Sometimes life-changing health events sneak up slowly; other times, it’s sudden and shocking. Unfortunately, the far-reaching implications can be almost as unsettling as the actual event itself.

Planning helps take the short-term “shock” and the long-term burden of caring for family and friends who need care. Even though the pandemic was on the news ad-nausea, families were hard-pressed to develop a viable plan. The Generational Advisor is like an orchestra conductor coordinating the various players as the plan comes together.

The stark reality is that the ratio of older adults at risk of needing care to potential family caregivers — known as the CSR-caregiver support ratio— is declining dramatically from 7:1 caregiver to older adult ration today an expected 1:1 ratio in 2050.

Family caregivers provide an estimated $470 billion per year in unpaid care. While a critical component for individuals, we also see that states via education and a change in Medicare regulations are moving toward providing support and services to encourage people to “age-in-place.” However, there is a definite shortage of training healthcare personnel, so we can anticipate that it will fall to families to provide care.

Meanwhile, the size and nature of the “American” family are in flux with more singles choosing not to marry, others choosing not to have children, others divorcing, and others, remarrying which directly will affect the “pool” of available caregivers.

Family members may move due to marriage, employment, etc. Long-time friends who may have offered support may move away due to retirement or their family obligations shrinking the caregivers’ pool even further.

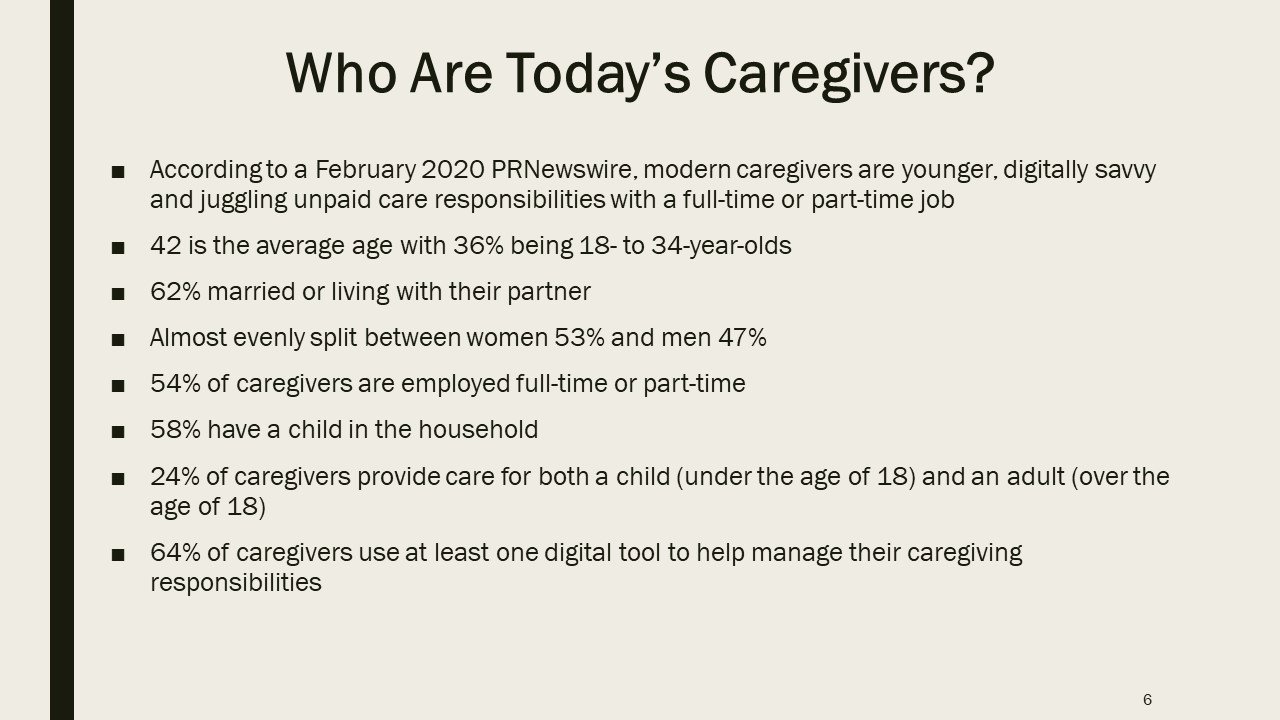

We saw that most care comes from adult children ages 45–64, which is a prime cohort for advisors to work with clients concerning insuring and investing for extended or long-term care.

