So, I really hope you’ll leave today being able to spot issues for your clients, avoid common planning mistakes, and identify potential solutions so that they’re better served.

The Basic Definition of Elder Law

Elder law is a legal practice that really places an emphasis on issues that affect the growing aging population. We break that out into four major categories.

- The first is basic estate planning with the use of wills, revocable trusts, powers of attorney, advanced healthcare directives, and asset protection planning for seniors. (Laws in the federal estate tax world have changed and now a married couple can leave $11 million or more at their death free of tax, so there’s not as much of a need any longer to do a lot of tax avoidance planning.)

- Adult guardianships, or conservatorships, for an incompetent adult who does not have a power of attorney in place and is not able to make his or her own legal and financial, or maybe even medical, decisions.

- Asset protection planning is where we are looking at legal and ethical ways to shelter a person’s savings. We necessarily don’t save everything, but if we do pre-planning, we can save a bundle. We can also do call “crisis planning,” where we can still shelter between 50 and 60 percent of the remaining assets at the last minute.

- Obtaining eligibility for government long-term care benefits such as Medicaid and/or Veterans Pension with Aid and Attendance.

What is Medicaid?

I see a lot of confusion about the difference between Medicare and Medicaid, I think mostly because the two names are so similar. The easiest way, I think, to remember the difference is Medicaid has “aid” at the end. It is a needs-based government benefit, or aide. It’s assistance that a person must qualify for, whereas Medicare is health insurance for a person who is age 65 or older, who has worked, and who has paid into the system. Medicare is a health insurance benefit that anyone can qualify for, regardless of need, so they can have an unlimited amount of wealth or income and still qualify for health insurance.

The federal government and each individual state share the cost of Medicaid. The states are required to comply with federal requirements to receive the money from the federal government. Every state can do it differently; if the state isn’t any more restrictive than what the federal rules allow, then the state is in compliance with the federal framework.

One of the major changes that occurred in 2006 was that the look-back period changed from three years to five years, meaning that any transfers made out of the applicant’s name within five years of applying for Medicaid had to be disclosed to Medicaid.

A few relevant resources are “The Program Operations Manual System”, often referred to as POMS, and is where the Social Security Administration looks at their policies and procedures. So, if a person is employed by Social Security, they turn to this and look at how the federal regulations are really interpreted. There is also the State Medicaid Manual, which is a federal resource that can be found on the Centers for Medicare & Medicaid Services website.

Payment Options for Long Term Care Costs

If a person needs extended long-term care that costs $100,000 a year, how are they going to pay for it? The first option that we always consider is Medicare. Medicare is interesting because it is a federal program. It pays for doctors’ visits, it can pay for prescriptions, and it can pay for hospitalizations, but Medicare will only pay for up to 100 days of care received in a skilled nursing facility.

Once someone no longer needs hospital care, they’re discharged to a long-term care facility for rehab. The Medicare program only covers, at full pay, the first 20 days of that rehabilitation in the skilled facility. Days 21 to 100 are paid partially by Medicare, and then, if there’s any supplemental insurance, the supplemental health insurance picks up the rest. After 100 days, if the person still needs rehabilitative care and cannot go home because it’s not safe or the care in the home is not going to be sufficient for what they need, Medicare stops.

The next payment option is long-term care insurance. If a client has long-term care insurance, it’s a great contributor toward the cost of long-term care. However, a lot of my clients don’t have long-term care insurance, and it may be because it’s very expensive and they don’t think that they can afford it. Or it may be because they can’t qualify for it due to a previous health concern or diagnosis.

The daily benefit of long-term care insurance generally is still insufficient to pay for the daily rate to the nursing home. A long-term care insurance contract might provide $100 of daily benefit. If the cost of care is $300, there’s still a $200 daily shortfall, and that multiplied by months and then years is a staggering figure.

Next, we look at whether there are other sources of income which can be used to help pay for the care, such as Social Security, pensions, alimony, and required minimum distributions. However, in a lot of cases, because the cost of care is so high, long-term care insurance and other sources of income are still insufficient to pay that nursing home bill. They might then start liquidating assets and privately paying. Some people choose to do this because they don’t know of other options or because they don’t want to engage in asset protection planning for one reason or another.

The final payment option is public benefit programs. Long-term care Medicaid and/or VA Pension with Aid and Attendance is often what we are looking for. Is there a way to do legal and ethical asset protection planning to qualify an applicant for Medicaid and/or VA? By adding in those additional benefits, we can potentially shelter and protect some of the assets that are left.

How Do You Qualify for Medicaid?

