Why focus on widows? I didn’t have any long-term planning knowledge as a young wife, a mother, then a caregiver, and then a widow. What we want to be clear on is that widows are very, very different. When you lose a brother or a sister or a mother or a friend or a child, that type of loss and grief is one thing, but it’s financial when you lose a spouse.

The financial impact is huge. Half of the income is now gone, yet your bills are still there. Here’s one interesting thing that a lot of financial advisors don’t understand. Yes, it is a blessing to receive life insurance funds when a widow. I was well taken care of; my late husband had a pension. But with this money comes a lot of emotions – guilt, sadness, and regret because it came with such a high price.

Why Focus on Widows/Women Now?

You’ve heard about the great wealth transfer with Baby Boomers. Seventy percent of all married Baby Boomers will experience widowhood. These are females. The great wealth transfer is coming, and it’s passing approximately $30 trillion over the next several years. Widows will be first in line, and they also could be dual inheritors from a spouse or a parent. For advisors, this is huge information.

It makes sense to market to widows and women. How many widow clients do you have currently? Maybe a few? How many clients do you have currently? Sadly enough, of your women clients, the data predict that they will be future widows.

You simply cannot ignore the numbers. While researching this topic for several years, one of the things that still stands out to me is that pie chart where 80% of men die married. That is a tough pill to swallow. Many of these widows are not the grandma/granny sitting in a rocking chair knitting and with nine cats. The demographic of widows is much more different.

There are an estimated 258 million widows worldwide, 13.6 million in America. Worldwide, 2,800 a day are widowed, or one million a year. This is sad, sobering, and a subject that some people don’t want to talk about. It seems disrespectful, but the more you know as financial advisors, the more we’ll be ready.

What is the number one rated most stressful life event? Loss of a spouse. There’s more information that this stressful event is most vivid the first year. Who will be there for them? Widows today are younger. The average age is 59, living 15 years on her own. For widows, those 15-plus years will probably be a different financial picture and have different financial goals than what they did before the death of their spouse.

