Let us go back even 1,015 hundred years more to the second millennium BC. We are now in ancient Mesopotamia, and gold and silver coins did not yet exist. If any of you read Cuneiform, you basically see a contract on a tablet. You may notice a buyer, a borrower, a lender, and what looks like some grain passing hands. If we go back then 2,700 years, there were, in effect, bond dealings, or simply, an “I owe you.” Since they did not have silver coins, they used cows or sheep to transact business, perhaps enslaved people, but most commonly, grain.

As the years went on, bonds developed into certificate form. Let us move forward to the 1100s in Venice. Venice is at war with other city-states on the Italian peninsula. Venice needed money to raise for waging war. It turned to its citizens; those were the first real modern bonds. They offered what was called a prestito at a fixed interest rate. The interest rate decreased from about 33 percent to 12 or 15% in those days. A prestito, by the way, was like today’s bonds, but they were infinite. There was no maturity date. So, if you held a prestito, you would earn 12-15% every year for as long as you held it, which would be the rest of your life, unless you sold it.

Bonds were eventually issued with actual coupons, and they were ripped off or cut out and turned to the borrower, who would then pay you back what was then called and still called the coupon rate. So, if you had a $1,000 bond earning five percent, you would get $50 a year for as long as you held the bond or until the bond’s maturity. It still is called a coupon.

In 1982, the US government decided that too many of these bonds, called bearer bonds, were allowing the holders to hide their interest collected from the taxman, so just about all bonds went electronic. So, now the US Treasury issues a statement indicating that the holder has holdings in US Treasury bonds. Currently, bonds are held by banks and brokerage houses, or you can get them directly through the Treasury. All you will have is an electronic statement, just as you do with stocks, which no longer issue certificates. The only exception I know of is the US Treasury, which still offers some savings bonds in certificate form, which you can buy with a tax refund of up to $5,000 a year.

Why Invest in Bonds?

Depending on your age, your grandparents or perhaps your great-grandparents may have been saved from destitution or from having to sell apples on the street during the Great Depression because of bonds. In 1929, the market lost about 12-13% on Black Monday, and the same thing happened the next day. Over the ensuing weeks, it lost another 25%; in the end, the Dow lost 90%. It would come back until the Japanese attacked Pearl Harbor in 1941, and we entered into a wartime economy.

It was a long, dragged-out, severe depression, but bondholders did rather well. Over that decade or so, bonds never lost value. US Treasuries earned about six percent a year, and remember: this was not a time of inflation; this was deflation. So, prices were going down, and six percent was a very handsome take for bondholders.

Why hold bonds? Because bonds pay cash. Every month, every three months, every six months, you will get, again, a coupon payment which is cold, hard cash. I cannot think of many other investments that promise you a steady stream of income.

Why hold bonds? Because even if we are not headed toward another depression, many people have a hard time with the daily ups and downs of the stock market. Bonds tend to smooth out a 60/40 portfolio. Bonds and stocks, stocks and bonds will be much less volatile than a portfolio of all stocks. Bonds have a zero correlation with the stock market. If the stock market goes down, sometimes the bond market will go down, but there is no reason for it to. It may go up when things get rough. The safest bonds, Treasuries, especially long-term Treasuries, do tend to go up. There are no better hedges than bonds.

Cash is the second-best hedge after bonds. The problem with cash, of course, is if you put money under your mattress, you are going to lose two, three, or four percent a year, whatever the inflation rate is. And even if you have your cash in a money market or savings account, you will still be lucky to keep up with inflation.

Gold is an excellent diversifier when it wants to be. Sometimes it moves in lockstep with the market; sometimes, it moves against the stock market. It is always very volatile, and of late, because gold has become very liquid with the coming of all kinds of gold ETFs, we are finding more correlation with gold than we have in the past. Gold has a long history of almost keeping up with inflation.