Medicaid has a three-part test. A person is not eligible for Medicaid unless or until they have satisfied all three branches of this test:

- qualify medically,

- qualify under the income part of the test, and

- qualify under the asset and resource part of the test.

If a person is sitting in our office, they’re here because they have a loved one who needs care; they’re not sitting here because they just want to be admitted to a nursing home. So the medical piece of the test is not something we spend a lot of time on because all applicants who apply for Medicaid must complete a pre-admission evaluation, which is a form submitted in order to start the Medicaid process. They have to be medically eligible.

Where we spend our time in the Medicaid context as elder law attorneys is in the income and resource parts of the test. Let’s talk about the income test first. Delaware is known as an “income cap” state. There are 24 income cap states, so nearly half the country has this same rule. The other half of the country does not have an income cap, and when there’s no income cap, there is no need to satisfy any type of income test. When there’s no income cap, the person is eligible under the income rules.

When you have a married couple and only one spouse needs care, there are rules in terms of income for the well-spouse who is still living in the community, and then for the ill spouse who is receiving care in a nursing home. Generally, there’s something under the federal rules called the “spousal impoverishment” rules, and these rules are designed to prevent the well-spouse from becoming poor, destitute, and impoverished.

One of the spousal impoverishment rules says this: The well-spouse is entitled to retain all of her own monthly income. So, if a well-spouse living in the community receives Social Security, receives her pension, and maybe receives alimony from a former marriage, all of those sources of income are retained by the well-spouse. She is under no legal obligation to contribute any of her monthly income toward her ill spouse’s cost of care.

There is a rule called the Minimum Monthly Maintenance Needs Allowance, which says the well-spouse could be entitled to a portion of her ill spouse’s income if her own income does not equal $2,002.50 (2016). If the well-spouse only has a few hundred dollars coming in from Social Security, even if her spouse is in a nursing home, she would be able to keep enough of his income to put her at $2,002.50 to ensure that she can continue to live in the community, pay her house-related bills, pay for her gas, and pay for her normal, everyday living expenses.

The Medicaid Asset or Resource Test

The third part of the Medicaid test is the asset or the resource part of the test. These rules are so strict, and most, if not all, of our clients have more than they’re allowed to under the resource rules. This is where we put our planning hat on to look at what planning opportunities may be available to strategically, legally, and ethically reduce a person’s assets and qualify them for public benefits.

The strict resource limit, under the Medicaid rules, is $2,000, so a single applicant can have no more than $2,000 in assets to qualify for Medicaid. What is counted as a resource? Medicaid says that it’s pretty much anything the applicant can put his hands on. If the applicant has the right authority or power to liquidate, that is an available resource under the Medicaid rules. Life insurance, for instance, which has cash value, is an available resource because it could be liquidated for its cash value. We would forego the death benefit, and we would have to use that cash value and spend that down, paying for long-term care.

There are some exclusions. The first exclusion is the person’s residence, but in a single-person case, the residence can only be excluded if one of two things occurs. The first is if the applicant is still residing in the home and receiving home-based services under the Medicaid program. Then, the house is protected, because the resident is the applicant and is going to continue to live there.

The second case where the residence can be excluded is if a single applicant is in a nursing home but signs a statement that says he intends to return home. Even if everybody knows that there is no way that he’s going to be able to go home, if he is able to sign a statement that says he wants to return home and intends to do so if he ever could, that’s enough to delay the house from being considered an available asset.

However, be aware of what’s called “estate recovery.” Estate recovery is the branch of the Medicaid department that has the right to place a lien against the residence or to file a claim against the decedent’s estate after the applicant has passed away, requiring the residence be sold and those proceeds used to satisfy the lien or satisfy the claim against the estate.

A vehicle is excluded. A person’s household goods and personal effects are always excluded. Life insurance with no cash-surrender value is off the table, and any prepaid irrevocable funeral arrangements are also off the table. Everything else is available and would have to first be reduced to $2,000 before a person could qualify for Medicaid.

Then there are married couple asset rules. Say you have a family that has done absolutely no planning. One spouse needs nursing home care; the other spouse is well and still able to live at home. Which assets are excluded? The house is excluded, in this case, because the well-spouse lives there. Again, one vehicle, household goods, and personal effects are protected. Life insurance, again, with no cash value is excluded, and prepaid irrevocable funeral arrangements are excluded.

So, if you’re looking at a married couple’s assets, and you take everything out of the excluded section and set it aside, everything else is what’s potentially available to pay for the care of the ill spouse: normal, everyday bank accounts; stocks, bonds, and CDs; life insurance with cash value; and it’s the retirement accounts of the ill spouse. We look at all of that together as part of a common pot, and the general rule is this: We split that pot, and we allocate half to the wife and half to the ill spouse.

