The answer to both problems (and this is now becoming more generally known) is that you just do not take from your portfolio when it is down because what happens is if you draw from your savings portfolio in a down market, you are doubling down on the exhaustion risk. At the same time, what we have found is that you can use home equity, which is that other big asset that most retirees have, to supplement your retirement incomes.

Four “Archetypical” Retirees

Until last year, home equity strategies were typically thought only to apply to what is called the mass affluent, the retirees with high savings and home equities. In 2017, we came to the idea that we could extend that idea and apply the strategy to a much broader class of retirees, so we did research to see if we could apply this strategy to four distinct kinds of retirees. [Editor’s note: Sacks’ and Neuwirth’s paper, “Integrating Home Equity and Retirement Savings through ‘The Rule of 30’”, was published in the Journal of Financial Planning, October, 2017.]

We chose a large section of retirees that represented the wealthiest 50 percent of retirees because those are the people who have home equity. If you are below that level, you are just not going to have a home, and therefore, you are going to need to do something else.

What we also did was not just consider these retirees, but we also looked at different ratios of home equity to savings because the original study (“Reversing the Conventional Wisdom: Using Home Equity to Supplement Retirement Income”, by Barry H. Sacks, J.D., Ph.D., and Stephen R. Sacks, Ph.D., Journal of Financial Planning, 2012) only examined one class of retiree with one specific ratio. One of the key questions was, could we extend this strategy to classes of retirees that had different proportions of home equity and savings? It turns out the answer is yes.

We considered four different retirees. The first one (Retiree #1) which was the typical mass affluent retiree, is the kind of retiree that Sacks and Sacks addressed in their original paper. This is someone with a home equity of about $400,000 and retirement savings of $800,000. This is typical of somebody at the very top of the mass affluent, kind of between the 80th and 90th percentile of wealth in America.

While looking at the second kind of retiree (Retiree #2), we realized not everybody has that kind of balance between home equity and savings, so we consider it what we will call the “house-rich mass affluent”. This is someone who might be living on either of the coasts and just has not been able to save as much in their retirement savings because they have been paying their big mortgage, but this is someone with home equity of $800,000 and retirement savings of $400,000. Again, this is more typical of mass affluent retirees on the East and West Coasts.

We then said there is a vast number of employees, multiple of many tens of millions of more retirees who are below that level, and the question is, could we extend this to that kind of retirees? We considered a third kind of retiree (Retiree #3), one we will call the almost affluent retiree, and this is someone who has far less in retirement savings and far less in home equity.

We assume they are kind of typical of the same ratio as was considered in the past of someone whose home equity was only half of that of their retirement savings. We assume this person has home equity of $150,000 and retirement savings of $300,000. This kind of retiree has never been considered before in the literature, but as we will see, this strategy that Sacks and Sack originally developed can be a very, very powerful strategy to use to enhance retirement income.

Finally, we considered the house-rich, almost-affluent retiree, and this is somebody who has the same total level of assets, $450,000, but two-thirds of those assets are tied up in home equity. This is the one kind of retiree (Retiree #4) who can benefit most dramatically from the use of a HECM (home equity conversion mortgage).

In 2012 when Barry and Stephen Sacks did their original study, it was a different economic environment, interest rates were somewhat higher, and the kind of common wisdom on unexpected returns was somewhat higher than it is today. What we chose to do for consistency’s standpoint, just to make it more comparable to the prior study, was to use the same assumptions that were used in 2012 for this study. We did run sensitivity testing, which we will talk about. We will talk about how the results would change if you took a “more current view of the economy,” but recognizing also, that the old assumptions were the kind of assumptions that were used to develop the four percent rule. In fact, if you use the current assumptions, you would not have a four percent rule to compare things to. You would have to use a three percent or a three-and-a-quarter percent rule.

The Analysis: Two Strategies Compared

We start by establishing a reverse mortgage credit line or a HECM, the home equity conversion mortgage, which is the most common, most prevalent sort of reverse mortgage.

In the first year of retirement, the retiree is to withdraw from the securities portfolio. In each subsequent year, we see how the investment portfolio performed in the preceding year. If it performed positively, then we will withdraw from it, and the reason is to harvest those winnings. However, if it performed negatively, we had a bad result and then did not choose to withdraw from the portfolio. Rather, we wanted to allow it to recover. Of course, any retiree has to eat, and one of the ways they can do it is to get some money from another source. That other source would be the home equity line of credit.

