We also want to help spouse beneficiaries choose the correct method when moving inherited assets because they have more options than non-spouse beneficiaries. But the type of movement they use could is determined whether they owe the 10 percent distribution penalty, for instance, on distributions they take from inherited accounts. What if you meet with a client and find out, “Hey, this client has already made a mistake.” Can that mistake be fixed?

We have so many American millionaires, and guess what? They are millionaires because they are 401(k) millionaires and IRA millionaires, but what no one is paying attention to is how we preserve that growth, right? How do we ensure that we do not end up eroding years of market growth by one transaction?

Now, estate planning, particularly distributions to beneficiaries, must also be considered because, in some cases, beneficiaries can continue benefiting from the tax-deferred treatment available to these accounts with limited options.

One mistake can cause an entire account to be included in income in one year instead of stretching it out for over ten years or over the beneficiaries’ life expectancy if that is an available option. When we have that conversation with clients, we have to talk to them about, “How do you move those assets,” and part of the conversation has to be, “Are you the owner or are you the beneficiary that has inherited a retirement account?” because the rules are different.

There is so much money in retirement savings accounts: over $37 trillion as of the third quarter of 2021, and $13.2 trillion is in IRAs. The rest of it is in employer-sponsored retirement plans. But guess where those assets are going to end up? Eventually, in IRAs, right? The statistics show that most 401(k) participants eventually move their assets to IRAs. When I say “401(k)s,” I am using it as an all-inclusive term to mean pensions, 403(b)s, governmental 457(b) plans, profit-sharing plans, and the like.

Now, when a client walks into your office and says, “I have a 401(k) account, and I want to roll it over to an IRA with you,” there are certain factors that we must take into consideration. It includes something as simple as, should I do a direct or indirect rollover? Do I have after-tax assets in my 401(k), and should those be treated differently? Are there advantages using specific strategies instead of others?

Now, here is the deal when it comes to IRAs, especially. Ultimately, the IRA owner is responsible for ensuring things are done right, but we know that they engage us to help. Sometimes it is not about responsibility from a regulator’s perspective, and it is a matter of customer relationship. If a client depends on you to point them in the right direction when things do not go right, they will be upset with you. “You did not tell me I had 60 days to return this money. Now I am finding out that my $2 million distribution is included in income because here I am, it is day 70, and no one told me.” No one is required to tell them. The IRS has confirmed this, but as I said before, they are relying on us to help them, and part of the way that we are going to help them is by educating them on the proper ways to move their accounts and the limitations that apply.

It starts with the basics. Almost every week, I get a client call from an advisor who says, “Denise, my client has an IRA at firm A, and they want to roll it over to firm B with me,” and I will say, “Hang on a second, before we go any further. I think you mean a transfer, right?” And they will say, “Yes, I know because that is what you teach me, but you and I know that that is what I mean.” And my response usually is, “Well, that is true, you and I know, but you do not want to say rollover when you should be saying transfer because guess what? When you go to the financial institution and say, ‘I want to do a rollover,’ they will give you a distribution form because they think you want to take a distribution and then roll it over within 60 days.”

If you want a transfer, you must say, “transfer.” If it is a direct rollover, you have to say, “Direct rollover,” instead of, “send me a distribution,” which I would then rollover within 60 days, which would be an indirect rollover. We must distinguish between a rollover and a Roth conversion because one is included in income, and one might not be included in income, especially when the assets come from an employer-sponsored retirement plan.

Let us first look at the rules applied to retirement account owners. It is such an important distinction to make. If a client walks into your office and says, “Advisor, I want to rollover an account that I have with firm A to an account with you.”

One of the only things you must find out is: are you the owner of the retirement account, or is this an inherited account? Why is that? Because the rules are different. Some can be rolled over, and some cannot be rolled over. For some, the only option is to move those assets is as a trustee-to-trustee transfer. If it is assets in an employer-sponsored retirement plan, then for the beneficiary, the only option is to move those assets as a direct rollover.

