Changes Made by the SECURE ACT

The SECURE Act is the most comprehensive piece of legislation that affects IRAs after the Pension Protection Act. Part of the challenge is this was signed into law at pretty much the last minute, so it left professionals scrambling to educate our audiences and IRA custodians scrambling to make changes, so the information provided to clients is accurate.

With any big piece of legislation like this, there are going to be gaps and areas of confusion. We expect the IRS to publish corrections, and they have already started.

Stretch IRAs are gone.

The big conversation is that beneficiaries no longer have the option to take distributions over their life expectancy. The reality is that most beneficiaries never took advantage of the stretch anyway. It really won’t affect most of your clients because when they do inherit IRAs, they think, “It’s free money. I didn’t work for it? Why not take that inherited IRA and just spend it?” Because leaving the assets in an IRA allows it to continue to grow on a tax-deferred basis, but that’s really a financial and tax planning issue.

How do you advise the client how to handle their IRAs after the SECURE Act? You’re going to find that when you’re advising clients about most of the changes, you’re going to have to parse your clients into two categories, especially when it comes to beneficiary options. Category A will be IRAs that were inherited before December 31, 2019 and Category B are IRAs that were inherited after because that’s going to affect the distribution options that are available to those beneficiaries.

Elimination of the age restriction for IRA Contributions

The first change Congress made is they eliminated the restriction on making contributions to traditional IRAs for individuals who are at least age 70½ by the end of the year. Life expectancy is getting longer. I see many people who are well past age 70, still working, and they’re young and sprite. Why should these people be prevented from making contributions if they have the funds to do so?

Before the SECURE Act, if someone was at least age 70½ as of the end of the year, that person was not eligible to make a traditional IRA contribution. But they could make a Roth IRA contribution if their modified adjusted gross income (MAGI) was not too high. This change is effective for contributions made for 2020 and after. So now we’re within that period where you can may care about contributions, which is up to April 15 (editor’s note: now delayed until July 15, 2020 for COVID) of this year. We have to be careful because even though those contributions are being made in 2020, they are for 2019 when the age limit still applies. So if your client walks into your office today and says they want to make a contribution for 2019 because they have up until April 15 (July 15) to do so, check to see whether or not they were at least age 70½ by December 31, 2019, because they might not be eligible to make that contribution to a traditional IRA for 2019.

Qualified Charitable Distributions (QCD)

The SECURE Act left the age by which someone becomes eligible to make a qualified charitable distribution (QCD) at age 70½. A qualified charitable distribution allows an individual to make a tax-free distribution of up to $100,000 to an eligible charity. To do that, you must be at least 70½ on the date on which the qualified charitable distribution is made from the IRA. The QCD is non-taxable if it meets a certain requirement. However, many people took advantage of this by making a deductible contribution to a traditional IRA and immediately turning around and making a QCD, in effect double-dipping.

The SECURE Act includes a caveat that if you make a QCD for a year, and you also make a deductible traditional IRA contribution, your QCD will is reduced by the amount of the deductible IRA contribution.

For example, 71-year-old Tom made a deductible traditional IRA contribution for 2020 of $6,000, and he made a QCD of $50,000. Before the SECURE Act, Tom would not have been able to contribute to a traditional IRA because he was at least age 70½ by the end of the year. Now he can, but because Tom is claiming a deduction for that contribution, the new rules say that the $6,000 contribution must be deducted from the qualified charitable distribution. Only $44,000 will be treated as a non-taxable QCD on his tax return. But while the $6,000 difference is included in income, the contribution amount may now be claimed as an itemized deduction on his tax return.

Required Beginning Date

An increase in the Required Beginning Date (RBD) – the age by which someone must begin taking their required minimum distributions (RMDs) – is another positive change.

To determine the rules that apply to an IRA owner, we need to determine whether this person was at least age 70½ on December 31, 2019. If this person was at least age 70½ on December 31, 2019, then the old rules apply, which means that if they reached age 70½ on December 31, 2019, they must take an RMD for 2019 and they have until April 1, 2020 to take that RMD. They then must continue taking RMDs for every year after that.

