I am concerned that many of the assumptions we use today in financial planning tools do not effectively demonstrate the value of lifetime income. If you want to learn more, I wrote a piece a little over 10 years ago titled “Exploring the Retirement Consumption Puzzle,” published in The Journal of Financial Planning in May 2020. In this article, I came up with this effect called “The Retirement Spending Smile,” where I noted that individuals do not tend to increase their consumption yearly by the inflation rate. It tends to fall one or two percent versus inflation as you move through retirement, but it could increase for those still alive in late retirement.

Some newer research that effectively uses the same data set (the University of Michigan’s Health and Retirement Study (HRS), which is a longitudinal panel study that surveys a representative sample of approximately 20,000 people in America supported by the National Institute on Aging and the Social Security Administration), evaluates how do retirees utilize their resources in retirement to fund spending. Another article I published with Michael Finke on “Guaranteed Income: A License to Spend” focuses on better understanding how retirees utilize their savings.

The role of protection for lifetime income is based on your client’s personalized situation:

- How much do they value the certainty versus the uncertainty, but then,

- If something happens, if they run out of money, what does that mean for their lifestyle?

I will address some of these issues more later on, but I want this to be a framework of why and how people might be willing to buy insurance and lifetime income – because of the protection.

Spending in Retirement

I am sure that almost everyone is aware that how people prepare for retirement has structurally changed. Defined benefit plans are an incredibly effective way to create income in retirement. There is this pool of people and individual longevity risk. That individual longevity risk is pooled in a defined benefit plan, making retirement planning easy. You do not have to worry about living to age 100 because the law of large numbers allows a defined benefit plan to pool that risk together.

That is not what happens with defined contribution plans such as 401(k)’s and 403(b)’s. We all have to plan individually to live to an advanced age, making them structurally inefficient for retirement. If everyone has to plan to live to age 95, age 100, and age 105, we will spend less than we could if we were in a defined benefit plan because we have to manage this idiosyncratic longevity risk ourselves.

Combine this with the unknowns in retirement. There are two critical structural things that we do not know that radically complicate figuring out how much you can spend in retirement. The first is what the market is going to do. Historically, specific markets like the U.S. have done awesomely well over the last 150 years. Other markets, such as Germany, Japan, etc., have had bouts of incredibly low returns. We also do not know how long retirement will last; for some, it may last 10 or 15 years; for others, it could last 30 or 40 years. These two uncertainties create much anxiety among retirees.

We have all heard of the four percent rule. It uses certain assumptions to help someone figure out, for example, how much they should spend in retirement. It assumes that when you retire, you withdraw four percent the first year and increase that amount yearly by inflation for 30 years. Your portfolio balance will be zero at the end of that 30-year period. It assumes that if you are incredibly healthy and have been alive for 29 years, you will spend the entire portfolio effectively no matter where things are.

This is not the most realistic model for spending, but it is not a terrible starting place. Again, the problem with these rules is just all of the uncertainty.

How do people deal with uncertainty? Fundamentally, if you do not know what the markets will do or how long retirement will last, you will not be as comfortable spending money. However, we have found that retirees do not tend to respond the same when they have their wealth in a portfolio versus the wealth of some kind of income protected for life.

How Do Academics Feel About Lifetime Income Annuities?

Academics love annuities for the most part. Particularly, research focuses more generally on why it makes sense for retirees to pool longevity risk. Pooling longevity risk is incredibly smart because there are two key pieces when considering the drivers of an annuity or lifetime income. One is investment returns. The other part of an annuity payout is longevity and mortality credits.

We can all go out and invest in a portfolio. That is not unique to insurance companies, for example. Still, the key is that only pooled vehicles, such as annuities (there are tontines in other countries now), benefit from longevity or mortality credits or pooling. This is really, really important. Transferring this risk to a third party makes much sense when you understand how risks work.

