Secondly, the index component is a fixed indexed annuity. This means that the return is linked to an index, whether that’s an ETF, blend of indices, etc., but there is no direct investment in an index. These are promise products from an insurance company. They have a reference index without actually providing the direct index performance and protection from loss.

The third component is guaranteed income, particularly in the form of an income guarantee, whether somebody is looking for income today or in the future, such as guaranteed lifetime withdrawal benefit (GLWB), guaranteed minimum income benefit (GMIB), or other riders. These are the primary way clients receive guaranteed income from an FIA. FIAs can be annuitized, which is rarely done.

What Role Does a Fixed Index Annuity Serve in a Portfolio?

An FIA is a fixed income replacement because we expect the returns to be fixed-income-like with the possibility for more upside potential. The guaranteed income is either through an income benefit or through some form of annuitization. These products work well for people who want to supplement or delay Social Security and may want some other form of guaranteed income on top of Social Security or help them get to that point.

Another element of these income benefit guarantees is that you may want to have or provide a safety net of future income. It’s something that the client might end up not needing or might want to use those assets differently in the future. But you want to put the guarantee in place. This is a pretty common utilization of these products. It’s not necessarily the most economically efficient, but it’s certainly understandable that people want security. These products are also often used for systematic withdrawals, which is a non-guaranteed form of income.

Lastly – and this has actually nothing to do with the annuity component in itself –sometimes folks invest in an FIA because they want life insurance through the death benefit for somebody who’s uninsurable or very difficult to insure. This is not that uncommon, particularly now. Long-term care benefits are another thing people try to access through an FIA. These are other valid use cases for the FIA that are not necessarily core to the product’s functioning.

How Does a Fixed Index Annuity Work?

The basics of it are you are limiting downside to a floor of zero, so you cannot lose money, and in exchange for that, you are provided upside that is modified. It’s the interaction between these two things that end up giving you the yield.

With an FIA, we take an index, and we push the index through the crediting strategy. It’s neither the index itself nor the crediting strategy alone that provides the yield; they function together. The index is the reference asset, and the crediting strategy determines the shape of the yield that comes out the other side and how that credited interest is applied.

One of the components of any fixed annuity is that it’s “free” – there are no explicit fees. But there are costs. Everybody gets paid for the work they do, including the insurance company. But it may just be that you’re not paying an explicit cost. The costs are implicit; they’re not a line item charged as a percentage of the contract. But they manifest in the rates paid for the crediting strategy.

There may be some explicit fees: the index itself may have a fee, the crediting strategy may offer higher upside potential for a fee, and additional benefits such as an income or death benefit may have an explicit fee.

If there is an explicit fee, it will be deducted after you calculate the 0% floor, so it is possible that the fee can reduce the account value below the original starting principle when there is no or close to no interest. But it’s important to know how that works, that the end credited interest comes first, and then the fees are taken off of that.

How Do Insurers Price a Fixed Index Annuity?

How the carriers price these products is actually fairly straightforward. The first thing they do is very similar to what they would do with a regular fixed annuity. Most of the money from the premium goes into fixed-income investments to establish the principal guarantee that causes interest-rate sensitivity. Some carriers use zero-coupon bonds to return principal at some point in the future. This step is the base for the principal guarantee.

Step two is to establish the options budget. From this money, the insurer pays for everything that it takes to run these products, such as administrative fees, distribution, the insurer’s profit, compensating for the use of capital for reserving, and other expenses that must be covered. Whatever is leftover is the options budget which is the pricing component where we see the effect of volatility.

Why is volatility so important? It’s crucial to the actual pricing. The volatility of the reference index drives the cost of the options, which is the basic math that determines the rate or upside potential. For example, with the same budget, if you have an option that has a lower cost, you can buy more of it, which is why there are different rates based on a specific index to which the product is tied.

Though it may be counterintuitive, lower volatility can increase yield with all things being equal. Having fewer periods where you have zero to negative returns can equate to a higher net yield. Volatility also affects the stability of renewal rates because lower volatility options have more stable pricing in general. These are things to think about in the pricing dynamics.

Most products have a rate guarantee in the first year. After that, you have a renewal rate, and the renewal rate can change. It may well be that the insurance company wants to keep that renewal rate stable and will do that even when there’s some fluctuation in the market. But there’s no promise of that, except obviously in the case of products that are designed that way. There’s a little bit of a “trust me” relationship between the insurance company and the client over the renewal rate.

