Clarification on terms I will use in this article:

- By IRA I mean traditional IRAs, Roth IRAs, 401(k)s, 403(b)s—basically, any ERISA-based plan.

- There are two similar terms out there: one is required minimum distributions, and the other is minimum required distributions. I will refer to them as RMDs.

- Custodians or plan administrators or the plan manager will be referred to simply as the “custodian”.

Who Should Use a Retirement Plan Trust?

With qualified retirement plans, good planning usually means one plan for everything else and a totally separate plan for qualified retirement plans. They can become the biggest problem asset after death because they have different distribution rules and different tax rules than any other asset. Most people just do not get the significance of that.

Say a client is concerned that the beneficiary would not make good choices regarding distribution. Either the beneficiary is irresponsible, or they are too young to make good decisions. Many times, a 22-year-old kid may be smart. They might have had a 4.0 in college, but they do not yet have any experience in the world and understand the significance of avoiding taxes and enjoying tax-free growth. Alternatively, they are concerned that a beneficiary would lose part of their inherited IRA in a divorce, a bankruptcy, or a lawsuit (a very state-specific issue).

Texas law is one of the most favorable in the nation. Under Texas law, inherited IRAs are protected from bankruptcy and lawsuits. However, they are not protected from divorce. No state protects them from divorce. With most states, inherited IRAs are not asset-protected. There are only seven or eight states in the US that protect qualified retirement plans and IRAs in particular when they are passed on. Inherited IRAs for minor children are particularly problematic. I have seen many people just put a minor’s name on a beneficiary designation.

If the plan owner is incapacitated, how do you get a signature to get authorization to do anything? Do not expect a normal power of attorney to work. My experience with financial institutions is, the larger they are, the less likely a normal power of attorney is going to work. Asset or investment changes are times when we might need a signature, such as if we need a change in beneficiary designation, or if they are going to convert the plan to an IRA, particularly a Roth IRA, or if they need to change custodians, especially if a custodian has become uncooperative, or if they need to take RMDs. You usually need a signature for all of that.

The cost of one year’s guardianship is way more than the cost of using the retirement plan trust. That is really the cost consideration in a case like that. You may also have a beneficiary who qualifies for a governmental assistance program, and inheriting the IRA would cause them to lose those governmental benefits.

Second marriages really complicate QRP planning because you are bound by certain rules as to who can be named and whether the spouse has to do a waiver. If there are children from before the marriage, and a person wants their spouse to benefit while the spouse is alive, but then they want to go back to their prior marriage children, the only way to do that is through a retirement plan trust. If the spouse does a rollover, those kids are never going to see it. If a family has $200,000 or more in qualified retirement plans and you do a cost-benefit analysis, it is basically a no-brainer. It might worth the cost of the trust with as little as $150,000.

For young couples who have children and growing 401(k)s, this is frequently a big problem asset. Minor children also complicate QRPs. If there is any chance that minor children would be the beneficiaries, they really need to think this through.

If the plan owner had yet to take the RMD, the inherited retirement plan beneficiary has until September 30 the year after the owner’s death to decide how to take it. There is no real reason to hurry this decision. They always have from nine to twenty-one months. However, my experience is that many custodians treat this like somebody has pulled a pin on a hand grenade and tossed it in their office.

There are penalties for making wrong choices that cannot be abated. You cannot tell the IRS my accountant or my custodian or my financial planner or my attorney gave me bad advice. The IRS is not going to waive penalties for that. It is always important that the client depend on professionals hired by the family and never depend on the custodian. Sometimes custodians just give bad advice. Clients have no recourse against them. They do have recourse against financial planners, attorneys, and CPAs if they hired them.

A Trust Well Done

A poorly drafted trust or an improperly done beneficiary designation form can be a disaster for any kind of plan that depends on a beneficiary designation form. Trust drafters should be attorneys who are familiar with drafting trusts as beneficiaries for retirement plans. Many attorneys who may be great estate planning folks do not deal with this area. Relatively few estate planners do these types of trusts. Trust drafters should understand the nuances of beneficiary designation forms. I cannot tell you how many times attorneys have had me look at their forms, and I have to tell them that their form actually does not comply with the law.

Attorneys should also be willing to work with the custodian. It is a real problem if the trust drafter and the custodian cannot get along with each other and will not talk to each other.

Typically, custodians give three choices:

- They will accept the drafter’s beneficiary designation form, or

- They will accept a concept that is required on their own forms, or

- They are not going to allow the concept. The answer here is that you get another custodian.

