Studies show that, first, for each investor, we need to find the suitable risk/return sweet spot. If we are working with a retiree who is 70 years old and has $3 million in the bank, we are not going to invest his money the same way we would invest the money of a 30-year-old with $70,000 in the bank. We know that markets are largely unpredictable, and therefore, it behooves us to diversify, diversify, diversify. At the very least, depending on the size of your portfolio and the complexity, we want to diversify within those stock and bond asset classes.

On the bond side, we want long-term bonds, short-term bonds, treasuries, and corporates. On the stock side, we want U.S., international, large-cap, small-cap, and perhaps value in growth and all different industry sectors. We know that costs matter and matter a whole lot. Keeping cost management fees to a minimum is critical. Trading, we know, has hidden costs. There are middlemen in there who take a penny here and a penny there. Of course, frequent trading often leads to unnecessary taxation.

Finally, we know that a portfolio needs to be regularly rebalanced; otherwise, your risk/return sweet spot can move too far from its original point. Rebalancing helps keep your risk in check, and, in the long run, by forcing yourself to buy low and sell high, you are going to juice your returns.

Integrating ESG Principles into a Portfolio

How do you integrate the ESG principles into the kind of portfolio that we have been talking about? Can you offer a financial plan to clients that genuinely excites them because it promises not only profitability but also to match their values and personal goals much more than any traditional plan ever could? The answer to that is yes, you can.

If you are a company manager, you should try to add these criteria to a business strategy. Why? Because you believe that sustainable companies can be more profitable, you want the world to be a better place, and you believe that business can play a role in making that happen. You want a company that will impact climate change as little as possible, perhaps help slow it. You want to limit your pollution and waste. You certainly want to refrain from doing anything to contribute to deforestation, rare resource depletion, or biodiversity loss. You are going to use renewable energy wherever and whenever possible.

On the social front, human rights, workplace safety, diversity in the workplace and on the board are important to you. You are going to engage with your local community. You are going to act ethically, whether it is here in the U.S. or abroad, where you might hire a subcontractor who is going to use child labor. On the governance front, you want ethical leadership, transparency in your company’s operations, and accountability. You want to make sure a company’s financial reporting is clear and accurate.

As investors, we will look to invest in companies that do this integration. We might invest in the company’s stocks or bonds. If it is not yet clear, the answer to the question as to whether ESG is a methodology or ideology, is that it is both. ESG factors have been taken into consideration since forever. It is an integral part of due diligence. How can you invest wisely without knowing whether a company may be subject to IRS fines, labor unrest, worker lawsuits, consumer boycotts, or higher cost of capital because of investor disgust?

You want to know how loyal customers are, how loyal a worker is, and how clean their books are. As for the environment, the bankruptcy of Pacific Gas and Electric, PG&E, just a few years ago shows that you cannot ignore liabilities resulting from massive wildfires. A company’s sustainability is critical to successful investing in the long run.

How Did the E, the S, and the G Come Together?

Where did this come from? Although it did not come from one place at one time, in 2006, the United Nations introduced an initiative called the Principles for Responsible Investment. That is really where the term ESG started to become popular. The U.N. launched the Principles for Responsible Investment as a set of voluntary guidelines for incorporating ESG factors into investment practices.

Here is the beginning of the mission statement for the Principles for Responsible Investment.

“We believe that an economically efficient, sustainable global financial system is a necessity for long-term value creation. Such a system will reward long-term, responsible investment and benefit the environment and society as a whole.” That does not differ very much from what Adam Smith said in 1776. He said capitalism, the invisible hand, and the free market would benefit investors, labor, consumers, and the world’s nations, which is why he called his book Wealth of Nations, not Wealth of CEOs. In Smith’s words, capitalism should “benefit the overall interest of society.” Now, Smith was not an economist because economics had yet to be born. He was a philosopher.

Two hundred years later, in the 20th Century, the most highly respected economist, John Maynard Keynes, also talked much about sustainability. As one biographer of Keynes, Eric Berr, said, “Numerous writings of Keynes contain the premises of sustainable development. Our positions on uncertainty, money, and economics are consistent with a strong sustainability-based approach.”

Why is ESG Then So Controversial Today?