Then there are REITs, real estate investment trusts, and high dividend-paying stocks, which have limited correlation to bonds but are correlated to the stock market. They will tend to go down when the stock market goes down and up when it goes up. For that reason, they are not great hedges, and dividends are different from interest payments, and dividends are not guaranteed.

There have been index funds and mutual funds for years. Lately, there have been dozens and dozens of inverse ETFs introduced to the market, whereby if the S&P goes down by five percent on a particular day, your inverse ETF will go up five percent. A perfect negative correlation is a great hedge. These funds tend to be pretty pricey, and you are fighting a juggernaut. The stock market goes up over time. And for that reason, people have lost money on these inverse funds over the years.

Not all hedges are created equal. And if we look back over the last 50 years, stocks have returned to a healthy 10% a year. The three-year standard deviation of the S&P 500 is 21.1 percent, which is very volatile. Bonds have earned about half as much, with much, much less volatility. Gold has returned not half of what bonds have returned, and cash has just about kept even with inflation.

What Kind of Bonds Belong in Retirees’ Portfolios?

When I have been talking about bonds, I have been talking about investment-grade bonds. These bonds have minimal credit risk, and there is minimal risk or no risk that the issuer will go bankrupt.

There is no risk with Treasuries and minimal risk with companies like Microsoft and Apple. I suggest that retirees’ portfolios should be bond portfolios and all investment-grade. High-yield junk bonds over history tend to return about two and a half to three percent more a year than investment grade. But they can be very volatile and correlate to the stock market. When we go into a recession or a depression, companies fold. And those companies will no longer pay bond interest or the principal. So, high-yield junk bonds are risky. I am not saying there is never a point in owning them. But investment-grade bonds are part of a retiree’s portfolio that serves as ballast and as a hedge.

Once we decide we want a portfolio of investment-grade bonds, the next big decision is government versus corporate. Government bonds, or US Treasury bonds, were considered the safest because if the government can tax, presumably, they will never go bankrupt. And if it does, we are all in much trouble. Government bonds pay about a point and a half less than investment-grade corporate bonds over history.

Muni bonds can be a very good substitute for corporate bonds. Muni bonds belong in your clients’ portfolios in the stratospheric tax brackets. To estimate the taxable equivalent yield of a muni bond, you start with a straightforward formula. Take the muni bond yield and divide it by the reciprocal of your marginal tax rate. So, if a muni bond is paying five percent and you are in a 30% tax bracket, you divide the reciprocal of that or 70 into five percent. A muni bond paying five percent would have a tax equivalent yield of about seven percent.

The next big question is whether you want short-term, intermediate-term, or long-term bonds or a little of each. Short-term bonds tend to be much less volatile 90-95% of the time under normal conditions when the yield curve increases. When the yield curve increases, short-term bonds will be less volatile but pay less, and longer-term bonds will tend to yield more.

The Risks of Bonds

We talked earlier about credit risk. People first think of this when they think of risk in bonds or the risk that the borrower will go bankrupt. However, a borrower does not have to go bankrupt for you to lose money. There is also downgrade risk. When a bond goes from investment grade to junk or from triple A to double A or AA to A, you are taking on downgrade risk. I looked a couple of weeks ago at Bed Bath & Beyond bonds. At the time of this writing, their bonds yield 40%, and there is a good chance that you will not get your money back since they’ve been downgraded. The price of Bed Bath & Beyond bonds has significantly fallen.

Downgrade risk and credit risk are, again, what people think of most. But a more considerable risk in my mind, as we saw over the last year, is interest rate risk. The price of bonds moves inversely to interest rates. So, bond prices went down when interest rates went up as they did in 2022.

Reinvestment risk is the flip side of interest rate risk. With interest rate risk, you are afraid interest rates will go up, pushing your bond prices down. With reinvestment risk, you are afraid that interest rates will go down if you have too much in the way of short-term bonds. Remember, you are getting that fifth on a five percent, $1,000 bond. You are getting $50 a year for the 15-20 years you hold that bond. Reinvestment risk means you cannot reinvest that $50 at the same rate.

