The federally insured reverse mortgage program, which Congress created in 1989 and improved in recent years, is the safest way for a retiree to access his housing wealth without giving up his home. Congress named it the Home Equity Conversion Mortgage, or HECM. This is the reverse mortgage that is chosen by roughly 95 percent of homeowners today.

The HECM is a financial tool which scholars in your industry have found to provide significant portfolio survival protection, especially when a HECM strategy is implemented early in retirement, and especially when that strategy begins with the creation of a HECM line of credit as soon as the client reaches the qualifying age of 62.

If you look at the retiree segments on a hypothetical bell-curve, you can see that our traditional clients used to be only the clients who were house rich and cash poor. This is because the mainstream media has always described the HECM as a loan of last resort. It is also because HECMs used to always have very high up-front costs. But now, scholars in your field have quantified the benefits of proactive, strategic use of HECMs by the middle group of retirees, the so-called mass affluent.

Retirees in this group are not massively affluent. Rather, they are the great mass of people who are not quite affluent. This group of roughly 11 to 15 million people tend to own a home and a modest investment portfolio. For this group, the primary focus is to avoid outliving their assets. These are the people who can benefit from the strategic use of a HECM, because funds received from a HECM are loan proceeds, therefore they are not treated as income.

How the HECM Programs Work

Before I explain the strategic benefits of a HECM, let’s first take a look at the HECM program and how it works. The HECM program was created by Congress in 1989 to provide older homeowners with a safer alternative to the reverse mortgages that were available at the time. HECMs provide solid guarantees and some very flexible options that earlier reverse mortgages did not provide. This is why HECMs can be useful in a wide range of circumstances.

The HECM program is regulated by the US Department of Housing and Urban Development, and all HECMs are insured by the Federal Housing Administration, which is part of HUD. To qualify for a HECM, the client must be age 62 or older. Money can be borrowed as a lump sum, or as a payment plan that provides level monthly payments, or the client can choose to leave the money sitting in a line of credit to be accessed as needed. The client can also choose any combination of these options, and the client can switch between options later on. Debt service is never required. In other words, the client is never required to make monthly loan payments. All principle and interest can be deferred, which causes the loan balance to grow over time. The loan balance does not have to be paid back until the last remaining borrower has died, sold the home, or vacated the home for 12 consecutive months. A HECM is non-recourse, meaning that the homeowner and their heirs are not personally liable for the debt.

The debt is secured only by the home. This is a nice guarantee in case the home is upside-down when the borrower moves out or passes away. The only way to default on a HECM is through technical default. In other words, doing things that put the property at risk, such as failing to pay property taxes, failing to maintain hazard insurance, or letting the property fall into disrepair.

Consumer Safeguards in the HECM Program

Let’s take a look at the consumer safeguards that are embedded into the HECM program. If the client chooses to receive monthly payments or chooses to have a HECM line of credit, both of these are guaranteed, regardless of what happens to home values, etc. Remember, this is federally insured. The borrower continues to own the home. One of the many myths about HECMs is that the lender will take the house, but this is just a myth. As long as at least one of the borrowers resides in the home, there is no maturity date for the loan. Debt service is never required. Assuming that the client chooses not to make any debt service payments, it is important for the client to understand that the more he borrows from the HECM over time and the longer he lives, the larger the loan balance will grow, due to the deferred interest.

Because of this fact, mandatory third-party HECM counseling is required before the client can sign an application for a HECM. The counseling is simply a phone call with an independent, HUD approved, non-profit housing counseling agency. The lender provides the client with a list of HUD approved agencies that offer the HECM counseling. The client chooses an agency from the list and schedules the counseling. The counselor provides basic information about the HECM program during the counseling. This is information that the client will already know if the client has consulted with a responsible reverse mortgage salesperson. There are never any pre-payment penalties. The borrower can pay down their balance, pay off the balance, refinance, or sell the house without any pre-payment penalty. In fact, it is possible to refinance a HECM into a new HECM in order to get more money if home values have increased substantially.