The U.N., Adam Smith, and John Maynard Keynes all said that businesses that are successful in the long run tend to improve the lot of humanity. It is a feel-good sentiment. Who could be against it? Yet today, ESG has just become very, very controversial. I am going to review at a high level the points of controversy, and then we are going to go back to each one and look at it in some depth.

Perhaps the largest controversy, and the one that concerns some the most, is the profitability of ESG. Can an ESG portfolio be profitable? Some argue that a company’s primary and only focus should be on maximizing profits. They fear that ESG integration negatively impacts financial performance. Adherents to ESG, on the other hand, say that ESG criteria enhance due diligence and, like Smith and Keynes, say that sustainability is key to long-term profitability.

Some say that ESG is poorly defined, has some points of subjectivity, and lacks investing standards. Others point to “greenwashing.” They say ESG is most profitable to the ESG raters and fund companies. Finally, ESG, in the last few years, has been accused of being woke.

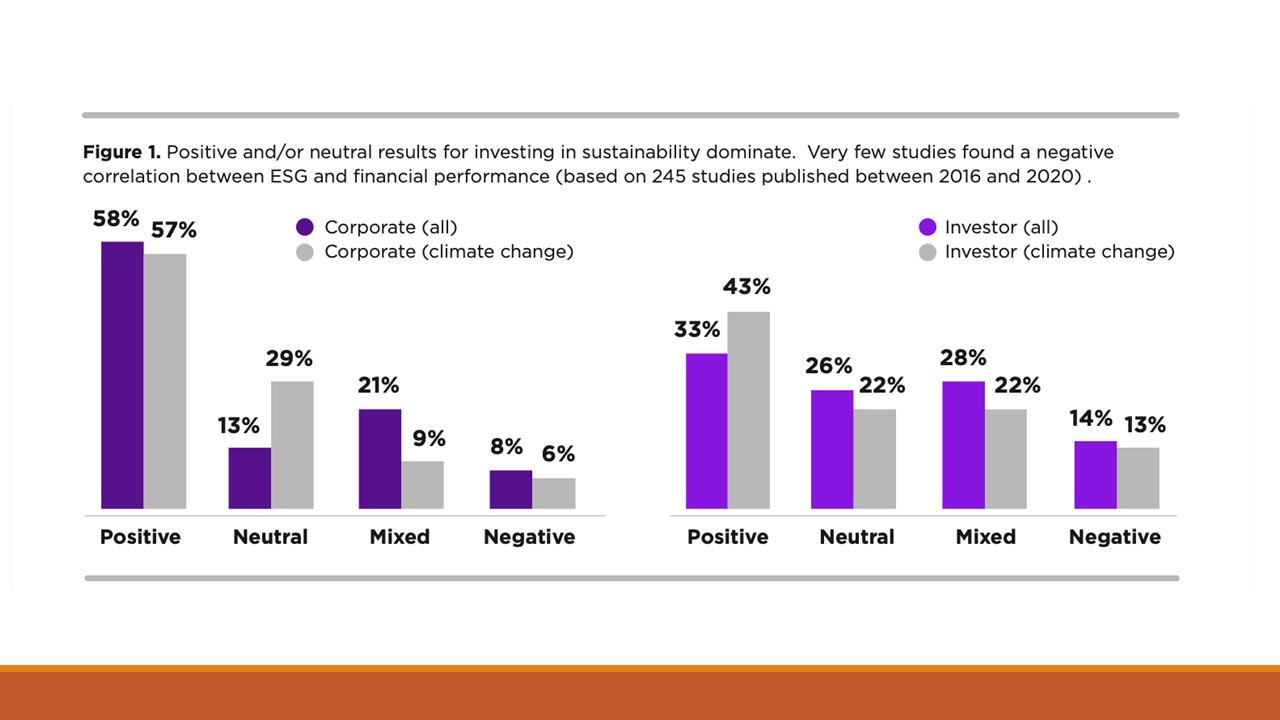

Let us look at all of these controversies, starting with profitability. The most expansive, in-depth study I know of was done by New York University (NYU) Stern School of Business in 2021. They looked at 245 studies, but among these studies were many meta studies that included dozens of studies. They looked at virtually every respectable study done about ESG between 2000-2022. Below is what they found.

