests right away by rolling her money over to a provider that allows her to invest it in equities. At the age of 55, she has about $260,000 in her HSA to help her achieve her FIRE goal.

At age 55, Shelby uses her HSA to pay her COBRA premiums while she is unemployed. You can use your HSA to fund COBRA if you’re on unemployment, but you cannot use your HSA to pay other healthcare premiums except for Medicare. Once her COBRA expires, she enrolls in critical care – so super cheap insurance that she has to pay out of pocket – but her HSA is there for actual medical costs. (We’re assuming Shelby is healthy.) She doesn’t have many medical costs, but if she were to fall and break her leg on one of her adventures in her late 50s, her HSA would swoop in and cover the cost because her medical insurance is anemic.

Then once she’s 65, she uses it for Medicare premiums, and – because, during her 25 years of working, she did accumulate some medical expenses that she didn’t use her HSA for – she can reimburse herself for prior year expenses. She uses it for some tax bracket planning. In other words, you might talk to your clients about filling up your tax bracket each year. Once she’s at the top of her tax bracket, she uses her HSA to reimburse herself for previous expenses versus taxable withdrawals. Because she has a certain balance at the age of 65, she may even be able to forego buying long-term care insurance knowing that she can self-fund with her HSA.

Ben, on the other hand, because he uses his HSA throughout, only has enough to pay Medicare premiums, pay for his hearing aids, and the other costs that he might have as a retiree. He also uses his HSA to pay for long-term care insurance premiums.

It’s worth pointing out a few things here:

- Be sure to your receipts to allow yourself those tax-free reimbursements in the future.

- HSAs aren’t just for co-pays or your standard medical bills.

Keeping good records is paramount if you’re going to engage in these tax-free withdrawals for prior year expenses. Save those receipts when you buy eligible products and supplies. The way I manage it is I keep an app on my phone called DocScan. I take a picture of all of my receipts, keep them in a file labeled with the current year, and – when I’m ready to engage in this HSA reimbursement game – then I’ll go year-by-year and add up all my 2020 receipts. Whatever that adds up to, I’ll take that withdrawal out, and then – if the IRS ever asks me to justify it – I send them my 2020 file. The other thing to note is that it’s on us – because these are consumer-driven healthcare plans – to retain and prove that we spent this money on HSA-eligible expenses even if it was 20 years prior.