What Happens When the Owner Dies?

If there is equity remaining when the borrower moves, sells, or dies, the remaining equity belongs to the borrower or their estate. The lender is not entitled to anything other than the loan balance. What is most important about this feature is that the homeowner has secured the mortgage only with the property and the HECM is non-recourse. This means that if the home is underwater at the end, no deficiency judgment may be taken against the borrower or his estate. This is true even if the FHA no longer exists.

So let’s take a look at the options for the heirs after a HECM borrower passes away. Ownership of the home passes to the estate according to the client’s will or living trust. The estate will be notified regarding the amount of the HECM loan balance that is coming due, and an independent appraisal of the property’s value will be performed in order to determine whether or not there is equity remaining. If the debt is less than the appraised value, in other words there is equity remaining, then the options available to the estate are as follows:

- Keep the home by paying back the debt, typically through a refinance. If the heirs choose this option, they are given at least three months, and they can typically get an extension.

- Sell the home and keep the net proceeds from the sale after the loan balance is repaid, just like when a home is sold that has any type of mortgage on it. The estate typically has nine months to do this, sometimes longer.

- If the home’s value at the end is less than the loan balance, in other words the debt is greater than the home value and there’s no equity left, then the estate still has options. The heirs can keep the home by paying back 95 percent of the home’s value, instead of having to repay the entire loan balance to keep the home. Or, they can deed the home to HUD. Either way, the debt is erased thanks to the non-recourse provision. There is no effect on anyone’s credit score or credit history. In fact, HECMs do not even show up on my clients’ credit reports, because it’s only secured by the home, and no one has any personal responsibility for the debt. The lender relies solely on the FHA to make the lender whole if the debt is greater than the home value.

Qualifying for a HECM

All persons on title must be at least 62 years old. A common question that I receive is, “What if the client is a married couple and only one spouse meets the age requirement?” The answer is that the older spouse can qualify for the HECM, but only if the spouse who is under the age of 62 removes herself from title. In this case, the younger spouse is known as, “the non-borrowing spouse.” Obviously there is risk associated with being a non-borrowing spouse. Fortunately, HUD created new rules last year which provide some protection to non-borrowing spouses. Under the new rules, the HECM loan balance will not come due when the borrower passes away, as long as the non-borrowing spouse has continued to live in the home. The loan will not come due until both spouses have permanently vacated the home or passed away. This is a welcome improvement to the rules. However, a non-borrowing spouse will not be allowed to draw funds from the HECM after the borrower has passed away. Therefore, it is typically best to wait until both spouses are age 62 before getting a HECM.

Only primary owner-occupied residences qualify. The residence can be a house, or a two, three, or four unit property, or a HUD approved condo. No liens can remain on the property. Any mortgage or other liens must be paid off at closing. Typically, it is the HECM money that is used to extinguish the mortgage or other liens. In other words, the homeowner replaces their mortgage with the HECM. What if the HECM cannot provide enough money to pay off the client’s mortgage? In this case, the client does not qualify for a HECM unless they are willing and able to bring some of their savings to the closing to cover the shortfall.

The last rule is a brand new rule that HUD put into effect this week after about two years of working on this rule. It is called the “financial assessment.” Lenders are now required to review the applicants’ income, assets, and credit history, to determine the applicants’ ability and willingness to meet their obligations of home ownership, namely their property taxes, homeowner’s insurance, routine home repairs, and their HOA dues if they live in a condo. If the applicant fails the financial assessment, the lender will be required to set aside some of the client’s HECM funds to cover future property taxes, homeowner’s insurance, etc. These funds that are set aside are not borrowed. They do not increase the debt. They are simply set aside in the same way that money sitting in a HECM line of credit is just sitting there not borrowed yet. This set aside rule will prevent some applicants from being approved due to the following simple math: if an applicant who fails the financial assessment also has a mortgage on their home, and if the HECM will not provide enough money to pay off the mortgage and fund the set-side, then the application will be denied.