The mother of a friend of mine died and had a $500,000 IRA. Greg and his sister, Anne, were the recipients. Greg took the IRA because the custodian asked him what he wanted them to do with the account, and he said, “Just send me a check.” Then he wrote his sister a check for half of it. The following April Greg called me, and says, “My CPA is saying I had $500,000 of income last year. He is an idiot. Why would he say that?” I realized that he had taken the check and cashed it, and then written his sister a check. I told him that he had taken a $500,000 distribution and owed income tax on that.

This is a case where the IRA can turn into a large IOU to the IRS without careful planning. Taxes are not the only problem, though they are certainly a big problem.

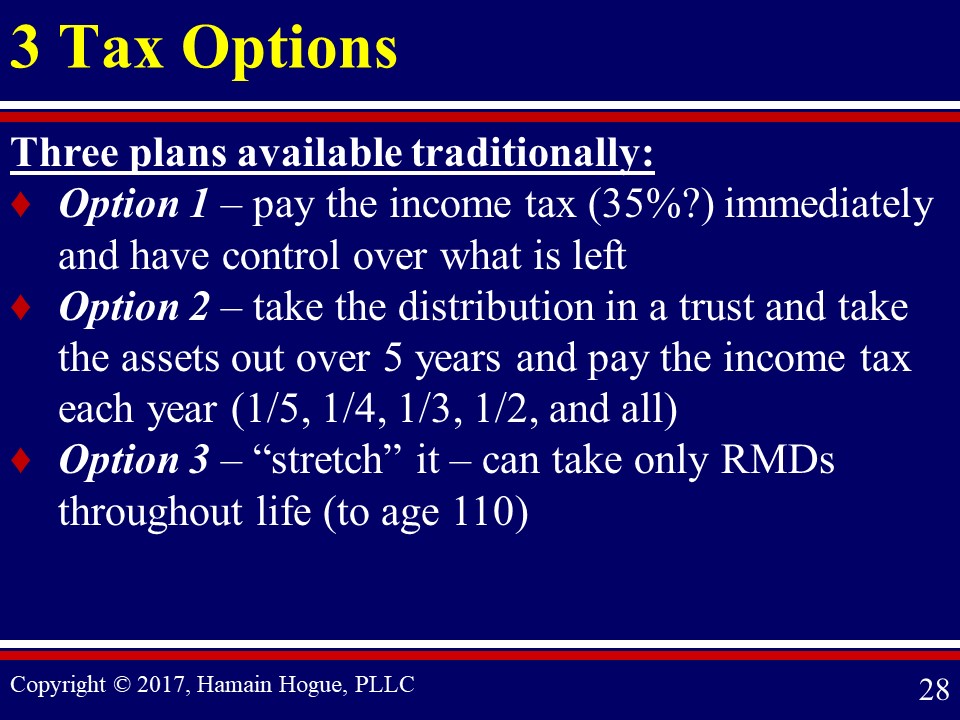

Tax Options for Beneficiaries to Receive Distributions

In January of 2003, the IRS created new minimum distribution rules that allow for longer tax-free compounding. They also made it easier to calculate RMDs. But what happens on death when there are assets remaining in the plan? There are three options.

With Option No. 1, the beneficiary can pay the income tax, let’s call it 35 percent immediately, and have control over what is left. As stupid as that may seem to us as professionals, many people will just go ahead and pay the tax, and do what they want with it. That is a very bad strategy when it comes to IRAs.

Option No. 2 is a trust named as beneficiary. If the trust has language in it, then you can do a five-year payout. That means that you take one-fifth the first year, one-fourth the second year, one-third the third year, half the fourth year, and all of it in the fifth year. For tax purposes, that is how the tax rates calculate it.

Option No. 3 is to stretch it so that the beneficiary can take the RMDs throughout their life, and they can stretch it to age 110. The beneficiary is going to calculate how many years by taking 110 minus their age. For the first beneficiary, that is as long as it can be stretched. That is an important consideration in planning.

Let us look at an example. Harry is married, and he has one child. He has a $250,000 IRA. He turns 70.5, and he must start taking RMDs. With good planning this IRA can become worth over $2.5 million. When I am talking to somebody about that age, and they say, “My IRA is not that big,” I tell them, “Well, you might be sitting on a goldmine and not realize it. It could be worth a lot of money if you manage it and plan it correctly.”

Let us see how that might happen. The current amount is $250,000. Harry takes distributions from required minimums only to age 86. He takes out $281,000, but that leaves $327,000 in it. Then his wife takes distributions for another four years. She takes almost $89,000. Then on her death, there is $330,000 left. They took out almost $370,000, and there is still $330,000 in it. If they do not do any planning at the wife’s death, roughly 35 percent is going to be paid in income tax, or about $115,000. If there is estate tax on top of that, that total is going to be $191,000. There is only $139,000 left for the family. That is pretty sad on a $330,000 IRA. I have seen things like that happen.