For most of us, our clients and friends can be found embedded somewhere in this list. You might even see yourself in more than one statistic or expect to be there at some point.

Notice that 36% are younger (ages 18-34). Think about expanding your practice by adding a younger advisor focused on this expanding need.

Caregiving and employment are increasingly intertwined. Some of your clients are probably already doing some level of caregiving since already about half of the nation’s caregivers for older adults are employed. As noted above, working caregivers—especially those who care for people with dementia or with substantial personal care needs—are at risk of high economic costs: loss of income, the out-of-pocket cost for the care recipient, and lower lifetime earnings, savings, and retirement. Discovering and listening to this concern is a way to expand your relationship. Or, as a conversation starter, use this list and ask your client if he is or expects to be in one of these categories.

Setting the Stage for Our Case Study

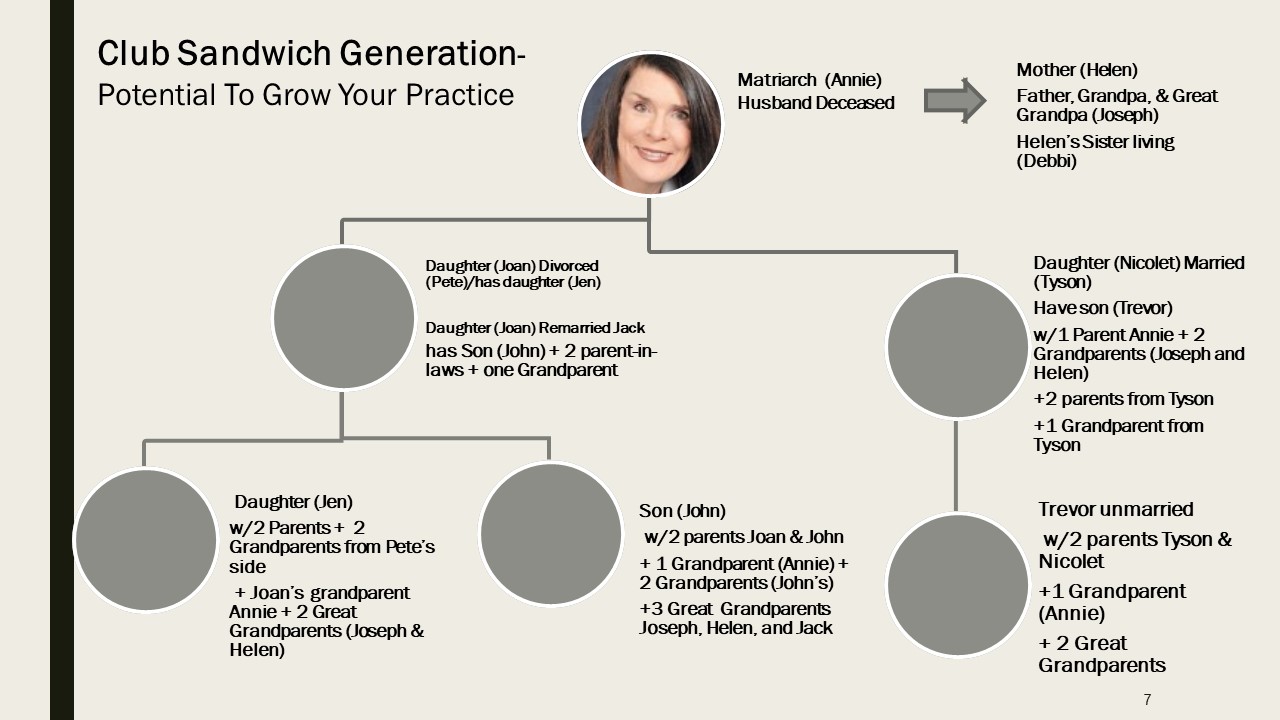

Here is a four-generation family: we will focus on Joseph and Helen, who are in their 70’s. Joseph contacts his advisor and wants to work out a plan so that he and his wife, Helen, can stay independent and age-in-place. Joseph contacts his daughter Annie and invites them all to meet.