The final rule is, you cannot qualify for HECM if you own another home that has an FHA mortgage.

Types of HECMs

Let’s take a look at the types of HECMs that are currently available. The first type is a fixed-rate HECM. With a fixed-rate HECM, funds can only be received as a single lump sum at closing. There are no other ways to receive the funds. This is because in lending, if it’s a fixed rate, it’s pretty much impossible to offer a fixed rate and still offer open-ended credit.

Adjustable rate HECMs are much more flexible. The borrower can choose to receive monthly payments, they can choose to have the money just sitting available in a line of credit, they can take a lump sum, or they can choose any combination of these options. They can also switch between these options at any time.

There are two types of adjustable rate HECMs. The first is the monthly adjusting rate HECM. This is the type of HECM that has existed ever since 1989 when Congress created this program. The interest rate is the one month LIBOR, plus the lender’s margin. Lenders’ margins currently range between two percent and three percent.

The annually adjusting rate HECM was introduced last year. This HECM provides significant protections against rising rates. To begin with, the rate adjusts annually instead of monthly. Also, the lifetime cap on the interest rate is much lower than it is with the monthly adjusting rate HECM. It is only five percentage points above the starting rate, instead of 10 percentage points above the starting rate. There is also a two percent annual cap on the interest rate, if the customer chooses an annually adjusting rate HECM.

What Does a HECM Cost?

Let’s first take a look at the out-of-pocket cost to get a HECM. Simply $300 out of pocket goes straight to the appraiser, and also the HECM counseling agency will charge anywhere between $100 and $150. That is it.

Now let’s take a look at the finance closing costs. These costs can be paid up front, but no one ever chooses to do that. So they are typically just added to the loan balance. In other words, they are financed. Thanks to a rule change recently, the FHA’s initial MIP (mortgage insurance premium) is now significantly lower in most cases. As long as the borrower agrees to take less than 60 percent of the total amount available within the first year, then the FHA’s MIP is only one half of a percent instead of two-and-a-half percent. This is a big improvement.

The third party closing costs are the same as they are with any refinance transaction. Here in San Diego County, they’re around $2,000 to $2,400. The lender’s origination fee depends on the interest rate. It could be as high as $6,000, or it could be negative; in other words, a lender credit.

Different Ways to Take the Money

There are three different ways to take the money: lump sum, line of credit, or monthly payments.

If the borrower chooses to receive monthly payments, there are two different types of monthly payment plans. 10 year payments are guaranteed to continue for as long as at least one borrower remains in the home, up to age 120. Term payments depend on the term chosen by the borrower. It can be any length of time. The shorter the term, the larger the monthly payments. The borrower can switch from a monthly payments plan to a line of credit at any time, or switch between 10 year payments and term payments at any time.

Now let’s take a look at the HECM line of credit. This unique line of credit cannot be frozen or arbitrarily reduced, and remember this is federally insured. This is one of the many reasons why this can be such a useful financial planning tool. Amazingly, all of the unused credit will actually grow for the client based on the credit line growth rate. This growth is guaranteed even if home values fall. There is also no limit to this growth. The credit line growth rate is the same rate at which the loan balance is growing, which is the LIBOR plus the lender’s margin plus the FHA’s 1.25 percent MIP. The FHA adds that 1.25 percent MIP on top of the interest rate for every type of HECM.

Since the line of credit is guaranteed and growing, it reduces the necessity of holding cash reserves. This could be treated as revolving credit. If the client chooses to pay down the loan balance, the available credit increases accordingly, just like with a regular line of credit. The client can convert some or all of his available credit into monthly payments at any time. There is no cap on the credit line growth, even though the loan balance is capped by the HECM’s non-recourse provision. In other words, if we have another Great Recession or Great Depression and home values collapse, the credit line is guaranteed to be there and guaranteed to keep growing based on the credit line growth rate, even though the amount that will have to be paid back, if the borrower passes away, is capped by the home’s value, no matter what that home value is.

