Wealthier clients have the longest life expectancy, so the longevity risk for those people who have many assets and have much social capital are the ones that you need to be looking out for in terms of meeting that longevity challenge.

The Pros and Cons of Reverse Mortgages

Let’s start with the things that are not so attractive about a reverse mortgage.

- It will cost your clients some equity because the product is FHA-insured. There are premiums, both up-front and ongoing, that are going to the Federal Housing Administration (FHA) to provide the safeguards available in reverse mortgages, which we will discuss later. Sometimes, there is quite a sticker shock when your clients see that setting up a reverse mortgage will cost them some of their equity. It is not up-front cash that they need to commit, but depletion of their equity.

- A reverse mortgage involves compound interest assessment. What that means is because there are no monthly payments. Because the client is not making a payment on the interest, the interest is tacked onto the loan balance, so the loan balance will be larger the following month. The interest is then assessed on that larger loan balance, and so on. The client can make payments on the reverse mortgage, but most people do not do that. So, compound interest is, as we know, just a beautiful thing when it is working for you and not such a beautiful thing when it is working against your equity.

Let’s now look at the pros of reverse mortgages.

- Because of the FHA insurance, the reverse mortgage is a non-recourse loan. That means that the client or their estate will never owe more than the value of the house.

- Reverse mortgages are incredibly flexible. The client may choose to pay the interest, make payments on the interest and the principal that they have drawn, make no payments, make payments, as Dr. Wade Pfau suggests, in good years. When the market is up, and the retirement assets are healthy, go ahead and make payments, but do not make any payments on your reverse mortgage if they stress the portfolio. Many people do not realize that a reverse mortgage cannot be canceled, frozen, or reduced, and that is even true if it is in a line of credit structure.

- One of the problems with a HELOC is that just when the client needs liquidity, the banks often cancel and freeze the HELOCs. You cannot be foreclosed on with a reverse mortgage because you have missed a payment, as no payments are required.

- Credit capacity grows with age.

What is a Home Equity Conversion Reverse Mortgage (HECM)?

A reverse mortgage is a mortgage where the amount of money the client is eligible for is based on the home value. The home provides the dollars, but it also serves as the sole collateral. The client never has to make a payment from any other resources; the house provides the repayment.

Since the loan is non-recourse, actuarial principles apply. The amount of money that the client is eligible for is based on their life expectancy. If the house is going to pay the loan back and you are younger, the assumption is you will be in the house for a longer period, so you will be eligible for less money up front. If you are older, the assumption is you are going to be in the house for a shorter period, so you are eligible for more money. Also, your borrowing power increases as you age because of the actuarial or insurance aspect of a reverse mortgage.

Brian Montgomery, a former FHA commissioner, calls the home equity conversion mortgage the “law of the land.” What does that mean? In 1988, President Reagan signed a HUD bill (the FHA is the insurance arm of the Department of Housing and Urban Development) and signed the home equity conversion mortgage into law so it is FHA insured. The bank does not take the house. You are not trading your title and giving it to the bank in return for getting money. You maintain the title to the home.

With reverse mortgages, you cannot owe more than the fair market value of the home. The house is the sole collateral. It is in effect until the last spouse dies, moves, or sells. Many people think that if you use all your money in a reverse mortgage or housing values drop, you will get kicked to the curb by the lender. That cannot happen.

How is a HECM different than a forward mortgage? The homeowner has the option to make monthly payments but is never obligated to make a mortgage payment. There is no prepayment penalty; the loan can be prepaid at the homeowner’s will. That is an FHA guarantee. We have seen people who have taken out a reverse mortgage, and then a situation changed rapidly, so they just pay off what they have borrowed, and they can move out of the house. They have not given up title or control of their home.

The FHA non-recourse insurance guarantees that a person or their heirs will never owe more than the home’s value, regardless of how long the homeowner lives on the property. It is crucial to be able to understand and articulate this. If using a line of credit arrangement, the unused line of credit grows at the same percentage rate the homeowner is paying on the outstanding loan balance. This rate of growth is not affected by home values. It goes back to that concept that as you age, you get growth in your ability to access your home equity, and it is a predetermined, contractual rate. It is not at the discretion of the lender.

Any unused funds in the line of credit cannot be canceled, frozen, or reduced arbitrarily by the lender. The home must be the primary residence of the borrower. Snowbirds are okay, but the reverse mortgage must be on their primary residence. They must remain current on their property taxes, just like everybody else in America who owns a home. Anyone who has a mortgage also has to be current on their homeowner’s insurance, and they have to keep their home in reasonable repair and up-to-date with any HOA fees that might apply.

