We have known for quite a long time that when you are investing for retirement distribution or taking distributions in retirement, it is different from the pre-retirement wealth accumulation phase. It is not just a matter of getting to the top of the mountain but safely getting back down the mountain in the face of the longevity risk, the sequence of returns risk, amplifying investment volatility, the spending shocks related to long-term care, and other events.

Retirees must think differently when spending from their assets versus when they are accumulating their assets. But it is still the Wild West in terms of strategy. You can ask the fundamental question, “What’s the safe spending rate from an investment portfolio?” and get wildly different answers. The correct answer is to understand better when the different approaches might best apply to different types of clients.

Back in 2017, in one of my older books, “How Much Can I Spend in Retirement,” I made an effort to identify different retirement strategies available today. At that time, there were 37 different spending strategies. How can we start to position these different strategies with different individuals? The solution here is to assess retirement income style preferences. When a client starts to think about how they might want to approach building a retirement strategy, we can match these individuals’ preferences to a method for sourcing their essential retirement income. How do they want to draw to cover their core retirement expenses? Are they comfortable using a total return investment portfolio, or would they prefer a different approach, whether time segmentation, income protection, or risk wrap? Once they have their floor covered, how can we better align their discretionary goals to an investment portfolio?

We have known for a long time that modern portfolio theory, the accumulation-based models that many financial planners use, were not designed for retirement. Even Harry Markowitz, the founder of Modern Portfolio Theory, has pointed this out after winning the Nobel Prize. He said, “I never really thought about investing for households. Modern Portfolio Theory was meant for large institutions”, and households face many differences that coalesce into retirement. Modern Portfolio Theory was an assets-only model, and it is a single time-period model. How do you choose an asset allocation to affect the risk-adjusted returns over one time period if there is no distribution constraint if you are only trying to grow the pot of assets? The household’s problem is different; they need to fund distributions over an unknown time horizon. In an article from 1991, Markowitz pointed out that just after winning the Nobel Prize, Modern Portfolio Theory wasn’t designed to meet the household investing problem.

What are Today’s Primary Retirement Income Strategies?

Now, as well, we have had different retirement strategies. There are four core strategies that we are trying to help guide clients towards understanding which one might be appropriate for them: total return investing, income protection, time segmentation, and risk wrap.

How do retirees choose a strategy? Now people might be listening to radio shows, and many financial advisers have radio shows where one show after the other might present completely contrasting retirement approaches. They might read personal finance blogs or follow the personal finance consumer media. They might attend a local seminar or a webinar or attend a local class. Many advisors will teach through the local community, college, or education programs for the Parks and Rec in their hometown a class on retirement planning. Or they might go directly to work with a financial advisor.

Increasingly, I think we will find advisors who will be more agnostic and may be able to offer different strategies. Right now, however, it is not a very efficient process. We have lacked the tools to identify who should use which strategies, and that is really what this research was meant to help provide such a tool to help match people to strategies.

Risk Tolerance Questionnaires

We have these during the accumulation phase, and it presupposes everyone is a total returns investor. It is based on Modern Portfolio Theory to identify which asset allocation a person is most comfortable with. This is the tool that gets used for pre-retirement planning. Ultimately, to the extent that people do not treat retirement as being different from accumulation, it continues to be used post-retirement. Risk tolerance questionnaires were born out of necessity and designed to provide advisors with something to document the suitability of an asset allocation strategy. However, it is only about short-term market volatility. With retirement, there will not be a single metric that people are trying to optimize. They are going to have different concerns, and they will place different importance on different concerns, whether they are worried about outliving their money in terms of their core retirement expenses, worried about missing out and not maximizing their overall lifestyle as much as possible, worried about not having liquidity to cover the unexpected long-term care and so forth in retirement. They also might be worried about legacy. (However, we found this is a less critical overall goal for people with our study.) Today’s risk tolerance questionnaire wasn’t designed to handle these other types of concerns.

