The Retiree Medical Coverage Crisis vs. the Retirement Savings Coverage Crisis

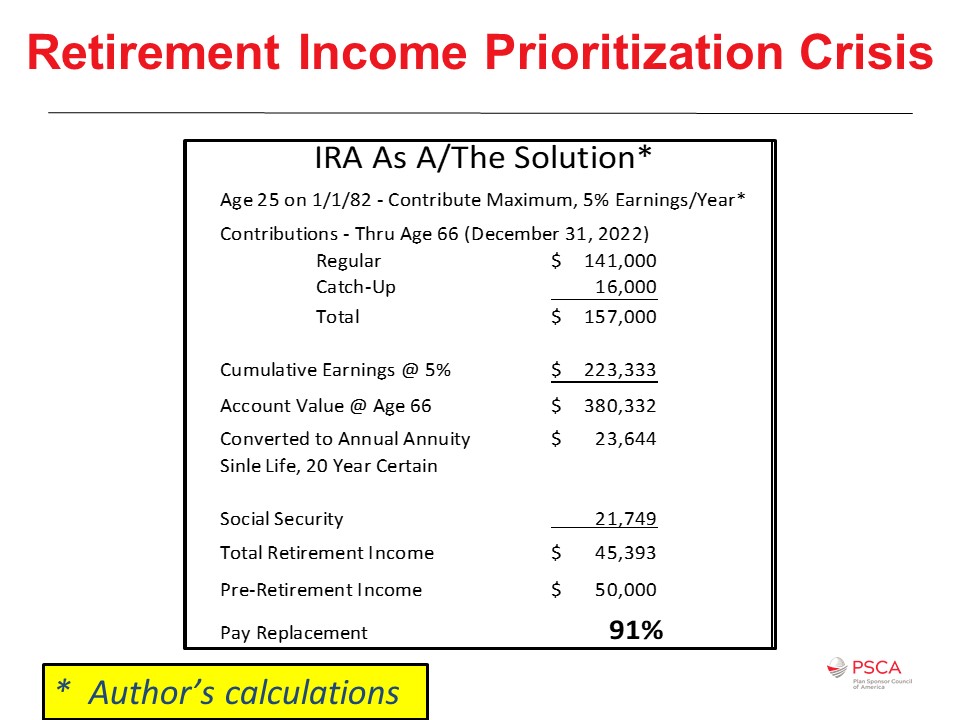

What percentage of wage earners had access to a more than adequate, tax-favored retirement savings program in each of the past 39 years? 100% of us. We’ve all had access to the individual retirement account (IRA) since the 1981 Economic Recovery Tax Act signed by President Reagan starting with the 1982 tax year. Retirement savings isn’t really a coverage crisis or an access crisis when it comes to retirement income. It is a prioritization crisis.

Some might say that the IRA isn’t adequate, but it, in fact, it is for those workers who are not highly compensated employees. The lowly, universally available, ubiquitous IRA as expanded by the Economic Growth and Tax Relief and Reconciliation Act of 2001 – that’s 20 years ago in the George W. Bush administration – is a more than adequate, tax-favored retirement savings plan. Simple, consistent saving in an IRA coupled with Social Security would generally have been adequate retirement preparation for many of the 75 million, or so, baby boomers averaging $50,000 in annual income if they only had the commitment, if only they had prioritized retirement savings and retirement preparation.

Some changes might prompt more savings in IRAs, especially among those who today live paycheck to paycheck. However, not too many folks seem to be interested in that other than mandates, for example, and frankly with COVID-19 and state-mandated Roth IRAs, let’s see what kind of leakage occurs there. If you’d like to see my thinking in terms of income and prioritizing saving, again, connect with me on LinkedIn, and we can have a great debate.

Impediments to HSA Adoption

What percentage of retirees had access to tax-favored retiree medical coverage during the past almost 30 years? According to Kaiser’s annual survey of employer-sponsored healthcare coverage, 18% of employers today provide retiree medical coverage. This, however, likely includes employers who no longer offer employer financial support for retiree medical to new hires. If we adjusted it only for folks who are offering coverage to new hires like you would offer coverage in the 401(k) to new hires, we might come up with a number between 5 and 10%. If we expanded this to include small employers with 200 and more employees, we’d likely end up with only a 1% to 3% of employers who sponsor or contribute to retiree medical coverage.