The reverse mortgage has received a bad reputation because they were provided for people who did not have the willingness and capacity to keep up their homeowner’s and tax payments. This was a terrible situation for everybody. We only want to provide reverse mortgages for people when it will improve their retirement security and be sustainable over time.

Dr. Wade Pfau’s Four Nevers About Reverse Mortgages

In Dr. Wade Pfau’s book on reverse mortgages, he points out the following “Four Nevers” about reverse mortgages:

- You will never give up title to your home. As I said before, the bank does not get the house.

- You will never owe more than the home’s value. The loan documents state that neither the homeowner nor his estate is ever subject to a deficiency judgment. The corollary is that any remaining equity beyond the loan balance belongs to the borrower or his heirs.

Let’s say that a reverse mortgage loan balance is $400,000. The house is sold for only $300,000, so now there is a $100,000 deficiency or gap. The FHA insurance covers this gap. The corollary is lender does not get a share if the house sells for more than the home’s value. Say the house sells for $500,000, and the loan balance is $400,000. That $100,000 remaining equity belongs to the homeowner or their heirs.

HUD gives the heirs up to 12 months – you need to be in touch with the servicer about this – to sell the house. You need to tell the servicer what your plan is. You are either putting the house up for sale or arranging for your financing to pay off the remaining balance. But again, just remember that it is a non-recourse loan, so if the house’s value is not adequate to pay off the mortgage, there is no personal liability to the heirs. They are insured, and they can walk away from the house.

- The homeowner is never forced to move. Should the available credit be exhausted, the homeowner has the right to remain in the home.

- There is never a monthly payment required on the principal or the interest until the last borrower leaves the house permanently.

It is also important to note that money accessed via the HECM is considered proceeds from the loan, so those proceeds are not taxed.

Who Qualifies for a Reverse Mortgage?

One of the homeowners needs to be 62 or older. They can have a mortgage.

The No. 1 use of a reverse mortgage is to replace a current mortgage with a reverse mortgage so that the client does not have principal and interest payments to make. Sometimes, it is quite a bit easier to qualify for a reverse mortgage. There is no minimum credit score. Again, it has to be a primary residence. It can be all these different configurations: single-family, condo, duplex, triplex, fourplex, and in some cases, a manufactured home.

HUD especially wants to make sure – and lenders comply, of course, the loan is a suitable and sustainable solution. There is a financial assessment or kind of underwriting to protect against the client eventually going into tax and insurance default.

There are now protections for non-borrowing spouses, so those under the age of 62 have protections to stay in the home should the homeowner die.

There are limitations on accessing the equity. There is a cooling-off period now that encourages the sustainable use of home equity.

Clients also will need to go through mandatory counseling with an FHA-approved and independent counseling agency. The purpose of this is just to make sure that everybody understands that even though payments are not required, interest is involved. This is a mortgage, and they are responsible for their tax and insurance. Borrowers tend to forget these things.

