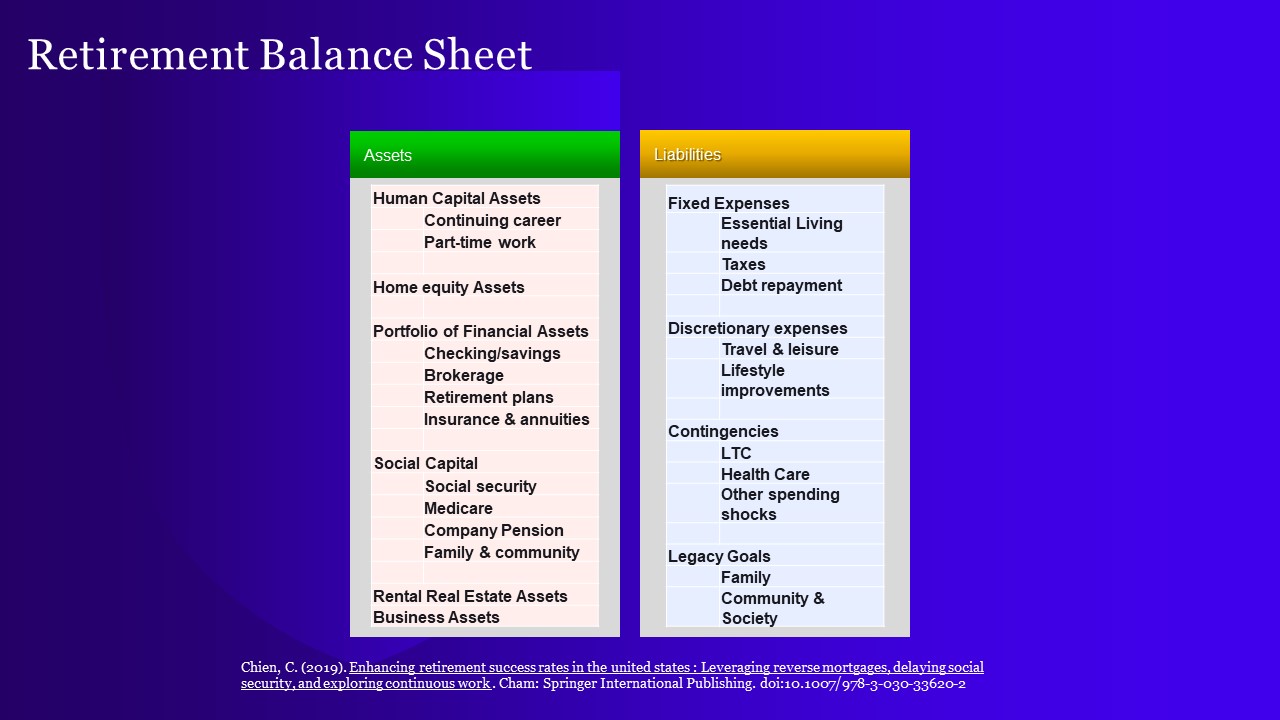

However, a typical balance sheet has three components: you have your assets, you have your liabilities, and at the end of the day, you will have your equity. This is a very traditional accounting type of balance sheet. However, there are only two components when we speak about retirement, specifically from a retirement balance sheet perspective. We will be looking at, first, the assets and then second, the liabilities. The liabilities will be calculated to represent future expenses, such as your retirement income, that you will need for the next 30, 40, or 50 years.