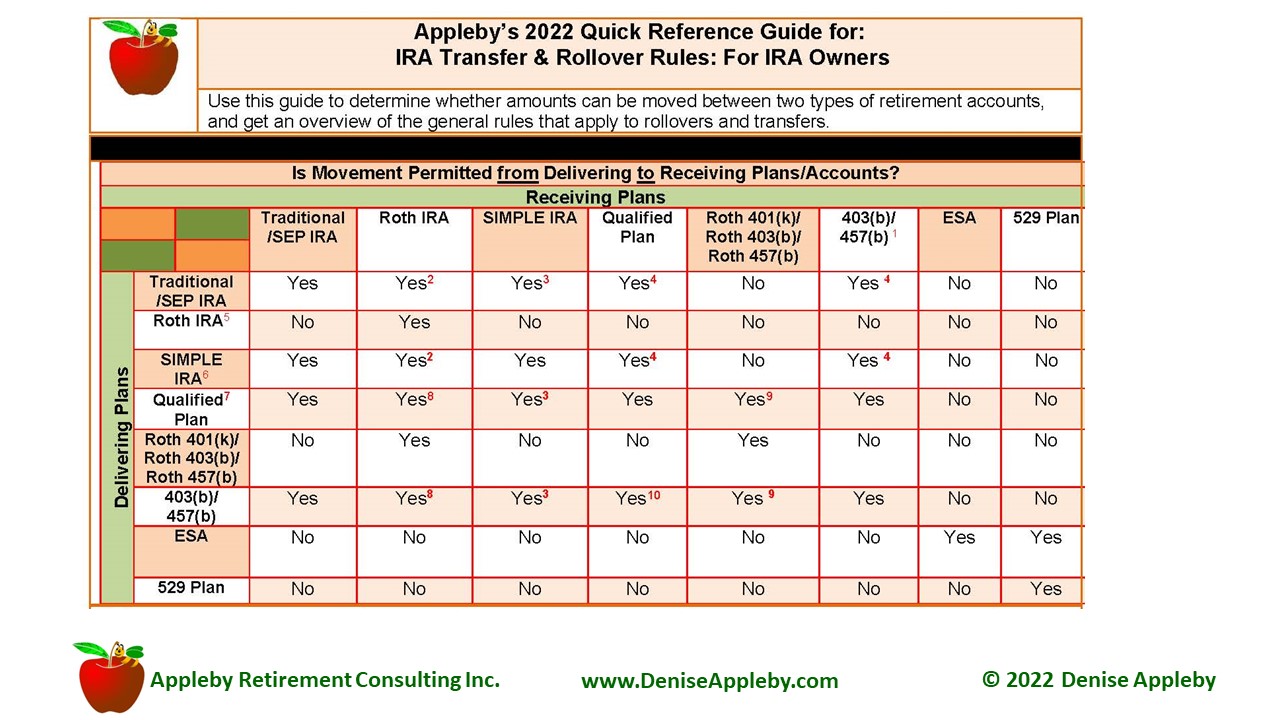

Here is a chart that provides guidance about the allowable movement of retirement accounts.

© 1998-2002, Appleby Consulting. All rights reserved. To order this and other Appleby Retirement Consulting Guides, please visit IRAPublications.com/quick-reference-guides.

Suppose someone comes into your office and asks, “I have a Simple IRA. Can I move it to a Traditional IRA?” The answer is yes, but there is a footnote. You can do that only if the Simple has been funded with a Simple contribution for at least two years. “Can I move my Roth 401(k) account to my Simple IRA?” No, you cannot do that. A Roth 401(k) account can only be moved to a Roth IRA or to another designated Roth account such as a Roth 403(b), Roth 457, or another Roth 401(k). Sometimes there are limitations or caveats that must be taken into consideration.

Transfer/Rollover Rules for IRA/401(k) Owners

When a client walks into your office and says, “You know, I like your firm. I want to bring my IRA to your firm, and my existing IRA is at the bank across the street. I just want to run over there, ask them for a distribution, and bring it over to you. Is that okay?” Well, it could be, but here is what we need to consider. If the client runs across the street and asks for a distribution, then the only way to put it back into the IRA with the new advisor is as a rollover. And that is perfectly fine if the IRA owner has not done an IRA-to-IRA rollover in the preceding 12 months or cannot do another in the succeeding 12 months. What am I talking about here?

Unless the client needs to use the funds temporarily, the transfer method is the one they should use. Why? It is not subject to the 60-day deadline I will be talking about; it is not subject to the one-per-year rollover rule; it is not reported on the individual’s tax return, and there is no tax withholding. Transfers are better. Rollovers are non-taxable; that is true. It is reportable but non-taxable, but it is only non-taxable if the amount is, in fact, eligible to be rolled over. You do not have an issue with a transfer.