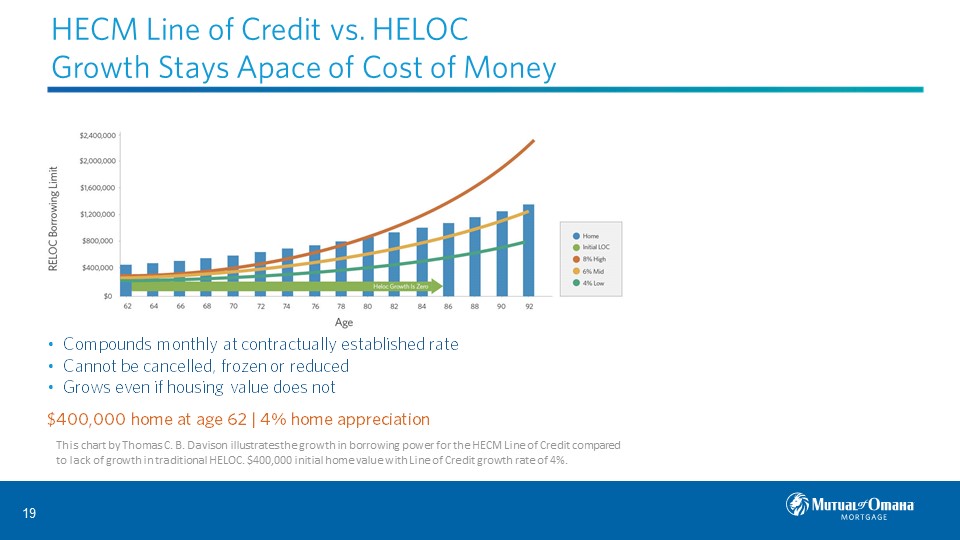

Differences Between a Traditional HELOC and a HECM Line of Credit

With a HELOC, unless you reapply, you will have a static credit capacity, and it is usually over within ten years. With a HECM line of credit, your borrowing power will grow over time (see orange line below).

Dr. Pfau says, “Opening a HECM line of credit earlier in retirement allows for greater availability of future credit relative to waiting until later in retirement.” You get compounded monthly growth at a contractual rate in your line of credit. Nobody knows what the future holds. You could say, “I will wait ten years,” and then when you go to open your reverse mortgage, the housing values maybe have dropped, or interest rates could be higher, and you would be eligible for less than you would have been eligible for ten years before. A way to ensure that you have access to an increasing value of your home equity is by setting up that line of credit early in retirement.

The example below is of a traditional HELOC where you do not get the automatic growth in the line of credit. The other lines show the HECM line of credit growing at various points. The interest rate is around four percent right now, so the green line provides an example of today’s growth and borrowing capacity from the line of credit.

Three other critical differences are:

- A HECM is both a mortgage and an actuarial program.

- The lender does not determine access to equity. HUD does, and it is based on life expectancy.

- Unlike a traditional mortgage, unless the homeowner takes all available proceeds in a lump sum, they are not locked into an arrangement, and they can make changes as often as they want.

Let’s say a client has set up a HECM line of credit. They find they are $1,000 short every month between their income and expenses. They can set up a monthly payment for $1,000 for around a $25 fee.

Lump-Sum Options for Dispersing Reverse Mortgage Proceeds

Proceeds can be distributed in various ways:

- Lump sum.

- Monthly tenure payment, which is basically annuitizing what you have available to you. It is a guaranteed payment until the last one of you dies, moves, or sells.

- Term payment. Say you need $12,000 a month so that one of the homeowners can have long-term care or hospice care at home. You can set that up for as long as it will last or as long as needed, whichever comes first.

- Reverse mortgage line of credit. Remember that the lender cannot cancel, reduce, or freeze.

Or you can set these up in a combination. Say you are eligible for $300,000 at the outset and have $100,000 HELOC. You can take a lump sum of $100,000 to pay off the HELOC and put the remaining $200,000 into the line of credit.

What are some ways to use a lump-sum distribution?

- Replace a current mortgage with a reverse mortgage.

- Purchase a new home, which is called a home equity conversion mortgage for purchase.

- Establish housing equity in silver divorce.

- Use a reverse mortgage on your primary home to purchase another home.

Lump-Sum Example #1: Dr. Pfau has this case study in his book: Mary and John are 65 years old. They have ten years left on their mortgage. Their mortgage payment is $15,574 a year. They will replace their current mortgage with a home equity conversion mortgage, which means they will have no mandatory payments. This establishes cash flow for them of $1,297 per month. The value of their home is $541,000. They owe $129,000, and because of what they were eligible for, they pay off the $129,000, and they still have $99,000 to reserve in their growing line of credit. This line of credit is going to grow in purchasing power as they age.

Lump-Sum Example #2: You can also use a reverse mortgage to purchase a home (HECM for purchase). If you are purchasing a new principal residence, the amount of money you are eligible for will attach to the new home. This is how not to use up all of your assets for a cash purchase or do not want a monthly payment.

For example, a client’s wife had died, and he wanted to move to the Bay Area to be near the kids. So, the price of the new house was going to be $700,000. He sold his house for $500,000 and netted $460,000. The advisor knew about the HECM for purchase, and at that time, he was eligible for a $300,000 reverse mortgage on the $700,000 house. He only had to use $400,000 from the sale of his house, allowing him to keep $60,000 from the $460,000 he netted after the sale. No payments are due on the principal or the interest until the last one of them dies, moves, or sells.

Lump-Sum Example #3: Use a reverse mortgage to restore or provide equitable housing for both sides of the divorce transaction. We run into this most often. Mom wants to stay in the house, and the adult children want Mom to stay in the house. Mom will have to take out a mortgage to split the marital assets and pay off the departing husband. This is going to be difficult for her. She is retired, and to take on a mortgage now in order to keep the house and pay off the husband is just not feasible.