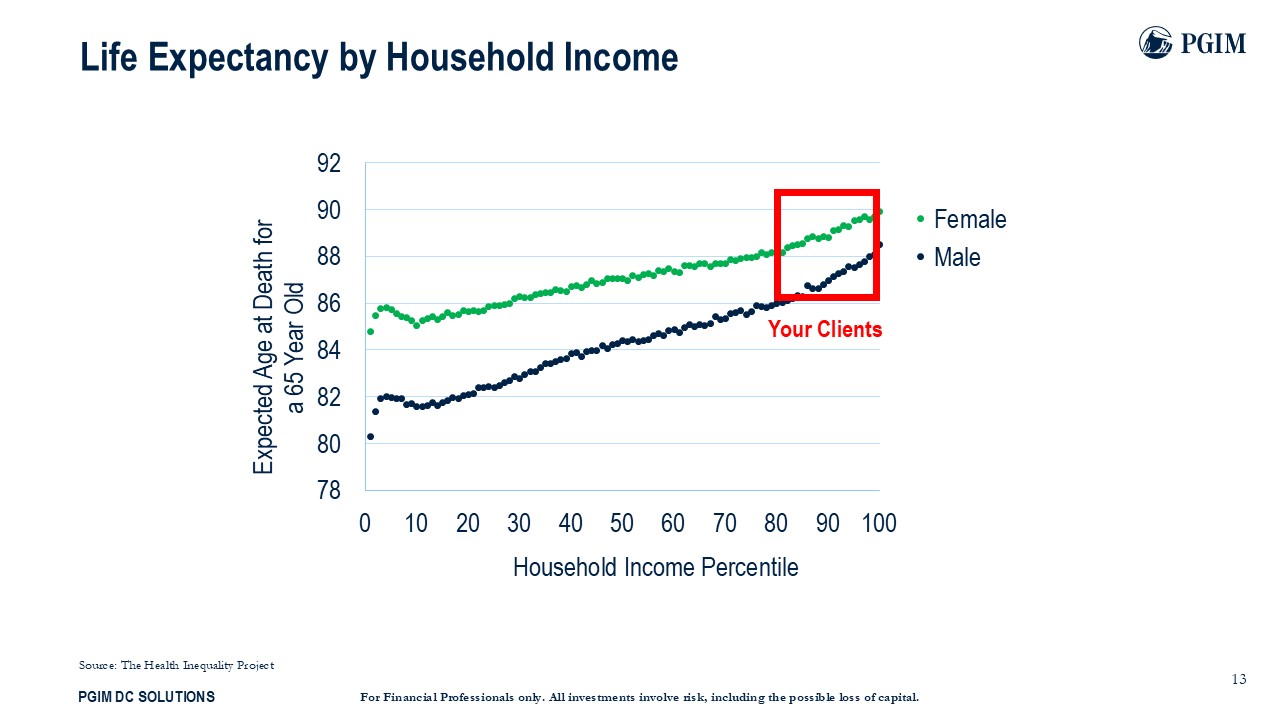

Regarding longevity and life expectancy, your clients are not average.

On this slide is the life expectancy for a 65-year-old based on the household income percentile. Individuals who utilize financial advisors tend to be in America’s highest two income deciles. These Americans will live three to five years longer than the average American, so when your client hears statistics about life expectancy at birth, that is irrelevant to your clients. When your client hears life expectancy statistics at age 65, that is also irrelevant. You need to understand that your clients will live much longer than the average American, which changes the benefits and the need for lifetime income products.

The probability of either member of a joint couple, male-female, living to age 95 or 30 years in retirement, is 51 percent or a coin flip. That is worth repeating. The odds of at least one member of a married couple retiring today, who is healthier and wealthier on average, is about 50 percent. For the average American, it is only about 20 percent. Remember, your clients are not average. Think about that. What do you do if you have to plan for a retirement period that could last 30 or 35 years? How do you handle it?

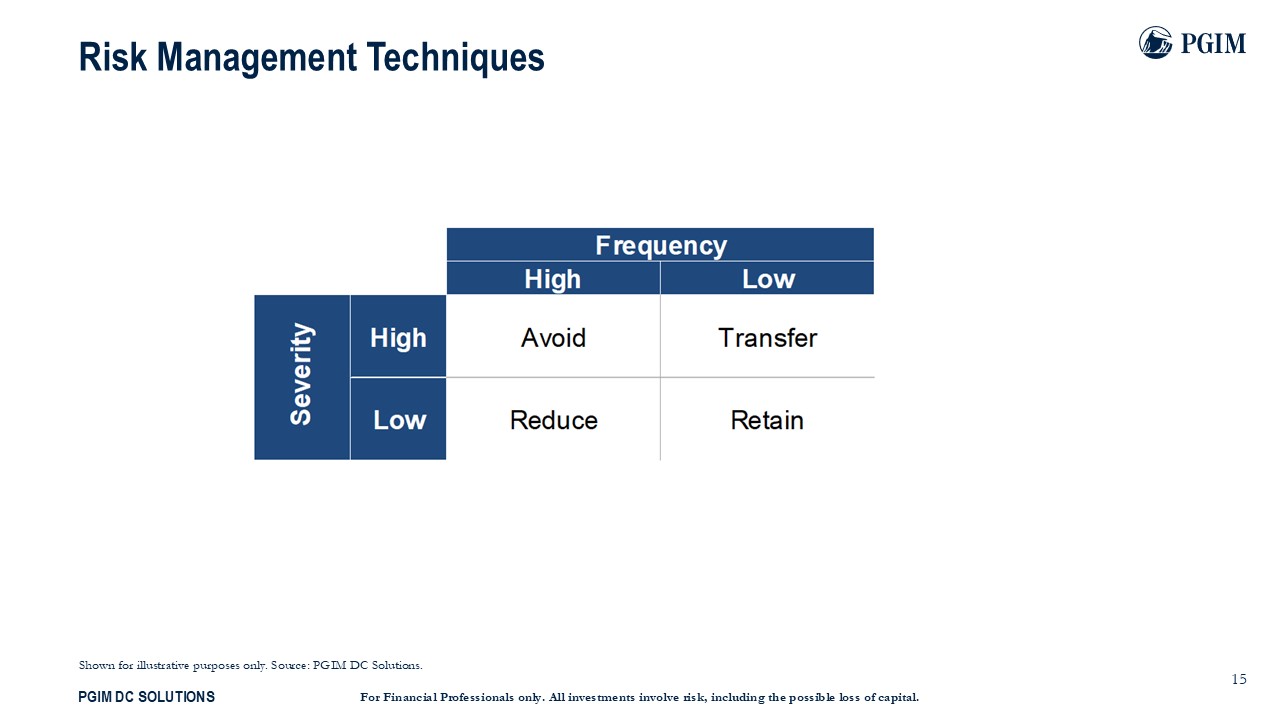

Well, that is a significant risk. There is a framework that exists for how we think about managing risks. We can think about risks in terms of their severity. Is the severity high or low, and the frequency; how often do these risks happen?

The risks you should always seek to transfer or buy insurance, such as a lifetime income annuity, are high severity and low frequency. That is the definition of longevity risk. Tail risks that are somewhat cataclysmic, which is a definition of longevity risk, are the risks that we need to be more proactively considering in terms of utilizing some kind of lifetime insurance. The place that you should start when looking for inflation-protected lifetime income is delayed Social Security claiming. Other things can work as well.

How do we think about risk? Too often, we define risk as asset volatility or standard deviation, but that is not a holistic definition of risk, right? Risk also accomplishes a retirement outcome, and there are very few investments that are low-risk when thinking about asset volatility and retirement outcomes. That would be guaranteed lifetime income or income protected for life – a strategy that checks multiple boxes. What is important, though, is to understand where and why individuals tend to benefit from buying insurance.

