First, a little background on health savings accounts. You can only contribute to one if you have high deductible health insurance, which for many employers, it is either the only option or one of a couple of options that they offer. There are over 30 million health savings accounts currently in the US, and the number of accounts has been growing by approximately 10 percent per year over the last few years.

Typically, people put in approximately enough to cover their qualified medical expenses for the year. Over two-thirds of contributions are withdrawn in the same year. But unlike a flexible spending account for health expenditures where you have to use or lose it, a health savings account is yours as long as you are alive, like a quasi-retirement account. You can invest it.

As of now, there are $90 billion in health savings accounts. This is about $70 billion higher than about seven or eight years ago. Only about one-third of the $90 billion is invested, so $60 billion is sitting in cash. Of the $30 billion invested, about $20 billion is in bonds, and only about $10 billion is in stocks. The opportunity being missed is putting money in these health savings accounts to the extent you do not withdraw it in the same year, investing it for the long term if you do not need the money for a good while.

I have had a health savings account since 2015. In other words, I have had high deductible health insurance through my employer every year since 2015. I put the maximum into my health savings account every year, and it has grown, and I invest it in pretty much the US stock market, just an index fund. I do not pay any attention to it. I looked at it recently. I have $60,000 in there, and I have saved since I started my health savings account at the beginning of 2015. I have saved $35,000 worth of qualified medical expense receipts. So, in other words, any time I want to go forward, I can take out up to $35,000 tax-free.

Why am I waiting? When I am retired, and let’s say I get to the top of a tax bracket, and I do not want to jump to a much higher tax bracket, that will be an excellent time for me to take money out of my health savings account tax-free and just put some of those receipts that I have accumulated into that year’s tax folder. A significant advantage of a health savings account is its ability to be a quasi-retirement account.

What are the amounts you can put into one of these health savings accounts if you have high deductible health insurance? In 2022, the contribution limit for someone with self-only health insurance is $3,650. This is for employer and employee contributions combined. So, in other words, if the employer puts $1,000 into the HSA, the employee can only put in $2,650. If the coverage is for more than self-only, the maximum in 2022 is $7,300. If the employer puts in $2,000, the employee can put in the maximum of $5,300. The 2021 maximum contributions are $3,600 and $7,200.

Is a Health Savings Account (HSA) Better Than an Employer Match on a 401(k)?

Here we will start answering the question – is a health savings account better than an employer match on a 401(k)? Specifically, I will focus on a 50 percent employer match because that is a typical 401(k) employer match percentage. So, the employee puts $100 in, and the employer puts in another $50. That is your 50 percent match. Here is the answer: Is the employee’s combined tax rate over 33 1/3 percent? If it is, and the employer’s 401(k) match is 50 percent or less, then the health savings account makes the employee wealthier than the employee match on the 401(k).

The Federal tax rate brackets start at 10 percent, then quickly go up to 12 percent, and they are there for a while, then they go to 22 percent, and they are there for a pretty good while, then they go to 24 percent. The tax rate brackets are there for quite a while, and then they go to 32, 35, and ultimately 37 percent. Those are the seven Federal income tax rate brackets under current law. And these rates have been in effect since 2018; they are scheduled to stay in effect through at least 2025.

Assume an individual is in the 22 percent Federal tax rate bracket to give you some idea of where that puts them as far as their income goes. For someone single, if their taxable income is over $40,000, which means their total income is over about $52,000-$53,000, they are in the 22 percent bracket if their total income does not go over about $100,000. Their taxable income does not go over about $86,000.

You might describe someone in the 22 percent bracket as moderate income. Assume that they are a resident of a state that also has an income tax and assume the rate there is six percent. Do not forget that this moderate-income individual has to pay 7.65 percent FICA (Federal Insurance Contribution Act) taxes on their salary, which is the 6.2 percent Social Security tax plus the 1.45 percent Medicare tax.

Add all these up – 22 plus 6 plus 7.65, and you get 35.65 percent as the combined tax rate for the moderate-income individual. That is over 33 1/3 percent. The health savings account will make the employee wealthier than a 50 percent 401(k) match. How do I know that? Take the tax savings of 35.65 percent and divide it by the after-tax contribution to the HSA, which is 64.35 percent of the total contribution. That is a 55.4 percent immediate return. That beats an immediate 50 percent return on an employer’s 401(k) match.

Again, I assume the employer 401(k) match is 50 percent. If the employer 401(k) match were 75 percent or 100 percent, then the 401(k) match would make the employee wealthier. Even if the employer 401(k) match is 50 percent or less, the health savings account contribution makes the employee wealthier.