If she is allocated half of that pot, she’s entitled to keep that, but if her half is higher than $119,220, she is capped at only keeping $119,220. Everything else gets allocated to the ill spouse and must be spent down to $2,000 before he can become eligible for Medicaid. There’s also a minimum there, so if what’s on the table is less, essentially, than $25,000, then the well-spouse gets to keep it all. That happens very, very rarely, but it does happen in some cases.

Medicaid Transfer-Penalty Rules

I mentioned earlier that there’s a five-year lookback period, but all that means is that if there have been any transfers made within five years of applying for Medicaid, they must be disclosed. The amount of those disclosed transfers then gets put into a calculation.

There is a current divestment penalty divisor of $301 a day, or $9,156 a month. In other words, if we apply for Medicaid and we disclose that we gifted, in the last five years, $9,156, that’s going to result in one month of ineligibility. If we disclose $18,000 had been gifted, that’s two months of ineligibility, and so on. If a penalty period is imposed, we must figure out how we’re going to pay for the care that’s needed during that penalty period. The penalty period cannot begin until the applicant is otherwise eligible for Medicaid. So, the assets have to be reduced to $2,000 before the 1-, 2-, 3-, 15-, 24-month penalty period would ever even start. Elder law attorneys help get a person otherwise eligible and create a plan to ensure that the applicant is going to have the ability to privately pay during the penalty period.

Medicaid has a presumption. It’s a rebuttable presumption, but they presume that any gifts made within five years were done for the purposes of qualifying for Medicaid. That includes charitable gifting. It includes annual exclusion gifting, so right now, that’s $14,000 a year that can be given away. That’s a tax rule. Under the Medicaid regulations, Dollar 1 of that would count against a potential penalty period.

There are some exceptions: Transfers between spouses don’t result in a penalty period, so we could transfer money, assets, or real estate between spouses all day long, and no penalty would be imposed. Transfers can be made to blind or disabled children without penalty. A house can actually be transferred to a caregiver child who has cohabitated and lived in the home for two years before the applicant needs long-term care, without penalty.

This doesn’t come up a lot, but if there are cohabitating siblings, and the applicant sibling has an equity interest in the house, and they’ve been living together for one year, then the house can be transferred, essentially, to the well-sibling, and it would not result in a penalty.

Veterans’ Benefits and Long-Term Care

Veterans’ benefits, just as a reminder, are another type of benefit that can be used to help pay for long-term care for someone who is facing a large bill. The Department of Veterans Affairs was established in 1930.

Here’s the chain of command: Congress passes a law; it’s then recorded in the United States Code, but then it’s enforced by new regulations that get published in the Code of Federal Regulations, or the CFR. If you’re helping someone qualify for Veterans Benefits, you must be accredited.

There are a lot of different types of veterans’ benefits. The first type I will mention is a disability benefit. It’s often called “service-connected disability” or “disability compensation.” This type of benefit is for someone who was injured during active duty.

Where I spend most of my time is dealing with a benefit that’s called the Pension benefit program under the VA is, which is essentially the VA’s Medicaid program. It’s a means-tested disability benefit. The specific name is Service Pension, for a veteran who needs the financial assistance to pay for long-term care, and then Death Pension, which is for the surviving spouse of a veteran who needs that same financial assistance to pay for long-term care.

A married veteran who needs the aid and attendance of another could potentially receive $2,127 of additional monthly income. That’s huge for somebody who is facing an outrageous nursing home bill each month, so we look at whether a person may or may not be eligible for veterans’ benefits.

Just like Medicaid, there’s a three-part test to be eligible. There’s a military test, a medical test, and a financial test, and a claimant must qualify under all three parts in order to be eligible for VA Pension.

- Military test. The service requirements are this: A person must have served in active military, naval, or air service. You may be thinking, “Well, what about the Coast Guard or the National Guard?” Those folks are only included in this if they were activated during wartime, so, in most cases, National Guard and Coast Guard are not included. If a person is a veteran who served in active duty, that active duty must have been for a continuous 90 days, and at least one of those days has to have been during a declared period of war. The veteran also must have been discharged or released under conditions other than dishonorable. If it’s a surviving spouse who was not a veteran – the deceased person was the veteran – we’re still looking at the deceased veteran’s service to determine whether that surviving spouse can get her foot in the door with the VA.

Reserve status is not sufficient. My own grandfather was in Reserve status during a declared period of war, so he would not be eligible.

