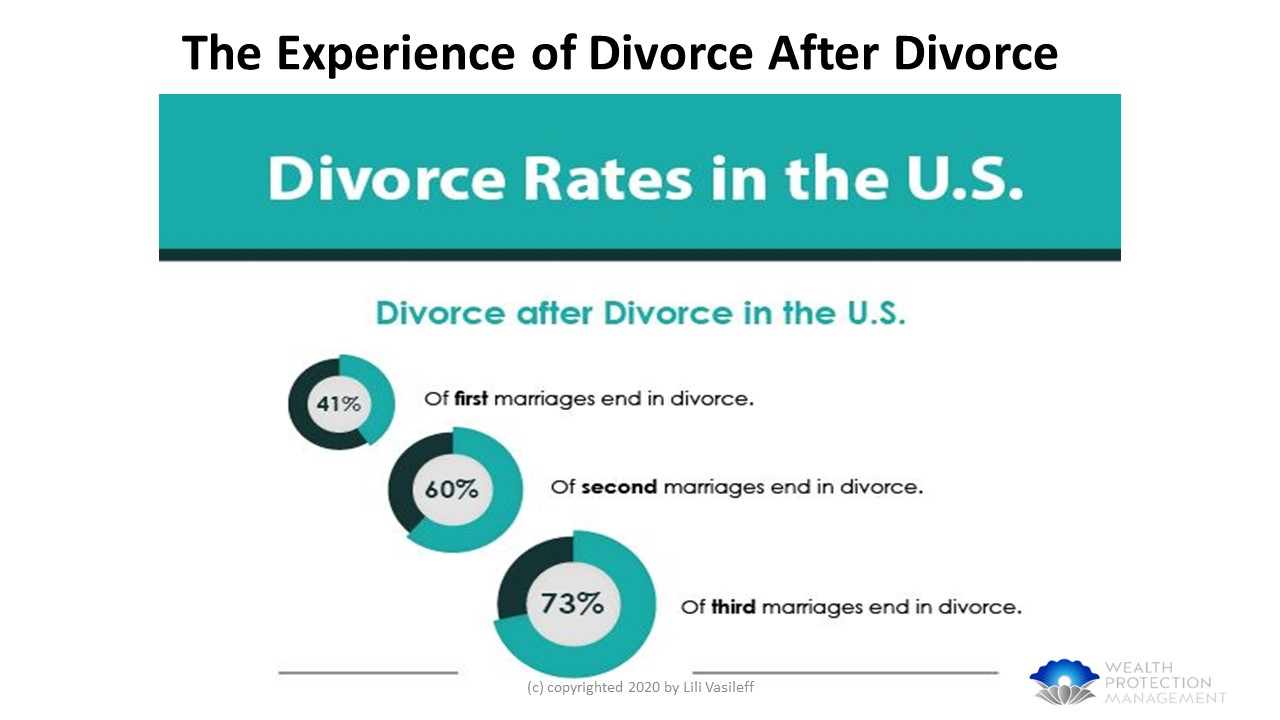

There is a post-divorce echo effect. The remarriage statistics are challenging, which means that those individuals that come out of a divorce and then sometime down the road fall in love all over again and remarry, God bless them for being optimists, much higher and more significant divorce rate than first-timers.

In fact, it’s 60 percent for second remarriages and for 3rd or 4th marriages, 73 percent. Why? There are many theories about it: perhaps there’s just less glue holding you together; you don’t have children together necessarily; maybe you have outside influences that are negative on a remarriage, meaning adult children or elder parents that you’ve been caregiving and distract you from your new primary spouse.

That doesn’t make it any easier for us as advisors when we have clients looking forward to a new life – possibly remarrying – because now we need to focus on these risks as well.

Late-life divorce for adults who are over the age of 50 has an almost double rate of divorce than any other age population. There is an increase in the divorce of first-time marriages, with more than 50 percent occurring for marriages over 20 years. However, this varies given different demographics, different economics, and different social factors. This statistic has been reinforced by many different surveys and by the Bureau of Labor Statistics. At some point, there will be a confluence of events that we need to address with clients going through a divorce, addressing finite resources.

What do Boomers want in their marriage in retirement?