The advisor quickly surmises that Annie is the “go-to” person for Joseph and is the family’s matriarch.

During the initial meeting, the advisor makes notes for the following categories:

- Current Health: Annie’s father, Joseph, says he is in excellent health, although Annie mentions that Joseph has a pacemaker and a family history of heart failure.

- Annie’s mother, Helen, on the other hand, has a family history of longevity with relatives having lived well into their 90’s. Helen is frail with little appetite, and Joseph mentions that she often appears less sure of her step. She takes B12 shots and had cataract surgery. Her sister, Susan, is three years older than Helen and resides in a CCRC (continuing care retirement community).

- Joseph and Helen are on Medicare with Medicare Supplemental policies, but Annie mentions that she or her daughter (Joan) must file the paperwork for any claims.

- When Joseph leaves the room for a moment, Annie mentions that Helen is very dependent on Joseph for financial, morale, and physical support, which Annie worries is starting to take a toll on Joseph.

- Housing: Joseph and Helen own their home and have a small mortgage. Joseph is no longer able to do chores that he previously managed, such as garden/lawn maintenance. For small home repairs, Joseph hires neighborhood teens and pays them hourly.

- Mobility: All the shopping chores fall on Joseph if it isn’t a far drive or Annie if it is too long a drive or things are too heavy for Joseph to manage.

- Financial: Joseph receives Social Security benefits; Helen receives spousal benefits. They also have a very modest income from savings/investments, so Social Security makes up the bulk of their income.

- Insurance: Joseph has a 100K Whole Life Insurance policy, which he wants to leave to his grandchildren. Neither has long term care insurance.

- Documentation: The couple has a will that they drew up 30 years ago and updated 15 years ago. Neither has health directives or a DNR (do not resuscitate order).

What are their options? How should this advisor go about planning for his client’s safety and security who wants to age at home?

Becoming a Generational Advisor

Long-term care plans rarely do not involve multiple generations and/or friends.

Aside from traditional families, like that of Joseph’s and Helen’s, there are blended families, same-sex marriage families, ethnically blended families, adopted families, out-of-state families. COVID-19 also showed the importance of friends as family and caregiving aids as family. Helen and Joseph depend on their family but also their friends and community (and vice versa). This is one reason they do not want to sell their home and want to live independently.

In this case, Joseph and Annie’s first thing to do is get a “Grab and Go” Bag ready for each Joseph and Helen. This is also the first opportunity the advisor can suggest that Annie do this for herself and maybe her children and grandchildren.

The “Grab and Go” packet should contain essentials such as a copy of their health insurance card, a copy of their license, contact numbers a family or friend who can call others or go to the hospital, the name and contact information for their doctors, specialists, and pharmacy along with a list of prescriptions, medications, and allergies.

Next, it is crucial to determine who will be participating in the “Core Team.” For our case study, having already determined that Annie is the alpha child/decisionmaker, the advisor explains that a Core Team member steps in if she is unavailable. Annie selects her daughter Joan and then mentions that she needs to also include Nicolet – for the sake of family peace.

Now we have three generations involved. The next thing the generational advisor focuses on is creating a “Care Squad.”

A generational advisor works as the team leader and leads the discussion: Who has knowledge of Helen and Joseph’s medical history and will speak for the group with doctors, notify family members, fill out paperwork, etc. in an emergency? All the “Care Squad” members know where the “Grab ‘n Go Bag” is kept, and one is in charge of keeping it updated. Annie and her daughters consider this is also a good idea for each of their families, so she lists the advisor ‘s contact information in case there are questions.

