By Jodi DiCenzo, CFA, CPA, Behavioral Finance Expert

There’s a changing face of retirement in America. Unfortunately, what we’re finding is that Americans are not doing a great job of preparing for their retirement, and we’ll go through some descriptive statistics that really bring that point home. From there, I plan to convince you that the only way to meaningful change is to help people save more. We cannot help them invest their way to a comfortable retirement. Also, I plan to convince you that behaviorally-based plan management is unarguably the most effective and economic options for helping employees save more.

We’ll go through some of the heuristics and biases that affect our decision-making. They’re not great. It’s not nice to learn that our decision-making skills aren’t optimal. But the bright side is that it’s those very things that enable behavioral economics to work in terms of its application to helping people save more. I’ll go through some illustrations of the application of what we’ve learned in behavioral economics to help people accumulate more.

We’ll touch on some other behavioral considerations before showing some of the applications of behavioral economics in the Draw-down Phase. We’re much earlier in the development there than we are in the Accumulation Phase. And then finally, we’ll look in the mirror and I say that, assuming that some of you, at least if you’re not responsible for choice architecture within the retirement plan, you’re probably at least influencing it. And we’ll take a look at some of the decisions and how folks, who are in these positions, are doing.

Retirement Un-readiness

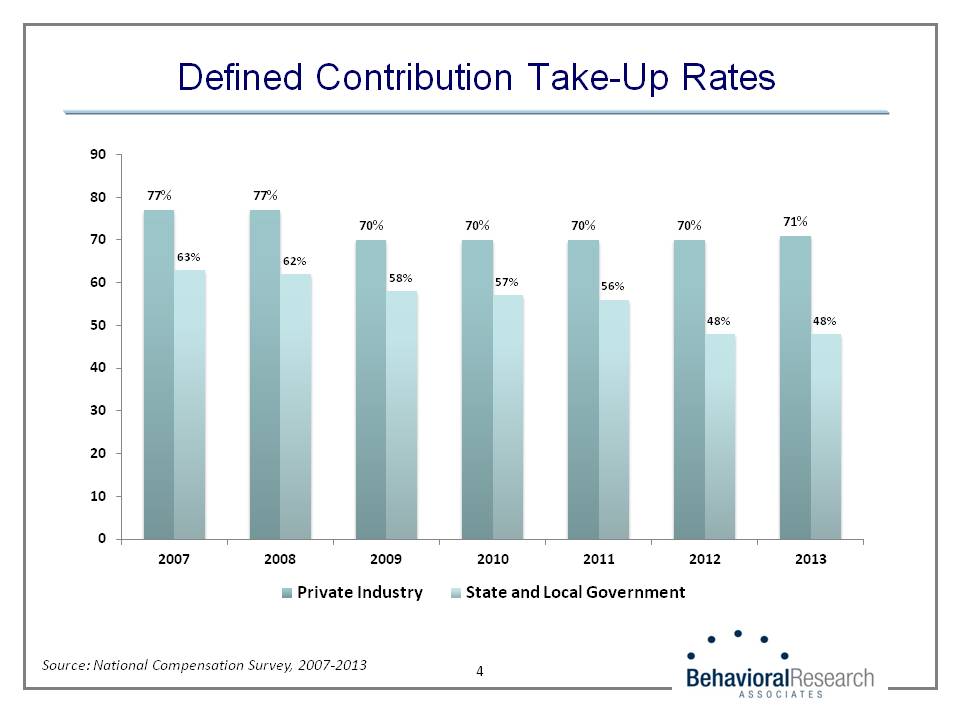

As you can see in the graph below, private industry participation rates are hovering around 70 percent when employees are offered a DC Retirement Plan. It doesn’t have anything to do with coverage, which is also a significant problem, and take-up rates in public plans, state and local plans, are just under 50 percent.

Savings rates, and this is for both public and private plans, have recently dropped, probably as a result of the economic downturn. They were around 7 ½ percent. In 2012, EBRI estimates were just under 7 percent. As you probably know, financial experts say that most people need to be saving between 10 and 15 percent, so these rates are woefully low.