I will discuss this more later, but I do not know that we are doing a great job quantifying outcomes in our financial plans. For example, those who make retirement income projections probably use success rates, just ones and zeroes, as their outcome metrics. That is not a very good way to think about how individuals experience outcomes or loss. In reality, what people mostly care about is wealth or income. While we are happier when we have more wealth or income, the dissatisfaction or the dis-utility of a shortfall upsets us. Life insurance, disability insurance, etc., are forms of insurance; they are not wealth maximizing. What they do is they ensure that we minimize when a bad thing happens, we do not have to worry about the negative consequences nearly as much.

You can add value by using an insurance framework for retirement income planning versus just an investment framework. Too often, advisors are prone to think about the role of annuities as an investment. There are annuities that are investments, but for discussion, I am using the annuity term more historically, focused on its role as providing income protected for life.

Despite all of my arguments herein and the arguments of others, there is this idea of the annuity puzzle. This notion has been around for over 30 years, which is simply that households should have more of their wealth in lifetime income. However, households are not doing that; there is a big gap between what most of us would think would be the optimal level of lifetime income and how much households are utilizing to fund retirement spending.

How Do Retirees Leverage Walth to Fund Consumption?

For this study, I essentially used the entire HRS data set. I looked up households with available spending data, applied some filters, and ended up with a total of 5,000 households and 17,000 observations over a two-decade period that showed how retirees utilized their money over time/how they utilized their holistic wealth.

For the analysis, I broke out their resources into five different types. There are their savings (qualified and non-qualified accounts), primarily because of things such as RMDs, and there is also income. There is lifetime income, wage income, and capital income. Collectively, I wanted to know how the household utilizes these five possible resources to fund consumption or spending.

Part of the analysis is this idea of an assumed spending rate. To make things easier to understand, I will often convert a balance, for example, in an IRA or a 401k, into what I would call spendable income. I do this using a very basic rule of thumb essentially based on the RMD-type table logic, but I tweak the factors so that the assumed spending rate from assets is four percent for a married couple, or the four percent rule, and five percent for a single individual. If they have a balance of $1,000,000 and it is a married couple, they could spend $40,000 from that this year. This can be put on par with what the household is spending or currently receives in terms of lifetime income.

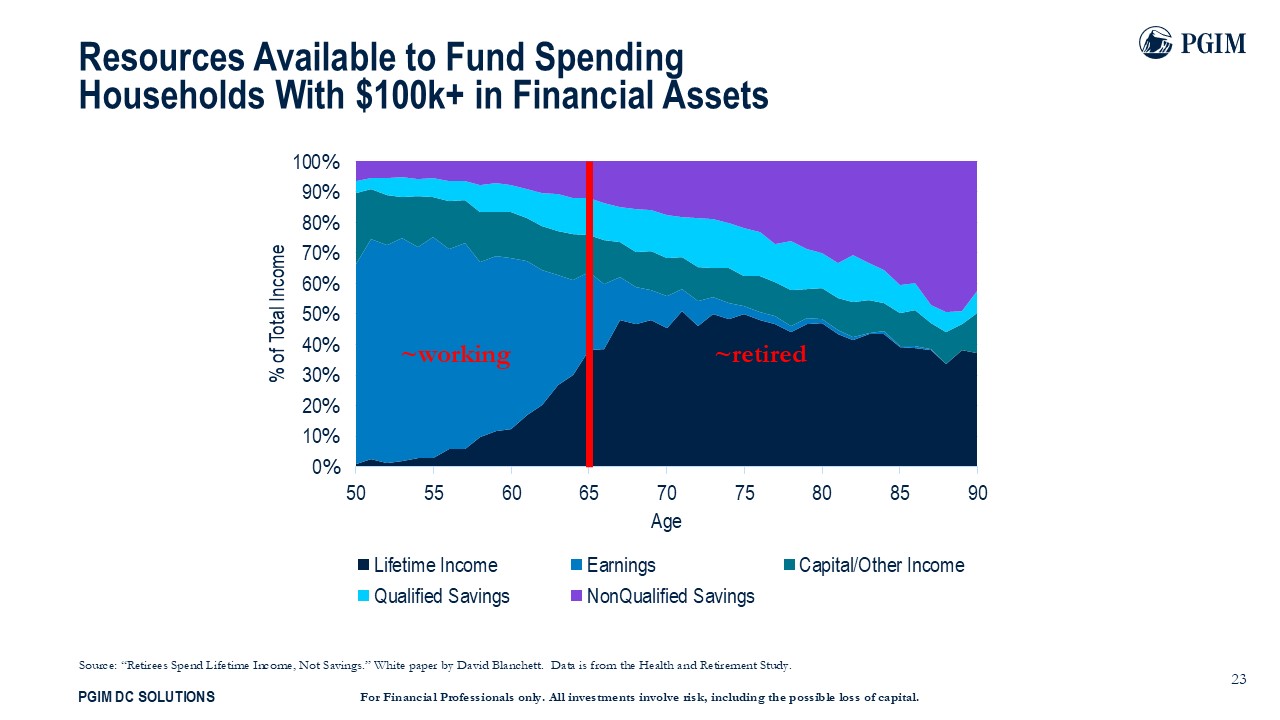

This slide demonstrates how the total resources available to fund spending evolve over time for households with average assets to fund spending over $100,000.

This is really interesting. If you look at younger individuals under the age of 60, all of the resources they use to fund spending are just based on wages, right? Sure, they could spend down their non-qualified savings or other things, but they are saving that for retirement.

But look at how complicated things get when people do eventually retire. You have non-qualified savings and qualified savings. You might have some lifetime earnings and capital income. Wow.