Twenty-eight percent of the studies showed that corporations that pay attention to ESG criteria are more profitable in almost six out of 10 studies and less profitable in less than one out of 10 studies. About 13% of the studies were neutral, meaning whether they adhered to ESG or not, those companies tended to make about as much as other companies in the field. It did not matter much. Twenty-one percent of the studies had ambiguous findings, unclear which way they went.

The gray lines are those are companies that focused on climate change. You can see that the numbers do not change that much. Companies that focused on climate in 57% of the studies were more profitable. Only in 6% of the studies were they less profitable.

It is fairly clear that companies that pay attention to ESG are maximizing profits. Those who argue otherwise and say a company’s primary and only focus should be on maximizing profits often cite Adam Smith without having read Adam Smith. They say that a focus on ESG can lessen profits, but the studies do not show that to be the case. The opposite is the case. Companies operating sustainably are overall more profitable, as indicated by six out of 10 studies.

Why are these companies more profitable? According to the NYU Stern researchers, it is because they have better protection from risks. For instance, had Pacific Gas and Electric been looking more closely at the risk of forest fires, they may not have gone bankrupt. There is also more innovation in these companies. They have lower costs due to recycling and reuse. They have better labor relations and more loyalty among consumers. NYU followed up their study with another study that showed that in recent years, consumer products labeled as sustainable have grown at twice the rate of conventional products despite an overall price premium of more than 25%.

Do ESG Investments Perform Better?

If we invest in these companies, will we do better? Warren Buffet has often said, “Great companies do not necessarily make great investments.” The kind of companies we want to work for in exciting industries, moving forward and earning profits, are called growth companies. Actually, throughout the course of history, they have underperformed value companies. The question is, are these companies more profitable for investors?

The same NYU study above found that the answer is yes, but not quite as powerful. Thirty-three percent of the studies found that investors with ESG portfolios do outperform the market at large. Only 14% of the studies found that ESG investors earn less. A lot was in the middle. A lot was ambiguous. Twenty-six percent showed that whether you have an ESG portfolio or not does not matter, and 28% of the studies were uncertain. Focusing on climate, the numbers become stronger.

I get it that ESG companies are more profitable. Here, I am not so sure.