What do boomers want? It’s nothing different than any other person going through a divorce. They want to be happier; they want to be more fulfilled; they want to have more opportunities to do what they think they’re owed or entitled to. Remember, the boomer generation is the “me generation,” “It’s my time, my turn.” These individuals have explored different opportunities since the sixties, or so that made them feel special. It’s not a dissatisfaction of an empty nester or a career change, or a life transition that seems different; it’s a general dissatisfaction with their marriage in its entirety.

You might call it the effect of the baby boom, but this was also the first generation that had women at work. This may be a very strong factor in how boomers now consider divorce; these were the women that pushed the boundaries to be viewed with parity in the workforce, the feminists. These are anti-establishment people who came out and worked hard to change the rules around what they wanted to do.

A key factor is an idea that this second chapter in their lives, meaning retirement or later years after they’ve worked so hard to accumulate what they have, should be what they want. To a large degree, there’s a diminished stigma associated with divorce. There’s also a financial opportunity because of their accumulated resources or work history that they may be able to be independent post-divorce. It stands to reason that if these people live longer, they have more years to think about becoming divorced.

What does it then mean if they decide to contemplate divorce and then move forward with this? What factors are important for us to know as advisors about their concerns, anxieties, and challenges are going to be? I remember a client in her late 50s who shared with me the following information. She said, “You know, I have never lived on my own. I graduated from college, became married, and worked for a little bit. Then I became a mother. Then I took care of my older parents. And then, one day, my husband walked in and said he wanted a divorce. And I went through this spectrum of different reactions; I’m angry because I’m out of control. It wasn’t within my doing. I also feel as if I’ve lost an entire identity. I used to be a married person. What am I now? Now I have newfound freedom. But what do I do with it? If I drive to the end of the earth, will anybody even care?”

It was a very interesting awakening that made me realize that there’s a mix of emotions that go through these individuals, whether they want it to be the divorcing person or are getting divorced in the sense that nothing is clear. They’re overwhelmed with many emotions. At the same time, they must make critical financial decisions.

The financial concerns are the following:

- Will there be sufficient income by dividing one household’s income into two?

- How much can they spend, and how do they project their spending going forward? They probably need to downsize their home.

- There’s always anxiety about when and if they have the financial wherewithal to plan for retirement at a certain age. What happens when they retire and no longer have earned income? Are they going to outlive their assets?

- There is apprehension about being financially independent when they’ve had no experience being so.

Many of these concerns are not unique to divorcing couples. Still, they’re heightened by the scarcity of resources for those individuals who were not necessarily experiencing scarce resources during a marriage.

What makes late-life divorce different?

If you are in your late 50s, you have a finite number of years left until your full retirement age. There’s a shorter time horizon, therefore, to replenish any savings that you’ve been accumulating over your entire career. It’s also more difficult to be able to plan or execute income that is higher than what you’ve been earning to date. You’re probably in your peak earning capacity already if you’re in the workforce, so there’s minimal upside opportunity to increase earned income. It’s also difficult for many individuals who have been out of the workforce for several years to go back and find any meaningful employment, even sufficient enough to cover health insurance.

The inexperience of those individuals who have managed day-to-day bill pay and day-to-day finances but not longer-term investments is a real detriment. Many of my female clients who have been out of the workforce feel they don’t know what to do for longer-term planning, whom to trust, or how to evaluate what their spouse has been doing with it. It’s a learning curve that they have to do unwillingly. Even if you are the person who initiated the divorce, there’s always an element of psychological or emotional depression in the closure of one chapter of your life and moving on to another one whether you want to or not. The transition piece is often sad, and we try as professionals to help individuals and couples acknowledge that it’s just the closure and the beginning of something new.

These are successful individuals at this stage in life; they’ve had good careers and home life; they’ve raised their children, they’ve been successful parents, and they face demanding jobs of up to 60, 80 hours a week. College tuition bills collectively cost more than what their house is worth. They have financial responsibility for caregiving for their elderly parents. Some of their adult children, sometimes whom we call boomerang children, are back home, and they’re unable to find a decent-paying job. Guess what? They’re spending down their parents’ assets. Some adult children conflict with your clients who may own family-owned businesses. Maybe they want to avoid going in and becoming a successor to that business. Maybe they don’t care about it. Maybe they’ve been doing nothing else to plan for their career.

