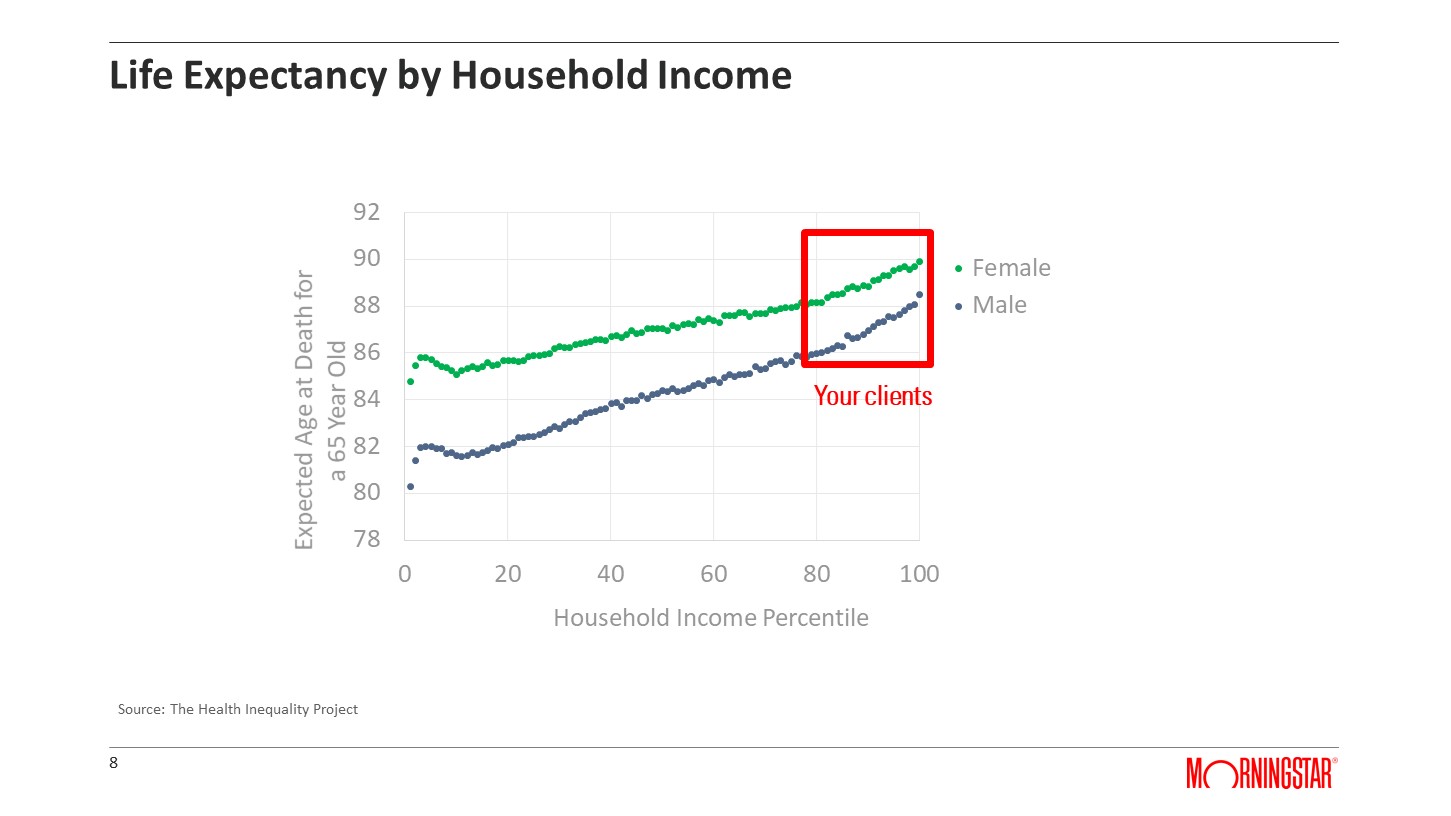

Life expectancy is defined as the average number of years remaining for a given cohort. Below are how life expectancies vary for households based upon their income. It includes males and females.