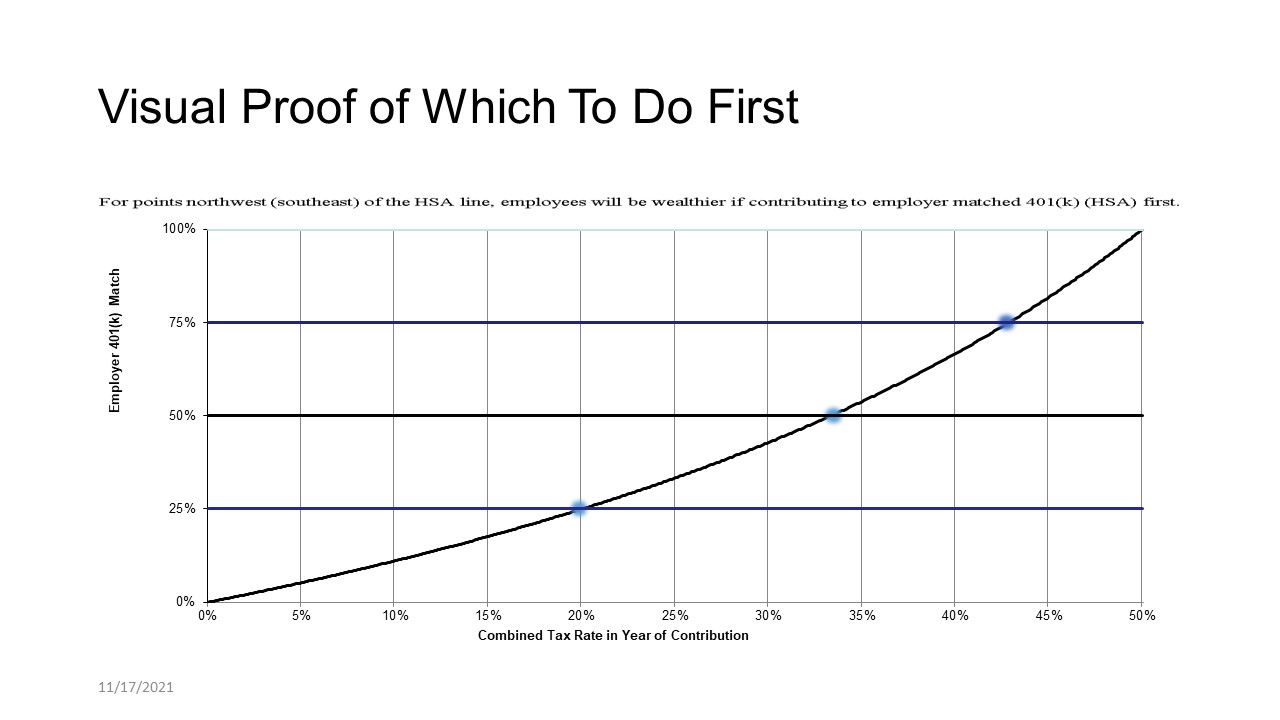

This graph was in the Wall Street Journal about five years ago. The curved line is the breakeven point. The vertical on the left-hand side is the employer 401(k) match. At the bottom, the horizontal line is the combined tax rate. You can see the second blue shaded bullet point right at the 50 percent 401(k) match line with the 33 1/3 percent combined tax rate. If the tax rate is anything above that you are in the southeast quadrant, you are underneath the curved line. That is a situation where the HSA contribution beats the 401(k) match. In contrast, the 401(k) match beats the health savings account if you are on the northwest portion.

Intuitively, you might question how a 401(k) match could not beat a health savings account contribution? The 401(k) match is extra money the employer is giving you. How can that not win? Think about any retirement account, whether a Roth retirement account or a tax-deferred retirement account like a 401(k). With the Roth, you do not get any tax savings at contribution. That is the downside to a Roth. With the 401(k) account, you must pay tax upon distribution.

In contrast with the health savings account, you get tax savings at contribution, and the distributions are tax-free if they are for qualified medical expenses. Now, qualified medical expenses for health savings accounts include your Medicare Part B and Part D premiums. Suppose you have long-term care insurance up to an amount limited by the tax law based on your age. Also, prescriptions and over-the-counter medicines. Suppose you go to the grocery store or pharmacy and buy allergy medicine over the counter. In that case, this is a qualified medical expense for purposes of HSA tax distributions, whether you pay for it with your HSA card or you reimburse yourself later for its payment. There are many more expenses than people think that qualify to be reimbursed tax-free through an HSA.