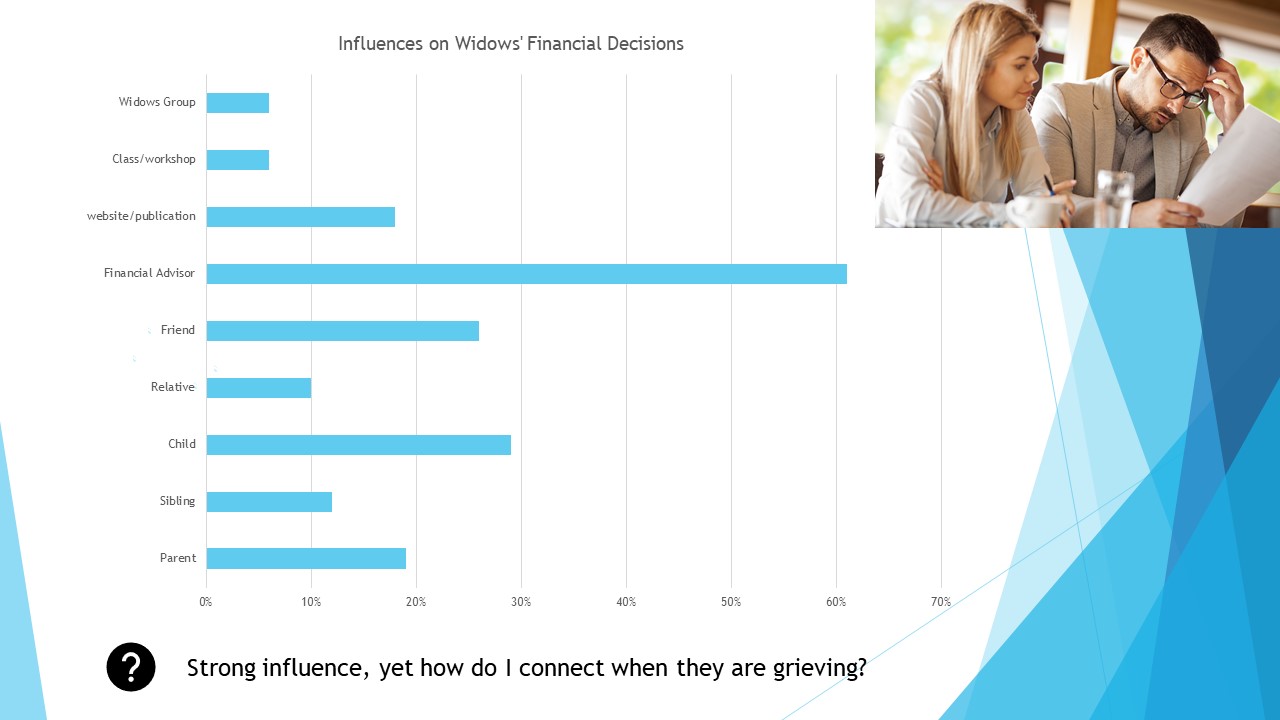

Most widows are educated. They have careers. They’ve overseen their career, raising a family, finances, and budget, but very few of them have had an equal part in the investment planning. They lack confidence in long-term planning. What we want to think about is who influences their money decisions moving forward? They don’t have anybody to bounce those ideas off any longer.

I’ve found this study very insightful. It was based on interviewing widows and how they move forward. Widows were asked if they could respond to one to three of their top influences.

You can see that financial advisors are still most turned to, but you’re going to need a different approach in the future, and that’s grief literacy.

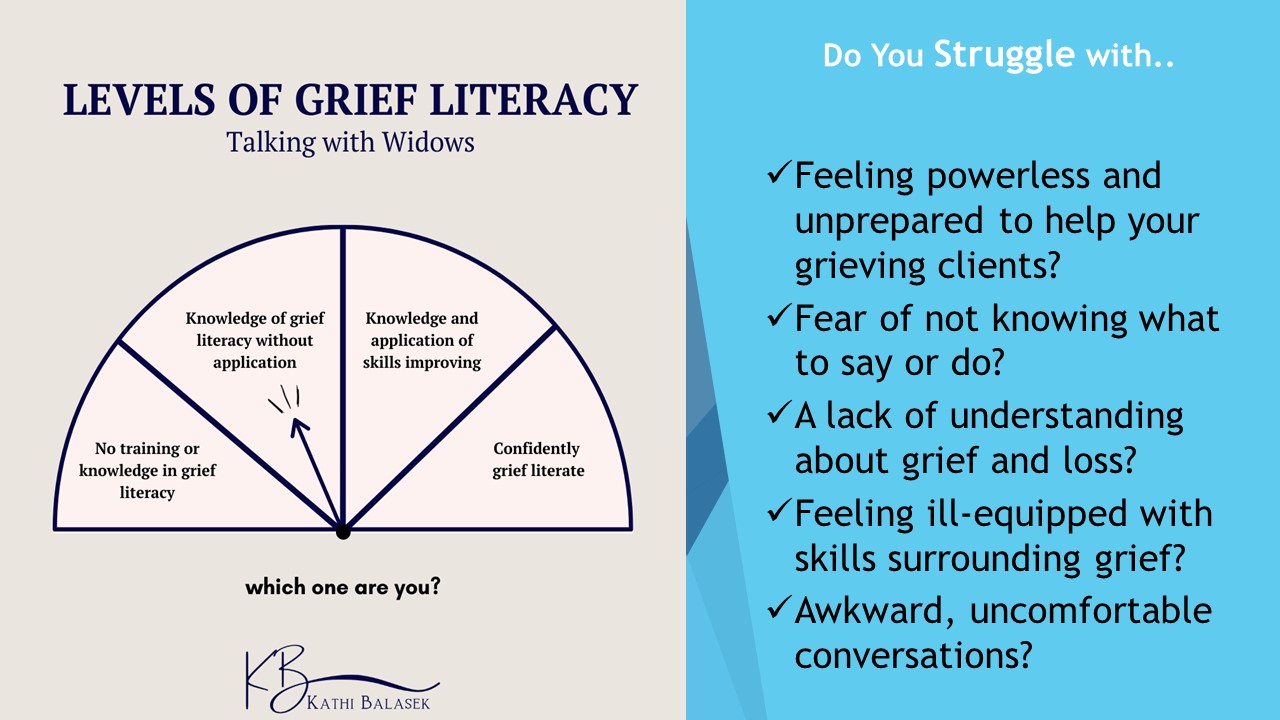

Levels of Grief Literacy

When we think about death, dying, grief, all of those things, our body language changes. We talk in hushed voices. We want to flip that, so ask yourself some of these questions.