Option No. 2 is they name their living trust as beneficiary, and they do a five-year stretch. Let us assume they are going to get a 6 percent return. That generates payouts of about $66,000 the first year, then $70,000, $74,000, $78,000 and finally $83,000. That gets the family about $741,000.

Option No. 3 is good planning. We go back to the same $330,000 IRA, and now they have decided they are going to give half to their son and half to their grandchild. The son takes out required minimum distributions for 27 years on his half. He takes out $521,000. Then the grandchild takes out required minimums of another $1.6 million. We now see that from the $250,000 IRA, the husband and wife took about $370,000. The son and the grandchild took out another $2.1 million, so the total to the family is over $2.5 million. Once I sit down and show people this, they get real excited about maybe doing something for a grandchild.

But it at least makes them consider that as a possibility. Now in 2005, there was a private letter ruling (PLR) that allowed trusts to be the beneficiary and do a stretch out. Up to that time even though the law allowed it, every time we named the trust as a beneficiary, the custodian would tell us the individual can take it out and do a stretch, or we will do a five-year payout. We would point out we have got the language here that allows us to do a lifetime stretch, but the custodian would never allow it. After this case, custodians started allowing it.

I am going to say that our experience over the last two or three years is that 97 or 98 percent of the custodians will now allow a stretch through a trust. Generally, the beneficiary can use their own life expectancy. It does depend on how that trust is drafted. But the way we do them, each individual beneficiary has her own separate trust share. They get to use their own life expectancy. Many people know that PLRs are only valid to the people who applied for it. But the ruling has been affirmed over 500 times since then in other PLRs, and it is not going away.

Even in the new tax proposal, there is something about this in there, but it is not going away. By now, this is well established in our law. But the stretch is not automatic. I have people say so that this just automatically happens. I tell people there is nothing in estate planning that is automatic. Something must happen to trigger it. You have to do something to exercise the options. That means the beneficiary must make the right options, and the beneficiary must handle it the right way.

Qualified Retirement Plans Can Create Estate Problems

Here is a planning opportunity for you: A lot of company-sponsored QRP custodians do not allow stretches beyond five years in those ERISA plans.

They do allow them in IRAs. So why do company-sponsored QRP custodians not allow them? Many times, they do not know the rules. Sometimes they are willing to administer the rules according to the law, especially if it is an employer’s plan. They do not want the liability. They feel like somebody pulled the pin on a hand grenade and tossed it in their office. They want to get rid of it. Unfortunately, there is no way to force them to abide by the law. You have to find out in advance whether they are going to accept it. One reason rollovers to an IRA can be so important is because you get to pick the custodian.

If you can pick the custodian, you can pick one who will go along with this. If the client does not do anything, they are not going to know there is a problem while they are alive. Many people do nothing other than sending in a beneficiary designation. If that is all they do, they just have to hope it works when they die. They are not getting any feedback from the custodian. But unfortunately, that can handcuff the beneficiaries upon death. They could be forced into what we call the blowout problem. With any sizable QRP, it does not make sense for a beneficiary to take more than they are required to any sooner than they must. A blowout occurs when the QRP is subject to an unnecessarily high income-tax rate because so much is taken out at one time. Many things can cause it.

Here is an example. Luke’s father left Luke a $500,000 IRA. Luke had never had that kind of money, never seen that kind of money, never managed that kind of money. So now he is rich. He increases his lifestyle and buys a lot of new stuff. Now he has $500,000 of income in one year. Unfortunately, he did not realize the tax bill is going to come due the next year, and this, by the way, was a real case in our office. In two years, he went from having a $500,000 IRA to nothing left at all. In fact, he even had some debt to the IRS because he did not have enough cash to pay the tax.

Another thing that can come up is the spouse of the beneficiary or a third party wants to spend the money. There is one question that is always important to ask when you are planning for the parents and they have adult children who are married: is your son’s wife a good or a bad influence on him over money, or your son-in-law a bad influence over your daughter? Many times, they will say they are not a good influence.

Another example: Angie’s mother died and left her a $400,000 IRA. Jack said to Angie, “Honey, I have always wanted my own business. If you really love me, you’d let me invest this in a business.” You cannot legally borrow from the plan, so they take a $400,000 distribution. Now they can “borrow,” but they can only do so once every 12 months, and they have to pay the entire amount back within a 60-day period.