How do you figure it out? Think about just the mental transition there, going from, “I know how much I can spend because I make $100,000 a year,” to “Oh my goodness, I am going to get $20,000 a year from Social Security. I am going to have some income. I am working a little, and I have all of these balances and assets.” From my perspective, it is not nearly as clear how a retiree would leverage their assets in retirement versus when working.

There is evidence that, on average, households under-consume. On this slide is the distribution of how much the household is spending, all of the households, at a given age versus what their spendable income amount is. Remember, spendable is their lifetime income, wage income, capital income, and what I estimated they could pull from their savings.

Even as they move through retirement, on average, households are not spending as much as they could. Some are spending too much. Some spend too little. This begs the question: are there differences in how households utilize their savings based on the composition of their wealth? That is the key analysis in this research, and the answer is yes.

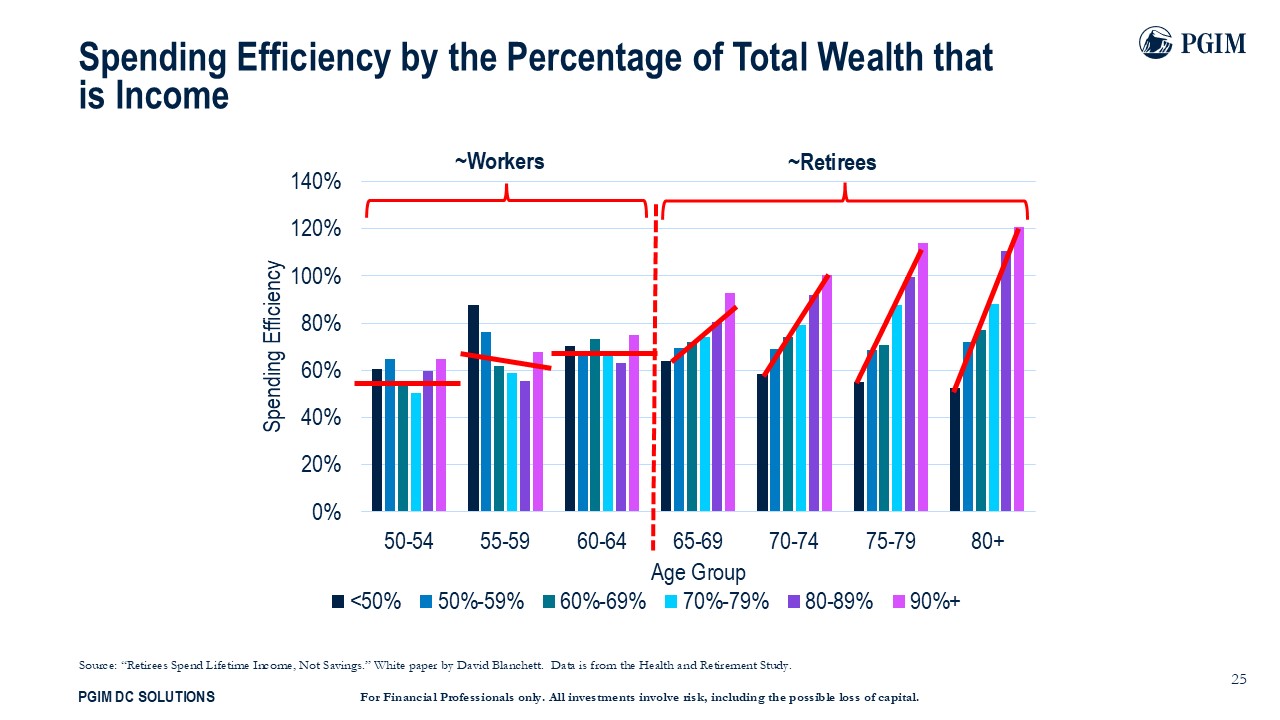

How does spending efficiency vary based on the percentage of total wealth in a particular income source? Think about all of the resources that exist. What percentage of those resources are in some kind of income vehicle? What we see here is that among those who are working, there is no clear effect.

This is not surprising because when you are working, you should not spend your savings. However, there is an incredibly clear effect here. It is almost astonishing that households with more of their wealth in income sources spend a lot more as they retire. This applies up to the 80-plus group. Households with less than half of their wealth in income sources spend only about half of what they can, and households with almost all of their wealth in income sources spend a little bit more than they should. If it were flat lines throughout, that would suggest it does not matter whether or not a household has money in a portfolio or lifetime income. This suggests it does matter.