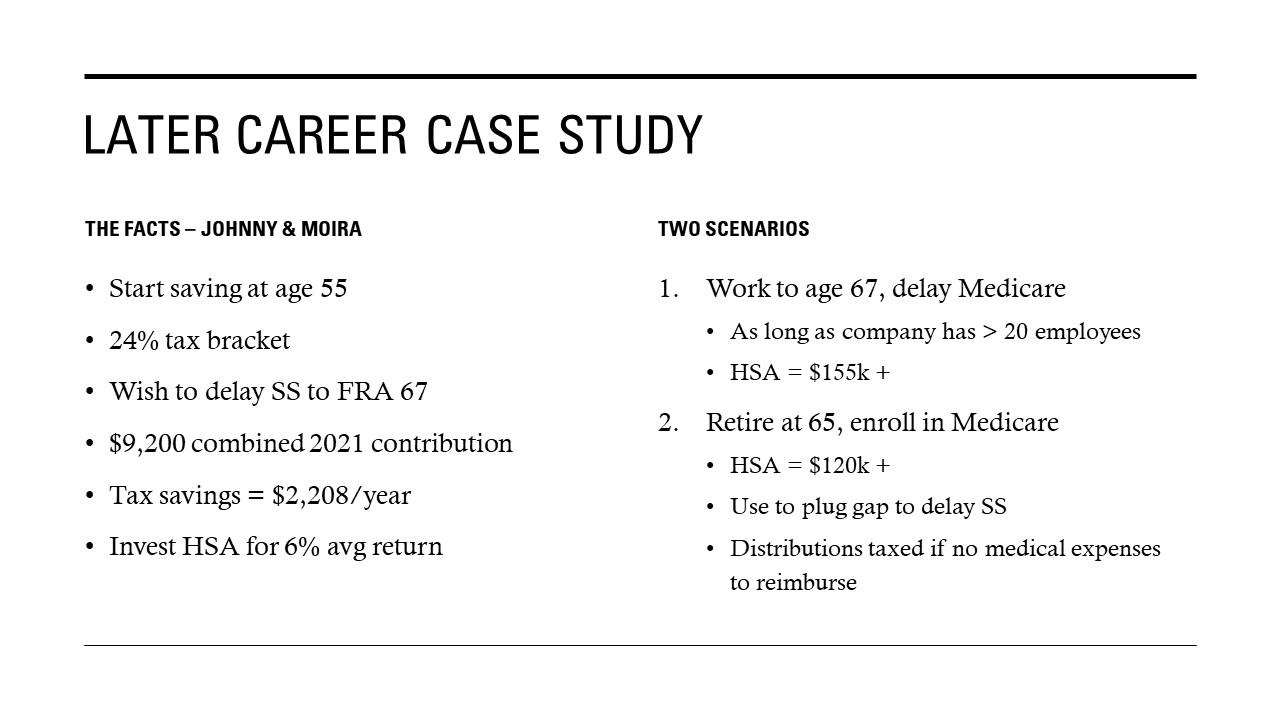

One final example is a married couple, Johnny and Moira, who didn’t care too much about money until later in life. They learned about their HSA from their advisor at the age of 55. They’re in the 24 percent tax bracket, and their goal is to delay Social Security until their full retirement age, so $9,200 will be their 2021 maximum contribution.

Now, if Moira is on Johnny’s plan, she would have to open her own HSA to make that extra $1,000 catchup, but Johnny would put the initial $8,200, which is the $7,200 family limit, plus the $1,000 catchup for him. Moira must do her $1,000 catchup into her own HSA. The good news is there are more and more consumer HSAs out there. At a $9,200 combined contribution with a 24% tax rate, they’re saving $2,200 in taxes per year. They are going to invest their HSA at a 60-40 mix for 6% growth.

So, let’s look at two scenarios. The first scenario is that they decide to work until they’re 67, which means they will delay Medicare. Why is this a key fact? If you are on a work-based plan with an employer that has more than 20 employees, you can delay Medicare until you retire. Because Johnny and Moira want to continue to contribute to the HSA, they decide to do that. They keep funding the HSA up to age 67 while they’re working, and then – the day they retire – they’re enrolled in Medicare, with no lifetime penalties, no delays, and they’ve got over $155,000 in their HSA.

The other scenario is that they retire at age 65. So, they go ahead and enroll in Medicare, so they must give up a couple more years of contributing to their HSA than they would in scenario No. 1. But here, they can use the HSA to plug the gap for those two years before enrolling in Social Security. Even if their Social Security would be $30,000 a year, and they don’t have medical expenses that they had incurred from 55 to 65 to justify a non-taxable withdrawal from the HSA, it would be a taxable distribution. They will not pay penalties because they’re age 65. There would still be some money left in the HSA after-the-fact to cover other medical expenses later in life.

Retiree Benefits of the HSA

- Use your HSA in retirement to pay a long-term care premium. You can use it for Medicare premiums.

- You can use it for things like new hearing aids or adding a ramp to make your house a little bit more accessible to somebody who might be using a walker or a cane.

- It allows for that tax diversification. Medicare premiums will go up once your income exceeds a certain amount, and it’s based on a two-year rolling average, and it can help reduce taxation of your Social Security.

- If you still have money in your HSA when you die and your spouse inherits it, they get to retain that tax-free quality and use it for their medical expenses just as if you’re alive. However, anyone else that inherits your HSA – your kids, your grandkids, your next-door neighbor, your girlfriend – is going to have to take an immediate distribution and pay taxes on the money. If a client desires to leave a bequest to a nonprofit, they suggest that they put the nonprofit as the HSA beneficiary. If they end up exhausting their HSA, then they can redo their will to include the bequest in their will, but otherwise, that’s a super tax-friendly way to pass along money to a charity.

Key Takeaways

- HSAs are fully portable, even if you’re still actively contributing.

- Contributions can be made via lump sum up to the April tax filing deadline and can typically be changed throughout the year via payroll deductions. Some employers have rules that may only allow you to increase your contributions. However, anytime I’ve had access to an HSA, I’ve been able to change my contributions throughout the year.

- Medicare enrollment stops the ability to contribute, but not to spend. If somebody’s over the age of 65 when they enroll in Medicare, remember there is a six-month lookback with Medicare where you cannot contribute to an HSA.

- Discourage HSA spending during working years but save receipts for future tax planning. It’s a savings account. If nothing else, it’s there to fund big things in the future. If you’ve got college-age kids, help them fund an HSA that can be there for them when they’ve got kids going to college. It can fund things in the future.

I like to tease young people by saying, “You can save in your HSA to pay for the expenses of children you’re going to have with somebody you haven’t even met yet as long as they’re a tax dependent.” So, don’t spend that money, but do save your receipts. Suppose you end up in a pickle in the future, and you have money in your HSA, and you’ve got receipts for previous expenses. In that case, you can always tap that to get you through, or ideally, in retirement, it will help with tax diversification and tax planning strategies.