With higher volatility options, the insurance company has to consider how they want to handle the price movement of the options for a highly volatile index. However, if you have a lower volatility option, you’re just not going to see that kind of price movement, so it naturally makes renewal rates much more stable. Suppose the renewal rate is a high concern. In that case, particularly if it’s an insurance company that you don’t know what their renewal rate practices are, you can estimate it based on the index’s volatility. The chance of the renewal rate being stable over time is much greater when you have a lower volatility index.

What Indices are Used in Fixed Index Annuities?

We’re very familiar with the broad market indices, like the S&P 500, which is ubiquitous. Russell 2000 is another example. All kinds of indices have typically been used that have common characteristics of being equity indices that are highly volatile; therefore, they are subject to all those pricing issues.

The pricing issues also apply in different types of market environments. If you think about where we are today with low interest rates, the volatility component can push the yield down on something highly volatile when volatility is higher. We certainly have seen this expressed in rates.

The indices can be blends of other indices or exchange-traded funds (ETFs), or some combination thereof. They can simply be a traditional broad market index that is in a lower volatility form. They tend to be unique to the insurance company. So, the carrier develops a relationship where they’re the only ones that are allowed to sell a particular index, and they may put it across many different products. Still, you won’t find the same index populated in other insurance companies products. Understandably, we see many people getting confused because there are so many different indices out there. There’s no consistency because insurance companies want to have their unique index.

There are performance components that can be helpful in terms of the ultimate yield. Some of these indices do some rebalancing or reallocation in response to market changes, though that’s not the predominant design.

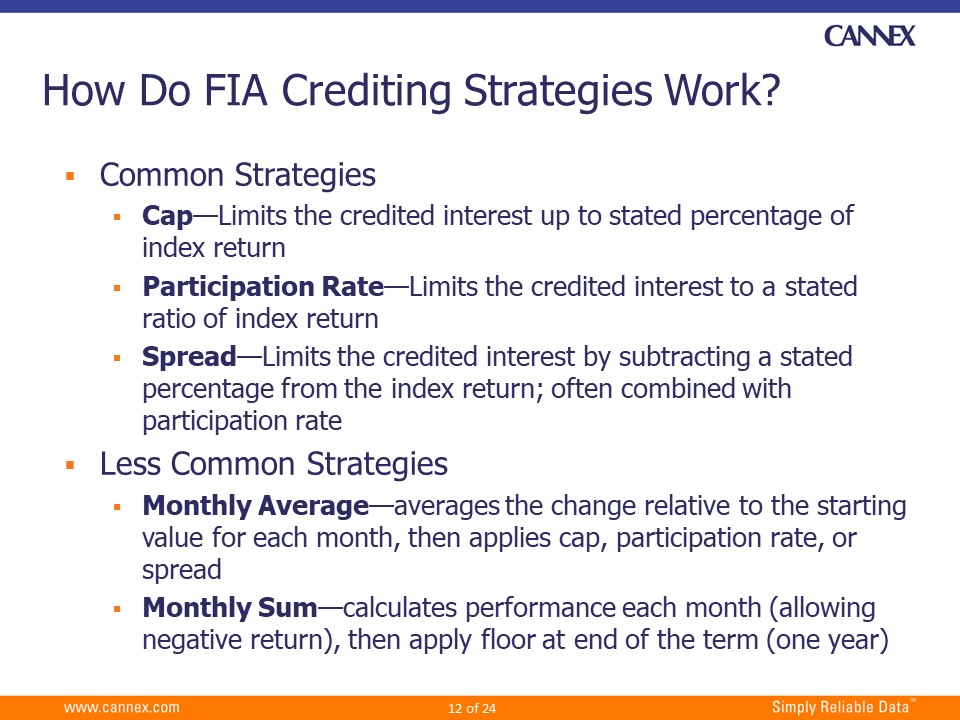

How Do Fixed Index Annuity Crediting Strategies Work?

This is not an exhaustive list of what’s available, and companies are constantly coming up with new crediting strategies. The most common strategies are listed at the top.