Let’s say that they “borrow” on April 1 and make the first withdrawal. That means they only have until about June 1 to pay the whole thing off. That catches people by surprise because they do not understand the 60-day rule. In this case, the tax was $107,000. Unfortunately, Jack was a better dreamer than he was a businessman. The business was unable to pay. The business went bankrupt, but they still owed the tax. Angie’s mother left her an IRA that could have been a huge benefit to her in retirement. Instead what she got is $107,000 that they owe the IRS.

Custodians often do advise the beneficiary of the rules. The beneficiary rolls the IRA into his own IRA. Once it goes to the beneficiary, it is not the custodian’s problem. The beneficiary feels rushed into making a decision. I know that happens. I have been through it personally. They are not aware of the rules and the choices. If someone is getting information only from the custodian, they are not getting good information. They often think it is not subject to estate tax.

But that may not be true. Fred was the son of one of our clients. Fred’s dad left him a $600,000 IRA. Fred’s dad died in January. Sometime in February, Fred talked to the custodian, and he asked, “Can I roll this into my IRA?” You might be surprised to hear that the answer is yes, you can. That is a technically correct answer, but it is misleading because when you do that, it is a $600,000 distribution. Fred does this, rolls it into his IRA, and the following April, he is doing his tax return. Then a CPA informs him that he has $600,000 more income, and owes an additional $218,000 in tax.

The only place that Fred keeps that kind of money is in his IRA, so he has to withdraw it from his IRA. The problem is he is not 59.5, so he suffers a 10 percent early withdrawal penalty. That is another $21,800. And that means that the total amount of tax that goes to the IRS is about 40 percent.

What Can Go Wrong When an Individual is Named the Beneficiary

A beneficiary can stretch it out. That is still not perfect. Even if the beneficiary is very responsible, there are still seven things that can go wrong when you name an individual.

Let’s look at another case. Jake had a couple of grandkids he adored, and he and his wife decided to leave their grandkids $50,000 each from an IRA. One of these kids is five years old.

Unfortunately, Jake’s daughter and her husband went through a very bitter divorce. They each convinced the court that the other was a spendthrift. Neither one was appointed the guardian of the estate for the grandchild; a bank got appointed. They had to go through a guardianship of the assets because the 5-year-old cannot legally own money or anything else for that matter. Twelve years later, there was nothing left. This $50,000 that could have been a huge benefit to this grandchild instead just winds up being a financial burden on the family. That is probably not what Jake had in mind.

If instead Jake had done a retirement plan trust, the 5-year-old would have had to start taking required minimum distributions but it would not have been in a guardianship; it would have been in a trust. If he took required minimum distributions only to age 65, he would have been paid almost $700,000. But there would still be $805,000 left in the IRA. That $50,000 could have become over $1.5 million if it had been handled in a trust instead of done directly.