The actual analytic strategy involves adjusting the cash flow only for inflation. Whether the portfolio went up by little or a lot or not at all, you always drew the same amount as the preceding year, adjusted only for inflation. The purpose is to maintain constant purchasing power because most people whom we are considering, most of their spending is not discretionary, so it makes sense to think of needing constant purchasing power, even if the portfolio has gone down.

We call this the coordinated strategy — that is, we look at how it worked last year. If it went up last year, we draw from it. If it went down last year, we draw from the other source, namely the home equity credit line. I would call it the coordinated strategy in the original article, and we called it strategy number one in our more recent 2017 article. Pete gets the credit for wondering whether it could be used to apply to other ratios of home equity to retirement savings.

Remarkably, with a surprising consistency, the article we wrote initially in 2012 — and the article that Salter and Evensky and others wrote in 2012, Wade Pfau in 2016, Jerry Wagner in 2013 — all of them somehow looked at a ratio of 50 percent, 0.5 to one of home equity to retirement savings. Actually, when you think about it, more people have more home equity than they have retirement savings.

Let us look at the other strategy, the conventional strategy. In the conventional wisdom, the retiree withdraws only from the portfolio, unless and until it is exhausted, and only then establishes a reverse mortgage credit line and then withdraws from it. Now, why is that? Why is that the conventional wisdom? The reason is that it comes from an old idea that once the house is paid off, you should avoid incurring any debt that impacts cash flow. The unique thing about a reverse mortgage is that you do not have to make any payments as long as you continue to live in the house.

So how do we implement the model? The model is implemented using spreadsheet analysis with Monte Carlo simulation. What we are simulating is the performance of the securities portfolio and inflation. These two spreadsheets run side-by-side, simultaneously, where everything is identical, including the investment performance of the portfolio, the rate of inflation, and the amount drawn by the retiree (because that is always an initial amount subsequently increased only by inflation). It does not matter how the portfolio does regarding what is drawn.

The only difference between the two spreadsheets that are run simultaneously is the strategy for determining whether the retirement income was withdrawn from the portfolio or the credit line. That is where the Strategy Number One is used or Strategy Number Two is used.

What do we use as input parameters for this model? You start with the initial value of the portfolio, the initial value of the retiree’s home, and the initial withdrawal rate. Consistent with the tradition of the four percent rule, it is what you stated as a percentage of the portfolio value, and the portfolio, which was assumed for both spreadsheets because they are identical, is a 60/40 stocks and bonds with annual rebalancing. We got data from various financial planners and investment managers that gave us the performance of those. In the 2012 article, we used historical data, which was fairly optimistic. In the 2017 paper, you will see results from both.

The focus of the analysis is on cash flow to the retiree, a constant purchasing power throughout a 30-year retirement. The Monte Carlo simulation runs 10,000 runs, and it runs a 30-year sequence of investment returns and withdrawals. Within a certain number of those repetitions, the cash flow is shown to survive for 30 years, and within others, it did not. For a given set of input parameters for each set, you will look at what the probability is: how many of those 30-year runs result in cash continuing to flow for all 30 years and if a set of parameters yields a 90 percent return. A 90 percent probability of cash flow survival — that is considered a successful set of parameters.

Obviously, if you put in a very low initial withdrawal rate, you are going to get a much higher probability of success, but the retiree will not enjoy his or her life as much. We are trying to find that sweet spot where the probability of cash flow survival is 90 percent, which means that it is as much as can be taken out to have that probability of enjoying life throughout a 30-year retirement. Anything less would be a higher probability of success but a poor lifestyle.

Key Findings

The first key finding is that Strategy Number One, the coordinated strategy, improves substantially over Strategy Number Two, with a far greater probability of cash flow survival. The second key finding was the interesting new result because the first one we found back in 2012.

For a particular initial withdrawal amount, as a fraction of total assets, if that results in a 90 percent probability of 30-year cash flow, then that same fraction of the total, that is home plus portfolio value, will result in a 90 percent probability of success across a broad range of both levels of total assets and ratios of home value to portfolio value, which is quite remarkable.