If a rollover misses the 60-day deadline and does not qualify for a waiver, it is not eligible to be rolled over; and if a rollover breaks the one per year rollover rule, it is not eligible to be rolled over. Also, rollovers could result in a loss of extension to the 10 percent early distribution penalty. That is usually an issue when you are changing plan types, and by that, I mean you are moving from an employer-sponsored retirement plan to an IRA or vice versa. So, that is one of the things you want to think about as you have that conversation about moving assets; and for non-spouse beneficiaries, they cannot do rollovers of inherited IRAs.

For employer-sponsored retirement plans, they can be rolled over, but only as a direct rollover. So, let us talk about the 60-day deadline. Now, once upon a time, the IRS used to get thousands of requests from people saying, “Please help me. I took a distribution and intended to roll it over within 60 days, but life happened. Can you give me a waiver?” To have the IRS even consider that, they must pay the IRS a fee of $10,000, and guess what? That fee applies whether or not the IRS issues a fair ruling. So, why not avoid that in the first place, if you can?

Let us assume, however, that the client is in the position where this is the only option. They take a distribution, and they use it on a short-term basis. Now they have 60 days to get it back in. What are some of the rules that we need to think about? Well, when does the 60-day period start? It starts when the account holder receives the distribution. Someone runs into your office, frantic, thinking, “Oh, I missed the 60-day deadline.” Then, you will ask them, “Well, when did you get that check?” It is not when the check was issued; it is when they got it because that is when the 60-day period starts, right?

Here is a point of confusion I want to clear up. You can do an IRA-to-IRA rollover only once for a 12-month period, but that does not stop you from rolling over one distribution in installments. So, if someone takes a distribution of $100,000 today, they can rollover $10,000 tomorrow, and $20,000 next week, until they rollover the amount that they can afford to rollover up to the $100,000. If someone does a distribution this week and a distribution next week, or distributions from two different accounts, then each stands on its own to determine if the 60-day period applies.

What if someone misses the 60-day deadline and does not qualify for a waiver? That amount is included in income because it is not eligible to be rolled over. Now, the 60-day period does not apply to a direct rollover. What if the client comes into your office and says, “Hey, I missed the 60-day deadline. What am I going to do? I have this check in my hand.”

Part of what you are going to do is check to see if the client qualifies for a waiver. First, you want to look for an automatic waiver, which would not apply if the client had the check in their hand because it applies to everything they should have done within the 60-day deadline, including giving you the check.

Let’s say you were so excited about going on vacation in the Caribbean, you stuffed that check in your drawer, and you forgot about it until the client returned six months later and said, “What happened to my check?” Or maybe you made a mistake and put that check in a checking account instead of a client’s IRA. In that case, the 60-day period is extended to a year. There is an automatic waiver in that case, so this is the first thing you want to look for.

The second thing you want to look for is self-certification. You want to check for a list of reasons in Revenue Procedure 2020-46, where the IRS pretty much said, “Listen, so many people are coming to us with so many requests that are similar about missing their 60-day deadline, why just not grant a blanket waiver for those instances?” This can apply when certain requirements are met, such as someone is sick, someone was in prison, or an issue with the Post Office.

The complete list is in Revenue Procedure 2020-46. If you check that list and your client meets any of the requirements or any of the reasons on that list, then all you need to do is get a self-certification certification from the IRA owner. There is a sample certification letter in Revenue Procedure 2020-46.

As soon as the reason for missing the deadline no longer exists, the check or the amount should be deposited as a rollover within 30 days. If a client does not qualify for any of those, the next step is to see whether or not they meet a suitability test for an IRS waiver because you do not want your client going to the IRS for a private letter ruling (PLR) when you know the IRS is going to say, “No.” Now, the IRS should provide a waiver request where the failure to waive such a requirement would be against equity or good conscience, including the death of a blood relative, natural disaster, etcetera. However, there is no guarantee that the IRS will say, “Yes.”

Losing Tax-Deferred Status by Breaking the One-Per-12-Month Rollover Rule

The one-per-year rule only applies to IRA-to-IRA rollovers. How does this work?

Someone takes a distribution; they roll it over in 60 days from either a Traditional IRA to a Traditional IRA or Roth IRA to a Roth IRA. That can be done only once during a 12-month period.

How do we know this? Before 2014, pretty much all of us, including the IRS, as they explain in publication 590, thought that you could do this for as many IRAs as you own. A tax attorney, of all people, used that rule because he had multiple IRAs, and he performed more than one IRA-to-IRA rollover during a 12-month period. The person reviewing his tax returns said, “How come I have two 1099-Rs and two 5498s for this one person for the same year?” They disallowed the second rollover. The tax attorney took the IRS to court, and he lost because the tax court said, “Listen, I do not care about what publication 590 says; you can do this only once during a 12-month period.”