A reverse mortgage can be placed on the marital home. The ex-husband gets half of that, and then he takes his half as a down payment on the new house he wants, using a HECM for purchase loan to provide the rest of the financing. Nobody has a monthly payment, and everybody is living in a lovely house.

Another option is that they sell the house, and each of them gets cash. They take the half that they were eligible for and leverage that with a HECM for purchase so that they both can enjoy living in an attractive living environment. This is an elegant solution that advisors do not know very much about, so I encourage you to learn more about this.

Tenure Payment Options for Dispersing Reverse Mortgage Proceeds

Tenure Payment Example #1: One option is to supplement income so Social Security can be deferred or to cover monthly obligations such as insurance products that will help them or raise their spending power.

If there are any longevity expectations, clients need to defer their Social Security until age 70 if possible. In this case study by Tom Davison, CFP, a client retires at age 62 with pretty high living expenses of $87,000 a year. She has $500,000 in her IRA. If she starts drawing on her IRA at age 62, there is a high probability she will quickly exhaust her portfolio. She could use the equity from her home to provide funds from ages 62 to 68 and not draw on her IRA, allowing her to delay taking Social Security until age 70.

At age 70, she gets a big bump in income from her Social Security at the most significant amount possible. This has an incredible effect on the probability that her portfolio is going to grow. Why did the reverse mortgage – filling the income gap or that bridge – work so well? The reverse mortgage funded six years of spending, so that is six years that she did not have to draw on the portfolio.

Taxes matter. Two-hundred and forty thousand dollars worth of home wealth were added to the $500,000 IRA. The client is in a 33% tax bracket in California combined. Every dollar that she spends of her reverse mortgage has the spending power of $1.50 from her IRA. The $240,000 from the reverse mortgage is the tax equivalent of $360,000 from the IRA.

The investment portfolio was untouched until age 68, so you had six fewer years of withdrawal. When you run a Monte Carlo simulation, it reduced the sequence of returns risk if bad returns hit early in retirement. Also, investment portfolio draws after age 70 were reduced by the largest possible Social Security benefit.

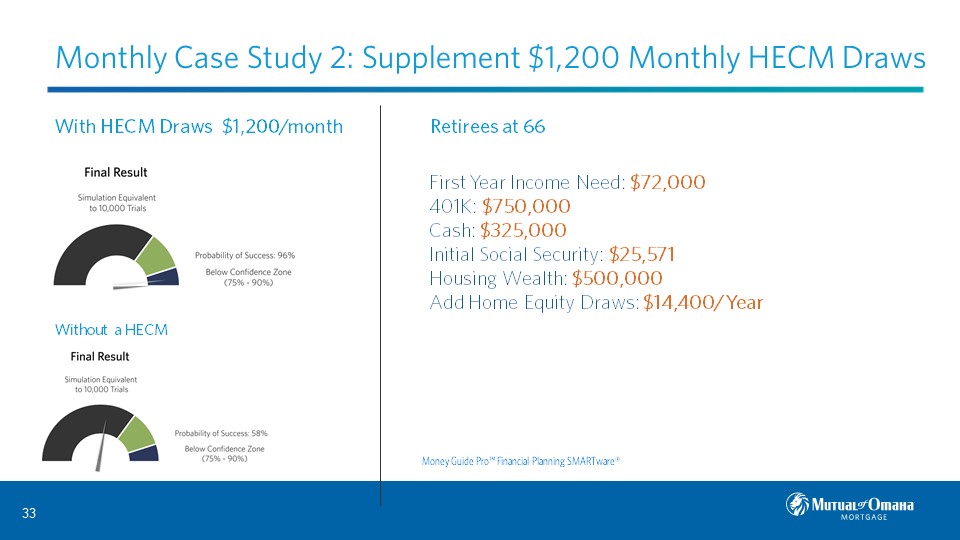

Tenure Example #2: Say a client is interested in supplementing their monthly income with $1,200 monthly HECM draws. It is a very modest amount.

Say a retiree at age 66 has a $72,000 annual income need, a 401(k) of $750,000, a cash bucket of $325,000, an initial annual Social Security income of $25,571, and housing wealth value of $500,000. They are just going to take home equity draws of $14,400 a year.