The Cap crediting strategy limits the credited interest rate to up to a stated percentage. This is the max that you’ll get, and obviously, you’re not going to lose money. The Participation Rate is very simply a ratio of whatever the index happens to return. And the Spread is more of a threshold, and you can get whatever is above that. This is often combined with a Participation Rate where you would calculate the Participation Rate first and then apply the Spread.

The monthly strategies – Monthly Average and Monthly Sum – sound very similar, but they’re extremely different from each other. The Monthly Average takes an average of each month and then applies whatever limitation on top of it. The result of that averaging is a lot of smoothing. This tends to be a more consistent type of strategy because you’re averaging within the course of the year, not just from that point to point. The Monthly Sum crediting strategy is subject to a lot more volatility. When it does its monthly calculation, the term may be an entire year, but then you’re assessing monthly. Within a month, you can allow for a negative return. Because you’re adding that up and then applying the 0% floor at the end of that period, you’re having the potential for negative return in the middle. It allows for volatility in both directions but in particular exposes you to interim negatives.

The term is just the duration of the crediting strategy at the point on which we do the calculations to determine what the interest is or whether it’s 0%. One year is very common, and it’s the most prevalent of the terms. But periods can be much longer, like five or seven years. If you have a five-year contract, and you’re using a crediting strategy with a five-year term, you only have one completed term within the course of that contract. And so, the chance of a 0% return at the end of that is infinitely higher than it would be if you had one-year terms all added up within that same contract period. It affects the yield that you get at the end.

I think that it’s essential to talk about this right now because we’re in a low-interest-rate environment. When interest rates are low, and insurance companies are looking to provide more value to the client, they can look at longer terms. This allows for a more significant upside, but it’s only at the end of that period. When you’re looking at these longer terms, you have to think about how many times that term will be repeated within the contract. With a two-year term in a six-year contract, that’s three repetitions instead of six, one-year terms. When the length of the contract and the term are identical, the chance of experiencing a 0% yield at the end is possible.

How Do Fixed Index Annuities Perform?

I can’t emphasize enough that an FIA is a fixed annuity. It’s the interaction of the index return with the crediting strategy that gives you the yield.

An effective market conviction is your or your client’s view of the specific index or general market expectations. This should play a role in selecting the index, the crediting method, and the length of the index term.

You can’t nominally compare the rates on different indices. If you have Index A and Index B, and one has a higher Cap or a higher Participation rate than another, you don’t know how one will work in that situation. It doesn’t necessarily mean a larger, higher Participation rate or higher Cap is better. When you see a Participation Rate of 100% or 150%, it doesn’t mean that you’re going to be shooting the moon. It may well be the opposite. The point here is that the length and repetition of the term – how many of them there are, and the probability of having negatives within that term – matter. So, suppose you have a seven-year contract with an index that’s likely to give you fewer negatives in that period. In that case, this can potentially help your index performance, especially depending on the environment.