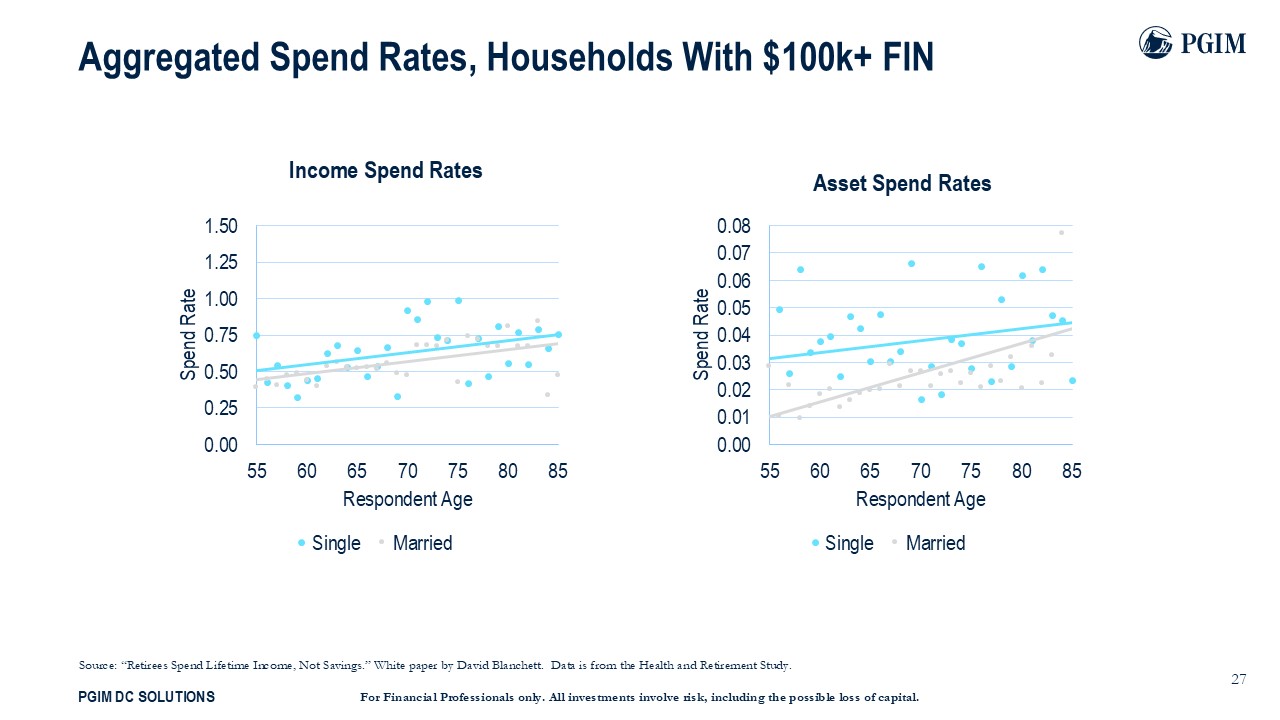

Next, I conducted a robust analysis of every household and pooled them together using an ordinary least squares regression. The goal here was to understand how each potential asset, such as qualified accounts, non-qualified accounts, lifetime income, wage income, and capital income, is related to the spending decisions of the household.

The regressions are done separately for every single age group and whether the household is married or single. What are the spend rates for single versus married household spend rates?

Evidence is out of the gate that neither income nor assets are fully utilized. In theory, I would want to see a spend rate from income close to one. We do not see that if we look at things collectively. We also see some very low withdrawal rates.

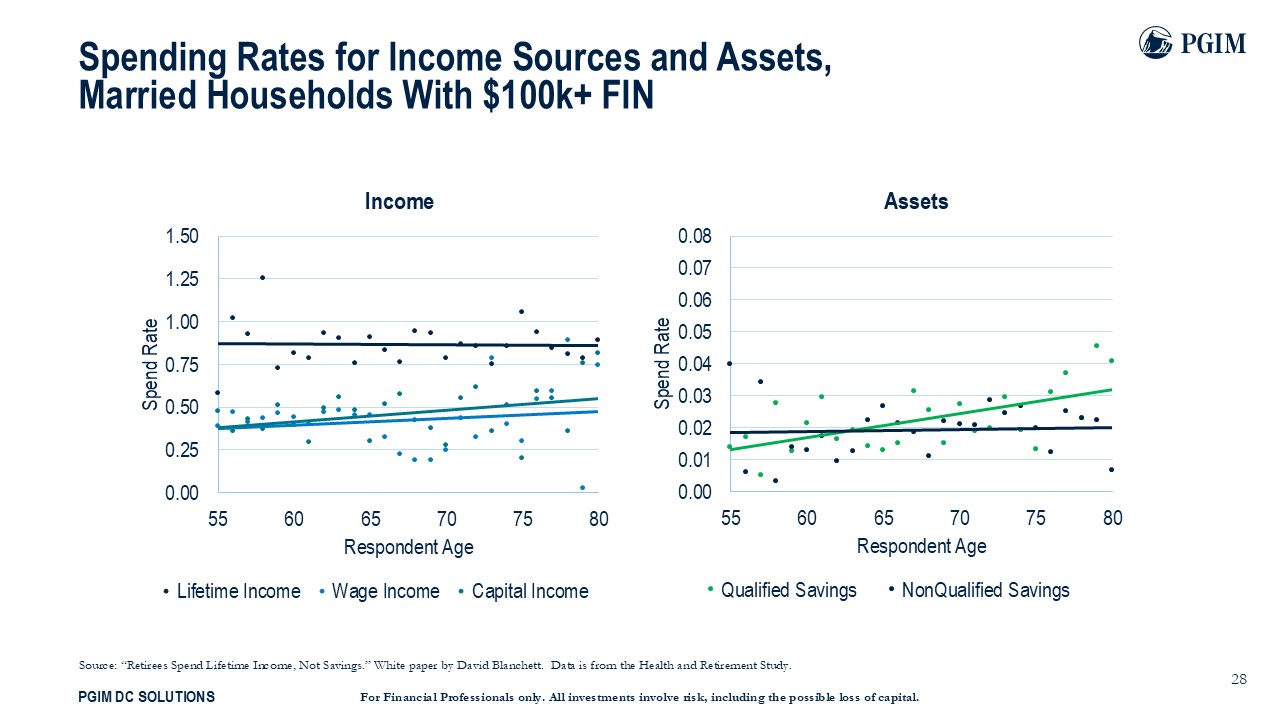

Now, this is what it looks like if I break out the income sources into three types: lifetime, wage, and capital income. I also break out assets into qualified and non-qualified assets. This is probably the most powerful result of the entire analysis.

Focusing on lifetime income (the dark navy dots and lines) suggests that households spend about 90 to 95 percent of every dollar they receive in lifetime income. Wage income and capital income are closer to 50 percent. It does not matter what age they are receiving it. Lifetime income is the only income asset that is effectively used in terms of spending and consumption. If you look at the assets, there is just dramatic underspending.