Bonds have just about kept even with inflation over the last 50 years. Aside from last year, it has been a good time for bonds. We went from the very high-interest rates of the 1980s when bonds were paying double digits 15, 16, or even 17% quality bonds down to the beginning of last year when Treasuries were paying about zero. So, even now, bonds just about kept up with inflation. There have been other times throughout history when bonds have not done a good job of keeping up with inflation.

Finally, there is FOMO or fear-of-missing-out risk. I have seen people come to me who really should have more conservative portfolios than they do, which is to save more bonds than stocks. But if the market is doing well, they see their neighbors, their friends, their hairdresser, and their plumber talking about how much they are making in the stock market. That can depress some people.

What Happened to Bonds in 2022?

Because of rising interest rates in 2022, the aggregate bond market lost 13.2%. When I talk about the aggregate bond market, that is the world of investment-grade taxable bonds, or two-thirds Treasuries and one-third corporate.

2022 was the worst year for bonds in history ever. Why? Let us go back to early 2020, in March- April. We had never heard of COVID before. And suddenly, we see an epidemic that turns into a pandemic. People are not going to restaurants, not going to bars, not going to stores. They may not be going to work. They may not have work to go to. We start spiraling into a recession, perhaps a depression. And the government responds to this the way, not only our government but most governments worldwide; certainly, all Western governments respond the way governments usually respond when they fear a coming recession or depression: they lowered interest rates. They lowered them and lowered them and lowered them to the point that Treasuries were paying about zero. German and Japanese sovereign bonds went below zero and were paying negative interest rates.

A year or two years go on. Most people get vaccinated and realize that if they catch COVID, they will probably not die; they will probably have flu-like symptoms. When I had COVID, it was not even that.

As the economy started kicking up again about a year ago, Russia invaded Ukraine. Suddenly, supply chains freeze up, especially oil. The rising price of oil, the closing of supply lines, people rushing back to fill their consumer needs that have yet to be filled, and suddenly we start seeing high inflation as high we have not seen since the 1980s. Governments respond the way they usually respond to inflation fears – they start raising interest rates. They raise interest rates and raise interest rates and raise interest rates. Until today, the 10-year Treasury is paying about four percent. Because we have an inverse yield curve now, shorter-term Treasuries are paying about five percent.

So, percentage-wise, that was a massive hike. We saw a perfect storm. Again, as interest rates go up, bond prices go down. The chances of us having another year like 2022, I will not say is impossible, but pretty close to it. Now if I can ballyhoo bonds once again as something that belongs in most retirees’ portfolios, if not all, keep in mind 2022’s 13.2% loss. Several times over history, the stock market has lost almost as much or as much in a single day. And last year, the S&P lost about 20%, and the NASDAQ about 33%. So, even in the worst year for bonds ever, bonds still served as a decent hedge, still served to smooth out volatility in seniors’ portfolios.