Life expectancy at birth is irrelevant for you and your clients for two reasons. First, when it comes to life expectancy, what matters is how long you’re going to live when you retire starting at age 65. Second, many life expectancy numbers are based upon US population averages. The most common mortality table that includes information about the odds of people dying is the Social Security Administration’s Periodic Life Table that includes all Americans.

What it doesn’t factor in is who your clients are. Individuals who use financial planners are overwhelmingly wealthier than average. They tend to be in the top two income deciles between the 80th and 100th percentiles in this analysis. And why that’s so critical is if you look at that group, they have life expectancies that are three to five years longer than the average American. This requires thinking about funding retirement differently than if you’re focused on the “average American.”

How Do We Measure Retirement Success Today?

How do you determine what a good outcome is for a financial plan? You can do it via success rates; you can do what I would call a deterministic projection, which is like a time value of money; but how do we define good and bad? Along these lines, there’s this question of “What would you define is a safe asset?” Again, this is kind of a trick question because you can define safety in different ways.

Here’s an example of defining different outcomes. If you want to fund income from a portfolio, by definition, the odds of that portfolio failing – of it not being able to accomplish that income goal – is greater than zero percent. At some point, bad things could happen, and that portfolio might no longer fund that lifestyle. With guaranteed income, it’s approximately zero percent.

“Well, the annuity company can fail.” There are the State Guaranty Associations that insure consumers in the unlikely event that their insurance companies fail, so it’s really, really unlikely. If annuity companies start failing, there’s going to be nowhere safe to hide. But again, there’s the perception of, “Well, which is safer – something that has a non-zero chance of failing or one that has a zero percent chance?”

A different lens to think about this is combining this idea of asset volatility and retirement outcomes. If you were to ask you what a safe asset is – people would often say, “Cash.” T-bills are an incredibly safe asset in that there’s a very high likelihood you’ll get your money back. Here’s the thing. If you overlay that safety with a retirement outcome, they become incredibly risky. If you buy an asset today with a zero percent return before fees, inflation, and taxes – if taxes really matter – then that will not last more than say 20 or 25 years in retirement. The odds of that portfolio failing if there’s a reasonable withdrawal rate over, say, 30 years is almost 100 percent.

So, treasury bills are a safe asset from an asset volatility perspective. They aren’t necessarily a safe asset when it comes to funding retirement. Guaranteed income, though – as maybe Social Security or private pension annuity – is a safe asset from a volatility perspective. You have that cash flow that’s effectively guaranteed, like the coupon from a bond, but it’s also going to lead to a safer retirement outcome. The key is thinking about the definition of safety across different dimensions. Safety for a retiree just isn’t asset volatility. It’s everything that impacts how that person experiences that retirement outcome.

Why that matters is because “Well, how do we define retirement success?” If you run a Monte Carlo projection, you might say, “Oh, Mr. and Mrs. Client, you have a 60 percent chance of accomplishing your retirement goals,” or it could be a 30 percent chance or a 90 percent chance. I think that is somewhat useful information, but it can be totally off base many times.

Here’s an example that I think applies well to retirement. Let’s just say that you have an income goal of $10,000 a year for ten years. In the 10th year of the goal, you fall $1,000 short. And so, by definition, you have failed to accomplish your goal. If this is a traditional Monte Carlo simulation – and let’s say that this always happens – you would have a zero percent chance of success. However, if you were to ask me, “David, has this person accomplished their goal?” I’d respond, “Yeah, they pretty much did. They got 90 percent of the way there.”

The problem with success rates is that it ignores the magnitude of failure. If you extend this kind of analysis out 30 or 40 years, what you often see happen for retirement is that the portfolio “fails” in the last three years of retirement. But even when it fails, you still have income sources like Social Security and pension, so it’s not giving you a fair perspective on what the actual likelihood of “failure” is.

Along these same lines, we essentially don’t even estimate failure correctly. What is the truly bad outcome for a retiree? A good outcome it’s not going broke over 30 years, right? The bad outcome for a retiree is being broke and being alive, and that’s important. It’s not just about not having any money over a 30-year time horizon, it’s you need to be still alive, and you must be broke, right? And we don’t capture that almost ever in Monte Carlo projections. We pick a fixed period like 30 years, and then we estimate the likelihood of you accomplishing that income goal over that time horizon.