For example, for qualified savings (which is the green line and green dots), at age 65 the average married household is only withdrawing about two percent of their qualified savings to fund consumption. That is way too low. If you think about the four percent rule, which suggests it should be higher. What we do see, though, is evidence that households spend more from qualified assets as they age. Why is that? I think that is because of RMDs. In my mind, this collectively demonstrates that households do not like to draw down assets to fund consumption but are willing to utilize lifetime income to fund consumption. This very real behavioral effect exists that households with more money protected or guaranteed for life are more willing to consume those monies in retirement than they are a portfolio.

Interestingly, there appears to be a dual benefit where households with more lifetime income have higher withdrawal rates from their portfolios. So, not only are they spending more money when they have more lifetime income, but they are also taking higher withdrawals from their portfolios. I think this is because they feel more comfortable spending down savings when they have a lifetime income base.

So far, I have talked about the evidence that demonstrates why households may consider allocating more to lifetime income beyond the more economic rationale. A lot of the research on lifetime income is really focused on the economic benefits. My research suggests that what retirees need when it comes to spending is an easy button. They want something where they do not have to worry as much about market uncertainties, market realities, and things like that.

What is the Optimal Lifetime Income Strategy?

Too often individuals (such as myself) who research annuities focus entirely on things such as economic efficiency. They ignore behavioral considerations, such as how people feel about products. They ignore the actual product landscape, such as how insurers might respond to insuring separate risks. In reality, there really is no one solution for everyone, but it is important to be aware of these perceived threats.

Take inflation, for example. We conducted at Prudential about a year ago, and inflation was noted as the number one threat to retirement security, which is new. This might change as inflation concerns go down or rates go down. However, inflation is not something that most lifetime income products can address actively, right? I am unaware of any products today that explicitly provide income for life linked to inflation other than Social Security.

I believe Social Security is the best place to look for lifetime income. I know there are some current uncertainties around the trust fund’s future. It is highly unlikely that anything will happen there, but Social Security is the only product available, solution, or effective strategy based on the average American demographic. Annuities, such as lifetime income products, are subject to adverse selection whereby the average person that buys a lifetime income annuity has a life expectancy at retirement about five years longer than the average American, so the payouts are not as good.

There are no providers today offering products linked to inflation, so I believe that every single American, every single person, should be thinking actively about the best time to claim Social Security to create that kind of base of lifetime income. If that is not enough, maybe it is time to think about annuities or creating a personal pension. People respond better to the term personal pension than annuity; annuity is actually a very ambiguous term.

Annuities do lots of different things for different people. The key, however, is to think of an annuity as a form of insurance. I go to Las Vegas once or twice a year for conferences. I am very good at losing money in Las Vegas, as the house has the edge in Las Vegas. I know that when I play blackjack or whatever game I want to play, the house is going to win on average, right? I would never equate annuities to gambling, but what I would want to make you think about is that the insurance company knows the odds. An annuity is fundamentally insurance. It is not an investment.

And so, when we think about the role of these products in a portfolio as part of a retirement income strategy, they need to be viewed as such. We need to remove our portfolio optimization hat and think about how to structure a plan that best helps someone accomplish their retirement income goal.