The HSA has three tax benefits: tax savings or contribution, tax-free while it is invested, and tax-free if withdrawn for qualified medical expenses. In contrast, Roth and traditional retirement accounts only have two tax benefits.

While the money is in the account, for both HSA and Roth accounts, you do not pay any tax on the dividends or interest or capital gain distributions, and with the Roth when you take the money out as a distribution. If the funds have been there long enough and meet the five-year rules, the distribution is tax-free if you are age 59 1/2 or older.

When you contribute to a 401(k), you save Federal and state income tax, but you do not save FICA taxes when you contribute to your 401(k). This is the intuition behind the triple tax benefit of contributing to an HSA because it also includes FICA tax savings versus only double tax savings if you contribute to a Roth or tax-deferred retirement account.

The Order to Invest and Pay Down Debts to Maximize Your Wealth

Contributing to the HSA and contributing the maximum to get the employer 401(k) match are steps 1A and 1B. The steps can be reversed; do not do the health savings account first and get the maximum 401(k) match first. Why? Because they both have such an incredibly good immediate return on them. Max out your health savings account if you have high deductible health insurance and get the maximum 401(k) match from your employer – steps 1A and 1B. It is not so much one beating the other; it is just doing both. Everybody needs to do both every year if possible. Why? Because you are on your way to maximizing your wealth by doing these two steps as step 1A and step 1B.

1A. Contribute the maximum to your HSA if you have high deductible health insurance. I cannot emphasize that enough.

1B. Put in just enough to the 401(k) to get the full match and then stop. Do not max out the $19,500 2021 maximum Federal law allowable contributions to your 401(k). What if the employer match is higher – 75 percent or 100 percent? Most of the time, a 100 percent match or even a 75 percent match by the employer of the 401(k) will beat the HSA. If that’s the case, get the 401(k) match first and then do the HSA maximum second.

- Pay off high-interest rate debts. Credit cards with the 20 percent or 24.99, or 29.99 percent APR. Do I not want to do that first? No. Are you saying get a 50 percent 401(k) match before paying off my high-interest rate credit cards? Yes. I thought the most important thing was to get rid of my high-interest credit card debt? No, it is the third most important thing. Why? What is the return on it? Let’s call it a 24 percent interest rate. That is a guaranteed 24 percent rate of return. That is not as good as a 50 percent 401(k) match. That is not as good as a 54-55 percent return in the example we did earlier on the HSA contribution. That is why I do this third.

- This is the only time I stray from the tax-efficient order. Contribute to a Roth IRA. You must have income that is low enough to do that. I am talking about your adjusted gross income, which is your total income minus any above-the-line deductions. Your total income cannot be too high for you to be allowed to contribute to a Roth IRA. That is why many people wait until the end of the year, see what their adjusted gross income (AGI) is for the year, make sure it is low enough that they can contribute to a Roth IRA. For 2022 your AGI has to be below $144,000 if you are single, and if you are married filing joint, your AGI has to be below $208,000 to contribute the maximum to the Roth IRA.

The maximum you can put in in 2022 is $6,000. Now, you can put that in up until April 15, 2023. That is the latest you can put it in, and you just check a box saying I want it to be a 2022 contribution. Even though I contributed in the first three and a half months in 2023, I want that to be a 2022 contribution.

If you are age 50 or older on December 31, 2022, you can put in an extra $1,000 or $7,000 to your Roth IRA if your income is not too high.

Why did I move Roth IRA up to fourth? You can use it as an emergency account. We know the importance of having an emergency account. What are those rules of thumb you always hear? You should have three- to six months of expenses in an emergency account. I tell you to have zero in an emergency account and instead have a Roth IRA. This is going to be your emergency account.

Contributions to a Roth IRA can be withdrawn tax-free at any time, not after you are 59 1/2. Any time. However, you cannot withdraw the earnings or the appreciation in value without penalty.

- If you have children or grandchildren you want to help put through higher education, contribute to a 529 account if it provides State tax savings. Notice that if it does not provide State tax savings, this is no longer in fifth place. Why is this fifth? Why is this better than unmatched contributions to retirement accounts (sixth in the rank order)? Basically, from a tax perspective, a 529 account is equivalent to a Roth, and it is tax-free.

You do not save any Federal income tax when you put money in. You do not pay any Federal, State income tax when you take it out for the beneficiary’s qualified higher education expenses. However, if you get State income tax savings, you do not get that when you contribute to a Roth. They changed the law within the last couple of years. You can withdraw from the 529 up to $10,000 maximum per year for the beneficiary for K-12. If they go to an expensive private school that costs $25,000 a year, you can only withdraw up to $10,000 tax-free per year.