These are awkward, uncomfortable conversations. As with anything, it takes practice. It takes rehearsal. We want to get advisors to a point where it’s like the fire drill we all did in school. We practiced the fire drill multiple times, so we know exactly what to do when it happens. We don’t even need to think about it. That’s where grief literacy can help you.

It’s important to know that grief literacy does not fix grief. It doesn’t take it away. It doesn’t ask the bereaved person to move on, let go, or get over it. On the contrary, the absence of grief literacy skills can lead us to cause harm to the very people we serve.

As a lifelong teacher, I’m not here to judge you or your skills. I’m here to help you along. When we think about this, grief literacy, widows, what do widows want from their financial advisors?

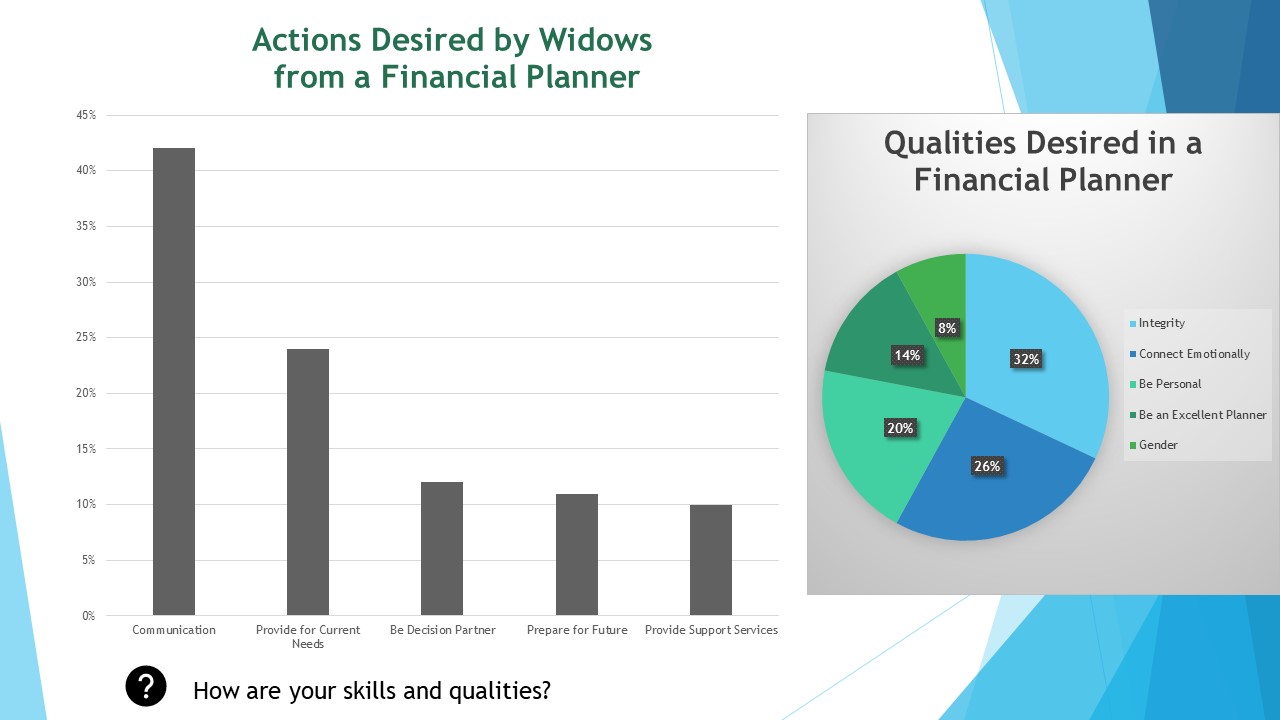

Actions Desired by Widows from Financial Planners

Here are a couple of studies; actions desired by widows from financial planners and qualities desired in a financial planner. The number one action desired by widows of advisors is communication. They want to be able to communicate with you.

I’m sure for many of you who have worked with bereaved clients, you know there are barriers put up before they come in to see you or when they speak with you. For example, assume you’ve bought a 1,000-piece puzzle, and you’ve spilled it all over the carpet. When you’re a widow, you don’t even get to see the picture on the box because you don’t know what the financial picture looks like.