Then, of course, there are blended family issues due to remarriage. There are also skyrocketing health insurance premiums and medical issues. Clients often want to say, “Can I now force my spouse to buy me long-term care insurance if I’m going to be divorced?” It’s easier to say what might be affordable when it has not been provided during the marriage.

Women are especially vulnerable for a few different reasons. Money ranks as the number one worry for women during a divorce, and it even tops their concerns for their children. “Will I have enough to live? Am I at risk that my spouse might just disappear or not?” The post-divorce decline in income hits women especially hard; women experience a 45 percent decline in their standard of living.

Nearly a third of all divorced women feel that the current quality of their financial lives post-divorce is worse than they ever expected. These are the same individuals who initiated the divorce. Gray divorced women have relatively low Social Security benefits and relatively high poverty rates. In a Nationwide survey, gray divorced women found that 62 percent of divorced women expect Social Security benefits to be their primary source of income.

Women who have not been in the workforce can choose to go on their divorced husbands’ record of Social Security or go on their own. If they meet the criteria and have been married longer than ten years, are at least 62 years old, have been divorced for two years, and have not remarried, they may be entitled to 50 percent of their ex-spouse’s retirement benefits. The maximum annual benefit was $45,480 in 2020, so cut it in half, and these women are living on $23,000 a year.

What should advisors be aware of with gray divorce and retirement?

Gray divorce hits every part of a person’s life. When you’re younger, you have more time to recoup, and you have more opportunity that lies ahead. When you’re on the cusp of retirement, you’re looking at the downward slope of what you’ve achieved and accumulated as your peak. You have competing demands; you’ve got conflicting goals; you’ve got limited resources stretched now between two households.

The strategy for working effectively with boomers is to involve them and help them find solutions. Let them brainstorm with you. They want to be a part of this, even though they may be kicking and screaming. Divorce is about making lifestyle changes; we must work with those clients to help them understand where they might be headed.

Divorcing on the cusp of retirement typically takes place in peak earning years, with a lifestyle reflecting wealth accumulation. It’s a powerful reckoning for clients to realize that their peak earnings funding a household’s mature lifestyle may not last longer than just a few years from retirement. Here’s the kicker: it might be insufficient to support two households at a comparable lifestyle standard post-divorce. This is the most challenging thing to get across to clients who feel guaranteed and entitled that their lifestyle should have no changes.

We must focus on all these areas at the same time with our divorcing clients because they all impact one another. There are work-life span considerations, retirement planning, estate planning, remarriage considerations, and Social Security claiming strategies. This is what makes Gray Divorce so challenging for advisors.

You’ve got different things happening at different times. Still, they all are interwoven to bring you to the point of ending a transition and starting a new life and hoping that your client has enough confidence and trust in you as their advisor that they can start listening and digesting the advice they need to hear.

What do you need to know? How does this impact your practice? Recognize that late-life divorce is the perfect storm that impacts your clients. Seize the opportunity to talk with them, discuss specific issues that should be brought up during the divorce process with their attorneys, and take advantage of certain financial strategies that are unique only to divorce.

So, let’s talk about what happens in late-life divorce. Retirement assets are usually divided down the middle in a long-term marriage, regardless of who’s earned or saved it. That’s the first slap in the face for the wage earner. The second one is that, generally speaking, the impact of taxes can be significant and should be addressed during the divorce. And I don’t mean transferring assets from one spouse to the other because those are non-taxable transfers. I mean, getting an asset and having it in your hand, signing the agreement, and then three minutes later liquidating that asset and not realizing it has a tax impact. That must be clear regarding the after-tax impact of dividing assets equally.

Some states have spousal support formulas; some do not. The trend is for less spousal support and fewer years of spousal support, which doesn’t make these individuals very happy. If you say, “I’ve been married for 25 years, and maybe I’m looking at five years of spousal support,” it seems very inequitable.

There are also issues of separate property, marital property, and valuing the family-owned business.

How are boomers prepared for divorce?

We are not a country of good savers, and many people need detailed financial plans. The general behavior of people could be saving better. According to the Government Accountability Office (GAO), one-third of households age 55 and older have neither a retirement account nor a pension.