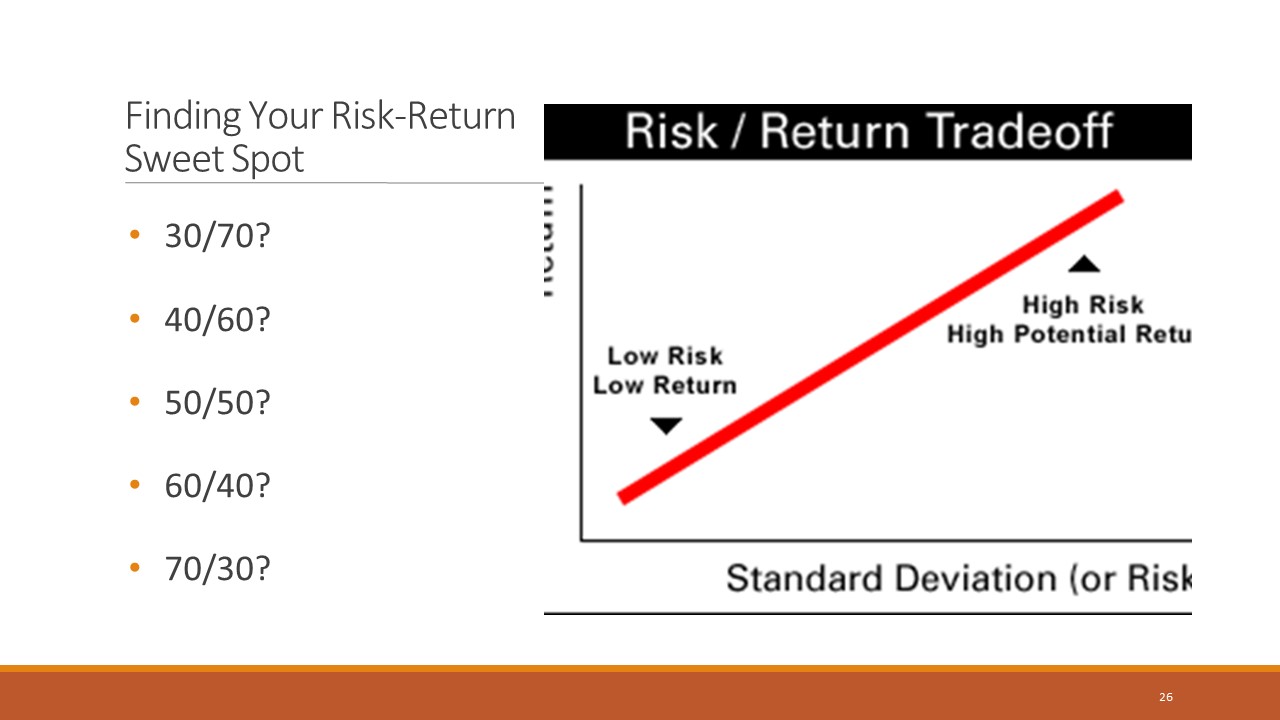

What percent of my retirement portfolio should be in bonds? There are all kinds of formulas. I am not going to discuss it in depth because other speakers talk about this in great depth and do a very good job of doing it. I will say that many, many studies look at safe withdrawal rates. The safety of portfolios suggests that most peoples and most retirees’ portfolios should be somewhere in the range below:

A very not risky 30% stock, 70% bonds would be a mild non-aggressive portfolio compared to a 70% stock, 30% bonds portfolio. Most retirees should be somewhere in the middle, somewhere between 40 to 60% stock and the rest in bonds.

How to Choose Bond Investments?

We’ve addressed the broad questions to ask before getting into bond investing. Now let us look at some of the particulars, nuts, and bolts.

You can invest in individual bonds, or you can invest in bond funds. I favor bond funds for several reasons. Bond funds have decreased in price remarkably over the last ten years, and trading individual bonds has not changed much. Bond trading and bond funds can be very economical, and bond funds also allow for easier diversification.

They also allow for automatic reinvestment, which individual bonds generally do not, reducing cash drag. If you are going to go with funds, I urge you to keep costs low. That is even more important with stocks than it is with bonds than it is with stocks because you are looking at a lower return. So, costs can eat up a much greater percentage of that return.

As we talked about earlier, do stick with investment grade. If you have a small portfolio, look at a broad core bond fund that invests in Treasuries and corporates with a larger portfolio. You may want munis in your taxable accounts and corporate bonds in your retirement accounts. Diversify. Diversify. Although funds do a great job diversifying within an asset class such as corporate bonds, you may want to have several kinds of bond funds, such as Treasuries, corporate, agency, and municipal.

Study after study shows that buy-and-hold investors do better than those who frequently trade because there are all kinds of trading costs when you trade that are often unseen.

How low can you go with bond funds? Fidelity, Vanguard, BlackRock, the bond funds, plain vanilla bond funds, where we are talking three, four basis points. For example, the PNY Mellon Corp bond fund has an expense ratio of zero.