You have so many missing pieces, and you don’t know what the future will be. It is just completely overwhelming, so you desire an advisor who can communicate with you, be a decision partner with you, and walk alongside you as you grow and walk through this grief.

What is relevant and valid in the pie chart is to point out is that gender was of little importance. I think we make many assumptions that the gender of financial advisors in an industry that historically leans male would be more important. Truly, regardless of gender, anybody can be a champion for widows.

C A R E

Gauge your qualities. Where are you? How are your skills and qualities in these areas for widows? This is my primary curriculum.

I’m a teacher, so I love a good acronym, and I also believe in simplifying it and making easy, actionable steps. When we talk about CARE, we mean:

- Communication, what you say

- Action, what you do

- Relationship, what you’ve built, and

- Empower, how you help your bereaved client grow.

Ask yourself, currently:

- What do you or your company have in place for widows?

- Is there a handbook? Are there resources? Are there forms?

- Is there a priority list or timeline when a bereaved client comes into the office?

- What ways are you engaging widows or women currently?

- Is this a part of your practice? In what ways are you building this part of your practice?

- What’s missing? Where are the gaps?

Think about you as the grief leader. This is something you cannot pass the buck for; they are looking for you, your staff, and your team to show grief leadership. Teach your whole team what to say, what to do, how to build, how to grow.

Financial advisors, like coaches, know how to play offense. You know how to anticipate, forecast, prepare, and practice. You know that value, so that should be your same approach to working with women and widows. I love this quote by Wayne Gretzky, the Great One: I skate to where the puck is going to be, not where it has been. So, where is the puck heading? It’s heading toward widows and the wealth transfer of Baby Boomers.

Communication

Let’s start with the first part of our acronym, or what to say. This is where we seem to get most stuck. We get tongue-tied, it’s awkward, and it’s not fluent. It’s sort of like when you go to a foreign country, and you order something at a restaurant, and you don’t know if you ordered the right food because you don’t know the language yet.

Underneath communication, there are several things. Our body language tells the story, specifically when we are not confident. When we are nervous or unsure, it shows. One thing that’s important in body language research is that women read body language better than men. When a female doesn’t understand the message, they will read the body language first.

That is key when we’re talking about grief literacy and practicing body language. We want to listen to understand, not solve, and practice those listening skills around grief, around death.

It seems to be noted that there’s much bias in the types of death. The unconscious bias that we can bring to the table means we approach types of death differently. We have a set of unconscious emotions that we need to make sure that we’re not showing in our meetings, in our conversations with our bereaved clients whether someone died of old age and they had a wonderful life, or if their death is suicide or overdose, or if they died very young with several children.

“I’m sorry.” That is our go-to. When somebody says, “My husband died, “My brother died,” we say I’m sorry. “I’m sorry” isn’t enough when someone you know is experiencing grief. This is your client. It’s what everyone says. It’s overused, programmed, and lacking original thought. Mostly though, it doesn’t cultivate connection and engage conversation. You want the conversation to continue with a bereaved client.

If you’ve ever had children or junior high students, you pick them up from school, and you say, “How was your day?” “Fine.” “What did you do?” “Nothing.” Those are conversations that don’t continue, so we need to learn how to ask better questions. We need to learn what you should say and what you shouldn’t.

When I talk about mirroring the grief terms, every grief therapist out there will say you should use the present terms like death, died, funeral rather than passed or loss. Those are ambiguous terms; however, you should mirror the terms that your bereaved client says.

If they say they lost their husband, then you mirror that, but if they don’t, then you say, “How are you dealing with the death of your husband? How are you dealing with the death of John?” Overall, we want to put this into practice. These are fundamentals we practice over and over and over. We roleplay. We script practice. The language will start to become natural, automatic, and authentic.

I’m sure many of you have had some training on what not to say. Here is what you should never say. I’ve put these into four categories; justifying, dismissive, manipulation, and my favorite, the takeover artist, who wants to make it all about them. What these statements are called is “disenfranchised grief.” This is a type of grief and loss that isn’t validated. It’s not recognized, and it’s not acknowledged, so there is no connection. It’s a disconnect. If I had a dollar for every time somebody said these statements to me – and they still do say them to me – I’d be taking my financial advisor on a trip on a yacht somewhere in the south of France. Let’s look at some of these.

- Justifying: “Well, at least they didn’t have to suffer. It’s God’s plan.” What they’re saying is that your grief doesn’t matter, and we’re just going to justify that it doesn’t, and I don’t want to continue to talk about it.