If you change your Monte Carlo approach to say, “I’m going to incorporate mortality, and I’m going to incorporate the impact or the probability of you or both of you passing away at ages 70 and 80 and 90,” this gives you a much more realistic perspective on failure. If you do that, safe withdrawal rates can go up significantly. Now when you look at retirement research, it doesn’t tend to use success rates. I still do sometimes because success rates are the language of retirement. If you are an advisor and go online and use online tools, you’re probably using a Monte Carlo projection and using the success rate.

That’s not how academics think about retirement outcomes. The biggest reason is that it ignores the magnitude of failure. If you run a Monte Carlo projection, each run is effectively a binary outcome. Did you fail, or did you succeed? It doesn’t provide context as to the magnitude of failure.

Guaranteed Income and Retirement Spending

A critical point here that is totally ignored in research is the impact that guaranteed income has on safe withdrawal rates.

Think about Bill Bengen’s seminal research that came out 20 plus years ago. The idea of having a safe withdrawal rate is incredibly valuable. Researchers have made improvements on it over time. However, almost all research that addresses safe withdrawal rates ignores the magnitude of failure. It assumes that if your portfolio fails, it’s the end of the world.

However, let’s assume you’re a retiree who gets 80 percent of his or her or their income from Social Security, and that portfolio is funding 20 percent. You can take a lot more from that portfolio than you could if Social Security was only 20 percent of your income because if that portfolio fails, you still get 80 percent. The magnitude of failure should impact the definition of safe withdrawal rates. I’ve researched this. Lots of folks have.

I find the optimal safe withdrawal rate changes dramatically based upon effectively the magnitude of failure. If you’re a retiree that gets most of your income from Social Security or guaranteed income or pension, you can be more aggressive. If you’re a retiree, though who gets most of their income from a portfolio and you don’t have any flexibility at all – two percent could honestly be your safe withdrawal rate – and that’s super low, but that’s just reality. Also, a client’s ability to change their spending significantly impacts what a safe withdrawal rate is. It’s not often captured in our projections when we do financial plans or research exploring safe withdrawal rates.

People don’t like to spend down their money. This is the behavioral aspect of funding retirement, and the markets have been incredibly volatile lately. How do you feel about dealing with volatility every year for the next 30 years? How do you feel about having to go in every month, every quarter, or every year and pull money from an account that has to fund retirement? You don’t know how long retirement is going to last, right? That’s painful. We’re so used to spending income when we work. It’s great. You get a paycheck every week, every month, every whatever it is. You earn income. You can spend it.

Creating income in retirement is not as automated and creates all these different pain points. You must pull money out at some interval to fund your consumption. You don’t know how long you’re going to live. There’s been research on this idea of how much people enjoy retirement more the more they annuitize their money. We find that the more someone converts assets into annuities, the happier they tend to be in retirement. There’s a host of reasons for this but just think about the radical simplification.

I know that everyone doesn’t need more annuities. Many folks are just fine without them. But as opposed to having to worry about, “Well, how much can I take out? How long am I going to live? What if I go broke? What if the markets go down? What about these low rates?” Instead, it’s, “Hey, I have a paycheck that the insurance company sends me. I can spend it going forward.” Guaranteed income can make things easier.

This calls into question much past research that utilized this idea of living off just the yield. Up to about a few years ago, you actually could live off the yield of your portfolio pretty easily. You could live off the income from your bonds and dividends from the equities. That’s not really an option today. The dividend yield today on equities is only around two percent.

You can allocate more wealth to guaranteed income in lots of ways. You can delay claiming Social Security. You can buy a private annuity. If you work, maybe you can somehow get a larger pension benefit. The key here, again, is who benefits more from more guaranteed income?

Annuities are only one type of guaranteed income, but they create this interesting, often negative, reaction among most planners. The key is that annuities, as a product, have been around for thousands of years. There are some good ones, there are some bad ones, but we just can’t dismiss them because there are some bad ones out there.