The HSA is a great solution for funding retiree medical costs. However, most employers don’t offer access. Most employees are not enrolled in an HSA capable health option. More than half of the employers who do offer an HSA capable health option don’t themselves contribute. And when employers don’t contribute, most workers don’t either. The Employee Benefits Research Institute (EBRI) confirms only half of HSAs receive a contribution, and less than 15% of HSA accounts are maxed out, fully funded in a particular year (2016 data) and that only 5% of HSA accounts are invested in anticipation of retiree medical needs. Why is this?

When healthcare was reformed, luckily, they retained HSA capable coverage when they introduced the patient protection and Affordable Care Act of 2010. But it did get a bad rap. Many perceived HSA capable coverage as substandard or inappropriate. Even President Obama said so. Besides lowering deductibles and out of pocket costs, the goal should also include saving and preparing for future expense, especially among the majority who won’t have significant out of pocket medical expenses this year.

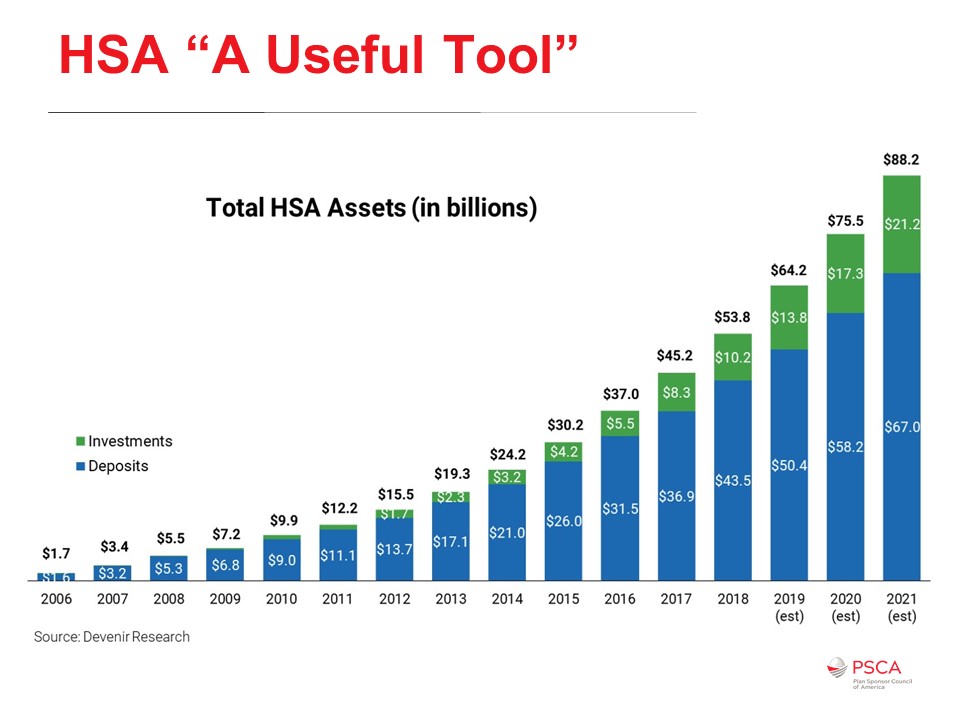

We’ve seen some growth in HSA assets. I wanted to compare the growth of HSA assets with 401(k) assets, but the comparison would likely be more misleading than informative because the 401(k) didn’t start from scratch. Instead, plan sponsors added pretax contribution functionality to existing thrift and profit-sharing plans starting very late in 1981, early in 1982.

For the first few years, the 401(k) didn’t have the 402(g) limit (Internal Revenue Code Section 402(g) limits the amount of elective deferrals a plan participant may exclude from taxable income each calendar year). Even when it was added to the tax code, it came in at $7,000 for 1987 and has been increasing pretty much ever since. Today, the annual maximums for 401(k) contributions for 2020 are $19,500 and a $6,500 catch up. The catch up can start at age 50 for a total annual contribution of $26,000.