What is the Difference Between an HECM and a HELOC?

Let’s take a look at a HECM line of credit versus a HELOC (home equity line of credit). With a home equity line of credit, the credit line can be frozen or cancelled. This cannot happen with a HECM line of credit. A HECM line of credit is easier to qualify for, because the borrower never has to make monthly loan payments. Therefore, we do not have to do underwriting based on the ability to make monthly payments.

With a HECM line of credit, there is no required debt service. With a HECM line of credit, you will not have clients who experience payment shock, because there’s no such thing as monthly payments resetting to switch from interest only to principal and interest. And of course with a HECM line of credit, the available credit is guaranteed to grow for the client every month at the credit line growth rate. The loan to value ratio for HECMs is very dependent on the 10 year LIBOR swap rate at origination.

Loan to value (LTV) ratios are inversely related to something that is called the “expected average interest rate” at the time of the origination. If the expected average interest rate is below 5.06, then the LTV ratio will be the highest loan to value ratio possible. But if it is above 5.06 at the time that the client gets their HECM, then the lower the LTV will be. So for adjustable rate HECMs, the expected average interest rate equals the lender’s margin plus the 10 year LIBOR swap rate. For fixed rate HECMs, the expected average interest rate is simply equal to the fixed interest rate. The fixed rates currently available to choose from are between 4.25 and 5.56. The age of the applicant also affects the LTV, but interest rates affect it more.

Here’s an example: a 62-year-old who qualifies for 50 percent LTV today but delays getting a HECM until he is five years older, will qualify for only 33 percent LTV if the 10 year LIBOR swap rate has increased a modest two percentage points while he delayed. Today’s rates are one reason for the mass affluent to secure a HECM sooner rather than later and why it makes sense to get a HECM line of credit as soon as the client reaches the age of 62, even if he might not need the money for years or even decades.

HECM Strategies

The dangers posed by sequence of returns, risk, and reverse dollar cost average are at the heart of two studies published in 2012 in the Journal of Financial Planning. Investigators quantified the effects of substituting home equity draws for portfolio draws, in order to avoid selling portfolio assets in a poor market environment.

The first paper was published by Barry and Stephen Sacks. They tested the long-held conventional wisdom that retirees should only get a reverse mortgage after they have depleted their assets. You might have seen this so-called wisdom espoused by financial writers such as Jane Bryant Quinn and Ron Lieber of the New York Times. The only problem with their widely-read advice is that it turns out to be completely wrong. Like many other financial writers, these writers never did the math. In 2012, Drs. Barry and Stephen Sacks compared three different reverse mortgage strategies for their groundbreaking research paper, which they cleverly titled, Reversing the Conventional Wisdom.

The first strategy that they analyzed is the old passive conventional wisdom of waiting and getting a HECM only as a last resort after the portfolio has been depleted. In other words, this first strategy, if it can be called a strategy, is simply a passive strategy. The other two strategies are proactive. They involve securing a HECM line of credit as soon as a client has reached the distribution phase of their financial plan. The age that the researchers used in their study is age 65, but it would be even smarter for a client to secure a HECM line of credit as soon as they reach the qualifying age of 62.

Of the two proactive strategies that the researchers studied, the first one is called the “coordinated strategy”. This is a strategy of drawing from the HECM line of credit instead of from the portfolio during periods when share prices are depressed. This is the most strategic of the three strategies. It minimizes the use of HECM draws while still protecting the portfolio.

The other proactive strategy, which the researchers labelled the reverse mortgage first strategy, is an exact reversal of the conventional wisdom. In this simple strategy, the client immediately begins living off of regular draws from their line of credit and does not take any distributions from the portfolio until the line of credit has been completely exhausted. It should be noted that a client who wishes to implement this strategy could just as easily choose to receive term or tenure payments from their HECM instead of choosing a line of credit. Either way, it turns out that this strategy is far superior to the passive conventional wisdom of only getting HECM as a last resort after depleting the portfolio. But the coordinated strategy works even better, as you will see.