It is important how we frame information about guaranteed income to retirees. Who would you rather be? A retiree with a half-million dollars and $75,000 a year of pension benefits or someone who has assets of $750,000 and $25,000 a year in pension benefits? Which retiree is worth more? The person with $75,000 a year in pension benefits, as they are easily worth another half-million dollars.

What is the largest asset of retirees when it comes to the household balance sheet? Social Security. In my experience, when advisors create a financial statement, they will include the value of the home, the value of a portfolio, they’ll even include furniture, but they don’t include any estimate about the value of Social Security.

You might say, “Well, David, why would I include the value of Social Security? It’s just an income source.” Here’s the thing: If you do a financial plan, you treat the 401(k) or the IRA as both an asset and an income source. It’s going to show up on your balance sheet. We’re also going to use that asset to fund your retirement. With respect to guaranteed income, it is also assumed to be an income source. However, in general, today, it’s not included as an asset. I think that’s wrong. What we need to do as an industry is do a better job at having someone understand what all their assets are.

Who Should Allocate More of Their Total Wealth to Guaranteed Income?

There are four ways to manage risks. You can reduce, retain, avoid, and transfer risk.

Most economists say annuities hedge the most dangerous kinds of risks, and that’s why you transfer it. It is a very severe risk if you go broke when you’re old, but it also doesn’t happen all that often. Risk transfer is most efficient for risks that are severe and low frequency. So, people think, “Well, should I allocate more to guaranteed income?” It makes a lot more sense than, say, buying products like that warranty from Best Buy because – if that bad thing happens, which is your portfolio goes empty – the implications are a lot more.