Since planning for extended or long-term care rarely involves only one person, the generational advisor’s role is to bring clarity to the process. Trust will transfer generationally or with the client’s friends as you orchestrate establishing a core group and suggesting an immediate benefit like the “Grab and Go” bag or later an insurance solution. We see this all the time with advisors whose successful practices are built on referrals.

Each member of the Core Team may approach planning differently. Stories are conversation openers and help the advisor see where his experience and knowledge establish a crossroad with team members. Listen to their story for essential clues as to what is genuinely their immediate or less immediate concern.

All the while, you are listening or asking:

- Who has had experience with extended or long-term care? Personally, or through a friend?

- What have they read?

- Whom do they believe?

- Who else has offered advice, and will they consult with that person as well?

- Is their family health history or lifestyle a factor in whether they chose life insurance or an annuity to fund care or go a route for being uninsurable?

- Did they ask about costs or mention concern about finances, or funding care for a family member or themselves?

Options for Extended and Long Term Care

Joseph has emphasized that he and his wife want to age-in-place because they feel they are too set in their ways to want to make “new” friends. Joan adds that she feels they will adopt and become adept with using only a limited tech and service support.

Annie wants to consider selling the home and moving them into an CCRC like Helen’s sister because at this stage if they age in place, she suspects that they will need additional help, and Annie works full time.

This leads to the topic of funding options. The advisor discusses the following:

- Since Joseph and Helen have a very small mortgage, the advisor asks if they are open to considering a reverse mortgage;

- Since Joseph has a $100,000 whole life insurance policy, might they consider borrowing from it, and

- Do they want to consider “spend downing” assets to qualify for Medicaid?

Not surprisingly, there are as many opinions in the core group as options. Now, the generational advisor takes control and selects various questionnaires and documents for the Core Team to complete, although the advisor can already fill in some of them himself. As a result of the process, Annie’s daughters start to ask her about a plan for their mother (remember she is single). The advisor indicates that planning now for Annie may offer more or different options – such as life insurance with a long-term care (LTC) rider, or using her health savings account to fund LTC premiums or an annuity with an accelerated benefit that may offer some income if she doesn’t need extended care.

The generational advisor temporarily pulls the Core Team back to planning for Joseph and Helen’s needs. The advisor now needs to get a complete picture of who will help if they stay in the home:

- Who lives closest to Joseph and Helen?

- What is the availability of family members?

- Who is listed, and in what order on the Communication/ Contact questionnaire?

- What is the current health and wealth of those that may offer support?

The advisor is now getting a fuller picture of both the immediate situation – arranging care for Joseph and Helen – while gaining a better generational picture of family availability and dynamics.

The Role of Technology and Aging in Place

For Helen and Joseph to remain in their home, Annie will need to discuss the role that technology can play in keeping her parents in the independent living environment that they desire. While not every device will be applicable, technology does make it more likely that Helen and Joseph – with Annie’s oversight – can stay in their home for a longer period of time.

The Aging-in-Place Tech Showcase highlights new and innovative technologies that look to address some of the biggest challenges in long-term care. It’s a rapid-fire format where companies across the care spectrum present how they are managing care, changing the way we age-in-place, and using technology-driven solutions to address the needs of a rapidly aging society. Many new tech companies are springing up, many of which got their ideas from personal experience with healthcare. Solutions like:

- A “digital pharmacy” that uses predictive inventory to deliver prescriptions in order to avoid running out of a drug and offers text and call services with a real pharmacist — not a chatbot — on demand.

- Light, sound, text and email alerts designed for caregivers to wirelessly track sleep duration and quality, to prevent falls and catch medication errors.

- Technology to navigate over 30 life issues, such as expenses, transportation, family support, counseling, and symptom management programs that support 500 unique symptoms with over 20,000 recommendations from over 30 different healthcare modalities.

- Technology that identifies early signs of deterioration in health before more obvious physical symptoms begin to appear.