Another problem, another area of sub-optimal decision making, is in the area of leakage, and this refers to the drain on retirement assets after they’ve been accumulated. It includes cash-outs at job change, in-service withdrawals, as well as loans. Between 17 and 19 percent of participants cash out at job change, and these tend to be younger participants with lower incomes and lower account balances. Around 7 percent of participants take in-service withdrawals, which includes about 2 percent, who are taking hardship withdrawals.

When loans are offered in plans, they’re taken by about 20 percent of participants. The drain on retirement assets of loans is pretty negligible, and is thought to reduce retirement income by about 0.5 percent. Cash-outs, on the other hand, reduce median replacement rates by over 25 percent in the lowest income quartile. In-service withdrawals reduce retirement income by about 10 percent in the same income quartile. All of these behaviors lead to retirement un-readiness.

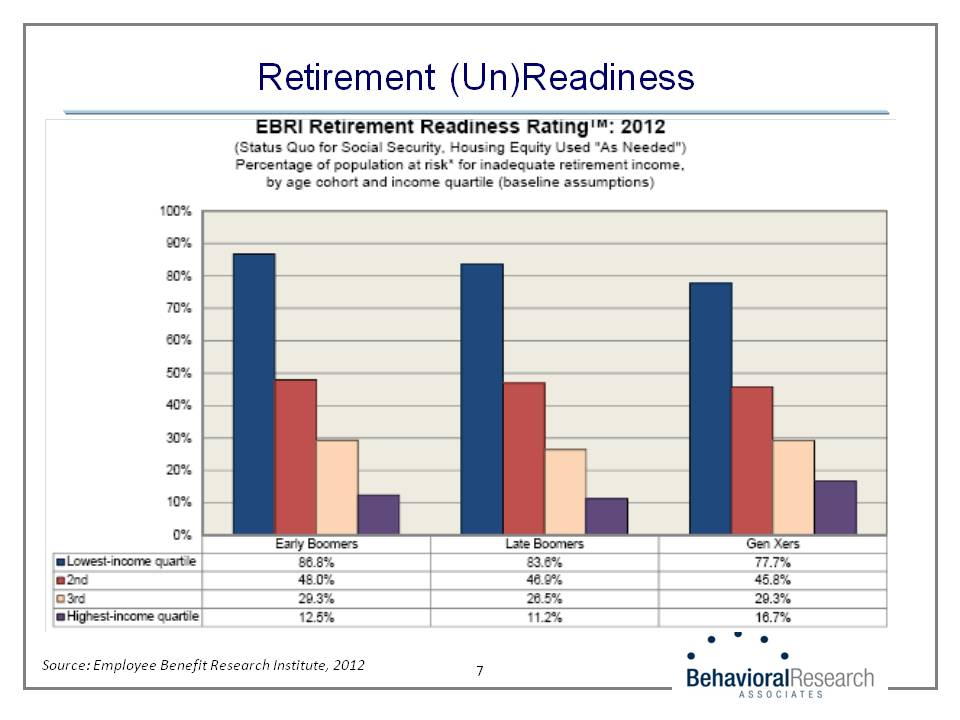

In the graph below, about 66 percent of households, aged 65 years or older in the bottom income quartile, faced income shortfalls. If you look and project it forward for boomers and Gen Xers on average somewhere between 43 and 44 percent are projected to have inadequate retirement income. However, as this chart shows, if you look at the lowest income quartile for early boomers, nearly 87 percent are at risk for having adequate retirement income.