Nearly 40 percent of married couples interviewed by NerdWallet just last year said that one partner was saving for retirement; one in five had yet to learn the retirement amount. A third rarely discuss personal finances with family members, and fewer than half make financial decisions in partnership with their spouse. We’ve got a dire situation of lack of communication in a marriage for financial planning, especially toward retirement.

Women, in general, feel much less comfortable than men planning for retirement, and yet only about 6 percent seek out professional help. Forty percent of couples disagree on when to retire and what their lifestyle will be during retirement together. These things bring the risk of divorce to a head; this is the key factor. So, when you add divorce to the mix of mismatched expectations for retirement years, lack of knowledge about retirement savings, what’s been happening, or how you’re going to live during retirement years, a lack of communication with your spouse or trust or even reliance on them for financial planning guidance, and maybe there’s even a potential age disparity between the two spouses, well, guess what? It’s just a ticking time bomb.

And we know that there’s one thing that lies ahead: in every case I work with, there is sticker shock. People who walk through this process have no idea what has been saved, what they need, and what they can live on. Compared to singles, married people accumulate almost four times more savings and assets, and those who are divorced have assets 77 percent less than singles.

What happens if you do work past retirement age? A significant percentage of workers say that they plan to work past 70. But guess what? A growing number of seniors are declining or unable to retire because of financial needs. This trend is up 22 percent since 1994, which runs parallel to the divorce rate that has increased for late-life individuals. Health problems and layoffs, COVID-19, the need to take care of a loved one, discrimination, and the scarcity of jobs have diminished this opportunity even more for seniors who must work past normal retirement age.

How does working past the normal retirement age affect an alimony obligation? You would think that if you must fulfill an obligation and you have the reason and recourse to work, that would be a good thing. Some states are trying to legally terminate an alimony obligation past an individual’s full normal retirement age. The downside risk of working past retirement age if you are divorced and have an outstanding alimony obligation is that it’s very tough to go before a judge and request a modification of that alimony if you are working and have no significant change in your financial circumstances other than you want to reduce your alimony obligation. On the flip side, for the alimony recipient, if you file for Social Security while collecting alimony, your income may be subject to taxes.

If you’re receiving Social Security benefits on your ex-spouse’s record and you remarry, there’s a suspension of your Social Security benefits for a whole year. You then have to apply on your new spouse’s record. The age disparity between the two spouses or a gap between becoming eligible for Medicare and coming off of COBRA can push women into menial part-time jobs in the hopes of purchasing health insurance.

How can advisors identify opportunities to maximize outcomes for late divorce clients?

We have to be realistic about longevity. If our clients are contemplating cohabitation and or remarriage, we also have to be mindful of what they think they want to do about their joined finances in remarriage. Will they be separate? Will they be co-mingled? If they’re co-mingled, are they at risk?

We focus on three key areas: cash flow, retirement assets, and dividing property. We have to plan how to maximize our cash flow from all sources and squeeze it from the assets. We must find out if our clients can continue to work and if there are other opportunities for producing income that has yet to be tapped. We must help them negotiate critical golden assets like annuities and pensions.

We must educate clients about Social Security claiming strategies and the risks of remarriage and working past retirement when receiving alimony. We also need to help our clients plan for health and long-term care insurance.

Cash flow sources for the divorce process.

- Get cash out of a retirement plan penalty-free if it is addressed in a qualified domestic relations order (QDRO) as part of the divorce agreement. You can’t do it after the fact. Pulling cash from one of these plans to give someone emergency funds liquidity to move to a new place or put as a down payment on a home is hugely important, and it could even be used as a buyout of another spouse.

- Divide an annuity. There is a catch with annuities in divorce. Can it be divided and re-issued to ex-spouses? If so, do the terms change? Does it involve a new cost? Is it the same annuity, or is it a lesser-value annuity? Can it be transferred in ownership or converted to a different policy? I have spent hours talking to annuity companies during a divorce because attorneys do not know this, and clients do not know this.

- A reverse mortgage can help a person stay in their home. What more does anyone now want from this pandemic than to stay safely in their home? A reverse mortgage can provide the cash flow for living expenses, and they can meet those, buy out their spouse, or facilitate an asset division. For divorce, this is a very important tool in our toolkit.