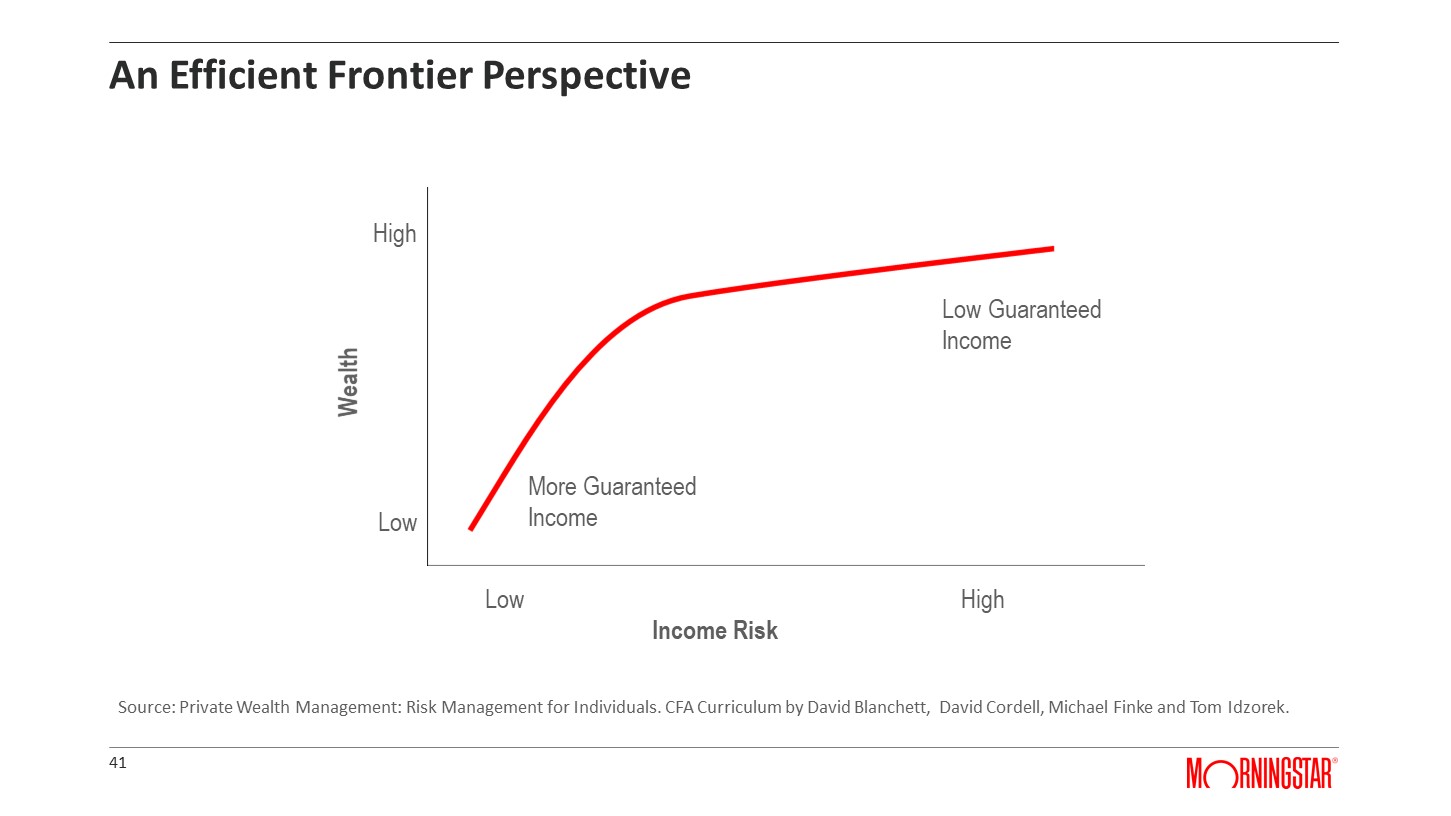

Now one of the most common approaches people talk about when it comes to, “Should you buy more guaranteed income?” is this idea of a retirement income efficient frontier. It lends itself to the original efficient frontier we use for investments. People have created papers on this for at least two decades. The idea is, “Who benefits from guaranteed income across different risk levels and return or wealth levels?”

What you see here is you’ve got income risk on the horizontal axis and wealth on the vertical axis. That red line is the most efficient combination of an annuity and a portfolio.