We modeled the above in Money Guide Pro. Using home equity conversion draws of $1,200 a month, the probability of success is 96%. But without the HECM, without that tax-free bump of $1,200 a month, the probability of success drops substantially.

HECM Line of Credit Client Scenarios

The HECM line of credit (HECM LOC) is a revolving line of credit. If you pay down your loan balance, and your credit available is going to go up.

Also, a HECM line of credit grows and compound at a contractually determined rate as the client ages. Let’s say you have a $100,000 HECM LOC. At the end of the first year, it will grow to $104,000, and then that will compound. Next year’s growth is based on the growth from the first year.

There are three ways a HECM Line of Credit can be used in retirement:

- Mitigate sequence of returns risk

- Self-insure for long term care, or

- Used as a shock absorber for unexpected events.

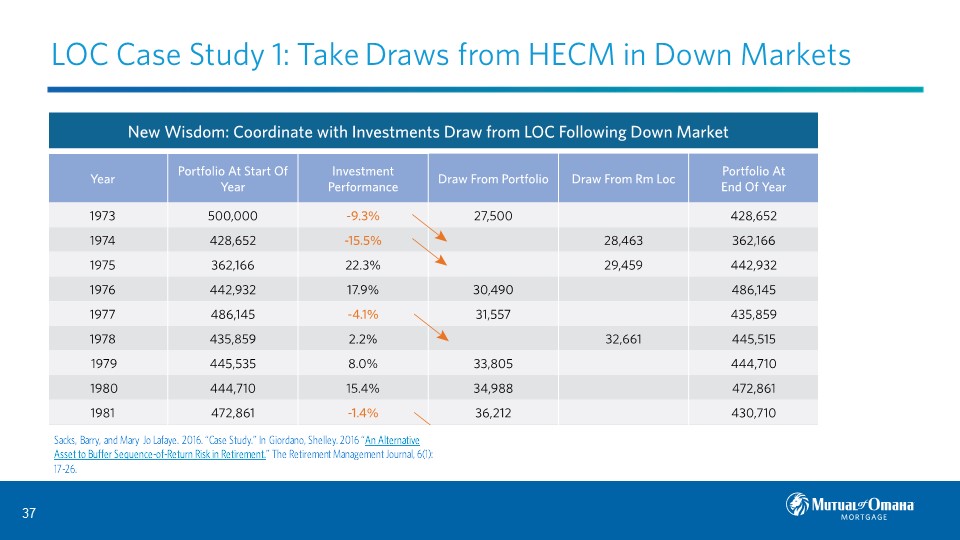

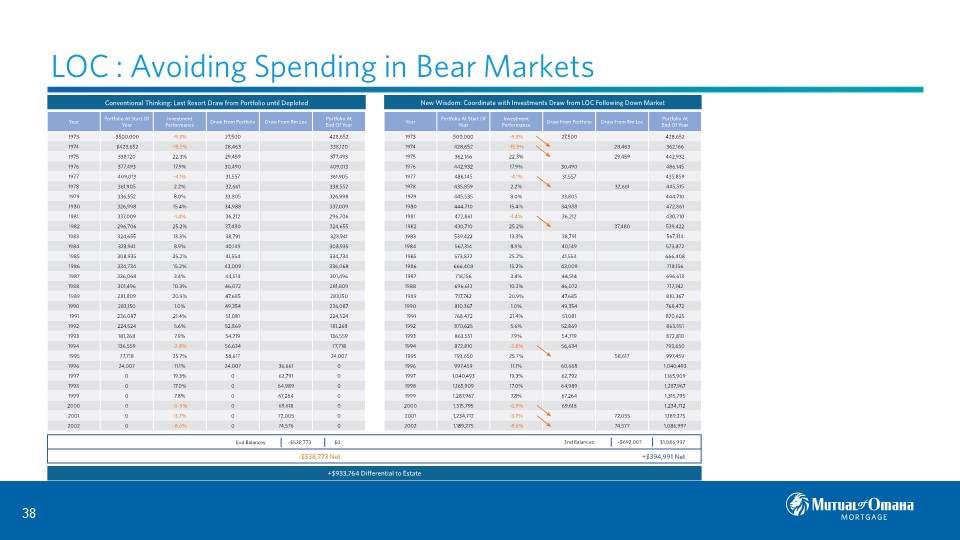

HECM Line of Credit Example #1: Dr. Barry Sacks was the first to identify that if you just take draws from your portfolio following growth years and not take draws in years when the portfolio has shrunk, it could have a fantastic effect on the longevity of the portfolio over time, particularly if you had bad investing results early in retirement.