- Real-time alerts that help staff and caregivers detect and prevent falls, detect wandering and help monitor issues such as side effects to medications, urinary tract infections, sleep apnea, depression, and dehydration.

- Smart sensor technology yields data showing changes in behavior (or missing of behaviors) that signal physiological changes. These behavioral changes can reflect medication adherence and significant activity levels in eating, fluid intake, sleeping, toileting, and socialization patterns.

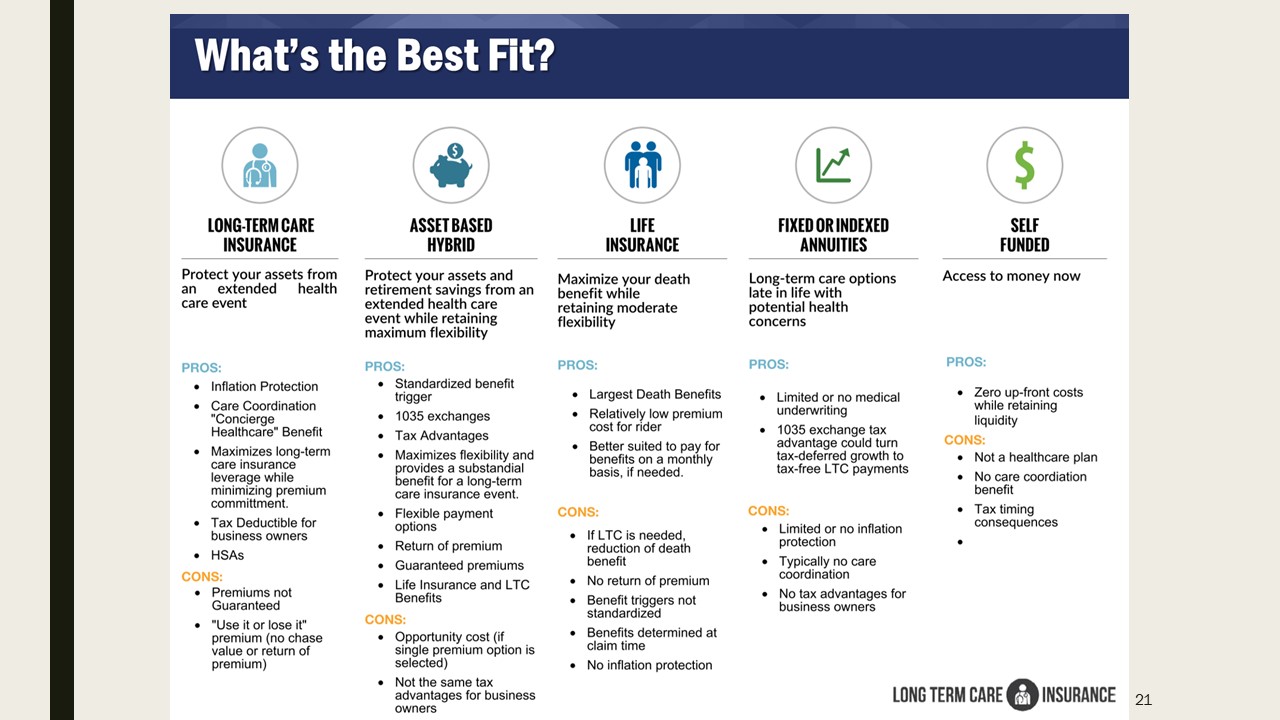

Potential Planning Options for Joseph and Annie

There are four choices:

- Traditional long-term care insurance,

- Asset-based long-term care insurance

- Hybrid Insurance (life insurance with chronic illness or LTC rider)

- Reverse mortgage.

Part of the decision-making process is considering which product and how much of the cost of care will be offset by the product. The Core Team is surprised by not only the current costs but also the exposure to increasing costs.

The group starts to discuss the effect that COVID-19 will have on costs for facility care. They discuss using insurance to offset some of the costs and technology to help them age-in-place. As it is likely that the Core Team is telling some of their friends about the plans or the technology, the generational advisor mentions that Genworth produces an annual Cost of Care Survey that will allow them to consider other county, city, and state costs.