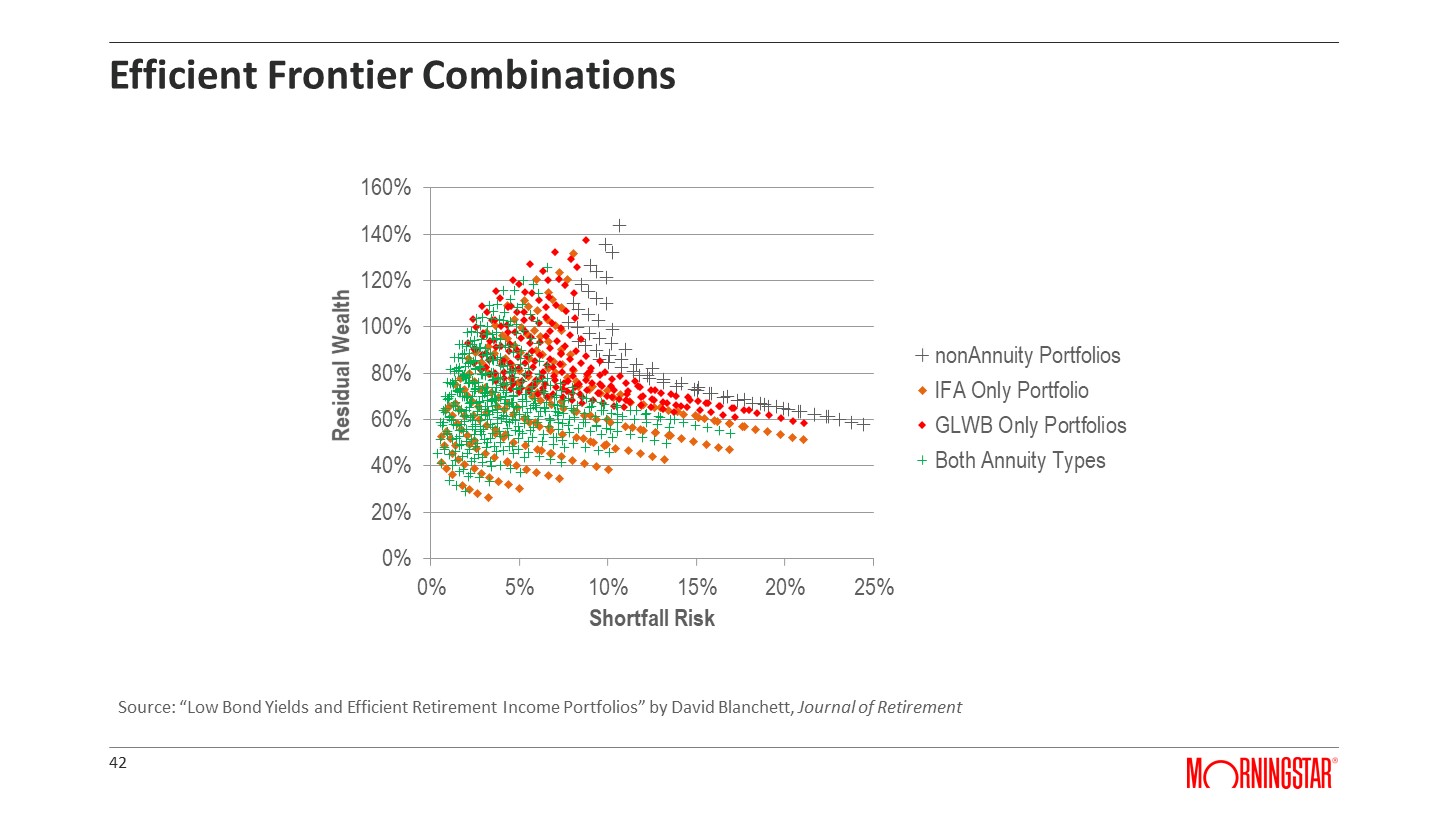

If I’m okay with less wealth and want low-income risk, I should buy more guaranteed income. If I am less concerned about income risk and want to maximize my wealth, I should have less of my overall wealth in guaranteed income. Now you can run projections – and I’ve done this countless times – looking at how you combine a non-annuity portfolio – i.e., a regular stock/bond portfolio – with different types of products. This is how you create a retirement income efficient frontier.

How does combining products with different attributes affect what someone should do, given that combination of how they feel about shortfall risks or income risks and residual wealth? The traditional retirement income efficient frontier focuses on your preference for income stability and your preference for bequests – your residual wealth. Other things matter too.

For example, that entire graph is going to shift based upon how much guaranteed income you have, how prepared you are for retirement, the quality of the annuity you’re considering, and how long you’re going to live. Long story short, all this matters, and to truly figure out whether you should annuitize is really, really complicated. One of the best frameworks is honestly the simplest. It’s asking someone, “How much income do you want to have locked in for as long as you’re alive?” and if that’s less than what they have locked in today, think about at least annuitizing that amount or possibly more.

I commented earlier that the term “annuities” is somewhat of a loaded term. We must acknowledge this whenever we talk about guaranteed income. There has been somewhat of a shift in the potential reception to annuities or guaranteed income over the last several years. There are better terms to call them. I like the phrase “personal pensions” because that’s because the word “annuity” has lots of baggage associated with it. Often people will say, “Well, I never recommend annuities to my clients.” I really have a problem with that.

Tongue in cheek, I have this thing that I call the mutual fund puzzle. There are mutual funds out there that are incredibly expensive. They have expense ratios of over four percent a year. There is overwhelming evidence that most mutual funds underperform their benchmarks, and most of the time today, advisors who recommend or sell them aren’t fiduciaries. The problem is that people will take this exact same logic and say, “Well, I would never recommend an annuity,”; but that’s ridiculous. We all recommend annuities for the most part because it’s not the fact that there are some bad ones out there. It’s the vehicle itself.

Many annuities do have high fees, and they aren’t very good. There are probably more bad annuities than bad mutual funds, but there are some great ones out there. Part of the problem people when think about annuities is, they don’t always apply the right framework.