- Dismissive: “You’ll be fine. You’re young. You’ll move on”.

- Manipulative: “You really should get back out there again.” Raise your hand if you like to be told what to do. I don’t know anybody who does.

- The Takeover Artists make it about them. Some of the things that were said to me I can’t even believe: “Well, my cat died. I know exactly how you feel.” Or, “You know, I bet you’ll go back to Montana, back where you grew up,” or, “You’re young. You’ll get married again. Let me set you up.” You’d be surprised at what people say.

This might seem out of the ordinary in a financial, professional setting. However, we get nervous and don’t know what to say, so we revert back to maybe things that we heard or what was said to us.

What are things we can say? I love this quote by Brene Brown. “Connection is the energy that is created between two people when they feel seen, heard, and valued.” Those three words, you’re going to hear a lot from me, seen, heard, and valued. We want to make a connection. Communication is one thing, but we want to think about how it’s landing. We’ve got to stick the landing here.

Some engaging questions:

- I can’t imagine your suffering.

- Can I just sit with you?

- Do you want space or more people around you?

- What has your friend and family support been for you?

Do you see how all these questions are leading into a conversation? I want the conversation to continue because, during that first month, there are some things financially that will need to get done. There are forms to be completed, but if you have not engaged and connected first, those will be tasks that are not going to be done easily.

Be sure that your statements validate, respect, and honor the deceased person. For me, it’s been 15 years. I never ever get tired of somebody saying my husband’s name or telling me a story or a memory that they had of him.

Use the name in their statement or question. Use the terms death, died, deceased, accident, and cancer, but mirror theirs if they don’t use them. You’ll want to prepare what you’re going to say before meeting with them. When you go to the funeral, the service, the memorial service, you need to have something prepared that you know you’re going to say. It cannot be about you being an advisor or any decisions that need to be made. It needs to be a human connection so that they feel seen, heard, and valued.

Action

The second in our CARE acronym is Action. What do you do? What type of help beyond the numbers can you provide because if you can do more than what you’re truly paid to do, in the long run, you will reap those benefits?

There are so many tasks to be done that it is overwhelming from a widow’s perspective. Let’s talk about a few of the immediate things, such as your first contact. I encourage all of you to be reading the bereavement and obituaries of your local paper. You need to know your community because you need to make that call. When you know a client has passed away, their spouse has passed away, you call immediately. They might not pick up, but you call, leave a message, and make that contact. Yes, you go to the memorial service. Yes, have something prepared.

That first office visit, we want to set them up in a place where it’s a comfortable environment. I believe that widows shouldn’t be kept waiting. That first time they come in, make sure that your team gets them right back to you as soon as possible. We don’t want to have to tell our story to three different people before we meet with you. It’s hard enough. We want to set up and break down as many barriers as we can in the office visit. Lots of caring acts and small gestures.

What do you send? Typically, it’s flowers, but the better you know your clients, you will know what they will need. Flowers aren’t always the best option. Specifically, there are some religions out there where that is not a respectful thing to send, so you want to be aware of your client. There are so many other things and resources to send right now. How about donating in that person’s name?

If they have kids in school, donate to the high school. Throughout the year, those small gestures matter, specifically with women, specifically with widows. Which dates and holidays do you need to reach out?

I remember getting a birthday card for my late husband from an insurance professional two years after he died. This just shouldn’t happen, so we want to keep those calendars, maybe the first anniversary, the holidays, December – those are really tough times for widows.

They’re overwhelmed. Help them organize tasks and paperwork. Offer your help. There should be things that you have in place right now that are now, soon, and later of financial tasks. Do you have priorities set up with your firm or set up with a widow packet or widow checklist of what needs to be done that first week, month, and so on? You should be a part of helping them do that, even if you feel them out yourself.

Widows don’t want to be handed a long handbook. With the organization of tasks and paperwork, it’s important that we don’t overwhelm them with the financial picture because grief fog, it’s a real thing. The number one question that new widows want to know is cash flow. They want to know if they will be okay and how the cash flow is going to work the first year. Any financial decisions beyond that first month, be more of the decision partner them.

Don’t make long-term decisions because, with the grief fog, they’re going to forget it. As a widow, your memory lapses. You don’t remember what they say. You’re forgetful. It’s a real thing. Sometimes they call it grief fog, widow brain, or widow fog.