The HSA limits are much more modest. The 2020 annual maximum for single coverage is $3,550, and for non-single coverage (family), it’s $7,100 plus $1,000 catch up per individual age 55 or older. But combined, a 55-year-old preparing for retirement who has non-single health coverage with a spouse the same age can contribute $35,100 a year, and if both spouses are employed, we’re talking almost $60,000 a year if the two spouses can afford it.

Is the deductible for a high-deductible health plan really that high? Well, back in 1984, I had a $200 deductible in my healthcare coverage. If I were to index that for 35 years of medical premium increases, that $200 increases more than 10-fold to exceed $2,000 today. Instead of indexing the deductible for inflation, many plan sponsors allow their point of purchase cost-sharing – the deductibles, the copayment – to be eroded by inflation. Today’s $1,400 funded with tax-preferred HSA contributions is a much lower percentage of median take-home pay if you were to compare it to, say, that 1984 $200 deductible funded with after-tax dollars, money out of your pocket.

It’s long past time to pay attention to how the HSA capable option is presented. When we offer workers a choice of coverage, too many employers tend to denigrate the HSA capable health option. Most workers can’t accurately compare the coverages where one option uses copays, and the other uses deductibles. The deductible prominence is highlighted by mandates like health reform’s side by side summary of benefits and coverage, which seldom includes the contribution difference or total cost-sharing. Typically, the HSA capable option – where it’s offered as a choice – is priced less expensive in terms of point of enrollment cost-sharing, the employee’s contribution, compared to any PPO or HMO coverage option that’s also offered to that same employee.

Too many plan sponsors have a passive annual enrollment process. You get your current coverage unless you make an affirmative election to change the coverage option that’s already in place. Studies show that American workers spend less than 30 minutes a year on average (averages can be deceiving) making their choices at annual enrollment, a passive default process that ensures that most are going to ignore any new choices. So, one thing that I always recommend folks consider is changing the default at annual enrollment to the HSA capable option. Even if you enroll them, if it’s the default, and they reduce their HSA contribution, or even if they opt-out of making HSA contributions, there’s nothing wrong with a default re-enrollment mid-year to make HSA contributions or to increase the HSA contribution mid-year.

As an aside, one of the items we really need to acknowledge is just how important an issue deductible prominence is. The reason why we need to kind of focus on this is because few workers meet their deductible each year. Eighty percent of medical expenses are incurred by less than 20% of the population. Benefits folks sometimes call that the Pareto principle. For example, if you have a $1,400 deductible, perhaps as few as 10% of individuals will satisfy that deductible. And importantly, those who do satisfy the deductible probably don’t do that every year. Think of it also in the not single coverage, that’s $2,800 deductible at a minimum, and all of a sudden, you’re talking about just 5% if it’s only one individual in the family who is incurring significant expense.

Why select the PPO with the lower deductible and the higher employee contribution? Why do employees do that when given the choice? Keep in mind that as many as 74% of Americans live paycheck to paycheck where a one-week delay, not missing the next paycheck, but just a one-week delay in their next paycheck, would cause some or substantial financial difficulty (Getting Paid in America, an annual survey by the American Payroll Association). It’s been consistently in the high 60s, low 70s. The Federal Reserve’s Household study shows that 40% of American households don’t have cash on hand to meet an unanticipated $400 expense. Because of that financial fragility, many stick with the health insurance option that has the lowest deductible. They over-insure even though it may not be the best choice for them, not this year and certainly not long term.

The other challenge is that when adding an HSA capable healthy option, too many plan sponsors fail to adjust the PPO, point of purchase cost-sharing so that it has the same deductible structure as the HSA capable option. I can confirm that the only way to get all workers to consider a new option is to amend or eliminate the existing choices substantially, make sure side-by-side comparisons are complete and not misleading, and to change the default at annual enrollment. You need an affirmative election process. Even knowing so many live paychecks to paycheck, and also knowing so many are over insured and financially fragile, too many employers don’t take steps to get workers over the hump.

Which Comes First, the HSA Chicken, or the 401(K)-Nest Egg?

How do we prioritize saving between the HSA and the 401(k) and doing what I call quadruple duty?

Many workers don’t have to choose between the saving in the HSA and the 401(k). They can max out both, and others can at least contribute enough to obtain the full employer financial support in both accounts. Sometimes, all you have to do as a plan sponsor is open the HSA account, and sometimes the employer will do that by making that initial employer contribution.