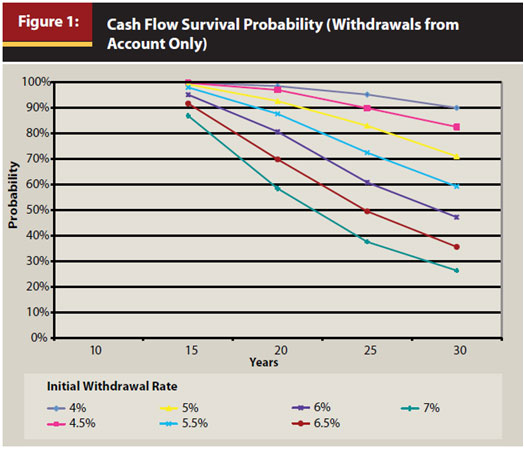

Before we look at the effects of the three strategies, let’s first take a look at the effects of different initial withdrawal rates on cash flow survival probabilities without any HECM strategy. For this chart and the following chart, the researchers ran 1,000 portfolio simulations covering 30 years.

At the four percent withdrawal rate, the probability of success after 30 years is 90 percent. That’s the top line in this graph. In other words, the portfolio succeeded for 30 years in 90 percent of the simulations. At higher withdrawal rates, the probabilities of success rapidly declined.

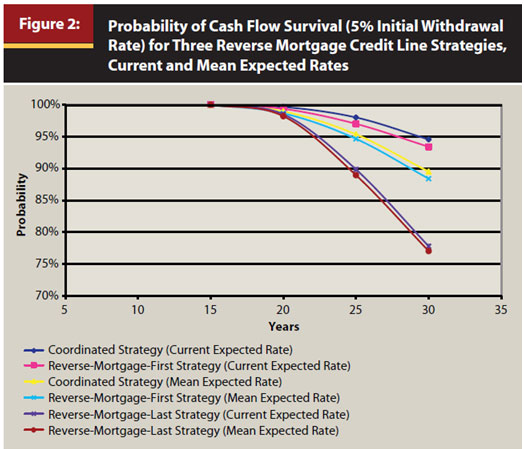

This next chart shows that the conventional wisdom of getting a reverse mortgage as a last result provides the worst outcome. These comparisons are for a five percent initial withdrawal rate. The results are even more dramatic for withdrawal rates greater than five percent. The horizontal axis is the number of years up to 30, the vertical axis is the probability of cash flow survival. Note that this is the probability of cash flow survival, not just survival of the portfolio. In other words, the probability of survival of all cash flow, including cash from the reverse mortgage.

For each of these strategies, two lines are plotted on the graph. One line is based on the HECM being obtained during a period of low interest rates, resulting in the largest possible HECM line of credit. The other line is based on the HECM being obtained during a period of higher rates, resulting in a smaller line of credit. Remember that the amount of money that any HECM can provide depends a lot on what the expected average interest rate is at the time of origination.

Therefore in today’s low-rate environment, clients are able to secure the largest HECM line of credit possible. As you might expect, the size of the line of credit had an effect on how many of the simulations succeeded.

So let’s take a look at the bottom two lines, the dark purple and dark red. These represent the conventional wisdom of just waiting and getting a reverse mortgage only after the portfolio has been depleted. As you can see, the probability of success after 30 years is only around 77 percent. And again, this is based on a five percent initial withdrawal rate. In other words, roughly 23 percent of the simulations failed to provide enough cash flow for 30 years. The two lines at the top, the dark blue and pink, represent the two proactive strategies based on securing a HECM line of credit while interest rates are low in order to get the largest HECM line of credit possible. The yellow and blue lines in the middle represent those same two strategies if the client got their HECM during a period of higher interest rates, and therefor they received a smaller line of credit.