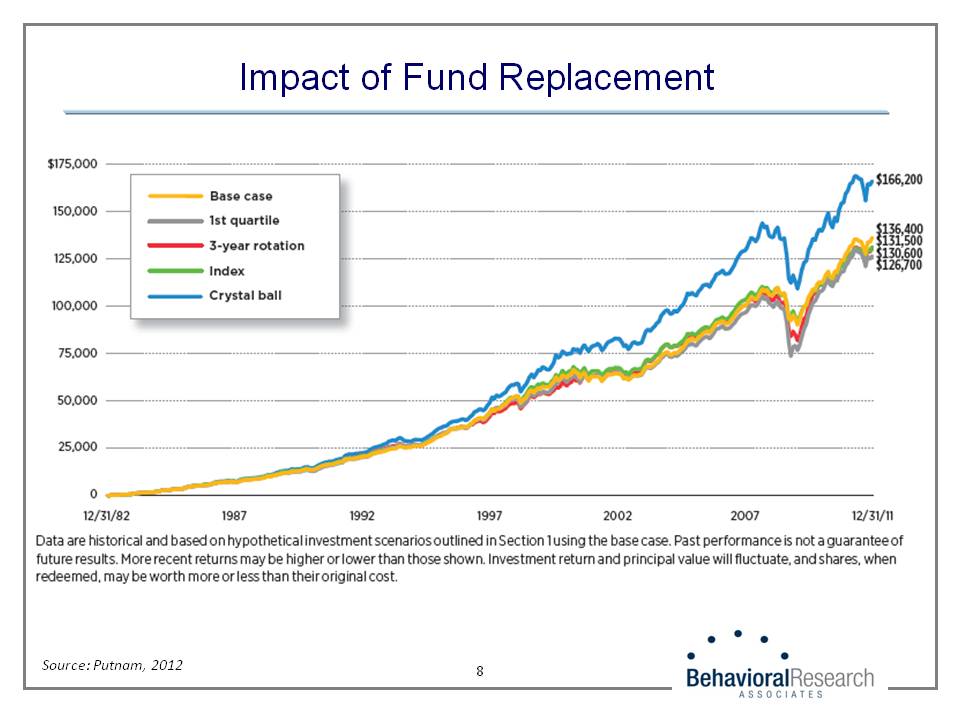

So what are we going to do about it? Well, I hope that you leave today thinking that, actually knowing that one thing that we’re not going to do about it, as I’ve said before, is to help people invest their way to a comfortable retirement without increased savings. I love this graph from Putnam.

I typically do not use vendor materials, but this one is fabulous. What it shows is the impact of fund replacement on the projected retirement wealth at age 65. So the assumptions here are that we have a 28-year old in 1982 making $25,000 a year, receiving 3 percent annual increases, participates in the 401k plan that has a 50 percent match with the first 6 percent of compensation.

He’s conservatively invested among six asset classes. The base case assumes bottom quartile funds. The individual defers 3 percent. That base case, at retirement in 2011, would be projected to have $136,400. I think what’s interesting to note is that even if he – we’ll call him a he – had invested in first quartile, top quartile funds at that point, he would have only had $126,700. If he had had a crystal ball and every three years, invested in the funds that were the best performing for that three-year period, yes, he would have had about $30,000 more.

But look at the impact of saving just 1 percent more. If that person had saved 4 percent instead of 3 percent, he would have had $20,000 more than he would have if he had picked the best funds, using the crystal ball. So this is one of the most important things that you can take away from this presentation today. We absolutely have to help people save more.

The next slide is from research that we did on target date funds to assess participant perceptions, misperceptions is more like it, of target date funds.