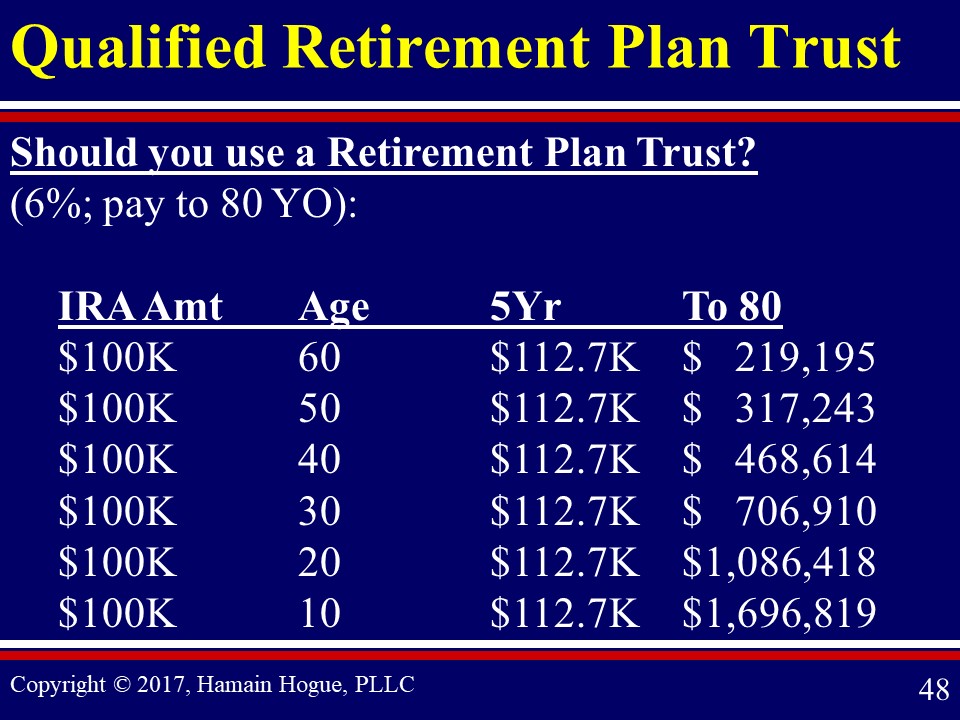

Here is a chart that illustrates two things. Using a 6 percent rate of return, we are going to compare IRA amounts of $100,000 and look at various agents and beneficiaries. Next, we are going to compare a five-year payout at 6 percent to taking required minimum distributions to age 80.

Let’s say the client is 85 years old. Does a retirement plan trust make sense when they are going to give it to a 60-year-old? Look what happens.

If the 60-year-old gets the $100,000 immediately, they pay income tax immediately. They are going to get a benefit of $65,000 or so. But if they take the stretch over five years because mom and dad used their trust, earning 6 percent, their total benefit is going to be about $112,000. But if they take required minimums only to age 80, between what they will get paid and what is left in it at 80, they get $219,000. You can see that the retirement trust produces a benefit of $100,000 more than if they just took it outright. The lower the beneficiary’s age, the greater the benefit over doing either the five-year payout or the outright distribution.

Look at what happens when a 20-year-old gets it. You are talking about over $1 million in benefits or more than ten times. When it is a 10-year-old, 17 times the benefit. When you are considering planning for retirement plans, look at the age of the beneficiary. If the client has any inkling that they might want to benefit grandchildren, this is a great place to do it because they can control what happens for many years into the future, and it would still be a huge benefit to the grandkids.

Why Do a Retirement Plan Trust versus Name a Beneficiary?

People will ask me why I would do the retirement plan trust instead of just naming a beneficiary. When we ask clients, “Do you want to do the stretch or do you want the asset protection?”, their answer is, “We want both.” The retirement plan trust is a tool that allows them to do both.

- You can do the stretch out in a trust. And because you can do it in a trust, you can asset protect it. Depending on the state of the beneficiary, if they take it outright not only might that asset not be asset protected but it is a very attractive target to a creditor because it is cash. They can go spend it quickly. If they are involved in a lawsuit, whether it involves their business or a car accident or anything like that, that asset is at risk. If it goes into a trust, they get to protect it. But if they are stuck with a five-year payout, economically that is not as good as being able to do a lifetime stretch.

- Divorce can be problematic. Parents do not really think about how it may affect their children. If you leave your son or daughter a retirement trust, and they take it individually, one of the things that is happening in a state like Texas is that as those distributions come out, they are community property.

- Another problem will come up when distributions come out and go into a joint account. That income is community property. The child decides I am going to go put that in with my other separate property because, after all, I inherited it. That inheritance is not normally subject to spousal claims on divorce. But you have now co-mingled it. You have got income, which is community property going into a separate property account. Under Texas law, that is presumed to be community property. Unless you can prove otherwise, it is going to be treated as community property.

Key Takeaways

Let’s talk about some takeaways. Hopefully you see from this that dealing with retirement plans can be very complex. There are many issues involved.

- Retirement plans pass by a completely different set of rules than other assets. My experience with planners and clients is that that just comes as a surprise. They think it passes by beneficiary designation, the same as life insurance. That is about the only connection between them. They do pass by beneficiary designation.

- Because of the income tax rules, the fact that you have got to take those RMDs and you have got to make choices about how you are doing it, it is just a totally separate deal than every other asset.

- Every other asset we can put in a trust. We can asset protect it. It can grow. That growth is not part of the marital income. You can do it in a retirement trust, but you cannot do it with just a retirement plan. The different rules create potential problems, but there are also planning opportunities.

The retirement plan trust is a great option. Because it is so flexible, it fixes a lot of the issues that come up today. Here is something else that I have learned: Many times, when we meet with clients, their planner has done a great job. They have $1 million in their IRA. But the client has never heard about a retirement plan trust.

Whoever teaches your client about this tool is likely to be the person to manage the assets. We are not in the asset management business. We are not going to take over that job from you. But there are some attorneys out there that they will refer to their own group of planners that they work with. We take a very different view of that. We are happy to work with any planners. We are not going to refer your clients to another planner. But it is important that you be the one to bring this to your client’s attention because, if they hear it from somebody else, that person gets in the driver’s seat to take away the management of their assets.