Many times, if the employer is using what’s called the comparability method for nondiscrimination in employer contributions to the HSA, just simply opening that account will ensure that employees get the employer contribution towards the HSA. However, it’s clear which one should take priority if we’re thinking about retirement preparation, and that would be the HSA. We know that as much as 20-25% of retiree’s costs in retirement are healthcare premiums or healthcare out of pocket expenses, or maybe even long-term care premiums and long-term care out of pocket expenses. The big difference is that the HSA contributions are made pretax for federal and state income taxes as well as for FICA and FICA Medicare (med), the Social Security, and the hospital insurance contributions that come out of every paycheck.

For comparison, 401(k) contributions are pre-taxed for federal and state income taxes but post-tax for FICA and FICA med. They were once pre-taxed, but that changed due to the Social Security Amendments Act of 1983. The other big difference, of course, is that HSA assets, when used to cover qualified expenses, are distributed tax-free. However, prioritizing the HSA contributions over the 401(k) may not be the right answer for those who live paycheck to paycheck, those who are not able to fully fund both accounts, or those who don’t believe they can afford to contribute enough to receive the full employer financial support in both options.

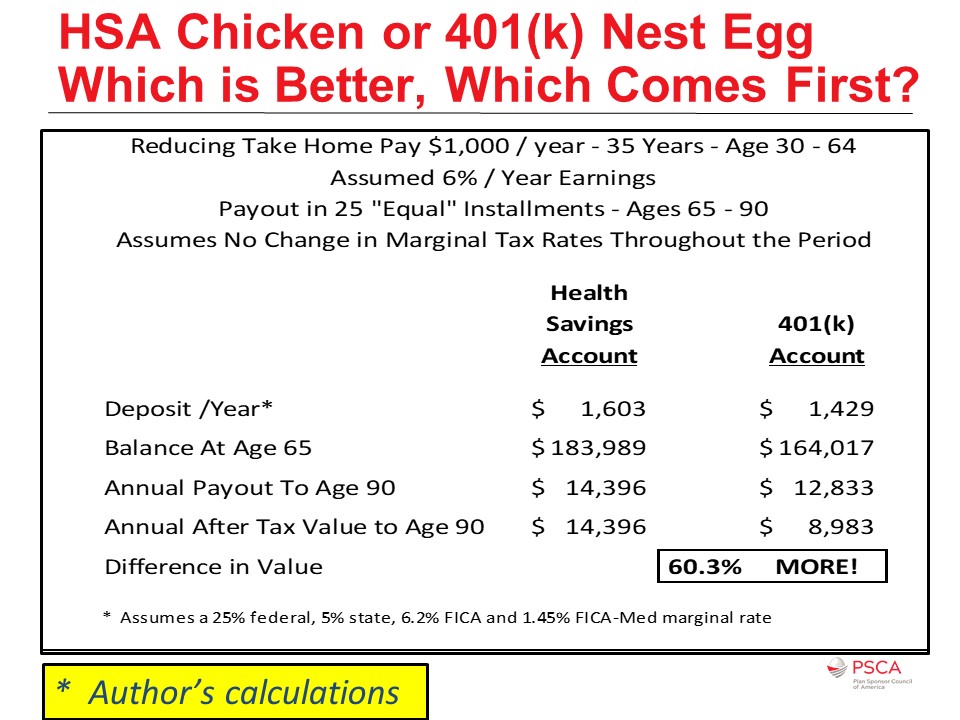

The right answer will vary from situation to situation. Here, I made some assumptions to give you an idea about why you might want to contribute to one before the other.

I assumed here that the HSA uses the comparability rules for the employer contributions, and that the 401(k) or the 403(b) plan has a match and that it also has a robust plan loan functionality and that both accounts are subject to true-up, that the employer contribution will be the same regardless of when the employee makes contributions throughout the year. In this situation, a worker would want to consider seeding the HSA even with just $1 to start that claims clock. Only expenses incurred after the HSA has been opened, typically in most states, you can’t open it except by putting in at least a buck. So, again, you want to start that claims clock for eligible expenses.