The other rule added within the last couple of years is if you still have some money in that account after the beneficiary completes their higher education, you can take a $10,000 total out and pay down the beneficiary’s student loans. Of course, you do not want to over save in a 529. Assuming you will use what you put into the 529 for the beneficiary’s qualified education expenses, it beats the sixth step, contributing to unmatched retirement accounts.

Does contributing to a 529 account not beat a Roth IRA? Yes, it does beat a Roth IRA if you get State income tax savings, but I put the Roth IRA fourth because it can be an emergency account, and that benefit is very valuable. If I stuck to my tax-efficient order, contributing to a 529 if you get state tax savings would be fourth, and contributing to a Roth IRA would be after that. But again, I am trying to open your eyes to Roth IRAs are excellent emergency accounts; contribute to them.

- Unmatched contributions to retirement accounts. Which ones? If the tax rate you put it in is the same as the tax rate you expect when you take it out, and years in the future, then it does not matter whether you contribute to a traditional or a Roth. In contrast, if your tax rate is lower today and you expect it to be and years in the future, invest in a Roth. Many employers offer Roth 401(k) as an option in their 401(k) plan but not all employers yet. On the other hand, if your tax rate now is greater than the tax rate you expect in years in the future when you are taking money out of the retirement accounts, invest in a traditional tax-deferred retirement account, like a 401(k).

If the best you can figure is that your tax rate should be about the same now as later, here are some other things to think about. When you contribute to a 401(k), you know the amount of tax savings you get. That is valuable because, in contrast, when you contribute to a Roth, it is uncertain until you take the money out in the future what the value will be. You know the whole thing is tax-free if it is in there long enough, but is your tax rate low or high or in the middle in the future when you take the money out of the Roth? There is uncertainty there.

On the other hand, so many clients are so loaded up with tax-deferred retirement account money and have no or little money in Roth’s, it might not be a bad idea to contribute to a Roth.

Lastly, the after-tax dollars contributed to a Roth are greater than after-tax dollars contributed to a tax-deferred retirement account. You can put in $20,500 if you are not age 50 or older in your 401(k) or your Roth 401(k) for 2022. You get tax savings immediately when you put money into the traditional 401(k); however, you get no tax savings when you put it in the Roth. So, effectively, you can contribute a lot larger amount of after-tax dollars to a Roth.

If you have a client who can max out their contributions to their 401(k) and their tax rate now is similar to what they expect ten years in the future when they are taking money out, that would be a good idea to put money into the Roth 401(k) if the employer offers one. A more considerable amount of after-tax dollars can be contributed to the Roth 401(k) compared to the after-tax dollars going into your traditional 401(k). Again, the tax savings effectively go into the account for a traditional 401(k).

- Pay off moderate interest rate debts. What is moderate? It depends on the client, or it depends on you, and it depends on how much risk you are willing to take.

- Investing through taxable accounts. Why is this eighth on the list? Of course, the uncertainty of the return if you invest in stocks compared to a moderate interest rate debt has a certain return, a guaranteed return equal to the after-tax interest rate. Why do I say after-tax interest rate instead of interest rate? If the moderate rate debt is something like student loans and you get to deduct it, the after-tax interest rate is less than the before-tax interest rate. On the other hand, if the loan is a car loan for five percent, you cannot deduct any interest, so the after-tax interest rate is the same as the before-tax interest rate.

Should you pay off that five percent auto loan before investing through taxable accounts? This is up to the client. Why? Maybe they would be better off if they invested in stocks or a balanced portfolio, or maybe not. You never know when you invest because of the uncertainty with the returns on the equities. If the client is more willing to take risks, you will not pay off that five percent loan. You would say that is a low-interest-rate debt, which is not even on this list to maximize wealth. I have a 0.9 percent car loan, and I will not pay that off early. I can do better investing.

Why is investing through taxable accounts last? Because sooner or later, you have to pay tax on those accounts. The after-tax return is not nearly as good as it is on health savings accounts, Roth retirement accounts, and tax-deferred retirement accounts.

Why Follow This Rank Ordering to Building Wealth?

Simple. It maximizes your wealth. Further, different people run out of available cash at different points in their rank-ordering, so you need some rank order to tell you what will maximize your wealth. The more you do not spend, the more you can pay down debts and invest, and the wealthier you will be.

You must have an excellent nontax reason for not following this rank order to build wealth. If you follow it, it will maximize your wealth, given however much of your normal monthly paycheck you do not spend.