The interest rates that were used for those scenarios would be the mean average rate over the past, I think, 47 years. As you can see, the coordinated strategy performs slightly better than the strategy of exhausting the line of credit before taking portfolio distributions. Both strategies perform far better than the passive non-strategy of exhausting the investment portfolio before tapping into the home equity. The researchers concluded that for initial withdrawal rates between 4.5 percent and seven percent, we have found substantially greater cash flow survival probabilities when the reverse mortgage credit line is used in either of the two active strategies, rather than in the conventional passive strategy as a last resort.

We have also found that use of these active strategies is likely to result in a higher residual net worth after 30 years, compared to the conventional strategy. Residual net worth is defined as the value of the retiree’s portfolio and the remaining home equity after 30 years. So what they found is that the superiority of the proactive strategies over the passive strategy does not come at the expense of residual net worth.

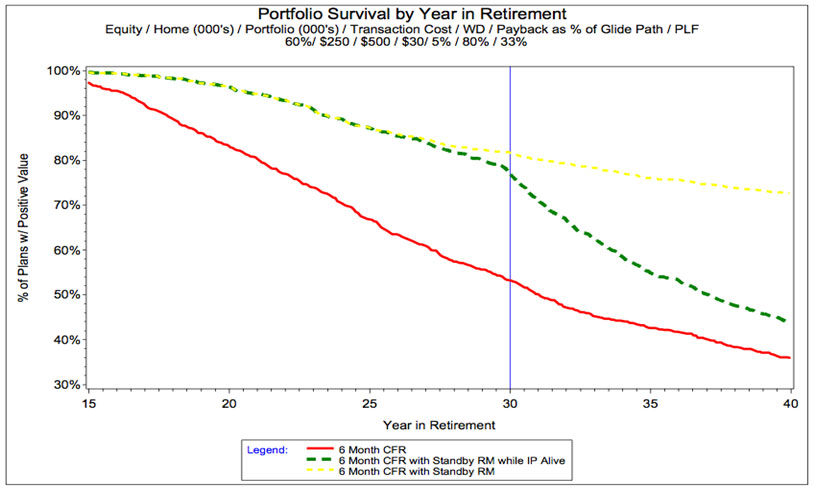

The second study confirming the power of a HECM line of credit was published in August of 2012. John Salter and Harold Evensky were so impressed by the HECM line of credit and its immunity against being frozen or cancelled that they undertook a study to determine if their two bucket retirement distribution approach would be enhanced by a third bucket. They called the third bucket the “standby reverse mortgage,” and it consisted of the HECM line of credit. One of the benefits of this strategy was immediate. By adding the third bucket, they were able to reduce the cash flow reserve bucket from a two year reserve to a six month reserve. Therefore, less money is tied up in the cash flow reserve bucket, and more money is dedicated to the investment bucket. This is an improvement on opportunity cost. Dr. Salter and Mr. Evensky modeled home equity draws substituting for investment portfolio withdrawals during volatility troughs when the portfolio value was not high enough to sustain the preferred glide path.

This chart compares the two bucket cash flow reserve bucket strategy with the three bucket stand-by reverse mortgage strategy.

Using the three bucket stand-by reverse mortgage strategy, HECM draws are substituted for portfolio withdrawals when the portfolio is performing below the glide path. When the market recovers enough for the portfolio to perform better than the glide path, shares are sold in order to pay down the HECM loan balance and replenish the HECM line of credit. Looking at the graph, you can see that the two bucket strategy, the one without the HECM, which is the red, six-month cash flow reserve strategy, produced significantly fewer surviving plans at 30 years. You can see that roughly 50 percent survived at the end of 30 years compared to 80 percent for the three bucket stand-by reverse mortgage strategy. The yellow line demonstrates added protection if the client continues to draw from the stand-by reverse mortgage for an additional 10 years or so after the investment portfolio is depleted.

Dr. Salter and Mr. Evensky concluded that the stand-by reverse mortgage strategy is appealing for four reasons:

- It diminishes the need for the cash bucket and thus the opportunity cost of holding cash

- It provides flexibility in that the investment bucket is not sold during bare markets

- It allows the retiree to decide how much home equity is used to meet their needs, and

- It increases the life expectancy of an investor’s nest egg.