If this person reached age 70½ on January 1, 2020 or after, they’re under the new rules, and they don’t need to start taking RMDs until the year they reach age 72. There’s a one-day difference that could determine whether someone is subject to this Rule. For instance, if someone reached age 70 on June 30, 2019, they’re under the old rules. But if they reach age 70 on July 1, a one-day difference, then they’re under the new rules. So those who reach age 70½ by December 31, 2019, are subject to the pre-SECURE Act rules and those who reach age 70½ in 2019 have a RBD of April 1, 2020 and must take their 2019 RMD by then. Those who reach age 70½ in 2020 have no RMD in 2020 and their required beginning date is April 1 of the year that follows the year in which they reach age 72.

Some rules haven’t changed. For instance, you still have the option of deferring an RMD for the first year until April 1 of the following year. Whether someone should do that is a conversation that they should have with their tax advisor because the primary reason why we save in tax-deferred retirement accounts is for the tax benefit.

Required Minimum Distribution (RMD) Notifications

The IRS seems to be on top of things, making sure custodians and IRA practitioners are able to handle the administrative functions that they were not able to implement as a result of the SECURE Act having been implemented so late.

IRA custodians are required to send an RMD notification to IRA owners if an RMD is due for the year and if they held that IRA as of December 31 of the preceding year. Usually, IRA custodians have their system set up to send out those RMD notifications. The problem is if someone reaches age 70½ in 2020, some of those individuals are receiving an RMD notification stating they were supposed to take an RMD for 2020. That’s not true after the SECURE Act since they reach age 70½ after 2019, they won’t have an RMD for 2020. The IRS published notice 2020.6 to let IRA custodians know they understand that some of those RMD notifications might have been sent out. What should an IRA custodian do? The IRS said IRA custodians are in compliance as long as they send a corrected notice by April 15. If you find yourself in that position, look at IRS notice 2020.6, and it will provide you with the guidance that you need.

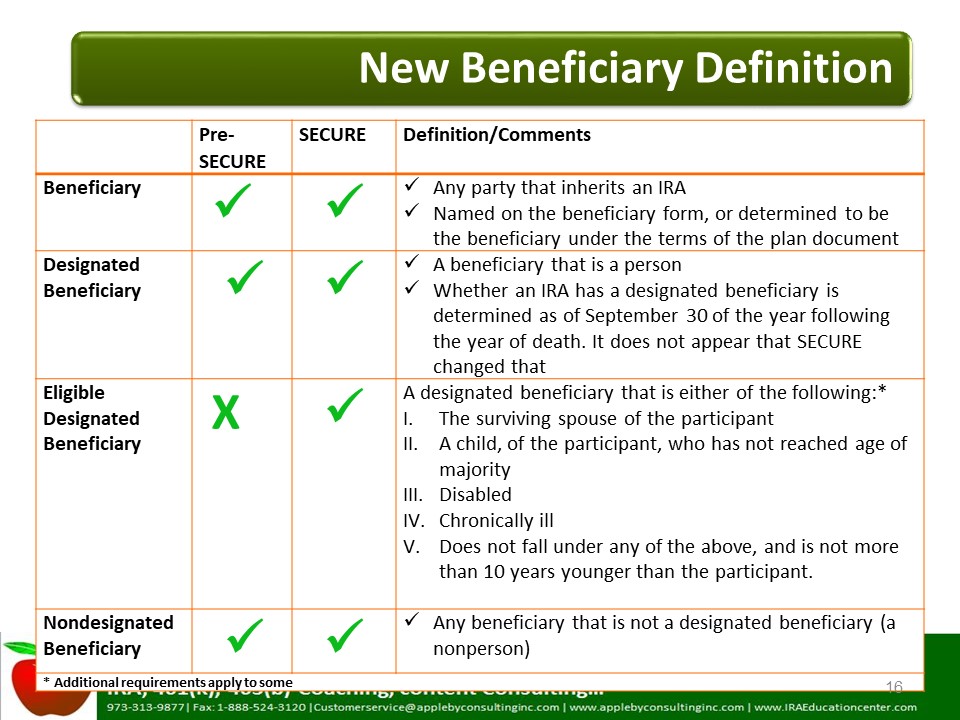

A New Category of Beneficiaries

We’re familiar with who is a beneficiary, which is any party that inherits the IRA. Usually, that person is named on the beneficiary form, or if not, they’re determined under the provisions of the IRA plan agreement. We’re also familiar with the term designated beneficiary, which is usually a person, a spouse or non-spouse. We’re also familiar with non-designated beneficiary, which is a non-person. Usually, the category that you fall into determines your distribution options.