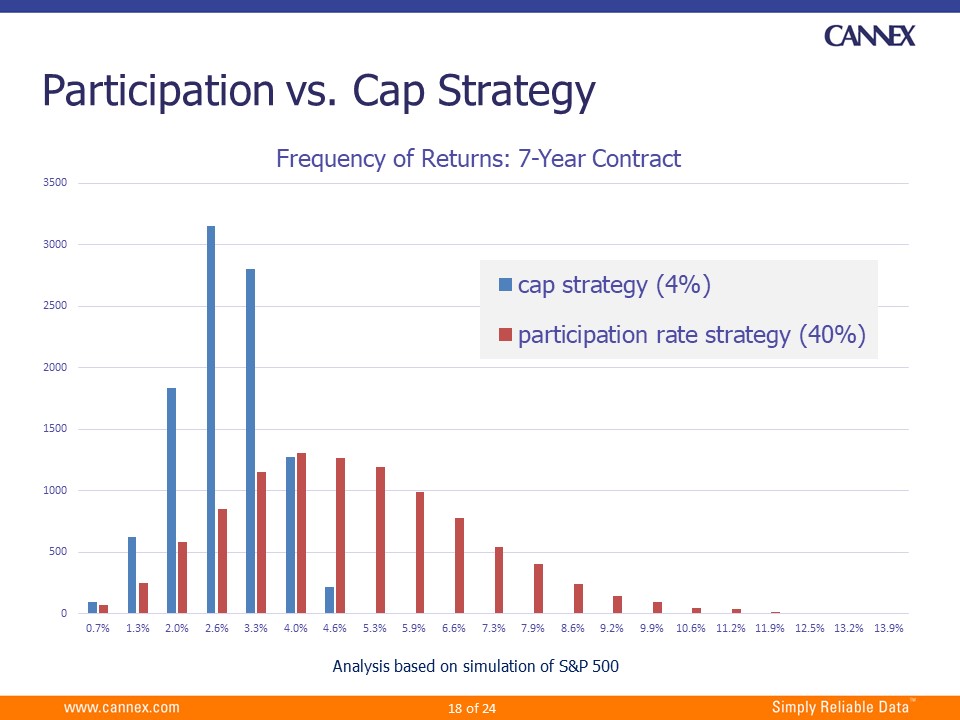

On Cannex.com, under “Thought Leadership,” we have a lot of research that’s available. If you want more details about the assumptions or methodology used on the following, that’s all in the report. This is a Monte Carlo simulation.

The Cap strategy is 4% with a 0% floor. The average ends up being 2.5%, with the shape of the distribution of returns clustering towards the middle. With a Cap strategy, the way to think about it is that anything above the Cap is ignored. You can’t shoot the moon, but you get tighter and more consistent returns over that period.

For the Participation Rate, you earn a ratio of the index performance. In this case, we ran this on a 40% Participation rate and 0% floor. It’s a very different distribution that is much wider than you get with Cap. And in this scenario, the return averages about 4.5%. You may think, well, that seems a lot better than the other. But you have to look over the available rates at the time to assess which would be a better choice. You can see the difference in the performance profile of these two approaches.

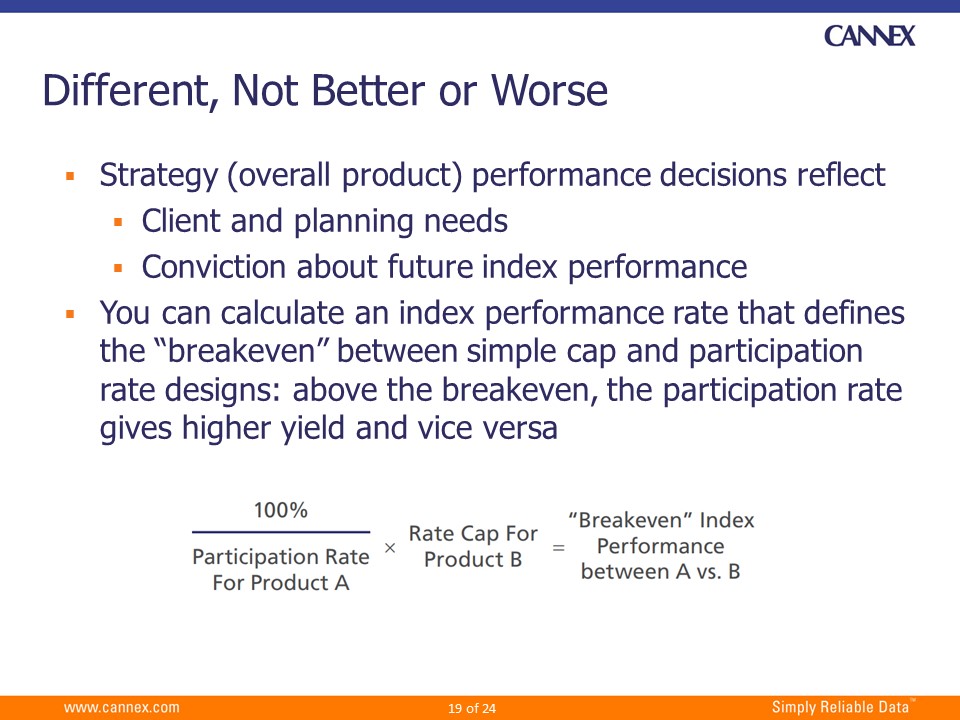

If you have two different crediting methods – a Cap and a Par –you can actually compare them. Our position is that one method is not better than the other; they’re different. It depends on what you’re looking for for the client and their planning needs. And it depends a lot on your conviction about what will be happening to the index in the future or where your concerns or fears are about the future.