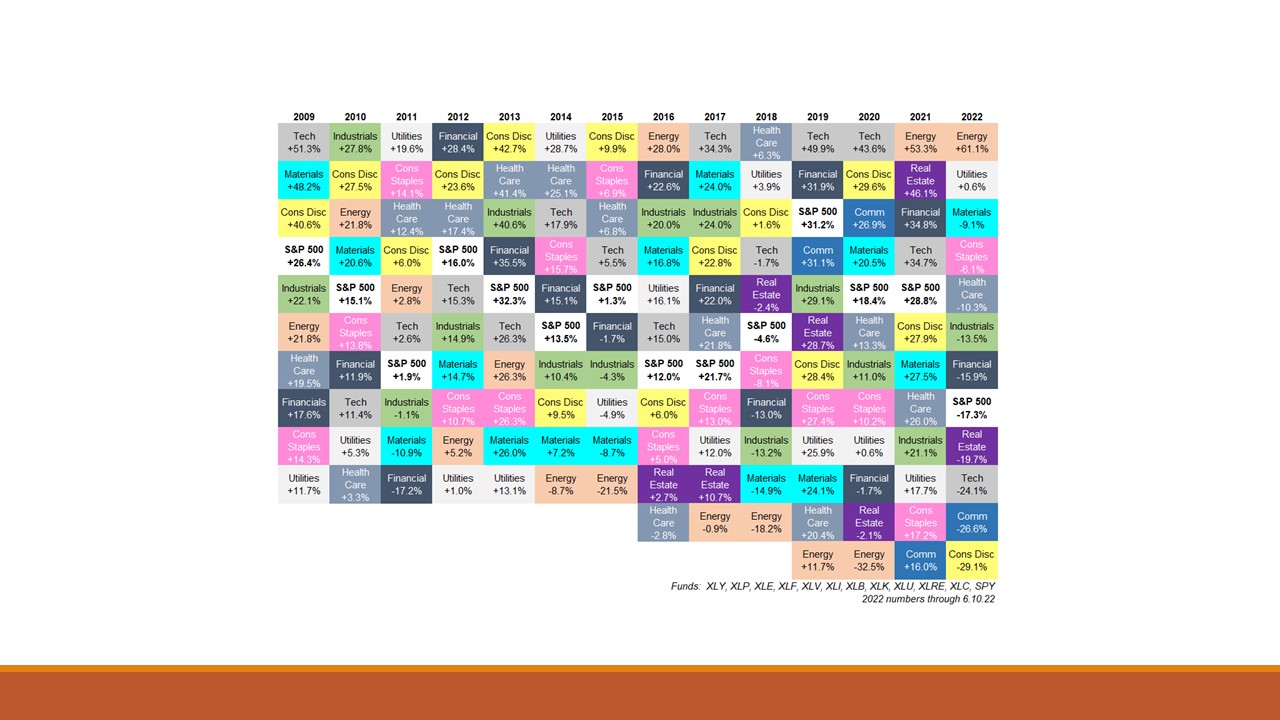

You may have seen one of these Skittles charts before. Each of these colored squares represents an industry sector within the United States. It shows how they perform vis-à-vis other industry sectors every year. The NYU Stern study looked at studies between 2016 and 2020. It just so happens that in four of the five years before 2021, the energy sector was the lowest-performing sector of all U.S. sectors.

If the study were done now in 2023, when in the last two years, the energy sector outperformed all other sectors, we might see different results.

In the end, whether you invest in ESG or not, keep in mind that it is a mushy term. In the long run, you cannot plan to underperform or outperform the market at large. In the long run, those things we looked at earlier, costs, diversification, rebalancing, and proper risk-taking, are all going to be much more important than whether you go out of your way or not to overweight or underweight ESG companies in your portfolio.

Other Controversies and ESG Funds

One of the strategies with ESG funds is to do what is called “negative screening.” ExxonMobil and Chevron will often be underweighted or eliminated from portfolios. Well, the energy sector is only 5% of the U.S. economy. Whether you underweight or overweight that 5% position, provided you have a well-diversified portfolio with lots of other industry sectors, it is not going to matter that much.

Now, let us look at the next controversy, which is ambiguity in ratings. ESG ratings are all over the map because some ESG rating firms, such as ISS, MSCI, Sustainalytics, Bloomberg, and S&P Global, emphasize E over S. Others emphasize S over E. Some of them look at absolutes. That is, they will include in their portfolio the best in class, the best petroleum companies, and the best pharmaceutical companies. Others are going to look more absolute. They will include the companies that emit the least greenhouse gas and eliminate those that emit the most.

The ratings are improving, but you will get different opinions. You will not get the same reviews, just as with car ratings and Consumer Reports versus Car and Driver. The difference in ratings does not make them useless. They are still helpful. Just last week, I was out shopping for a nonstick pan, and I looked at the reviews on Wirecutter. I looked at the Amazon reviews. I talked to the salesman in my local cook shop. They all had different reviews, but they were all helpful to me in making my decision.

Another controversy is greenwashing. No one can deny that ESG has been and continues to be used as a sales tool. In some cases, deceptively so. Companies say they have lofty targets to eliminate CO2 emissions by 2030 or 2035, but then they do nothing. Fund companies sometimes do very minimal screening and then charge more for funds simply because they have ESG in the name.

You must take note of flooding coastlines, droughts, and forest fires related to climate change to invest wisely. As a recent Goldman Sachs statement put it, events like oil spills, water contamination, and improper waste disposal, which can be mitigated through environmental controls, not only carry substantial headline risk but also can be a major detriment to the bottom line. Due diligence in fiduciary standards requires consideration of many factors. You cannot focus on ESG factors alone, of course. Nor can you neglect to address ESG factors, which are more than pertinent to the bottom line.

Can ESG investing do something to slow or halt climate change? Can it bring more social justice or slow the world’s deforestation? Yes, I believe it can. It is very well documented that consumer and investor actions throughout the years have brought positive social change.

Practical Advice for Financial Advisors and ESG Funds

Yes, there is a lack of standards. Yes, there is greenwashing. Yes, there is a whole lot of misinformation out there. Still, there are many avenues to use ESG as part of a successful financial planning process. You need to know how to avoid the pitfalls, make the right moves, and, above all, you need a strategy.