If you have multiple Traditional IRAs, multiple SEPs, or multiple Roths – it does not matter how many you have – you can do this only once during a 12-month period. So he appealed to the IRS and said, “Listen, I should not be penalized because I relied on publication 590,” and the IRS said, “I feel for you, but you rely on IRS publications at your peril.” Can you believe that? They tell you you cannot use IRS publications as any substantial authority. Now, when a client wants to rollover assets from employer plans or IRAs, part of what I recommend is that you create a checklist of items or amounts that are not eligible for rollover.

Why is that? Because if they are supposed to take an RMD, for instance, that amount cannot be rolled over; it must be distributed first. Hardship distributions, excess distributions, then this distribution or rollover, will it break the one-per-year rollover rule? Did they miss the 60-day deadline, and do they not qualify for a waiver? So, what if someone does a rollover on an ineligible amount? What happens then? If the amount is rolled over to an IRA, it creates an excess contribution that must be distributed by the IRA owner’s tax filing due date plus extension. And if it is not corrected, it is subject to a six percent excise tax.

Rollover to Change the Plan Type Can Be Surprisingly Costly

With rollovers from employer plans to IRAs, how does it affect estate planning? What are the distribution options for beneficiaries? What about creditor protection? Does the client have employer securities in those accounts because if it is rolled over to an IRA, then they will lose tax benefits? If they are in a situation where the client will lose a 10 percent early distribution penalty exception by rolling over that amount, and if the amount is in a pre-tax account, pre-tax 401(k), for instance, what happens if you roll it over to a Roth IRA versus a Traditional IRA?

Before rolling over those amounts, the client must be aware of the tax consequences. Trust me when I tell you, the Department of Labor does not joke about instances like that, where clients mean to rollover assets. A client needs to receive full disclosure of the differences between the accounts that they hold the assets in and the accounts that the assets are going to. So, check the account statement. Do they have employer securities? Because if they do, then there could be a tax-saving opportunity if those assets are not rolled over. You roll it to an IRA; you lose those benefits.

Do they have after-tax contributions in a 401(k) account? Because if they do, those amounts can be rolled over to a Roth IRA, as opposed to a Traditional IRA, so that the rollover is tax-free, and the tax-deferred amount remains in the Roth IRA, where it eventually grows tax-free. We can still do Roth conversions, which are not subject to the one-per-year limitation. Remember that when a client wants to do a Roth conversion, remind them, “Listen, you have got to make sure that you want to do this. Talk to your tax advisor.” Why? Because, once upon a time, when you did the Roth conversion, you could reverse it as a recharacterization by your tax filing due date plus extension. You cannot do that anymore. So, once you do a Roth conversion, you are locked in. Have your client talk to their tax advisor to do a Roth conversion suitability analysis to see if it works for them before they decide because once you pull that switch, you cannot turn it off.

So, can mistakes be fixed? If you find out that a client makes a mistake, do not give up just yet. Try to see what type of mistake it is and who made the mistake. If it is the financial institution, they must fix that mistake as long as it is not impossible to do so, and I have never encountered a case where it is impossible.

Look for remedies. So, they have missed the 60-day deadline. Do they qualify for a waiver? Where applicable, ask the IRS for the probability of the ruling, but only if it makes sense. Now, the IRS has the authority to waive the 60-day deadline, but they do not have the authority to make an exception to the one-per-year rollover rule. But, if the one-per-year rollover rule is going to be broken because of a failed financial institution, then an exception applies. You remember, in 2020, when RMDs were waived, the IRS made an exception to allow those amounts to be returned.

The Transfer/Rollover Rules for Inherited Accounts

Moving onto beneficiary options, I am sure you have heard by now that the Secure Act took away the option for beneficiaries to take distributions over their life expectancy. In most cases, the 10-year rule applies unless the beneficiary is an eligible designated beneficiary. So, the question becomes, then, what is the big deal?

When it comes to inherited IRAs, have that conversation with the client, but do not send them on their merry way to take care of it themself. Help them as much as you can, and if you are on the receiving end of the inherited IRA, make sure that you submit for the transfer because, in that case, it is less likely that mistakes are going to happen. I can guarantee you that 90 percent of the time when the client goes to the financial institution that has the inherited account to handle it themselves, they make mistakes because they do not know the lingo.