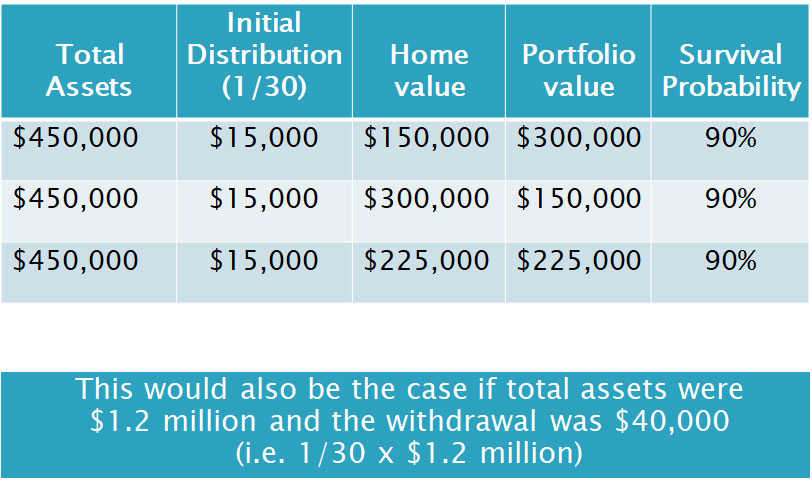

Here is, then, an example to illustrate that. The total assets in this picture are $450,000. Look at the central column. Home value varies, and by extension, the portfolio value has to vary because the sum of the two has to add up to $450,000. To figure the initial distribution, use one-thirtieth of that total, and you will get $15,000, the same figure. Each of those and many more in between gives you a 90 percent survival probability.

That is what we found. That is the consistency across a range of ratios. Across a range of values, here is another example below, which says that this would be the same case if total assets, instead of being $450,000, were $1.2 million, and the withdrawal was, again, one-thirtieth. That is where we got the name, Rule of 30. One-thirtieth of 1.2 million gives you a $40,000 annual distribution adjusted for inflation with a 90 percent probability of that continuing for 30 years.

This is the key finding, and the safe withdrawal rate can always be determined as a fraction of the total home value plus portfolio value. When the investment returns used in the Monte Carlo simulation are consistent with historical averages, the fraction is one-thirtieth. That is how we gave it the name Rule of 30. Currently projected investment return figures, which are more conservative because of the markets, are over-inflated, so the future returns cannot be expected to be quite as favorable.

There was also a recent revision in the parameters applying to reverse mortgages. The result, instead of being a Rule of 30, is a “Rule of 38”. Nonetheless, whether you are using a Rule of 30 with historical investment returns and historical reverse mortgage parameters or current figures using a Rule of 38 instead, you nonetheless get a remarkable consistency across a range of ratios and a range of values.

Observations Regarding Cash Flow

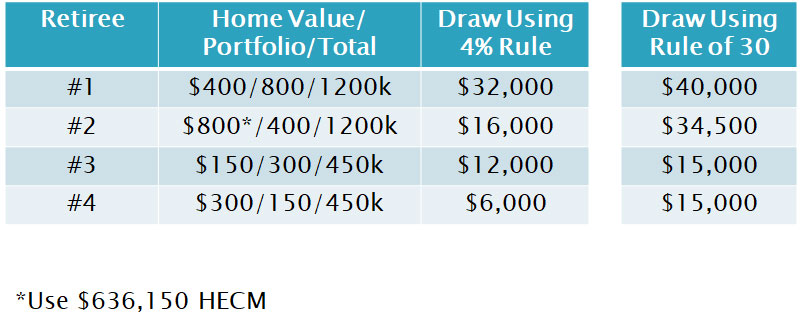

The most important takeaway from here I think, as a practical matter and for the retirement income crisis in general, is that retirees with only modest retirement savings who own a home (Retiree #4) can dramatically increase the retirement income without risking the exhaustion of their resources by using this Rule of 30, as well, if they use Strategy One. If you look at what Retiree #4 can take using the four percent rule, it is peanuts— less than half of what he or she could take under the Rule of 30 and much, much safer.

Historically, financial planners have been telling people like Retiree #4 that they can only have a few thousand dollars since they only have $150,000 of savings. In fact, this retiree could have $15,000 in retirement income, which would make a huge difference in his or her lifestyle. Again, the total cash flow for retiree four throughout the entire 30-year period using this approach is actually even greater. It is 30 percent more total cash flow. The annual draw is much higher, and the total cash flow is also much higher under this.

To put this in perspective, look at the last line in this chart. There are tens of millions of these retirees like this, and right now, financial planners are saying, if you are going to use a four percent rule, that may be too aggressive. Even so, you are telling people you can only take $6,000 a year. In fact, if you combine it with a reverse HECM and you use the coordinated strategy, you could increase that initial draw to $15,000 a year, which could make the difference, a huge difference, to retirees at that level.

We mentioned before that the total cash flow available under this strategy is 29 percent higher than under the four percent rule. Part of that is because HUD FHA guarantees that even if the ultimate HECM loan balance exceeds the value of the home, the retiree nor his beneficiary will ever have to pay back more than the value of the home. Essentially, the government is providing a backstop in a very, very important retirement security guarantee through their program. They are getting plenty of premiums. That is what their insurance premiums, which are part of the upfront cost of getting a HECM, pay for.