So, retirement is different, and we need a tool to capture the differences. We need a more multidimensional assessment of the risks people face in retirement to understand better their concerns and what kind of strategy might better facilitate them. Concerns such as:

- Are you concerned about longevity, or are you concerned about meeting your core retirement expenses over your whole lifetime?

- What is your concern about lifestyle? This is the discretionary income goals. Are you concerned about not maximizing your overall spending and getting the most enjoyment out of retirement?

- Are you concerned about meeting legacy goals and leaving something to the next generation?

- Are you concerned about liquidity and having reserve assets available for the unexpected in retirement?

It can be hard to match up a style, but this is how we might be able to facilitate that conversation with clients by having a starting point for the conversation of the style that might best appeal to them.

Our research was based on a large literature review of reading and anything we could about retirement planning, designed for consumers, financial professionals, etc. What was being discussed? What were the factors that might impact people’s decisions and that represented a range of potential attitudes? We ended up writing about 900 questions. This initial research phase was done through Retirement Researcher, my website. We had about 1,500 participants, many of whom are do-it-yourself retirees who treat personal finance as a hobby.

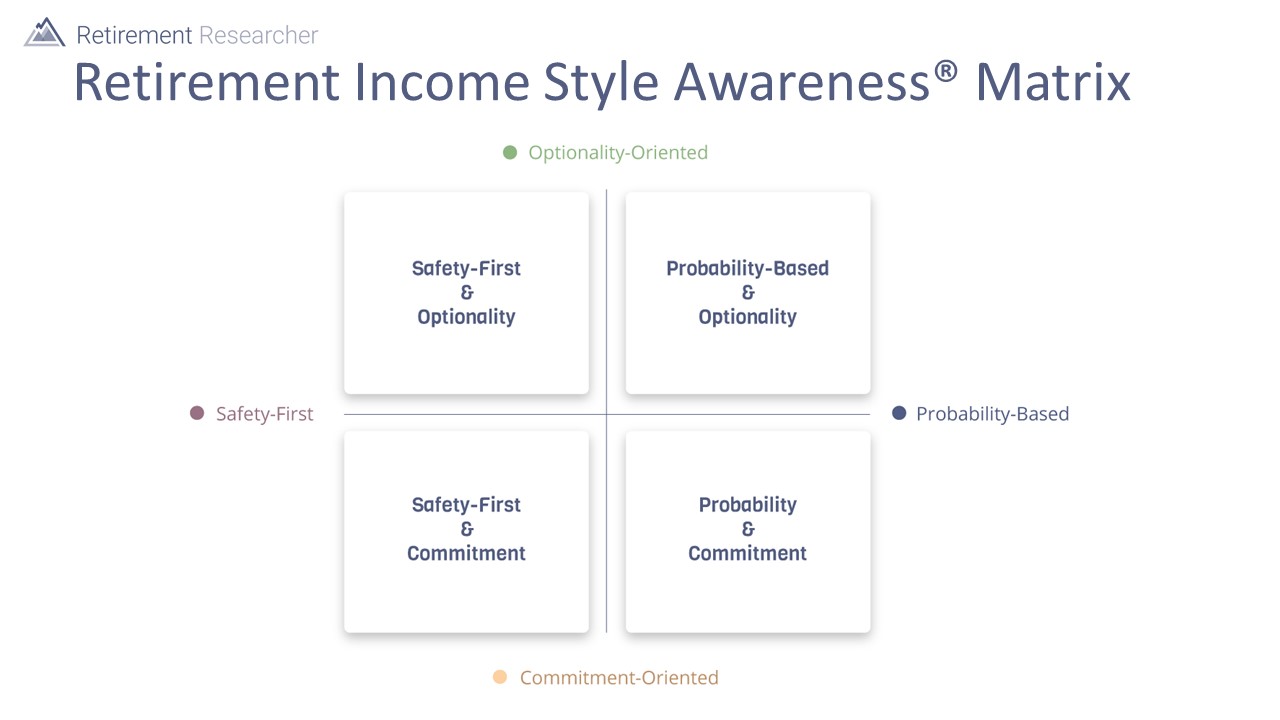

Two factors showed the most importance in explaining the style: probability-based versus safety first and optionality versus commitment. Four secondary factors (time-based vs. perpetuity income floors, accumulation vs. distribution, front-loading vs. back-loading retirement income, true vs. technical liquidity) were also important and relevant to understanding a person’s preferences for retirement income.