Assume a client has a $500,000 portfolio, and the client draws $27,500 from his portfolio in year one (see below). Following Dr. Sacks’ strategy, during that year, since there was a negative return, the client will draw from his HECM line of credit instead.

Then there is a second negative year. The client again draws from his HECM line of credit to protect the portfolio. In year three, there is a positive performance year, so the client draws from his portfolio. When portfolio returns are positive, draw from the portfolio; when negative, draw from the HECM line of credit. Notice that four of the first nine years are negative, so this is a case with an adverse early sequence of returns.

In the chart below, you see the client eventually runs out of money in the portfolio, so they have to wait and pray. They must hope there is a reverse mortgage around that will provide them spending dollars. At this point, they are relying on their reverse mortgage as a last resort, which is the worst possible strategy.

In the column at the far right, you can see that the protective effect on the client’s portfolio by utilizing the strategy above is just astounding. They end up with twice as much in the portfolio as when they started. There is debt on the house because they allowed the interest on what they borrowed to compound over 30 years. They could have paid this down or just paid the interest, but they did not, so they had $692,000 worth of debt on the home. Remember, if the house is only worth $500,000, they do not owe that back, and they still have $1 million in their portfolio. Even in this situation, they are ahead $394,000 versus the $538,000 in the negative.

HECM Line of Credit Example #2: This growing line of credit is kind of a “put” on long-term care.

For clients who cannot be underwritten for long-term care or just reject the idea of buying long-term care insurance, an option is to provide self-insurance with the reverse mortgage line of credit.

Say a client age 66 has a home value of $400,000 and cannot qualify for long-term care insurance. Their initial line of credit is $194,000. After five years, the line of credit is $237,000. After ten years, the line of credit is $291,071. The HECM line of credit is an asset they can deploy and be ready if they have a long-term care expense.

HECM Line of Credit Example #3: The HECM line of credit can be used as a shock absorber to plan for the unexpected. How do you plan for unexpected spending shocks? We have had people leave the closing table, walk across the street to their dentist, and spend $10,000, $20,000 on dental work.

Car repairs and transportation are also costly as people age. Housing value shock, health shocks, liquidity shock, inflation shock, divorce shock, and portfolio shock. Who does not need a backup in retirement? What is your backup if you are thinking proactively? It is to have your clients start thinking about their house as an asset and put a reverse mortgage on it early, whether they use it or not.

Key Takeaways

The question then becomes: Can you justify ignoring a client’s major asset? Jamie Hopkins Esq., LLM, CFP®, ChFC®, CLU®, RICP®, Managing Director of Carson Group Coaching says, “The lack of focus on home equity in retirement income planning is nothing short of a complete failure to properly plan and utilize all available retirement assets. This needs to change immediately because strategic uses of home equity, especially reverse mortgages, can save many people from financial failure in retirement and help stem the overall retirement income crisis facing Americans.”

Many of you have broker-dealer sanctions against discussing reverse mortgages. If you would like to get the conversation going, the Academy of Home Equity in Financial Planning at the University of Illinois has published model language that some broker-dealers are using to make sure everybody is compliant with using home equity. 81% of Americans over age 65 own a home. It is there. You do not have to create it.

Key actions to take with clients and reverse mortgages:

- Differentiate your practice by providing advice on America’s No. 1 asset.

- Prepare your clients early for market turbulence, have it ready to go.

- Guarantee access to home equity throughout the retirement years. You do not know what the future holds. You do not know what home values are. You do not know what interest rates are. You do not know if reverse mortgages will even exist in 20 years. But if you set up a home equity conversion mortgage now, access to home equity is guaranteed by the full faith and credit of the US Government.

- Assist clients in financing a preferred home for retirement. Help them make that move.

- Suggest novel solutions to restore equity in housing at divorce. Everybody needs to know that who is in the financial services advice arena.

- Provide bridge income in Social Security deferral. We have to have people deferring their Social Security.

- Improve liquidity throughout retirement. You cannot guarantee – the banks are not necessarily going to be your friend when they are having liquidity issues.

- Focus on preserving cash assets for longevity and the estate. Protect that portfolio with another asset, coordinate, integrate all your assets.

- A reverse mortgage can be used to self-fund for long-term care needs.