This combination of Rule of 30 and strategy one provides this much higher cash flow without the risk of exhaustion than using strategy two for all retirees. It is both the mitigation of the risk of the adverse sequence of return and the impact of this HUD FHA guarantee. As described earlier, these results are remarkably robust across a variety of assumptions and for retirees with different levels of home equity and savings. In fact, everywhere from 50 percent, up to 200 percent ratio of home equity to retirement savings, the Rule of 30 works well.

Just last October, HUD (U. S. Department of Housing and Urban Development) changed the parameters under which future HECMs may be issued, and these changes include two different things. One is a new insurance premium structure and slightly lower, what are called PLFs, which are “principal limit factors”. The amount that is available under a reverse mortgage is slightly less than it used to be before this October 2017 change, so we built that into the calculations that led to the Rule of 38. The other thing that led to the Rule of 38, since the Rule of 30 was developed, was that interest rates and general expectations of future investment insurance had declined.

Let us leave out the HUD rules for a second. Without them, investment returns, which are lower, would say that if you are drawing from a portfolio, only then you should not draw more than 3.2 percent as the initial distribution amount. Thereafter, the same dollar amount is adjusted only for inflation. That is the kind of basic cash flow premise that is used in all of these analyses.

The bottom line in this is that the more house you have in proportion to the portfolio value at the outset, the more the house can do to continue the cash flow to buttress and offset those negative returns that occur, those adverse returns.

Key Takeaways

What we can make of this research and what kind of the exciting opportunities and necessary opportunities are there for additional research?

There is other good work that is being done by people like the Society of Actuaries and many other financial planners and researchers Wade Pfau and others addressing ways to address the expense side of the equation, the extent to which additional employment is necessary, ways of optimizing social security and so forth.

What our research shows is that there are vastly greater numbers of retirees than have previously been thought that can benefit from the use of HECMs — in particular, the use of HECMs with a coordinated drawdown strategy.

While results are robust and consistent across different economic environments and for retirees with different ratios of home equity/retirement savings, the INITIAL rate of withdrawal is sensitive to economic assumptions. For example, there is the strategy of saying, let us use the HECM as a last resort, but still, let us take it out initially as soon as you retire. It is kind of as soon as you retire, that would be a combination of the two.

There are approaches where you use the HECM for tenure payments. You turn it into an annuity, which has the advantage of being simple, but again, it is not as effective as this coordinated approach. There are other uses of HECMs that we are not addressing, such as the use of taking out a reverse mortgage and then using for long-term care insurance as a way of downsizing and paying off existing mortgages and various other strategies.

To some extent, this is really just the opening of the territory where there is an enormous amount of research still to be done and strategies to be mapped and discussed because different ways of using HECMs might be more appropriate depending on a particular retiree’s situation.

One other thing became very apparent which was a little bit of a surprise to us as we pursued the research, was when we were looking at Retiree #4 in particular and realized just how critical those HUD FHA guarantees were to ensuring the long-term survival or protection against exhaustion of resources, we realized that this is a very important backstop to this strategy.

We think some additional analysis of these HUD guarantees need to be done. Preliminarily, we believe that it is not only an important government program, but it is actually well-funded via the premiums that are currently gathered. To some degree, HUD has been shooting in the dark and not knowing the level of premiums and the premium structure, whether or not it is going to be sufficient for the long term. I think that is manifested by the recent changes that HUD has implemented in these rules where the upfront premiums have been pretty significantly increased.

It is quite possible that there are going to be future changes in these rules, as well, and we need to be prepared for that. We need to be in close communication with the policymakers who are in charge of that. The bottom line is that it is not just the economic environment that is important, but it is also the HECM rules and the HUD themselves and how the lenders react to it. It is a dynamic, interactive situation, and as researchers and financial planners, we need to monitor, track it, and keep looking at it.

So, what are we leaving you with? What should you take away from this article?

- Rule of 30 is a reasonable starting point for retirement income planning. When a retirement planner sits down with a new retiree or a future retiree, think in terms of the total assets, including home equity and retirement savings and think about the Rule of 30.

- Think about the Rule of 38 depending on the investing environment or think about something in between.

- Also, make sure you monitor the regulatory environment. It can change quickly. It can have an impact.

- It is pretty clear that these HECMs, with their unique features, are worth utilizing and utilizing as soon as one qualifies. What history and research have shown is that taking out a HECM as soon as you retire is much more effective than waiting a long time.