Brian Korb focuses on widows and financial advisors. He provides five main tips that he came out with when he interviewed widows and financial advisors.

- Communicate well. You need to learn to communicate confidently when talking with widows, thus the reason for grief literacy.

- Provide for their current needs. We’ve talked about cash flow. Make sure they are okay that first month.

- Be a decision partner. Widows go into decision fatigue. When you think about it, how many decisions do you make in a day? How often do you bounce them off someone else? When you’re a widow, you don’t have that privilege anymore. You’re doing it all on your own. Shift from advisor to guide, partner, and listener and be that back-and-forth to bounce ideas.

- Prepare for their unique future. This is really important. It goes back to when I say the word widow, we have this connotation of just an elderly grandma. Your women widow clients could be in their 30s with children. They could have college-age children. They could be a person approaching Social Security retirement age. There will be a different context and scenario, so make sure that this is not the Amazon shopping, one-size-fits-all.

- Provide them with some support services. What do you have currently with your company in grief resources? Are there some documents that they could read? Is there a handbook of managing grief that first year? Are there resources or recommendations for support groups in this area? These are things that you could put in place now.

Relationship

The third in our CARE acronym is Relationship, or what you build. With relationship, rapport, respect, you will have referrals for your lifetime. Widows want you to know them, and they really want to know you, so how do you keep a professional relationship yet still have personal conversations?

One of the things that you need to do with all your women clients right now is to create a better client profile. I can’t even tell you how often my advisor or other people that I dealt with first year kept on asking me the names of my children, how old they were, or mixing it up and saying, “How are your two girls,” and me having to repeat that no, I have five children, three girls, and two boys. If you make a better client profile, you can have conversations with these people upfront before you need it.

You should know where they grew up. You should know if there are family in the area, what groups they might belong to. What’s their lifestyle like? Do they like to travel? The more we know about our clients when you’re a financial advisor, the better you can relate to them when a relationship is what’s truly needed.

We all love a recipe from scratch, right? It usually tastes pretty good, but this is not when you can start from scratch with a new window. They do not want to build a relationship with you during grief, so we want to front-load this with every woman widow client you have.

Overall, remember that the death of their spouse does not define these people. There’s so much more than this, and they need to be understood and valued and respected because, bottom line, women are very relationship driven. They’re conversational-driven. They go by word-of-mouth of their friends. They’re very tribal. They take recommendations from friends. We want to make sure that you build this relationship with them before they become a bereaved client.

Here are some ways to accept that widows are your current and your future client, so you start to relate to them better. I’m involved in many widow’s and Facebook groups, and I sometimes poll 5,000 – 10,000 widows. I ask them what an advisor or financial professional said to them. Some of their responses are, “I hardly knew them. They mostly talked to my husband.” Or “I just couldn’t relate to them because they were talking about rates of return and financial terms that I didn’t understand.”

These are four things you can start doing now.

- Always use the term “my clients,” not “this is my client and his wife.”

- Initially, talk about basic financial terms without sounding condescending. You want to gauge where they are and meet them where they are. I didn’t know any financial terms before my husband’s death. I trusted him to work with our financial advisor. I didn’t have a strong desire to do it until I needed to. It’s very, very intimidating, the financial literacy and not understanding the terms.

- When you meet, meet with both partners together.

- You should be asking the partner questions, joint goals, individual goals; you should know both spouses. Sometimes, it isn’t feasible with our busy schedules, but it should be an objective to get to know both as best you can.

Empower

The fourth component of CARE is Empower. That’s a word you see almost everywhere right now. I think about it in these terms. It’s empowering to protect because one of your main jobs in being a financial advisor to a widow is to protect them and teach them how to move forward. Here’s a quote by Ann Heath, and she says it best: “Grief is in two parts. The first is loss. The second is remaking a life.” You have the distinct privilege of helping widows remake their lives.

These are proven ways that can help you.

- Financial education – this can be a big part of your business. Short workshops, easy take-home materials, opportunities to engage with other women widows; get all your women clients together.

- Introduce your widows to other support groups.

- Get them some grief literature.

- Provide them with resources moving forward. They’re going to have new professionals, new people that they’re going to have to deal with on their own.