The decisions you always make in investing are certainly pertinent to building an ESG portfolio. You must decide, first of all, whether you are going to invest in individual securities or funds, mutual funds or ETFs. Are you going to go with an active approach or a passive approach?

Beyond that, you must decide what ESG strategy you will use. The most common strategies are:

- Negative screening

- Positive screening

- Direct engagement, and

- Proxy voting.

You can use one. You can use two. You can use three or all four.

Negative screening is perhaps the most common. Negative screening means, as we discussed earlier, you are underweighting, or you are eliminating what you consider to be the most poorly rated ESG companies. By the way, Morningstar Direct does a very good job of looking at funds and rating them as to how well they address ESG issues.

Positive screening is the opposite of negative screening. You are going out of your way to find dynamic companies that are perhaps using or developing new forms of alternative nonpolluting energy or figuring out ways to clean the oceans of plastics. With negative screening, you are looking for companies to eliminate, such as polluting coal companies or companies that subcontract out to far Eastern concerns that hire child labor.

Direct engagement means you are engaging with management to make sure that they are setting ESG goals, and they are achieving them. Proxy voting means you are voting for proxy measures that will make the company more of an ESG company.

Whether you go with funds, whether you go with individual securities, regardless of which strategy you use, screening or direct engagement, you want to educate yourself first. These are some very good sources to educate yourself. Gitterman Asset Management has online courses. The Sustainability Accounting Standards Board offers education and certification. Harvard Business School offers a reasonably priced six-week course on sustainable investing. Now, the CFA Institute, which we are all familiar with, offers a certificate in ESG investing.

If you go with funds, the question always is, do you go with an active approach or a passive approach? If you go with the active approach, these fund companies here, Brown Advisory, Calvert Group, Domini, Franklin Templeton, Impax Asset Management, Invesco, Northern Trust, Nuveen/TIAA-CREF, and Parnassus all have a good track record of running actively managed ESG funds, both ETFs and mutual funds. They are not guilty of greenwashing. You can have trust. They have, by and large, very good track records. If you are going to go with an active approach, you can do a lot worse than going with one of these companies.

There are certainly many more, and you might start with Morningstar and Morningstar Direct and look at their suggestions for which fund companies they give the best ESG ratings to. Now, one caveat. I am the author of not only Bond Investing for Dummies, but Index Investing for Dummies, and ETFs for Dummies. I am an index investor at heart because study after study shows that index investors, in the long run, do better than active investors.

If you go with an active approach, you are probably going to do a little better as far as having an impact on the world at large, but in the long run, you may underperform the market. Even though some of these companies have great track records, over the long run, you may underperform the S&P 500. I do not think it would be by very much, but I do have to throw out that caveat.

You can go with a passive approach, such as low-cost index funds that use ESG indexes. There are, however, different companies to consider, and they are both good and bad. I look first at these companies here that have high ratings from Morningstar, that have studies that show that they do vote their proxy votes in favor of ESG proposals as opposed to these companies that do not.

One thing you should keep in mind is that ESG is not the Three Musketeers. It is not one for all and all for one. You can focus on E, on S, or G, or none at all. It is not impossible to vote for your values. You do not have to go for the whole United Nations ESG package. There are plenty of funds out there that offer you the option of voting, just going with E, or going with S. If E is more important than S, environmental concerns are really where your heart or your client says, “I am really concerned about global warming,” you can choose one of these low-cost ETFs. KraneShares Carbon Strategy ETF, Invesco Global Clean Energy, or Xtrackers US Green Infrastructure Select Equity ETF.

If S is more important to you than E, there are plenty of funds to choose from, such as the YWCA Women’s Empowerment ETF, the BNY Mellon Women’s Opportunities ETF, and Impact Shares NAACP Minority Empowerment ETF.

Solid investing and due diligence on the part of advisors always has and always will incorporate ESG factors. It is not some strange, extraneous thing. Companies that operate sustainably have high ESG scores and tend to be more profitable. ESG investing should incorporate all the basic do’s and don’ts of fundamental investing. The E, the S, and the G can be grouped or separated. They are not like the Three Musketeers, all for one and one for all. You can invest your values.