Joseph and Helen decide they want to stay in their home for as long as possible and choose to work with a reverse mortgage specialist recommended by the advisor. Meanwhile, the Core Group tells the advisor that they want to understand the different approaches used in hybrid life insurance policies.

The generational advisor starts with a simple explanation of three common forms of hybrid life insurance policies with accelerated death benefit riders, which are add-on features to enhance the underlying life insurance policy. He mentions that the riders must be decided at the time of purchase and are factored into the total premium costs accordingly.

The devil is in the details with policies, so the advisor will review the particular policy language and contract details carefully as he gets closer to quoting specific policies.

- Life insurance with LTC death benefit acceleration rider: The benefit of this type of policy is that policy-owners may accelerate payments (i.e., take an advance) from their death benefit for qualified LTC needs. Under this acceleration of death benefit, the LTC benefit received will reduce the death benefit dollar for dollar. Once the death benefit is fully used up for LTC needs, the policy terminates. Any unused death benefit will be paid out to beneficiaries at the time of the insured’s death.

- Life insurance with a chronic illness rider: This type of policy is very similar to the previous policy, except some carriers will only accelerate death benefit payments for a qualifying, permanent chronic illness. A chronic illness refers to a condition with no medical cure such as heart disease, Parkinson’s, some cancers, etc. A broken hip may generate payments under an LTC rider, but it would not qualify under a chronic illness rider because it is not a permanent condition. There are three common approaches to chronic illness accelerated death benefit (ADB) riders: the discounted death benefit approach, the lien approach, and the dollar-for-dollar approach.

- Linked benefit life insurance with extension-of-benefits (EOB) rider: This policy with EOB rider offers two distinct benefit pools. LTC benefits may be paid out even after the death benefit has been completely depleted. The first benefit pool is an acceleration of the death benefit, available for monthly LTC benefits or as a death benefit. Once this first benefit pool is completely used up, and assuming the insured still has an LTC claim, monthly benefits will be paid from the second benefit pool, which may be up to three times more than the policy’s death benefit.

What About Options for Annie?

It is not uncommon for individuals involved in the planning process to start to stress about their plan or the plan for someone whom they may have to care for. As the Core Team works on a plan for Helen and Joseph, Annie’s daughters become increasingly concerned about the impact caregiving for their grandparents may have on Annie.

Joan calls the advisor on her own. She has two concerns:

- The effect or negative impact of taking time off from work may have on Annie’s career or retirement plans, and

- The impact on Annie if she would have to supplement Joseph and Helen’s income and care expenses. She mentions that since Annie is single, she would not be able to help given she has children and grandchildren.

So which planning option could the generational advisor introduce for Annie? Traditional long-term care insurance, long-term care asset-based hybrid insurance, life insurance with a chronic illness or LTC rider, or a reverse mortgage?

The advisor shares this sample chart to get feedback as to a general approach suitable for different generations.

Speaking to the Core Group, the generational advisor can detail various features depending on which product and type of contract the various family members are interested in for themselves. Depending upon which type of coverage a family or family member selects, the advisor can review important features, which allows each generation to indicate their concerns – allowing the advisor to move forward instead of hearing, “I’ll think about it!”

In this case, while the asset-based product may offer Annie a supplemental income opportunity, for her personal needs, Joan is interested in a life product that could cover her and her husband but also provide some protection and funding if they need extended or long-term care.

Key Takeaways

To become a generational advisor:

- Focus on immediate client needs and build relationships that support those needs.

- Build family trust by creating a personalized plan for those who require caregiving and those who will be the caregivers.

- Family and/or friend dynamics tell the story! Create a file for each family unit in the core group to work differently with each generation by listening to their concerns and future plans.

- Capture each person’s emotional, psychological, and financial viewpoints and level of knowledge in the core group.

- Discuss the process, so each generation understands that the product and services you suggest fit that generation’s needs and concerns.