I was always so afraid to call somebody to repair something in my home because I didn’t want anybody to know I was alone with children. There are so many opportunities for you to protect and educate these widow clients because they get taken advantage of quite a bit.

Initially, they may need a little handholding. I always think of the analogy of a kindergartener. When you take a kindergartener to school for the very first day, you’ve got them all ready, you’ve prepared them, and they’re ready to go. Well, you wouldn’t just drop them off in the parking lot and say, “Okay, good luck. Hope it goes well.” We have to take that approach with new widows. They are a very fragile population, and they get taken advantage of, so what do you currently have in place? Do you have some resources in place for them? Do you have some referrals in the community that you could send them? We want to start working towards that.

Here are four takeaways based on that information. These are things they prefer.

- Widows want frequent, consistent, and shorter-duration workshops. Have you ever taken that university class where it’s like, oh, it was a three-hour lecture? We don’t want this. Short, frequent, to-the-point; give me a one-pager to take home.

- A bespoke program – we want the unique experience tailored to them. You may want to have some programs or workshops for widows who are retiring or widows who have children in school. I remember my financial advisor helping me fill out forms for college entrances, the FAFSA forms. That was a huge help. I didn’t have any clue how to do this. We want to make sure that whatever programs you’re doing, you’re tailoring it to their needs and age.

- You want to create community. A widow’s workshop should promote social interaction, active participation, group participation, and a little F-U-N. Widows are smart. They are witty. They relate to one another, and they want to have fun. So, the more you can do this, the more open and inclusive this will be for your widow clients.

- The last thing is the take-home materials. Whatever you have in place now or don’t, keep it short and sweet. Make it very easy and personalized for their current and future needs.

Key Takeaways

We’ve gone over much information. There are so many takeaways that we can think about, but jot down three things that you could do today for widows. Also, jot down two statements that you could say to a brand-new widow because you’ll want to establish yourself as a financial professional who advocates for widows.

- I want you to shout it from the rooftops that you work with widows. Become the expert. People will come to you because, as we talked about, there’s going to be a volume of widows coming your way. We want to talk about understanding the unique financial needs of widows. Loss, death, grief are monumental things. You’ve experienced, and we’ve watched this last couple of years with COVID, so much death, so much loss, so much grief. It’s incredibly sad, but when it’s a widow, it’s financial.

- Can you imagine giving half of your income away tomorrow? Could you survive and have the lifestyle that you want with half of what you have currently? That’s what they’re experiencing, and there is so much fear and guilt around money that it’s hard for them to want to keep it and invest it. Many of them just want to get rid of it because it’s associated with some different emotions. It came with such a high price.

- You’ll want to recognize the impact of wealth, the wealth transfer. This is going to be the most significant wealth transfer in our lifetime. Let’s get ahead of it. Can you get ahead of the curve? That Baby Boomer generation, sadly enough, is going to be a Death Boom, and it’s beginning.

- Practice, practice, practice; I want you to practice grief communication skills, what you say, your responses, what questions you ask, your body language, making sure those skills build connection, continuing the conversation. That’s the goal.

- Create better opportunities to engage your current women widow clients. You’ve heard me say it. Your current women clients will be your future widow clients. The data isn’t lying, and the trends aren’t reversing, so what are you doing now? Are you doing workshops? Are you providing some resources, some pamphlets, and some things that could help support them? Put those in place now so when the fire drill happens, you’ll have them in place.

- Start applying best practices and delivery methods. In your events, they want shorter workshops. They want them more frequently. They want them to be social. They want to have some fun in these workshops. They want to engage with other women and widows, and they want it specific to their age group, to their needs. When you are a 32-year-old widow or a 67-year-old widow, there are very different needs financially.

- Provide community resources for widow clients. Get to know what’s in your community. Who can you recommend, grief counselors, grief groups, what people can you recommend for windows? I call it “When a widow walks on a car lot.” I had no clue how to buy a car. I got taken advantage of; I paid too much. I knew I was getting taken advantage of. I just was too tired or exhausted to deal with it. That’s the reality of a widow.

- Lastly, you’ll want to educate your team with grief literacy workshops and training sessions. We really must practice this. It’s like a piano recital. It’s rehearsing it, script practice, knowing the dos and don’ts. The more you can do this, the more fluent you will become in grief literacy. Bottom line: when you care beyond their portfolio, don’t be surprised if you become a better parent, partner, and community member, basically a better human.