Now a new category of beneficiary has been added. It’s called “eligible designated beneficiaries.” If someone falls under the category of an eligible designated beneficiary, then he or she can take distributions over his or her life expectancy.

Here is a high-level description of who is an eligible designated beneficiary.

A new definition that has been added to our IRA dictionary, so to speak. An eligible designated beneficiary can be the surviving spouse of the IRA owner, a child of the IRA owner who has not reached the age of majority which is usually defined under state law, a beneficiary who is disabled, a beneficiary who is chronically ill, or a beneficiary who does not fall under any of those four but is not more than ten years younger than the IRA owner.

For these individuals, they still have the option of taking distributions over their life expectancy for 2020 and after.

How Does the 10-year Rule Work?

Most of you are familiar with the five-year Rule. Under the Five-year Rule, distributions are optional for years one through four, and the account has to be fully distributed by the end of the fifth year following the year of death. The 10-year Rule is similar, except we’re talking about a 10-year period. For any beneficiary who is subject to the 10-year Rule, distribution is optional in years one through nine, but by the end of the tenth year, the account must be fully distributed.

Let’s look at example. John dies in 2020. His designated beneficiary may take distributions from years 2020 thru 2029, but that’s optional. But by December 21, 2030 the beneficiary must take a full distribution of the IRA balance.

Let’s see how these new rules affect beneficiaries. We’ll do a calculation for 2020 using a balance of $100,000 because studies show that that’s the average IRA balance for Americans and using a reasonable rate of return of 5%. Assume we have a traditional IRA for someone who was born January 1, 1942, which means they have an RMD for 2020, but this person dies in 2020. If an RMD is due for that year, the RMD must be taken by the IRA owner. If it’s not taken by the IRA owner, it must be taken by the beneficiary by the end of the year. For 2020 the RMD for this individual is $4,926, but let’s see how it affects the beneficiary.

Let’s say the beneficiary has chosen not to take distributions for years one through nine and instead waits until the end of year 10 to take a lump-sum distribution, which is $154,000. Now the question becomes whether the beneficiary should choose the lump sum method. Again, this comes down to taxes.

If it’s a traditional IRA where the entire balance is pre-taxed, waiting until the end of the tenth year means they’re going to include that lump sum amount in income, which could put them in a higher tax bracket and require them to pay all the income taxes at once.

A tax advisor might say, “Why not stretch those distributions over the ten-year period so it’s more tax-efficient?” The decision is going to vary from beneficiary to beneficiary and that’s a question that should be posed to the tax advisor. Of course, if we’re talking about a Roth IRA then ideally, they want to leave the amount in the Roth IRA until the end of the 10-year period. Why? Because that means everything is going to be tax-free, penalty-free and it’s not going to affect their income taxes. The answer in many cases is going to lie into what type of account is it. Is it a Roth or is it a traditional?

What if a minor is an eligible designated beneficiary? Who’s a minor? That’s usually defined under state law, right? But here’s something that you must bear in mind. The minute that minor reaches the age of majority then they’re no longer eligible to take distributions over their life expectancy and instead must switch to the ten-year period. You can see how this is getting complicated.

Also, if that minor dies, then the minor’s successor beneficiary now becomes subject to the 10-year Rule.

Disabled individuals are also eligible to take distributions over their life expectancy. The question is then, “Who is eligible to be classified as a disabled individual?” Remember that if someone takes a distribution from an IRA while they’re disabled, they’re exempted from the 10% early distribution penalty.

The definition of disability for this purpose is the same definition of disability that applies for the exemption to the 10% early distribution penalty; at least we have that to rely on when you’re trying to define who is a disabled individual. For someone who’s chronically ill, usually that is a person who can’t help themselves with daily activities. They must rely on someone else to do that. You’ll see the trend here is that Congress doesn’t want to allow beneficiaries, in general, to take distributions over their life expectancy except for spouse beneficiaries.