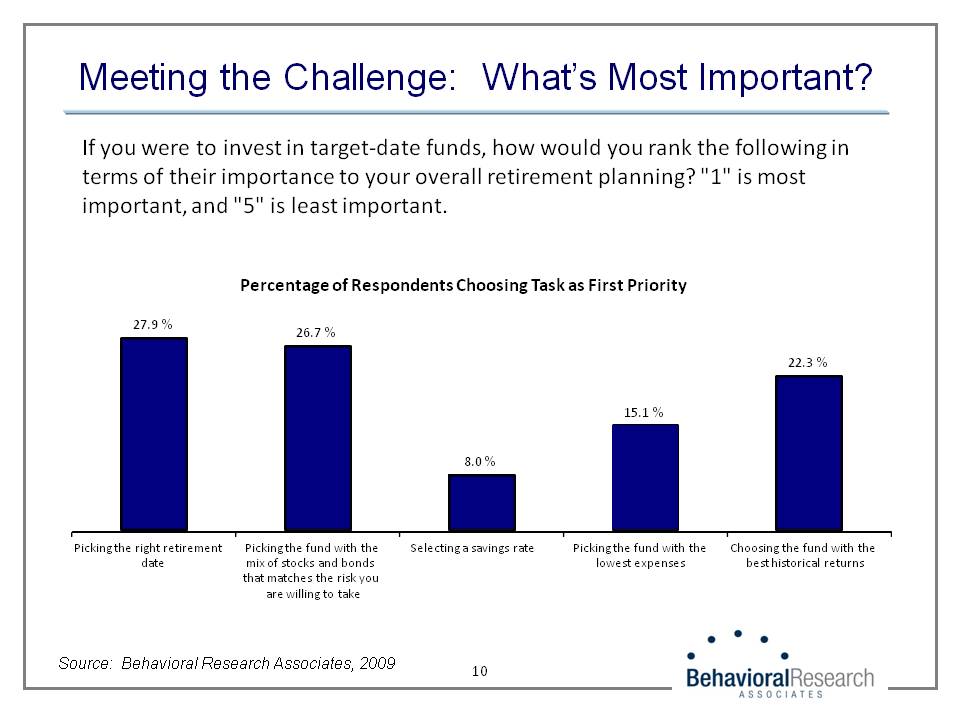

We asked them to rank each of the five items that you see at the bottom of the graph, according to their overall importance in their retirement planning success. Only 8 percent of the participants thought that “Selecting Savings Rate” was the most important task. What’s even more concerning to me is that I showed this slide at a break-out session of a Plan Sponsor Conference, where there were about 35 plan sponsors in the room. I went through each of these items and I asked the plan sponsors to raise their hand if they thought that was the most important aspect of retirement planning success. Unfortunately, only three plan sponsors in a room of 35 raised their hand when I got to “Selecting Savings Rate.” Recognizing the importance of saving in the whole scheme of things is really important.

Behavioral Insights to the Retirement Process

So let’s now get into behavioral insights and what we can learn from them and how they can be applied to the retirement plan process.

In short, we have irrational tendencies that undermine our ability to make fully rational decisions. These include loss aversion, status quo bias, the endowment effect, present base biases and self-control, framing effects, choice overload, and money illusion.

- Loss aversion. The term was really coined by Tversky and Kahneman, also Nobel Prize winners, and they discovered that the pleasure of a gain is about half that of the pain of a loss. Said a different way, losses hurt about 2 to 2 ½ times more than a gain pleases.

- Self control. There’s a problem of self-control. It, at least, contributes to it, which as Shefrin and Thaler point out in their 1991 article, called the Economic Theory of Self-Control; this requires a two-self model. We tend to have a farsighted planner self and a myopic doer self. The farsighted planner self is much more angelic than our shortsighted doer self. This creates conflicts. We want to save for retirement, but somehow, our short-term consumption needs seem to weigh heavy and we don’t get around to it.

- Framing effects. We’re also subject to framing effects and the way that an issue or a matter is framed really influences our decisions. So when a hamburger is described as 75 percent lean, more people prefer it, than when it’s described as 25 percent fat. It should make absolutely no difference; they are the same thing. Similarly, when medical procedures are described in terms of their survival rate instead of their rationally equivalent mortality rate, more people decide to move forward to have them.

- Choice overload. We tend to become overwhelmed by too many choices, and can become paralyzed by them. But yet, we like a lot of choices. As these researchers found, when there were lots of jelly jars available, more people visited the stand than when there were only six. But the percentage actually buying them was 10 times higher when the choice set was smaller.

- Money illusion. We have a tendency to think in terms of nominal dollars rather than real dollars, so $100,000 retirement plan account sounds like a lot of money, and we don’t think really intuitively that wow, that, depending on our age and inflation, might really be more like $30,000 in today’s dollars

The Effectiveness of Nudging

So let’s look at the application of some of these behavioral insights.

There are a number of nudges that we can offer employees to help them. Traditional enrollment rates, we showed earlier, are about 70 percent when people are offered a plan. Researchers have shown that by simplifying the retirement choice, so offering them a pre-selected contribution rate and investment choice, we can increase participation rates by 10 to 20 percentage points in the plans that they studied. So what have we done here? We’ve reduced choice overload.

Required active decisions overcome inertia and self-control problems by forcing people to make a decision. So we don’t allow the shortsighted doer self to never get around to taking action. We force them to do what their farsighted planning self would do. We also are reducing the status quo bias by forcing people to do something even if it is to stick with the status quo. They have to decide to do so actively rather than passively. Automatic enrollment is really a reframing of the enrollment decision. It’s reducing the choice set because people have a preselected contribution rate and investment, and unlike the others, it reduces self-control problems and the status quo bias.

The downside is that participants tend to stick with the default savings rate. But automatic increase programs offer a way to overcome that.