The Retirement Income Style Awareness® (RISA) Leads to Specific Strategies

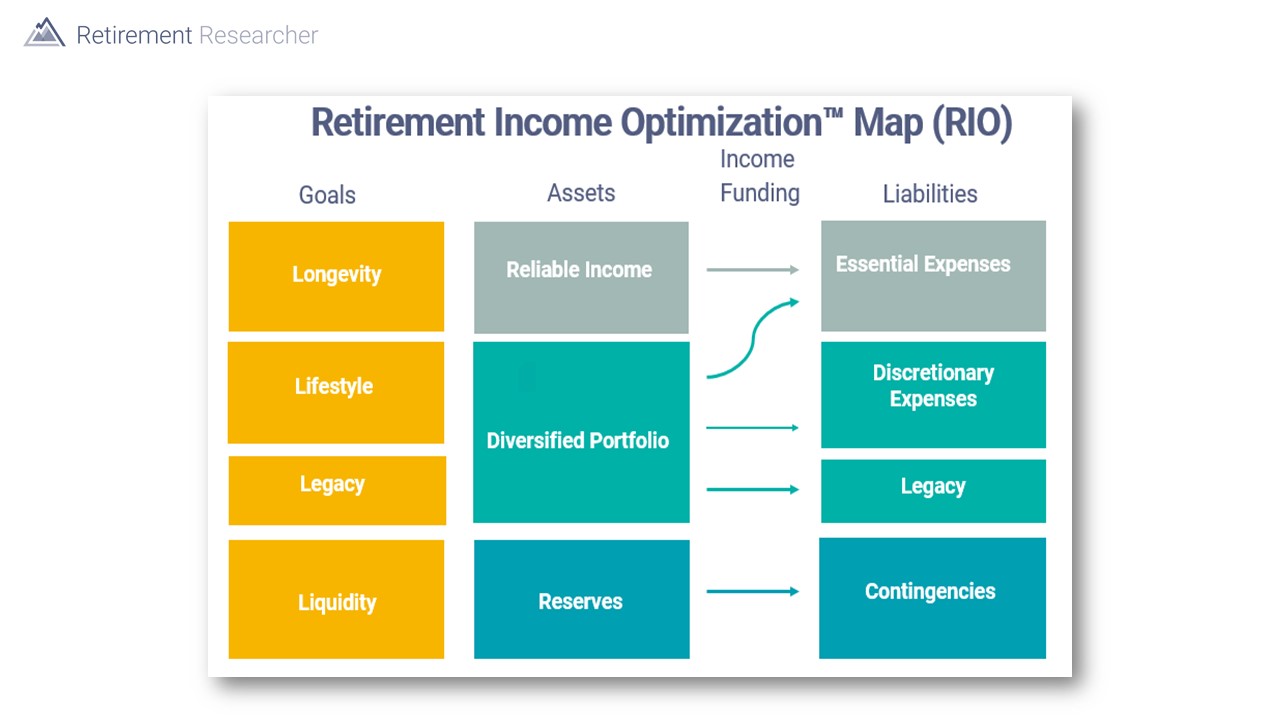

So, this is about building a financial plan for clients where the financial goals or those four Ls reflect those concerns, mapping the goals into the liabilities or expenses associated with those goals, and positioning assets to match the liabilities.

Assets are treated as reliable income assets (such as Social Security, pensions, annuities, individual bonds held to maturity, and so forth), the broader diversified investment portfolio, and then reserve assets (which are simply things not earmarked for other purposes that are available to help cover contingencies in retirement such as spending shocks and things that aren’t budgeted into either essential or discretionary spending).