An Exception to the 10-Year Rule

Here’s an exception to the 10-year Rule that I find many people overlook. The 10-year Rule applies to a designated beneficiary. A non-spouse beneficiary doesn’t fall under the exception to be an eligible designated beneficiary. I don’t know if this was an oversight by Congress. The rules were not changed for a non-designated beneficiary. So if you have an instance where a charity is the beneficiary now, in order to determine the options that are available to the charity, we have to look at whether or not the IRA owner died on or after the required beginning date and you’ll notice I didn’t mention that for the other beneficiaries. Under the old rules we would have to. When we’re trying to determine what the beneficiary options are, one of the questions used to be at what age did the IRA owner die? We no longer ask that question unless we’re talking about a non-designated beneficiary.

Now a non-designated beneficiary death occurs before the required beginning date then the five-year Rule applies where distributions are optional until December 31 of the 5th year following the year of death. But if the IRA owner dies on or after the required beginning date then the non-designated beneficiary is permitted to take distributions over the remaining life expectancy of the decedent. In some cases that might be beneficial to the non-designated beneficiary because if death occurs on or after the required beginning date and the IRA owner dies at age 72, then life expectancy could be over 14 years – a longer period than the 10-year period allowing the non-designated beneficiary to stretch distribution. Why is this important?

Because in some cases, non-designated beneficiaries are going to take a full distribution of the assets, especially if that non-designated beneficiary is a charity. But if you remember under the old rules if you have multiple beneficiaries on an IRA, and one of those beneficiaries is a person, and the other is a non-designated beneficiary such as a charity, the general advice was to have the charity take a full distribution of its share by September 30 of the year following the year of death. Why? So that the remaining beneficiary was a person would be able to take distributions over their life expectancy.

Now the rules of the game have changed because if the non-designated beneficiary remains on the account, then both the non-designated beneficiary and the designated beneficiary are eligible to take distributions over the remaining life expectancy of the decedent. This is one of those cases where the tax advisor would say, let’s talk about what the distribution options are depending on whether or not the non-designated beneficiary takes the full distribution of its share. There might be some planning opportunities, for instance, for a church to just take 99 percent of the assets and leave one percent as a non-designated beneficiary, allowing the other beneficiary who’s a person to take distributions over the remaining life expectancy of the decedent.

There are also new rules for successor beneficiaries. This is a big part of what they were talking about this elimination of the stretch distribution. The whole idea of the stretch distribution was to allow success beneficiaries to take distributions over the original beneficiaries’ lifetime. Let’s say Tom inherited an IRA, and Tom had a life expectancy of 50 years, but Tom dies five years later. Whoever Tom named as his successor beneficiary would have been able to take distributions over the remaining 45 year period. In other words, that successor beneficiary who’s the beneficiary of the original beneficiary would be able to continue taking distributions over Tom’s remaining life expectancy.

The SECURE Act took away that provision, and now the rules say when the original beneficiary dies, even if that original beneficiary was taking distributions over that beneficiary’s life expectancy, then the successor beneficiary gets switched to the ten-year period. When you have a conversation with a beneficiary about their beneficiary options, you’re going to have to ask the question at with age did the IRA owner die and on what date, because now we have to break it down into two categories. Because if the IRA owner died on December 31, 2019, or before then, the old rules, the more favorable rules, apply. But if the IRA owner died after December 31, 2019, the new rules apply. Most people are aware of that. But what I find that most people are missing is that the cutoff date also applies to a successor beneficiary.

If the designated beneficiary dies in 2020 or after, the successor beneficiary must switch to the 10-year period. So no longer is the successor beneficiary allowed to take distributions over the original beneficiary’s remaining life expectancy.

The same thing applies though to an eligible designated beneficiary. If we’re looking at an eligible designated beneficiary who is disabled, chronically ill, or not more than ten years younger than the IRA owner, we understand now that those beneficiaries are classified as eligible designated beneficiaries and therefore eligible to take distributions over their single life expectancies. But what happens when they die? Their successor beneficiaries get switched to the 10-year period.

The Old Rules Haven’t Been Completely Tossed Out

Some of the rules have not changed. How does this affect your clients with inherited accounts?

I thought it would be interesting to include a comparison of someone who died in 2019 versus 2020. You see the significant impact that this has on the amount of assets a beneficiary receives assuming that the beneficiary uses the stretch IRA strategy and takes no more than the beneficiary’s required minimum distribution amount each year. We start by calculating RMDs for 2015. Let’s use an average year balance of $100,000 and a reasonable return of 5%. It’s a traditional IRA. The owner’s date of birth is January 1, 1940. The year of death is 2005. There is a designated beneficiary. The beneficiary is not the spouse and the required beginning date is April 1, 2011. Everything is the same up until that time. Now during the non-spouse beneficiary’s lifetime, the balance will increase to $105,000 (we’re using the same rate of return and the inherited IRA owner’s year of birth is 1980).