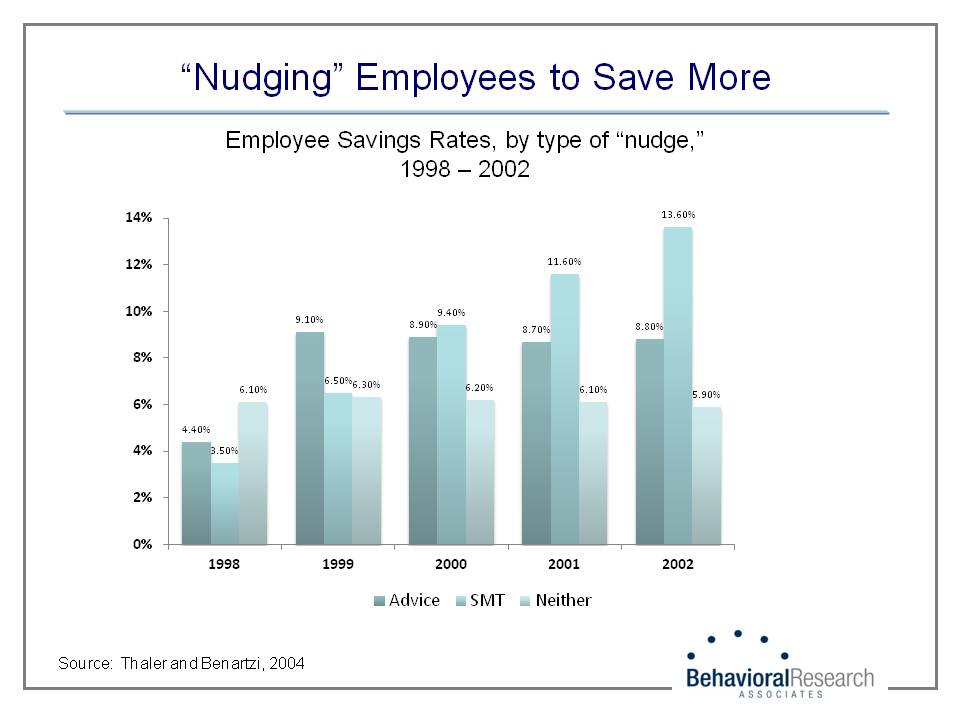

In the above graph, individualized advice is represented by the first set of columns, and an Automatic Increase Program is denoted here by “SMT.” The researchers called the program, Smart, for S, M and T (Save More Tomorrow).

So as you can see here, participants who enrolled in the Smart Program, which was a pre-commitment device to automatically have their savings rates increased every time they received a raise, their savings rates, over this time period, increased from 3 ½ percent to 13.6 percent, a pretty phenomenal increase over this time period. Well, automatic increase programs, when they’re structured the way that the researchers envisioned them, take advantage of loss aversion because people who sign up experience no loss because the actual deduction will take place in the future and only when participants receive a pay raise.

Automatic increase programs also take advantage of money illusion because people are getting a raise even when the rate of inflation outpaces their raise. So it could be people get a 2 percent raise and they’re happy even when inflation, over that time period, has been 3 percent. It’s also a reframing if it’s adopted automatically, so that participants don’t really need to do anything to save more; it is automatically happening. Unfortunately, this is not often the way that it’s implemented.