- Consider taking out loans from retirement plans or even against the cash value in life insurance. When our clients are going through a divorce, make sure you find out if any loans are outstanding against these assets.

Dividing retirement assets.

- Pay special attention to tracking deferred compensation assets. This can include long-term incentive awards, RS, restricted stock, performance shares, stock options, and deferred voluntary cash bonuses. All of these might not have value today but needs to be tracked to determine whether or not the risk is warranted for a spouse to assume them or if it can be offset with other assets that your client prefers.

- The sequence of spending adds value to income. Only a few clients are well aware of what assets to tap into and when and what the withdrawal sequence can help them manage their taxes and manage and grow their retirement assets while tapping into them. I usually review this briefly because there’s much overload during the divorce process and on the post-divorce side. Still, I point it out as a topic to discuss with their advisors.

- Ensure direct transfer of the retirement accounts from one spouse to the other; anything in between could be deemed distribution and taxed.

- It also helps to know that dividing IRAs does not require a QDRO, although some custodians will require a QDRO to divide an IRA, even though not required.

- While the clients are still married and perhaps in a better position, determine whether or not they should convert certain IRAs to ROTH IRAs and share the tax impact of that version so that one party doesn’t have to bear it alone after the fact.

- Dividing pensions, qualified and non-qualified, knowing the election options and how to designate beneficiaries.

- Is it important that you have the same amount of assets the minute you’re divorced or that you project forward how much you will have in the future if one spouse continues to earn and can replenish those assets while the other doesn’t? Defining goals is also helpful in helping them understand the equitable part of the distribution.

Dividing the property. There are other ways to get cash, right?

What exists that they may be able to benefit from and yet not have to come up with the cash? Sometimes we can squeeze cash from cash that doesn’t exist, dividing properties that are productive in providing benefits to our clients and not using cash, such as reward points, mileage points, cash rewards, cash rebates, timeshare points, HSAs, tax refunds, tax loss carryforwards, depreciation recaptures leases that have been entered into on a long-term basis.

Some states force the decanting of trusts for assets or income and business owners. You should pull in a business valuation expert to get an appraisal of what is the businessperson’s interest versus the value of the asset. This is also one of the most controversial in divorce because there’s a concept called double-dipping. Double-dipping refers to using a business as an asset as well as a source of income. And it’s not well understood by the courts.

It’s very difficult to explain this concept, which is why outside professionals usually come in and do these appraisals. It does cost money, but it alleviates liability on your part and the attorney’s part to have this expert report.

Key Takeaways

As a financial professional, you can clarify many topics that should be of key concern to our clients in late-life divorce. Most importantly, I want you to help your clients avoid having false expectations for divorce. The one derailing myth out there is that everyone will be the same after divorce as they were during the marriage in terms of financial capacity and resources and wherewithal, and that they have an entitlement to that and that the law guarantees it.

And more importantly, you want to ensure your clients do not make ignorant decisions. You’re there as their backstop.

Here is how you educate:

- Cash flow – you want to squeeze every asset, maximize every income source you possibly can, and identify how to replace irreplaceable cash flow and what to do about it.

- Risks – are your clients at risk of underemployment? Maybe no earning potential, early retirement against their will, remarriage by choice, or cohabitation by choice? What about working past retirement age and having illiquid assets at risk that can’t be squeezed for cash flow?

- Retirement assets – can we cherry-pick what we get in the divorce? Sometimes, yes, sometimes no. The more knowledgeable you are, the more prepared you are, the better your chances are. And you need to know what’s required to get those assets at the lowest risk cost possible.

- Social Security – You must help your clients understand Social Security claiming strategies for alimony and working past retirement age.

- Healthcare – if they fell short of health insurance, how will they get that coverage?

- Estate planning – Revisit all their estate plans, beneficiary designations, and POAs. You don’t want your ex-spouse as your POA in a situation, life or death.

With this information, you can help your clients focus better during the process. You’ll give them clear guidance on how to help them implement all of the terms of that divorce agreement and give them some post-divorce financial planning. We are most relevant by playing a critical role in the transition for our clients. We’re going to open a very personal and safe space for them to ask us any question and give them the most information we can to help them keep their financial negotiations on track.