- Medical test. For Basic Pension, all you must prove is that the claimant’s over 65. If the claimant’s not over 65, then we must prove that the claimant is permanently and totally disabled. Permanent and total disability is going to mean the Social Security Administration has determined disability: there’s been a Parkinson’s diagnosis; the person is a nursing home resident. All those things would show permanent and total disability. Basic Pension is the lowest level of Pension.

Most of our clients come to us unable to perform two or more of their activities of daily living. For VA purposes, that means dressing or undressing, keeping clean and presentable, and feeding. If a person is blind, if a person is a nursing home resident or assisted living resident, or is unable to perform two or more activities of daily living, then they would qualify for that increased aid and attendance benefit.

- Financial rules. Under the financial rules, there is an income and asset test. You probably expected that just like under the Medicaid rules. The income rules under the VA can get a little tricky.

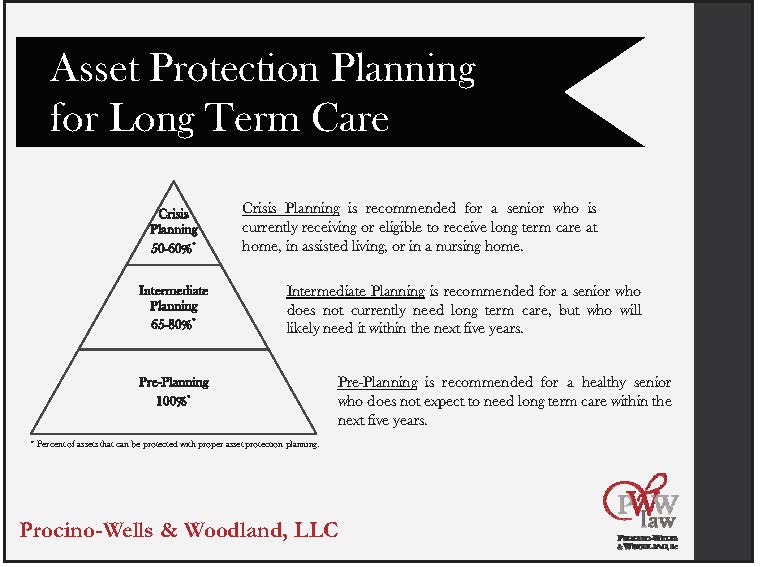

Three Levels of Elder Law Planning

We use this pyramid concept to talk about the options available to folks. The bottom of the pyramid, the fattest part of the pyramid, is where we put pre-planning. Pre-planning is recommended for that healthy senior when it’s not foreseeable that they’ll need any type of long-term care in the next five years. In the pre-planning context, assets that we set aside are protected at 100 percent, as long as five years or more go by.

The middle part of the pyramid is the intermediate planning context. Intermediate planning is recommended for a senior who does not currently need long-term care, but who will likely need care within the next five years. In the intermediate planning context, there’s planning that can be done so that 65 to 80 percent of the assets are still protected.

Crisis planning is that last-minute planning for a senior who is currently receiving, or eligible to receive, long-term care at home, in assisted living, or in a nursing home. With crisis planning – last-minute planning – 50 to 60 percent of the remaining assets can still be protected.

Michele, my business partner, recently had a case where a gentleman had been receiving care in a nursing home for ten years. He had spent over $1 million paying for his long-term care before his family ever came to us. When his family came to us, they still had a few hundred thousand dollars left. It wasn’t too late to engage in planning to protect about $150,000 of what was remaining. At least, we could create a little nest egg. We could protect him from being completely broke before he went on Medicaid, and then, ultimately, to leave a legacy to his family of something.

That’s a pretty extreme case, but it’s just important to know that crisis planning means this: It is never, ever too late to do planning, as long as the person needing care still has assets remaining.

The Goals of Asset Protection and Long-Term Care Planning

The goals of asset protection are, first and foremost, to ensure that there’s a payment for the needed services to make sure that a person doesn’t outlive their savings. The worst possible thing that could happen is for a person to need long-term care for so long that they blow through all of their life savings, have nothing left, and qualify for Medicaid because there is no nest egg available to supplement the things that Medicaid may or may not provide.

If a person completely runs out of money, is receiving care in a nursing home, and is on Medicaid because they’re poor, needs dentures, hearing aids, eyeglasses, a computer, TV, or a recliner, that resident is going to go without because he doesn’t have a nest egg that could be used for those things, or his kids and other family members are going to have to chip in their own money to pay for those.

So, the main goal of asset protection planning is to set aside some of the applicant’s own money that can be used for the applicant.

The second part of this article on Elder Law Basics will appear in the next issue of Retirement InSight and Trends, and will cover strategies to consider for ensuring there are income and assets to pay for needed services so a person doesn’t outlive their savings.