Annuities are like an investment. A lot of them have investment-like attributes. But the fundamental purpose of an annuity is insurance. Advisors view the value of guaranteed income annuities from an investment lens. Again, some have investment attributes, but the key benefit is protection, not necessarily growth.

Interestingly, we see that people who don’t own annuities don’t often have positive impressions of them. However, after they buy one, it becomes a lot more positive. There’s probably some selection bias here. People who buy them tend to like them, but this is the behavioral part of it that I think is so hard for people like me to quantify.

I’ve had many advisors tell me, “David, I have run the numbers, and annuities don’t make any sense at all.” Remember, annuities are insurance. They shouldn’t necessarily make you money. How are you running the analysis? Many advisors use historical long-term averages and compare them to an annuity quote today. That’s ridiculous. The average historical yield on US government bonds is close to five percent. That yield today is less than one percent. You can’t compare historical long-term average equity and bond returns to annuity prices today. When you equalize the return assumptions, annuities can become a lot more attractive.

Along those same lines, what about fees? Too often, advisors will run a projection that doesn’t include fees to the portfolio, and they’ll compare it against an incredibly high-cost annuity. It needs to be apples to apples. If you compare a high fee annuity to a low fee portfolio, of course, the portfolio is going to win. If you compare a high fee portfolio to a low fee annuity, of course, the annuity is going to win. The key is making it realistic and relative.

People will often say that annuities are expensive. Let’s just say that you’re going to pay a six percent commission today on an annuity purchase, or whatever it is. That is a lot, but so is paying a one percent management fee every year forever. I’m not trying to dismiss the value of advice here at all. I’ve done research talking about advisor value, but the key to all this is context. It’s how we all think about and internalize the value of different products and approaches.

Key Takeaways

What are some key takeaways?

- How do you think about guaranteed income? This is a serious question, and I think ahead in the sand perspective is honestly how most advisors view it. They say, “Well, I looked at it three or four years ago, and they didn’t look very good,” or “Annuities are very expensive. I don’t recommend them.”

So much has changed in the product space and the fee-only space in the last three to five years. I think you’ve got to be continually looking at how these can help you improve your practice and your clients’ retirement. For those advisors who are adamantly against annuities, I get that. Still, there are products like deferred income annuities or longevity insurance that aren’t very expensive that can help someone hedge away their longevity risk.

- Maybe your client doesn’t like them or know that they want them. If I’m an advisor, I want to have as many arrows in my quiver as possible. To just dismiss them for all your clients outright is a clear breach of fiduciary duty. There’s no way that some of your clients would not benefit from having more of their wealth in guaranteed income. For every single one of them, that could be higher Social Security benefits. That could be a pension from work. But I think we’ve got to think more about guaranteed income as part of a retirement plan, and to me, it is the cornerstone of a retirement income plan.

- Guaranteed income is the cornerstone of people’s retirement because it is the guarantee. It is that thing that we know will be there for as long as the person’s alive, and a portfolio can’t do that. Now it’s not necessarily as fun or as sexy to talk about annuities or Social Security or pensions as it is to talk about investment alpha. Still, they are so important to someone’s overall financial wealth – to how they invest their portfolio – that we simply can consider them at every part of a financial plan and give them their due. Now you might ask, “Well, how do I figure out what to do?”

The key with annuities – like almost everything else in this profession – is blending the art and the science. The art is your experience. It’s how you have seen clients respond to different environments. This is the behavioral stuff. I think the behavioral stuff is the most important out there. It’s funny that almost all the research is on the science of guaranteed income. It’s how they can improve someone’s utility or portfolio efficiency or their outcome.

Where annuities make the most sense is the behavioral side of things. It’s giving someone that automated paycheck that you can’t get from a portfolio.

It’s incumbent upon all advisors to understand the science, read journals like the Journal of Financial Planning, the Retirement Management Journal, the Journal of Personal Finance, or whatever it is, and understand what the academics that review these products think about them and where they think they fit.

Every client is different, and every situation is different. Unless you understand how people like me and others think about them and talk about them, it’s going to be hard for you to help clients make the best decisions, especially if you ignore guaranteed income as part of your overall retirement income strategy.