In other words, don’t feed the bear; draw from the portfolio only when portfolio returns are positive.

What is a Purchase HECM?

The purchase HECM, which is also known as the HECM for purchase, or the purchase reverse mortgage. The purchase HECM allows the client to finance the purchase of a new primary residence by getting a HECM on the new home as part of the purchase transaction, instead of having to qualify for a regular mortgage and make monthly payments and instead of having to pay all cash.

The purchase HECM was created a few years ago, and it solved a problem where clients could only get a HECM on a home that they were already living in. But what about clients who wanted to buy a more appropriate home for their needs, or move to a better neighborhood, or move closer to their children? So HUD addressed this need by introducing the purchase HECM.

So if the client is age 62 or older, they can finance the purchase of a new primary residence by getting the HECM on the new home as part of the purchase transaction, instead of getting a traditional mortgage or paying all cash. As with a regular mortgage, the HECM money goes to the seller at the close of escrow. However, this is still a HECM, so there are significant benefits to the buyer – no debt service requirement, and it’s easy to qualify for.

Remember that the LTV for a HECM is conservative. The client will need to bring a down payment of roughly 25 to 50 percent, depending on their age. And the remaining 50 to 75 percent will be financed by the purchased HECM. So now the client has purchased the right home for the retirement, and has withdrawn a lot less money from their portfolio than they would have if they were a cash buyer, and they will never face the burden and risk of required monthly payments. Put another way, the client is able to leverage his down payment, buy the house he really wants, and never have to make monthly loan payments and no debt repayment is required until he has permanently vacated his home or transferred title or passed away.

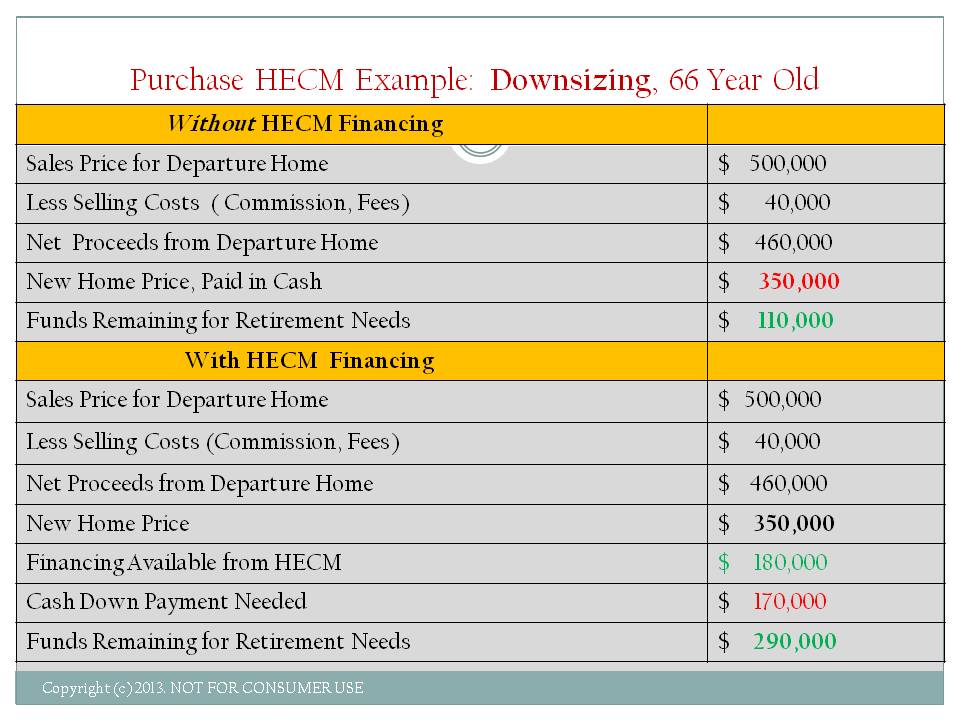

Here’s an example of the math. This is an example of downsizing. So the client sells his old home for $500,000, and subtracts out the realtor’s commission of $40,000, so his net proceeds are $460,000. He purchases a new home. This top part of this chart is without HECM financing.