Even though you say to the custodian, “I want to do a transfer,” and they fill out the distribution form and give it to the custodian, that will result in a distribution. The custodian does not care because their position is, well, here are all the disclosures. You sign the paperwork, and when you do that, you attest that you have sought tax and legal advice and read all the stuff. You know that no one will read that. Just like when I get my insurance policies, I do not read that because it is all Greek to me. It is the same thing with clients, even though it seems very simple to us.

Regarding IRAs, the only way to move those assets is a trustee-to-trustee non-reportable transfer. When you move from one inherited account to another, you can take the RMD from the receiving account if both are sent from the same decedent. For a spouse beneficiary, the transfer can be made from the spouse’s inherited account to their own account.

For qualified plans, the only way to move those assets is as rollovers, and for non-spouse beneficiaries, the only option is as a direct rollover. They cannot roll it over to their own IRA; it must be to a beneficiary IRA.

Spouse beneficiaries have the flexibility of rolling those assets over to their own IRA or a beneficiary IRA. If the beneficiary is a surviving spouse of the account owner, then they can treat the inherited IRA as their own and then convert it to a Roth IRA.

Employer-sponsored retirement plans can be rolled over to Traditional or Roth IRAs, and, in that case, that is the only way an inherited account can be converted. If you have an inherited Traditional 401(k), you can roll it over to a beneficiary Roth IRA and, in that case, you have a conversion of inherited amounts.

Spouse Beneficiary Making Wrong Choice That Cost 10% Penalty Exception

When a spouse inherits an IRA, they can move it to their own IRA, or they can move it to a beneficiary IRA. Then the question becomes: when that spouse’s beneficiary is sitting in front of you, and they do not know what to do, here is a tip. Have that spouse beneficiary keep the assets in a beneficiary IRA until they can decide if they want to put it in their own IRA. Why is that? Because if they put it in their own IRA, there is no going back. They must keep it in their own IRA, but if they put it in a beneficiary IRA, they can move it to their own IRA later on if they change their mind.

Now, what is the benefit of keeping it in a beneficiary IRA? Suppose the spouse beneficiary client is under age 59½ and they plan to take distributions before the age of 59½. In that case, the solution is to have them keep those assets in a beneficiary IRA and take distributions from that beneficiary IRA. Think about the 10 percent early distribution penalty. If you take a distribution of $100,000, for instance, and all of it is pre-tax, then that amount will be subject to a 10 percent additional tax of $10,000. Pretty stiff penalty, right? Unless an exception applies, and one of those exceptions is a death distribution or distribution due to death. A distribution can be treated as a distribution due to death only if it is taken from a beneficiary account.

If you work on the operations side, you will see this because the 1099-R issued for a distribution has a code in box seven. If it is a code four, it means a distribution is due to death. Code four says to the IRS, “This is a death distribution, and it is not subject to the 10 percent early distribution penalty.”

There is another opportunity where a spouse beneficiary might want to minimize distributions. If the account owner dies before the required beginning date (when you are supposed to start taking RMDs), the spouse beneficiary can keep it in a beneficiary IRA. They would not need to start taking distributions until the latter of December 31st of the year following the year of death or the year in which the account owner would have reached age 72. Now, if the account owner is very young, keeping it in a beneficiary IRA is a good strategy because the spouse, at that point, can decide whether they want to take distributions.

Once they are required to put it in their own account, you would use the uniform life expectancy table to calculate RMDs, producing a lower RMD than if they keep it in the inherited account. So, when the spouse beneficiary meets with you, you need to ask: “Are you under age 59½? If yes, do you plan to take distributions before you reach age 59½? How old was the decedent, and how old are you?” Because you can use the responses to those questions to implement distribution strategies for your spouse beneficiary client that is cost saving, including avoiding the 10 percent early distribution penalty.

Now remember, too, that spouse beneficiaries are subject to the one-per-year rollover rule. I had a case where a spouse inherited five accounts from her husband and decided to move all of them using the 60-day rollover method. You cannot do that, even though the accounts were inherited, so because of doing that, only one of those distributions could have been rolled over.

Your client is already dealing with the death of a loved one, you do not want them doing anything that will add to that, and part of what we can do is to help protect them from mistakes like this. Remind them they need to come and see you before they sign any paperwork or speak with other financial institutions because not every financial institution is training their associates on these nuances. If you have clients who are already distraught because a loved one died and are signing paperwork through tears, not even understanding what any of it means, this is where we need to step in and help them.