Consider ESG bonds. ESG stands for environment, social, and governance, which used to be called corporate responsible or sustainable bonds. You should align your values with your investments, and ESG is just another tool that can be used to look for risks. You may not want to invest in corporations with lots to lose if there is continued coastal flooding. One study by New York University and Rockefeller Asset Management looked at 1,141 other studies, including other meta-studies. They found that the great majority of companies that score high on sustainability tend to be more profitable, and their investors tend to get greater returns.

Now, moving to individual bonds. If you are going to invest in individual bonds, and there is no reason you should not invest in Treasuries, if you want to, you can get a Treasury refund bond for almost nothing. But if you want to invest with Treasuries, especially directly through Treasurydirect.gov or through a brokerage house, I know Fidelity and Vanguard do not charge anything for Treasury trades. Go ahead and do so.

But where corporate bonds and munis are considered where you are going to pay for trades, and you need diversification, I suggest funds. But if you want to go with individual bonds, please make sure you use TRACE or urge anyone you know to use TRACE. TRACE is FINRA’s system of tracking bond buys and sells. TRACE has been around since 2002, yet many people still trade bonds without looking at TRACE. TRACE is now available through most large brokerage houses. You can see where a bond was last traded. If it is a frequently traded bond, maybe minutes ago, you will see the price that it was traded for or the price it was purchased for. You will know exactly how much the middlemen are taking.

Plan to hold bonds to maturity if you buy individual bonds. That way, you are only dealing with the expense of one trade, not two. And ladder wisely. Do not be a slave to the yield curve. Let me explain what I mean by that. Laddering, of course, is having short-term, intermediate, and long-term bonds. This is especially important if you invest in individual bonds for a retiree who needs cash. You want bonds coming due to provide that cash over however many years. Do not be a slave to the yield curve. Right now, we have a very unusual downward-sloping yield curve, maybe less than 10% of the time; we do not have an upward-sloping yield curve. So, it means that you can buy long-term bonds, which are more volatile and get less return than you earn on short-term bonds.

Why would anyone want to have long-term bonds? Again, remember reinvestment risk. So, right now, you can get about five percent on a one-year Treasury and four percent more or less on a 10-year Treasury. If you have all one-year Treasuries, what happens in a year if interest rates start tumbling again? What are you going to do with all the proceeds that you are going to be collecting in one year? You are not going to be able to reinvest them. Not even at four percent. Perhaps you will not even get one percent. So, that is why it makes sense, even in times like this with an inverted yield curve, to have some intermediate and long-term bonds.

What do you do once you have bonds in your portfolio? Many people like bonds because they are a steady stream of cash, which is true. In the old days, retirees with bonds in their portfolios lived on their bond interest. The problem is that bonds tend to just keep up with inflation, maybe do a little better. If you take the interest out of the bond side of the portfolio, the bond side will shrink, and you want to keep your portfolio in proper alignment. At the same time, buying low and selling high is always great. So, set your bonds to reinvest automatically, reduce cash drag, and rebalance every six months, every nine months, and every year. If stocks have had a wonderful six months, you sell stocks. If bonds have had a wonderful six months and stocks have shrunk, you sell bonds. That way, you are constantly buying low and selling high and can juice your returns over the long run. More importantly, though, you will keep your portfolio in proper alignment.

Very Common Bond Myths

I want to talk about a few very common bond myths.

First bond myth: You can buy a bond at a discount, or you can buy a bond at a premium. It sounds better to buy a bond at a discount, but it is not. If you buy a bond at a discount, such as a Bed Bath & Beyond bond, there is a reason you are getting it at a discount. You are getting a discount because it used to be a AAA bond, and now it is a BB bond, or you are getting at a discount because it is paying $50 a year.

Interest rates for bonds have gone up. Bonds issed at a 5 percent coupon now need to yield seven or eight percent. So, a bond paying $50 a year instead of $70 a year will sell at a discount.