The Retirement Income Style Awareness® (RISA) profile is about understanding how people want to source their essential spending. Are they comfortable doing that with a diversified investment portfolio? Do they want to do that with individual bonds? Do they want to do that with some type of annuity product, whether it is an immediate annuity or a deferred annuity with a living benefit attached to it?

Our retirement income style approach is ultimately agnostic. We do not think any of the four general strategies are superior; we think they are all viable. It is really, “What are you comfortable with? Are you comfortable relying on the stock market, or are you comfortable having contractual protections?”

The first of the two primary retirement income style factors is probability-based versus safety first. How do you want to draw retirement income? How do you want to source your reliable income in retirement? If you are probability-based, you are comfortable depending on market growth. Depending on the risk premium, the idea is that stocks will outperform bonds over reasonable holding periods. Historically, that has been the case with the six percent risk premium we have seen with large-cap U.S. stocks over long-term U.S. government bonds going back to the 1920s.

If you are safety-first, you are not comfortable fully being dependent on the stock market to source your essential spending needs for retirement. You would prefer some sort of contractually driven income to have more safety. Of course, nothing is 100 percent safe, but relative to unknown market outcomes, having contractual protection implies a much higher degree of safety. That doesn’t have to be an annuity because this could include holding individual bonds to maturity where you are contractually protected to receive the face value at maturity and coupons along the way. Risk pooling is a way to get additional yield on top of the individual bonds to have something that may be more competitive with the risk premium from the stock market. That is the idea of mortality credits with annuities; some of the premium from those who do not live as long helps to fund payments to those who live longer and then provides that contractual protection. If I am someone who ends up living a very long time in retirement, I know that I do not have to rely on the stock market to fund that. I have risk-pooling mortality credits to help fund that longer retirement for me.

The other primary factor is how much optionality do you want to have? If you prefer optionality, you emphasize flexibility. You want to keep your options open as much as possible. You want to take advantage of new opportunities or make major changes to your planning approach in the future. You do not want to get locked in or committed to anything; you want to keep things open as much as possible.

However, if you have a commitment orientation and can find a strategy that will solve your lifetime income need, you are comfortable committing to it. You may give up some of the flexibility of being able to make changes in the future, but that is okay. You know it is going to solve the problem for you.

With the RISA matrix, we map the probability-based safety first horizontally and the optionality commitment vertically to get four sets of characteristics. If you are in the upper right-hand corner, you are probability-based, have an optionality preference, and so on. The secondary factors are not required. The two primary factors can tell the story, but this can help refine the story about retirement styles.

Secondary factors include:

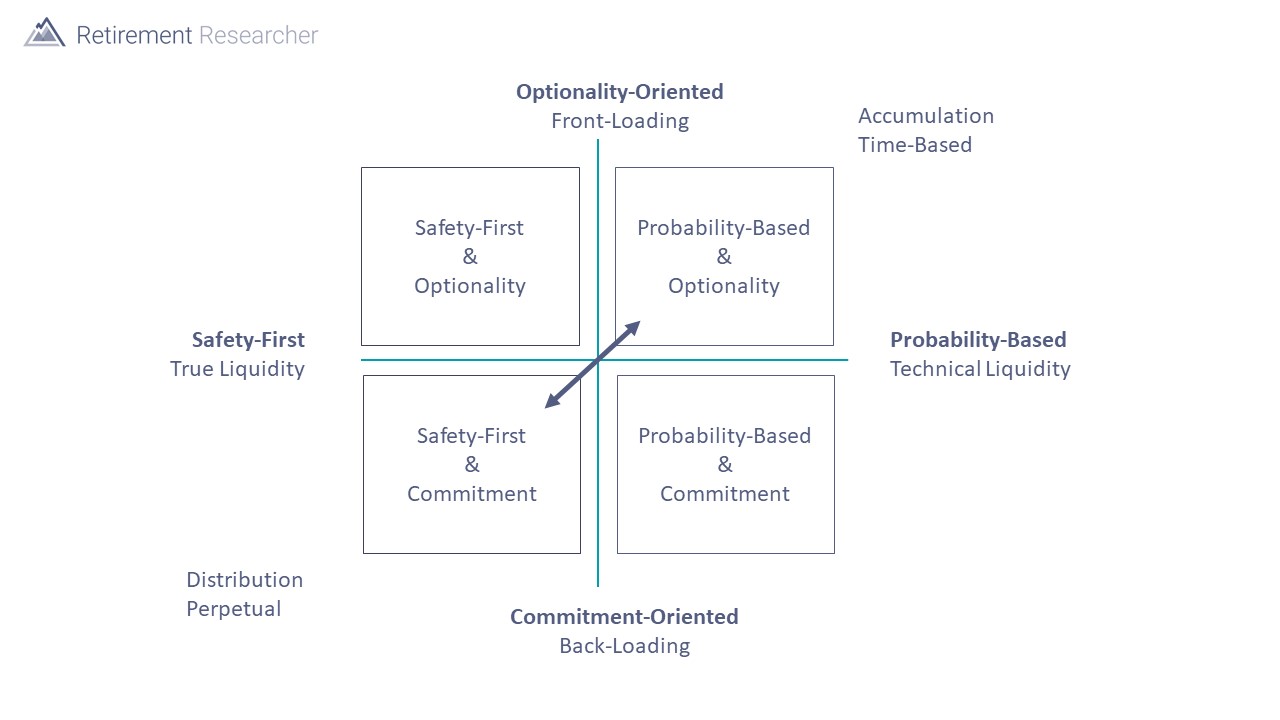

- How do you view your reliable income floor? Do you have a time-based preference or a perpetuity-based preference? If you are time-based, you are not thinking about lifetime income.

- How do you view your reserve assets? Do you have a true liquidity mindset or a technical liquidity mindset? The technical liquidity mindset reflects that you are not earmarking assets for different purposes, and you define liquidity as the technical. A brokerage account is liquid. With true liquidity, you will not count an asset as liquid if it is earmarked for another purpose.

- What’s your mindset about retirement investing? Do you have an accumulation mindset or a distribution mindset? If you have an accumulation mindset, you effectively use the same pre-retirement approach post-retirement. You are emphasizing growth over predictable income. If you have more of a distribution mindset, you become more focused on supporting spending goals and emphasizing predictable income over maximizing growth.

- How do you balance current versus future spending? Do you have a front-loading preference or a back-loading preference? If you have a front-loading preference, you are thinking about spending more today, maximizing the present lifestyle. Someone with a back-loading preference is comfortable sacrificing, not necessarily spending as much today because they have more concern that they might outlive their assets.

Natural Retirement Risk Correlations

Okay, so now we can add those characteristics into the chart and start talking about the natural correlations that happen.

In the upper right-hand quadrant is someone who is probability-based, so they are comfortable relying on the stock market and who has that optionality orientation. They want to preserve as much flexibility as possible. With the secondary characteristics, this is also somebody who also has more of a front-loading preference. They maintain that accumulation mindset. They are not as worried about having a predictable income to the extent they think about flooring. It is time-based, not perpetual. They also have more of a technical liquidity view of how they approach liquidity or total returns investing. That is the idea of building a well-diversified investment portfolio and taking systematic distributions from it throughout retirement. The starting point for all that conversation would be something like the four percent rule. It is how do you draw from an investment portfolio in retirement?

Now, this is one of the natural strategies, and this is where the existing strategies came out in such an interesting way. There tends to be a correlation. We think somewhere around a third of the population may exhibit this preference. We are completing a national study right now to confirm that further. Our existing studies are based on the Retirement Researcher community, not nationally representative of the U.S. population. Still, our preliminary results from doing a national survey at this point confirm that about a third of the population orient toward total return. Academics for a long time have known about this idea of the annuity puzzle, which is they cannot understand why people do not use annuities more. When you see the preferences that align in this total return quadrant, you understand why they do not want annuities. There is nothing here that suggests an annuity would help them. They are comfortable with the stock market. They do not want to commit to a strategy. They are more focused on enjoying their early retirement years. They are not thinking about predictable income, and they have that technical liquidity mindset and a time-based segmentation. They do not need an annuity.