Framing Retirement Assets

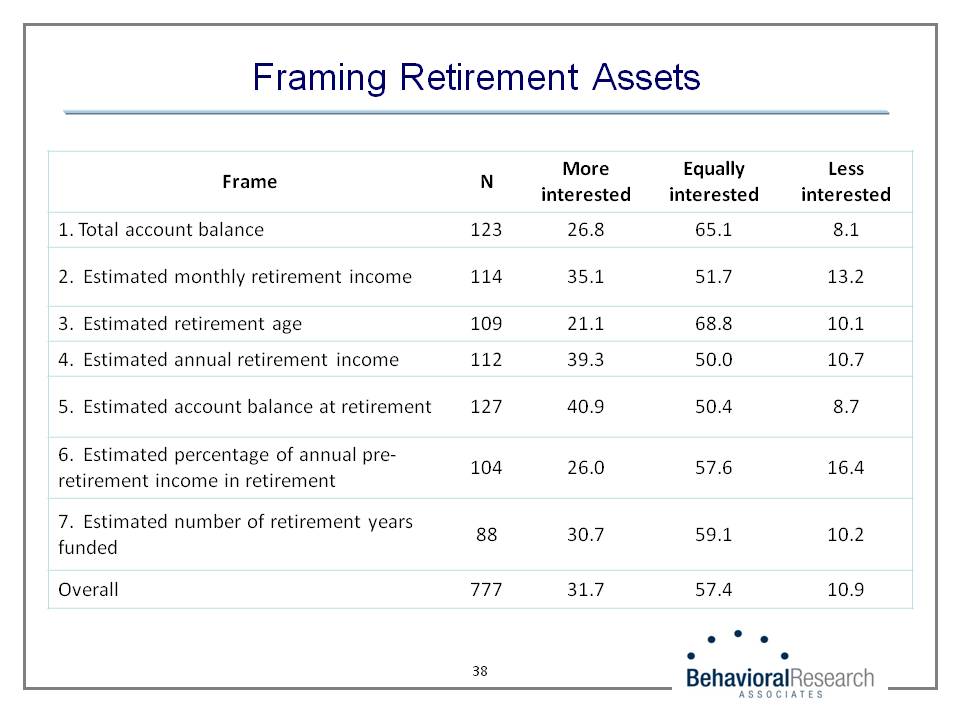

Next, I want to share with you a framing research project that we did with a large vendor a few years ago.

There’s a proposal now by the Department of Labor to include on participants’ statements “Projected Retirement Income.” And in this research, we tested seven different ways of framing retirement assets. The motivation for this research was that people thought, as I alluded to before, $100,000 was a lot of money, and so we wanted to show them how that amount would be reframed based upon different assumptions.

So this is a sample of the stimuli we showed them, in addition to their total account balance:

- Estimated monthly retirement income

- Retirement age

- Annual retirement income

- Account balance at retirement

- Estimated number of retirement years that they would have funded

All of these frames – increased motivation to save, their interest in saving more, etc., increased the interest to save more with the exception of replacement ratios.

The most effective frame was Projected Account Balance. Almost 41 percent of people who saw that frame were more interested in saving more. The most effective frame, to get people to save more, to motivate people to save more, is Estimated Account Balance at Retirement. Other behavioral influences to be aware of, social norms, and there are a whole slew of them. I encourage you to take a look at Robert Cialdini’s work, The Psychology of Influence.

Other Behavioral Influencers

Research in the retirement plan domain has shown that people are impacted by the decisions of others. So we’ve often taken advantage of that by using retirement plan advocates in hopes that there are positive influences. Also, we’ve found that people are influenced by descriptive and injunctive norms. So telling people what similar others are doing can have an impact as well as telling people what experts are doing. People tend to anchor to numbers, when they’re unsure of what to do. So the match rate can be an anchor.

Simply offering a range of contribution choices will provide people with anchors. So instead of a minimum anchor of 1 percent, if your minimum contribution rate that you show them is 3 percent, I guarantee you that more people will save 3 percent versus 1. The craziest things can have an anchoring effect. Researchers have also shown that getting people to think about the future, so priming them to think about their retirement life, can impact them to save more, as well as a cute thing that’s recently been done is to use virtual reality to actually show people their aged selves.

Top Take-Aways

So the top six for plan sponsors:

- Plan sponsors and their consultants are choice architects and have extreme control over participant outcomes. Some people view automatic enrollment as being paternalistic. Well, you have the control no matter which way you slice the issue. It’s what do you want the outcome to be? How do you want to nudge employees?

- There’s no neutral plan design. And whatever your plan design is, participants will perceive it as implicit advice.

- Retirement security: The only way we can improve it is by helping people save more.

- We have irrational decision-making tendencies, and they’re impacting our decision-making.

- Education and employer matching contributions aren’t doing the job.

- But behaviorally based plan design can.

I’d like people to think, as they go about designing plans, as they exercise their role or responsibility as choice architects, to think about it in the same way as an architect would design a building. Think about traditional enrollment as designing a building with a staircase, and each thing that a participant has to do to enroll in the plan are steps to a building. Let’s say it’s this fabulous museum; I like museums. Steps, even the number of steps, will eliminate some from entering. Automatic enrollment is the museum’s elevator.