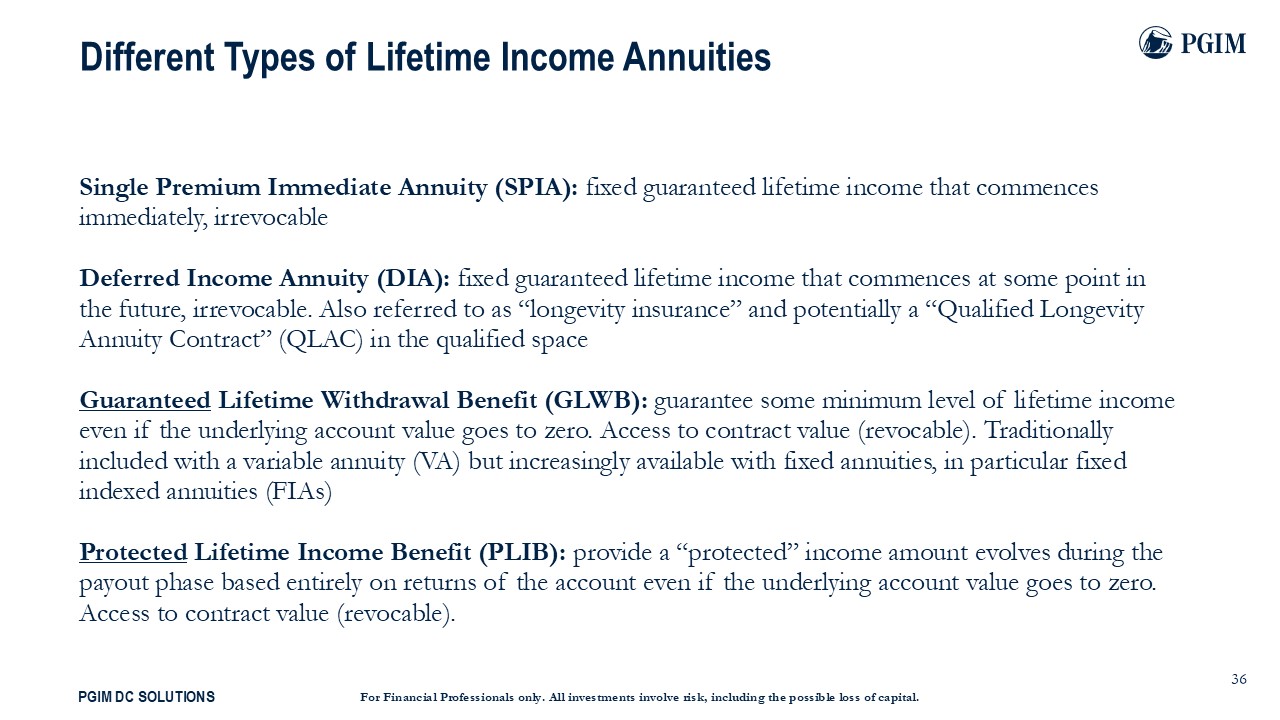

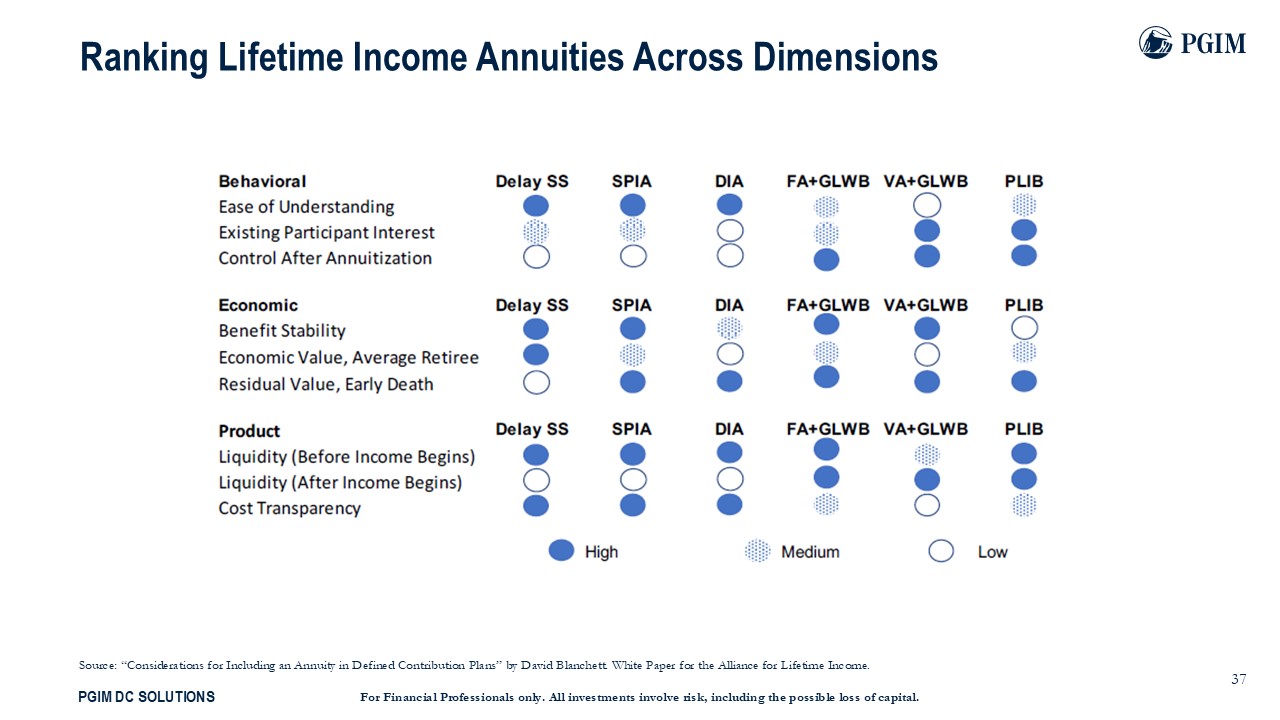

Four main products or strategies exist in terms of lifetime income annuities.

The first three listed are pretty common. Single Premium Immediate Annuities (SPIAs) or immediate annuities have been around for about 2,000 years. Deferred Income Annuities (DIAs) are somewhat new. They have different names, such as longevity insurance. There are Qualified Longevity Annuity Contracts (QLACs) as well. Academics tend to really like DIAs, but the problem in reality with products like DIAs is that only really healthy people buy them, which hurts the payouts. A lot of insurers do not love to write them because of the mismatch in assets and liabilities, and that hurts payouts, too.

DIAs are a really good example of a product that sounds really good from an economic efficiency perspective, but it really does not do as well when you think about the behavioral considerations and the product landscape. Guaranteed Lifetime Withdrawal Benefits (GLWBs) have been around for two decades. Historically, they were offered on variable annuities. That has been going away a lot, given some of the capital costs insurers incur to write them. They are becoming very common in fixed annuities, even fixed index annuities.

There is an emerging category that I think is a perfect way to get lifetime income, and I call it PLIB or protected lifetime income benefit. The key here is that you are buying something for the income benefit that evolves over time. It can go up, and it can go down, but it allows a level of risk sharing that is significantly more efficient for both insurers and retirees when we acknowledge that virtually every American already receives some type of fixed guaranteed lifetime income benefit.

Almost every American either gets Social Security or a public pension, however, we all need more lifetime income. I am not convinced, though, that the income needs to be totally fixed and guaranteed for life because we have that.

Here is how I rate these different products across all of these dimensions. There is a ton to unpack here, but again, it is based upon these different strategies’ behavioral, economic, and product considerations.

The key takeaway here is that there will not be one product that works great for everyone. There is no single solution regarding the optimal lifetime income annuity for a participant, a retiree, a plan sponsor, an investor, or whomever. Everyone is a little bit different. We all have different preferences. Our goals are different.

Certain products will work better on average than others. For example, delayed claiming of Social Security is usually very attractive, but there are issues. There is no cash refund benefit to the product. There is no liquidity, but I think that understanding, as an advisor, how all of these products work and where they fit is really important to help ensure that your clients get the best possible outcome. I would expect innovations in this space.

Advisors and Their Relationship with Annuities

It is worth taking a minute or two to address why all advisors should more proactively consider annuities.

Having a financial advisor who considers annuities as part of a holistic retirement income plan is still relatively rare. This means that for virtually every client, there should be an attempt to understand their retirement income goals and objectives and design a strategy that explicitly considers allocating some of their wealth to lifetime income.