The other natural correlation – that diagonal arrow is about moving from total returns in the upper right to income protection in the lower left – is the world of the simple income floor. These are people who value safety first, so they want contractual protections. They are comfortable committing to a strategy. They think in terms of a true liquidity mindset; they think in terms of distribution. They are focused on predictable income. They are thinking more about a perpetual income floor, not a time-based income floor. They also have a back-loading preference. They are more worried about protecting their future self and not having a significant cut later in retirement. These are the characteristics of using annuities to build a reliable income floor to meet your longevity expenses. Then you can invest on top of that for other discretionary types of goals. They do not want to be exposed to stock market risk to cover their basic retirement expenses. This is also a natural correlation because safety first correlates with a commitment orientation.

The other two strategies are less natural correlations, which also explains their evolution as more of a behavioral approach. This came up in a conversation I read recently on a discussion board, saying people need time segmentation because they are not comfortable with the total return strategy, and it is behavioral. They will panic and sell all their stocks after a market downturn, whereas time segmentation helps them stay the course of their strategy. Well, time segmentation people have inconsistent preferences. They want contractual protections, but they also want optionality, which are not natural correlations. If you sign a contract, it is hard to have options. So, time segmentation evolved to try to facilitate these preferences. You have the contractual protections by holding individual bonds to cover upcoming short-term expenses, and that is where you are getting that safety first feeling. But at the same time, you are maintaining optionality because you then have this growth portfolio. Your investments are meant to cover long-term expenses. You are relying on the idea of stocks for the long run. If I can leave my stocks alone for a few years, any sort of downturn should recover before I am forced to tap into those stocks. This is a behavioral story of how that can help people behaviorally stay the course. Not everyone, but if they have this type of time segmentation preference, they are also thinking more in terms of true liquidity and front-loading, so they are less concerned about outliving their money. This is what time segmentation is.

The other behavioral strategy is risk wrap. We have seen the evolution of deferred annuities with living benefits. People didn’t always want to commit to annuitizing a contract and losing that contract’s liquidity and upside potential. We see with risk wrap that these are individuals who are probability-based. They are comfortable relying on the market, but somehow, they do not 100 percent want to rely on it, so they have other preferences. They are also comfortable committing to a strategy. They do not need to have full optionality. They do also have this back-loading preference. They are worried about outliving their money more than a total return person. They also have a technical liquidity mindset, the same story as the liquidity of a deferred annuity. It is the same idea. This contract may be technically liquid, just like a brokerage account, but if you spend that money on something else, you will reduce the guarantee you receive. But you think more in terms of that technical liquidity.

About a third of the population does exhibit total return preferences. About a third are income protection. About a sixth of the population is time segmentation, and about a sixth of the population is risk wrap. After taking this questionnaire, individuals now have this starting point for a conversation about which strategy resonates with their preferences. We can help people identify where to have that starting conversation.

Key Takeaways

There are multiple viable approaches for retirement income. Total returns, time segmentation, income protection, and risk wrap are all viable strategies. It is just helping people understand when a particular strategy may resonate with them. The right approach for someone depends on their style.

A fundamental premise here is that all these strategies have good points, and it is then just a matter of finding the right approach for someone based on their style. These RISA factors can help identify a starting point for that strategy discussion. It is important for advisors to understand their own personal style, how it may impact their advice, and how to recognize whether their firm offerings align with the client’s style. Do they understand that the client might have a different style than what the firm can provide? How are they working with that? Are they pigeonholing everyone into a total return investing strategy when it may only be that that type of approach will resonate with only about a third of the population?

My newest book was published in September 2021, if anyone is interested. (Retirement Planning Guidebook: Navigating the Important Decisions for Retirement Success.)

The first chapter does go into more detail about this retirement income style awareness, including a link if you would like to take the RISA for yourself.