But discount bonds and premium bonds will tend to have the same yield. Premium bonds are probably paying more, which is why they are premium bonds. They were issued at a time when interest rates were higher. Let me say that discount bonds can actually wind up smacking you more tax-wise because if you buy a bond at a discount, you buy a bond that is, say, $900, and then sell it at a $1,000 two years later, you are going to pay a capital gain. And that holds even if it is a muni bond.

Second bond myth: A bond paying X percent today will pocket you X percent over the bond’s life. As you will recall, I said bonds look very simple but can be very complex. A 20-year bond that you buy at five percent will not necessarily earn you 20% over those 20 years because there is a reinvestment factor. Your bond will pay $50 a year, and you need to reinvest that. You do not know if interest rates are going up or down. Even though bonds are a lot more predictable than stocks, they are not entirely predictable.

Third bond myth: Rising interest rates are good. Sometimes you will hear they are bad for bondholders. Certainly, right now they are because people’s bond portfolios have lost 13% over the last year, although they have made something of a comeback in the last two months. You are hearing that rising interest rates are bad for bondholders. Keep in mind that you are currently getting healthy interest on your bond portfolio. Those Treasuries you may be holding are paying four or five percent right now, whereas a little over a year ago, you would have been getting zero. Over the very long run, rising interest rates are probably good for bond investors.

Fourth bond myth: Certain bonds, such as Treasuries, are completely safe. Treasuries presumably are free of credit risk, but they are certainly not free from reinvestment risk or interest rate risk. As a matter of fact, long-term Treasuries tend to be particularly sensitive to interest rates. So, we can see big swings in the price of Treasuries. Even though they are sometimes called completely safe bonds, they are not.

Fifth bond myth: Bonds are a retiree’s only true friend. I love bonds, and I hope I have conveyed that to you. But bonds are not a retiree’s only true friend. If you have a portfolio of all bonds, you are going to have to spend very modestly in retirement because your portfolio is probably going to just keep even or maybe a little better with inflation. So, a retiree’s true friend is a diversified portfolio that holds bonds.

Sixth bond myth: My favorite myth is that I do not have to worry about interest rates because I will buy a five percent bond for 20 years. I know exactly what I am getting and can laugh off interest rate movements. Let those people with bond mutual funds sweat it out. I am going to sleep well. Let’s look at Big Joe, who buys himself an individual five percent bond, say a Treasury bond, with no credit risk. He is going to hold it for 20 years.

Little Joe buys a bond mutual fund, and his mutual fund will see many, many ups and downs over the coming years. Well, let us say interest rates go up. Little Joe will not be getting five percent; he will get six, seven, or eight percent on his bond portfolio. And Big Joe will be eating crow for 20 years, earning five percent, but he is not taking any interest rate risk. No, I am afraid there is no way to avoid interest rate risk.

Key Takeaways About Bonds for Retirees

I hope I have communicated that investment-grade bonds lend crucial stability to a retirees’ portfolio and, for that reason, belong in all retirees’ portfolios.

Let me say bonds are the most common form of fixed income right now. And at certain times, CDs pay as much or more than bonds. So, CDs can be a good substitute.

And in certain circumstances, a fixed annuity can also fill that role. But for most retirees’ portfolios, a good chunk of investment-grade bonds makes all the sense in the world.

I hope I have impressed you also that 2022 is considered a black swan event with a fat tail, and it was the perfect storm and will not happen again anytime soon. As I have shown you, even though bonds had the worst year in history, it still serves as a decent hedge for retirees.

Fixed-income portfolios should make up 50 to 60% of most retirement portfolios. Again, this is based on many studies that show that to have a portfolio that will keep up with inflation but not be too much at risk from the volatility of markets, you want something in this ballpark.

As we covered at the end, you want to sell high and buy low by rebalancing stocks and bonds. Do not just have the bond portfolio and take the cash out of it to pay for the bills will lead to an uneven, unbalanced portfolio.

And finally, especially because bonds do not return what stocks return, you want to keep your costs very low and trade at a minimum.