Then you want to prioritize contributing to the 401(k) until you’ve obtained the full match. Then you want to start regular HSA contributions, and maybe gap-fill any hole in your take-home pay with a 401(k) or a 403(b)-plan loan. HSAs don’t allow you to take plan loans. Most 401(k) and 403(b) plans do. You want to contribute to the HSA until it’s fully funded, that’s that $3,550 or $7,100 (for 2020) amount, and then resume 401(k) contributions as finances permit. Remember that there’s no coverage crisis for retirement income. The IRA is available to all wage earners.

Perhaps the health savings account’s most significant value is the varied opportunities for tax-favored wealth accumulation along the way to retirement and beyond. Most employees don’t need to look beyond the value in the current year. The HSA monies are certain, and they’re readily accessible, and where they’re not used, growth comes from the investment and is carried over to future years. Monies are generally accessible on-demand at any time. You get to spend the monies that would’ve gone to the federal government, the state government, Social Security and Medicare on your out of pocket qualifying expenses.

The value for tax-favored funding of retiree medical is obvious. It is especially true for those who succeeded in preparing for retirement and maybe end up being subject to Medicare Part B and Part D income-related monthly adjusted amount. Today, that surcharge applies where 2020 AGI exceeds $87,000 for singles ($174,000 for married filers). As the Medicare trust fund runs dry, (according to the most recent report, it’s still going to happen in 2026) and as budget deficits and national debt skyrocket, it’s important to remember that Medicare Part B and part D are primarily funded with general tax revenues. The bottom line with those kinds of trends and challenges we should all expect that Congress will raise funding for Medicare Part B and Part D by lowering the income threshold for the income-related monthly adjustment amount.

Some folks are going to be lucky. They’re going to be in perfect health for 10, 20, or 30 years in retirement, and if so, they can spend those HSA dollars on nonmedical needs and wants. If they take the money after reaching age 65 for nonmedical needs and wants, in general, it subjects them to regular income taxes the same as if they were 401(k) dollars. Like any other deferral, federal income taxes are going to be based on the rates in effect and your marginal tax rate based on your total income and the state income taxes that apply. Finally, no matter your situation, any residual HSA account assets can be used by your surviving spouse or another tax dependent after you die. Then, any unused residual is then paid to beneficiaries as taxable monies. So, there’s no waste. There’s no forfeiture. It does quadruple duty.

Key Takeaways

The deductible for an HSA capable healthcare plan is not high. It never was. It’s just that we failed as plan sponsors to index our point of purchase cost-sharing for medical inflation. Creating a fair comparison, a fair informed choice during annual enrollment, will almost always require the plan sponsor to make changes in any other available coverage options those that are not HSA capable.

It’s springtime in America. So, remember to seed the HSA account. Maybe even seed the account each year, and if you’re a plan sponsor, and if you offer an HSA capable coverage option today, you can still seed the account this year. You can contribute today for those who enrolled in an HSA capable health option but failed to open their HSA.

Something else you may want to consider is to introduce employer-sponsored, retiree-pay-all, fully insured Medicare Advantage options. The most important words there are retiree-pay-all and fully insured. If you introduce it along those lines, typically, you can minimize any exposure, any liability reporting, under FASB 106, FASB 158. You want to give employees a target. You get to add some new benefits this way without adding to your expense or adding new liabilities on your financial statements, and it just might help workers prepare for retirement or maybe even help older workers transition into retirement. We’re talking Medicare Advantage options, which means we’re not talking about early retiree medical coverage. EBRI’s Retirement Confidence survey shows that increasingly folks expect to work longer these days. Giving them this target is going to be beneficial so that they know there is going to be an opportunity perhaps for me to access retiree healthcare coverage when I leave this particular employer.

Remember that the top 50% of wage earners, those who earned an excess of $40,000 (the median in 2016) paid 97% of all of the income taxes. Tax-free HSA distributions can be used to cover part B and part D premiums, long-term care insurance premiums, as well as out of pocket medical and long-term care expenses and doesn’t add to your federal and state income tax bill.

There is never any waste when it comes to your health savings account assets. Sooner or later, one way or another, you, your surviving spouse and dependents, or your named beneficiaries receive the value from your account. It’s what you get versus what you get to keep after taxes. Right now, when used for qualifying expenses, what you get is what you get to keep.