For many folks, that is just delayed claiming Social Security, but it could mean buying an immediate annuity. It could mean buying a QLAC, but it takes that explicit, active decision and focus for the advisor.

Time and time again, I have heard advisors say, “I do not like annuities; I do not think they are very good.” etc. I did a research study with DPL Partners last year that reviewed how advisor attitudes and perceived client attitudes vary based on how familiar the advisor is with annuities.

The evidence is pretty overwhelming where the more an advisor understands how annuities work, the more attractive they perceive them to be, and then the more attractive they think their clients perceive them as well. I get it. There are bad annuities out there. There are bad mutual funds. There are all of these things, but your job as an advisor, is to have human capital specifically targeted towards helping your clients accomplish their financial goals. Understanding where and how annuities work is vital, especially for retirees.

In this same survey, we found that among advisors who start using annuities, there is this recognition of stronger relationships, more assets, more referrals, and more AUM. A more holistic financial plan results in happier clients. It also results in better behaviors. Client reactions among those advisors who start using annuities are satisfied, they spend more. they take more risks, etc.

Again, I understand that not every retiree needs more lifetime income or an annuity. Still, when I talk to advisors, and they say they have 100 or 200 clients, and they have not found a single client that could benefit from using more income, that is when I say, “Wait a minute.” I would suggest you are not actively aware of the potential benefits, how the products work, and how they can benefit your client regarding retirement.

How to Improve Financial Projections

Now, one issue I am concerned about is that we are not doing a very good job demonstrating the value of some of these products in financial plans today. I see three key weaknesses in how we do income projections.

First, most financial planning tools treat retirement as a single liability. It is all needs – no needs and wants. No adjustments are assumed to occur as we move through retirement, and finally, and probably most importantly, we assume retirement is pass or fail. It is a binary outcome. That is just not reality at all. This can result in some pretty bad guidance around everything we must do at retirement: optimal portfolios, optimal saving rates, annuity rates, et cetera.

First, understanding the retiree balance sheet is critical. Virtually all Americans should have their essential spending covered with income they cannot outlive, right? Again, based upon the research earlier findings, doing this one thing will make people more comfortable in retirement and make them more willing to utilize their retirement savings to enjoy other things. Ensuring you understand that retirement is not just a single goal but a series of goals and then mapping out effective assets to fund those is absolutely critical.

We have to acknowledge that retirement spending will change over time. When you think about how we define outcomes, this is perhaps one of the biggest shortfalls in many tools advisors use today. Say you have a client who aims to have $100,000 a year in income for ten years.” And in that tenth year, they fall $1,000 short. An important question is, did this client really fail?

I use the word fail because if we think about success rates, there are only one of two possible outcomes in a traditional Monte Carlo success rate projection. It is zeroes and ones. You get a zero if you do not complete the goal, or you get a one. So, in Monte Carlo terms, this $1,000 shortfall in year ten would be deemed a failure, but if we stretch this out to look at income for 20 years, 30 years, or 35 years, I do not think of this as a failure. Way too often, when clients experience “failure in retirement,” it is not that big of a deal.

Why this matter is I cannot tell you how often I have heard, “David, I want to allocate to an annuity in my projections, but I cannot because the success rate goes down.” For example, I have an 80 percent success rate projection when there is no annuity, but I only have a 75 percent success rate when I allocate to the annuity. The problem, if that is what you are experiencing, is that your outcomes metric does not reflect what it means when someone fails.

I think a much more realistic way to convey outcomes to clients is to talk about when the bad thing happens is what their income might be. For example, do not tell clients they have an 80 percent success rate. I would recommend that you never tell a client a success rate. I think you just tell them if they are in fantastic shape, good or bad shape. Telling clients success rates does not mean the same thing to different clients. It does not give them effective information. They need to know if they are doing great, okay, or poorly. If you want to quantify outcomes, the best way to do that is to tell them what it means for their lifestyle

if things go poorly.

If you do not buy the lifetime income annuity for 30 years through age 95, in the worst one in 10 scenarios or runs, they will have $50,000 a year. However, if you buy the lifetime income annuity, delay claiming Social Security, or do whatever you want to do, you will have $75,000 a year income in that same worst one in ten. For a retiree, this is much more valuable.

At a high level, it is really important for us as an industry to understand some of the shortfalls of quantifying outcomes and relying on some of these tools and metrics, which may actually result in sub-optimal advice for our clients.

Key Takeaways

Lifetime income should be the cornerstone of a retirement strategy. For almost most of your clients, all of their essential expenses should be covered with income they cannot outlive. Fifty thousand a year of Social Security benefits is a one-million-dollar, inflation-linked government bond. Telling clients this is valuable because it might change their perception of their wealth, how they should invest, etc.

When clients allocate wealth to lifetime income, not only can they spend more – when you pool that longevity risk, they can spend more from their portfolio – but they actually appear to spend more. There is very powerful evidence here that there is this behavioral benefit to allocating their lifetime income. It is not too dissimilar from buckets. Buckets are a great example of a strategy that can really help a client take on more risk in retirement because they better understand how the portfolio is funding income over time. The behavioral part of why having more money in lifetime income is powerful and worth discussing with clients.

Finally, there is an art and science in determining the right client strategy. The art is understanding behaviorally how clients want to accomplish goals, how they perceive outcomes, and what they want to do. The science is understanding how products work, how the landscape is evolving over time, and why certain products may be more attractive today or less attractive than they were ten years ago.

All this takes effort, but it is your job as a financial advisor to help your clients accomplish their financial goals. I am not convinced you can do a very effective job, especially for retirees, if you do not understand how annuities work and for which types of clients it could benefit most by allocating savings to them.