We are going to assume that in one case the beneficiary dies in 2019 and we’re going to assume in another that the beneficiary dies in 2020. Assume that the successor beneficiary is taking a lump sum at the end of the ten-year period. There is a significant difference in the amount that the beneficiary would eventually receive. If the beneficiary died in 2019, the last year of distribution under the life expectancy method is 2063. Whereas if they died in 2020, the last year of distribution is 2030. And if they died in 2019 the total distribution would be $535,000. Whereas under the new Rule, it’s only $254,000.

Many beneficiaries do take distributions of those amounts usually within a two-year period but there are those beneficiaries who really plan on having these assets serve them for over their life expectancy to help cover expenses. You can see how this affects beneficiary and what the big hue and cry is about the elimination of the stretch because this is how it affects beneficiaries and successor beneficiaries.

There are some things to bear in mind. Some rules have not changed. As I read the SECURE Act I wondered if they forgot to address these rules. Because if that’s not the case then leaving these rules as they are could disqualify the category of beneficiaries that they’re trying to protect if any one of those beneficiaries is one of multiple beneficiaries.

September 30 is the determination date, the date that is used to determine whether or not an IRA has a designated beneficiary. Let’s say someone died in 2020. Does the IRA have a designated beneficiary? We make that determination on September 30, 2021. How does that affect beneficiaries if there are multiple beneficiaries of the account?

Spousal Beneficiary Options

The spousal beneficiary options have not changed. What does this mean? It means that if you’re a spouse beneficiary, you can still take distributions over your life expectancy. You can still move the inherited IRA to your own IRA instead of keeping it in a beneficiary IRA.

One of the factors that must be taken into consideration when making that decision is the age of the spouse beneficiary. Is that spouse beneficiary under age 59½, and if yes, does that spouse beneficiary plan to take distributions from the inherited IRA before reaching age 59½? If the answer is yes to those two questions, then it makes sense for that spouse beneficiary to keep those assets in the beneficiary IRA. Why? Because distributions taken before age 59½ are subject to a 10% additional tax or 10% early distribution penalty unless an exception applies. Well, guess what? One of those exceptions is distributions due to death, and a distribution is qualified as a distribution due to death only if it is made from a beneficiary account or inherited account.

There are benefits to moving it to the spouse’s own IRA, including there are no RMDs until the spouse reaches RMD age and even if there are RMDs, they aren’t calculated using the uniform lifetime table which produces a lower RMD amount than the single life beneficiary table.

The good news is that a beneficiary can change his or her mind at any time and move the inherited IRA to the spouse’s own IRA. A good strategy would be for when that spouse beneficiary reaches age 59½ to transfer those assets to the spouse’s own IRA.

Key Takeaways

Here it’s all about education. Your legal department is likely working on your IRA agreements now, but clients are coming in to see you. What do you tell them? Beneficiary options are a very important part. We don’t want individuals to take less than the amount they’re required to because if they do, they’re going to be subject to the 50% excess accumulation penalty.

What about making IRA contributions? Is the person who is bringing a check to your office really eligible to make a traditional IRA contribution? Confirm when this person reaches age 70½.

The best estate planning attorneys are right now still involved in discussions trying to determine how do the new changes affect the beneficiary options that are available when a trust is the beneficiary. What should you do? Direct the client to seek legal advice with an estate planning attorney.

Remember that some IRA custodians, unfortunately, couldn’t stop the RMD notice from going out for people who are not subject to our RMDs for this year, but they’re still getting an RMD notice that they need to take an RMD. What do you do in that case? Tip: Because it’s not an RMD, it can be rolled over if the rollover is done within 60 days and if that person has not done an IRA to IRA rollover during the past 12 months.

Bear in mind, though, that I didn’t cover everything. I covered the most common areas. Be on the lookout for opportunities and traps so that you can help your clients take advantage of opportunities and avoid traps that could rob them of opportunities and cause them to owe taxes and penalties that they could otherwise have avoided.