Here is a tool to calculate a breakeven rate between the basic Cap and a basic Participation rate.

In the previous example, we had a Participation rate of 40%, and we had a Cap rate of 4%. So, 100% divided by 40% times 4% equals 10%. What this means is if the index performance is below 10%, then the Cap does better. If the index performance is above 10%, then the Participation rate does better in any given year.

Using the current rates from one carrier, same product, to the two different strategies for the S&P 500, a 25% Participation rate, and a 4.5% Cap, the breakeven is 18%. This means that the Cap rate does better if the index performance is below 18%, and the Participation rate does better if it’s above 18%. This is a way to capture what you think will happen in the future and gauging which strategy seems to be a better fit and make more sense.

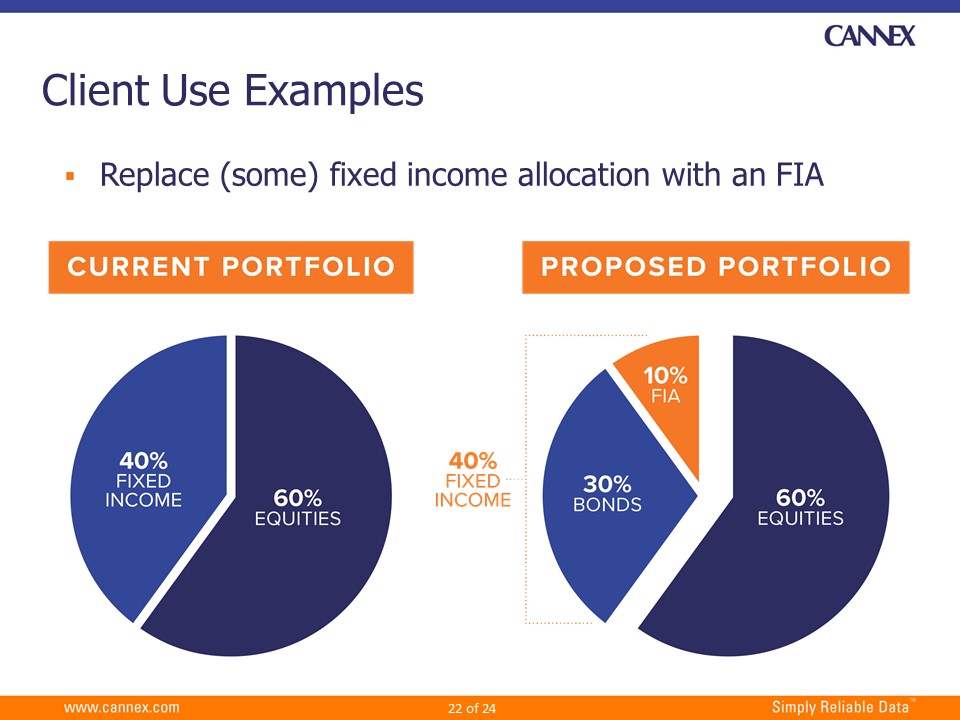

Client Use of Fixed Index Annuities Examples

Many people are using this as a fixed income replacement. The nice thing about thinking of an FIA within the fixed income allocation is that it works well before retirement, before income planning, and into retirement for a chunk of the money within the fixed income allocation. Even if you have a client interested in income later or some income planning but isn’t quite ready for it, the FIA is a suitable place to put that money.

Right now, we see fixed annuities competing against bank CDs because they provide higher yields. Those looking for 1-2% extra yields on top of a fixed annuity and who have some flexibility to accept lower yields.

We did a study a few years ago when we compared guaranteed income from different types of annuities that provide guaranteed income. One of the things we found was very often, an FIA, especially when there’s some deferral period, was providing more guaranteed income even than a deferred income annuity, which is purpose-built for that. In addition, the deferred income annuity doesn’t have any liquidity.

Key Takeaways

- An FIA is a fixed annuity that has the possibility of a little more upside. The performance of an FIA is fixed income-like with the potential of greater yield depending on market performance.

- Proprietary indices can provide valuable performance characteristics and renewal rate stability.

- Risk tolerance and investment goals will play a role in the selection of a crediting strategy.

- Outlook about future index and market performance will play a role in the selection of a crediting strategy.

- The income guarantee can be valuable and comes at the cost of yield.