So if he purchases a new home he’s paying cash, so he only has $110,000 left to put in his portfolio.

Now let’s look at the HECM financing option. So he sells the home, and he nets $460,000. The new home costs $350,000, the HECM in this example provides only $180,000, so this client is rather young. He’s 66 years old. So therefore the down payment is only $170,000 instead of $350,000. Therefore, $290,000 is going into his retirement portfolio instead of just $110,000.

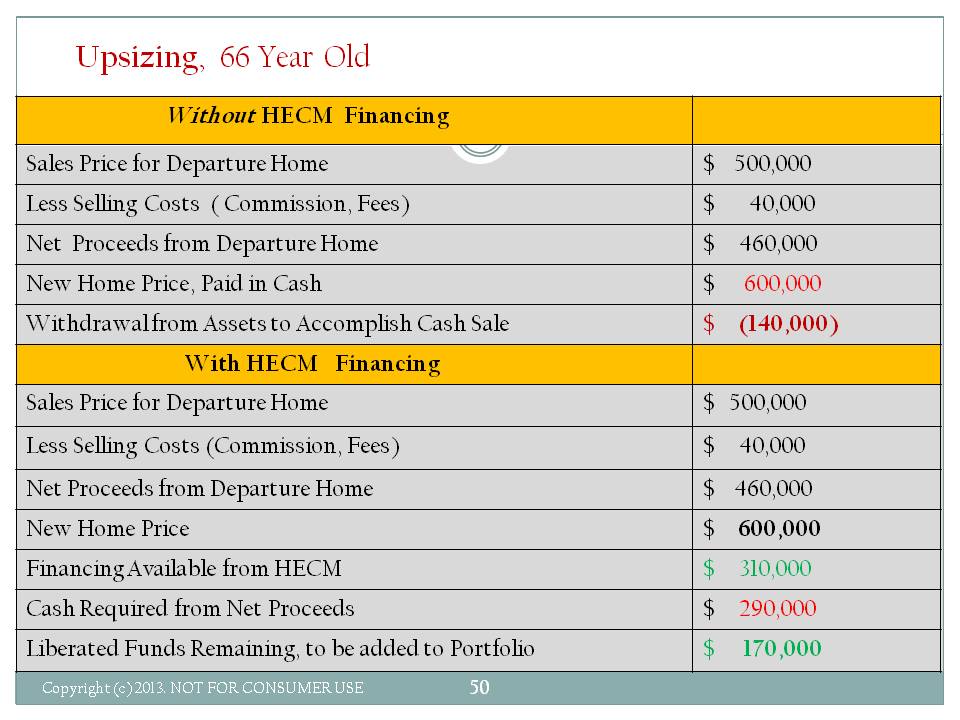

Here’s another example. This example is an upsizing instead of downsizing, where the client is buying the home for $600,000 after selling his old home for $500,000.

So in this example, he’s having to withdraw money from his portfolio, $140,000, in order to complete the purchase. But with the HECM financing, when you get down to the bottom line, he’s actually able to put $170,000 into his portfolio instead of withdrawing $140,000. So in other words, that’s a net improvement to his portfolio of $310,000.

Takeaways for Advisors

The takeaways for advisors regarding HECMs are:

- Consumer safeguards protect the housing asset.

- The HECM can protect the investment portfolio by improving cash flow survival probability and enhancing residual wealth.

- The HECM line of credit provides benefits that home equity lines of credit do not.

- The HECM line of credit insures access to housing wealth in the future.

- It is guaranteed.

- It cannot be cancelled or it cannot be frozen or arbitrarily reduced.

- In the current low interest rate environment, it makes sense for someone who is 62 to get a HECM line of credit now, even if he’s not going to need it for many many years.

- And finally, the purchase HECM is a good way to protect the portfolio.