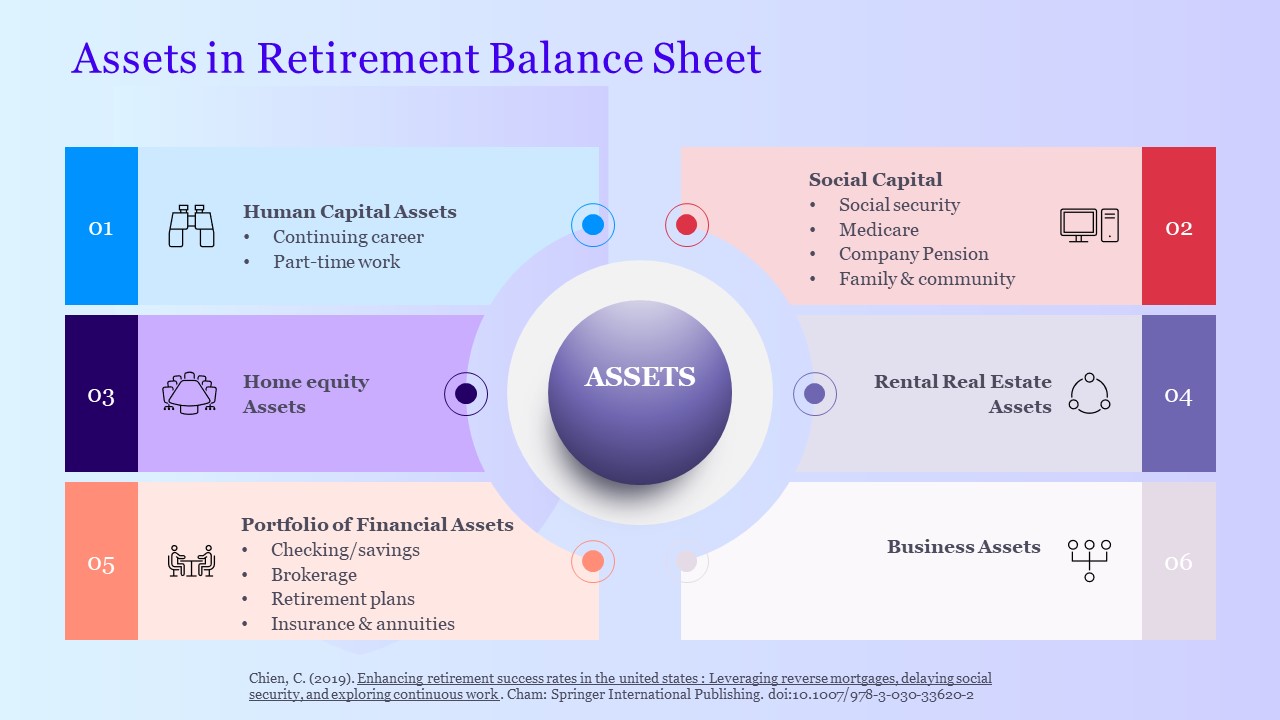

So, what do we mean by assets in the retirement balance sheet?

First, let’s look at what we call human capital assets. Human capital assets mean someone may continue to work full-time or part-time. Take my husband as an example. He is 60 years old, although he wants to retire like yesterday. But I encourage him to continue to work full-time. His goal is to work for another five years before he retires from his current job.

We expect him to continue to work part-time after he retires from his full-time job. He is not going to do completely nothing, and doing nothing during retirement may or may not be good for his mental and physical health.

Discuss human capital assets with your clients. Your clients must also be physically and mentally able to continue working full-time or part-time. Remember to explore these options, and remember that it is a blessing and a privilege to continue working full-time or part-time in retirement.

Home equity is the most overlooked asset in retirement income planning. What do I mean by that? Americans are very good at building their housing assets. Most people desire to purchase their home at a very early age and stay in their home for retirement. Therefore, home equity assets ought to be explored with clients as well.

Portfolio financial assets are probably the most familiar area that practitioners typically discuss. This includes checking, savings, brokerage, and retirement accounts such as Roth, IRA, 401k, you name it, and even insurance annuities accounts.

Social capital includes Social Security, retirement benefits, Medicare, company pensions, and potentially family and community supports. In some cases, people may not have sufficient Social Security retirement benefits or a company pension. They might need to rely on family or communities for support. For example, many of you probably are familiar with the sitcom Golden Girls, in which older women cohabitate with other women in the same household complex.

Rental real estate assets are one of those assets that clients often talk about, but financial planning practitioners need help with what to do with them. Many of my clients have rental real estate assets, so we talk about it, but I do not recommend that they take specific actions. I recommend that they explore other alternatives with their CPAs and realtors to make sure some things are considered. Therefore, take inventory of your client’s real estate assets because often, it could be a lot, especially for those who do not necessarily know how to invest in a portfolio of financial assets as they tend to invest in what they know, such as real estate.

For those not specializing in succession or exit planning, business assets are likely assets the most missed on the retirement balance sheet. First off, it isn’t easy to pinpoint the value. Many of the advisors I know use rough estimates. However, the rule of thumb is to ask your clients how much they think their business is worth and suggest that they do an appraisal. For example, several years ago, I was working with a client who happened to be a four-partner financial planning firm. I asked them when the last time they had their business appraised was. Let me repeat this question again. Instead of asking clients, “How much do you think your business is worth?” ask, “When was the last time you had your business appraised?” This question will get them thinking about not only doing an appraisal of their business but also how much it is worth.

First, let’s look at what we call human capital assets. Human capital assets mean someone may continue to work full-time or part-time. Take my husband as an example. He is 60 years old, although he wants to retire like yesterday. But I encourage him to continue to work full-time. His goal is to work for another five years before he retires from his current job.

We expect him to continue to work part-time after he retires from his full-time job. He is not going to do completely nothing, and doing nothing during retirement may or may not be good for his mental and physical health.

Discuss human capital assets with your clients. Your clients must also be physically and mentally able to continue working full-time or part-time. Remember to explore these options, and remember that it is a blessing and a privilege to continue working full-time or part-time in retirement.

Home equity is the most overlooked asset in retirement income planning. What do I mean by that? Americans are very good at building their housing assets. Most people desire to purchase their home at a very early age and stay in their home for retirement. Therefore, home equity assets ought to be explored with clients as well.

Portfolio financial assets are probably the most familiar area that practitioners typically discuss. This includes checking, savings, brokerage, and retirement accounts such as Roth, IRA, 401k, you name it, and even insurance annuities accounts.

Social capital includes Social Security, retirement benefits, Medicare, company pensions, and potentially family and community supports. In some cases, people may not have sufficient Social Security retirement benefits or a company pension. They might need to rely on family or communities for support. For example, many of you probably are familiar with the sitcom Golden Girls, in which older women cohabitate with other women in the same household complex.

Rental real estate assets are one of those assets that clients often talk about, but financial planning practitioners need help with what to do with them. Many of my clients have rental real estate assets, so we talk about it, but I do not recommend that they take specific actions. I recommend that they explore other alternatives with their CPAs and realtors to make sure some things are considered. Therefore, take inventory of your client’s real estate assets because often, it could be a lot, especially for those who do not necessarily know how to invest in a portfolio of financial assets as they tend to invest in what they know, such as real estate.

For those not specializing in succession or exit planning, business assets are likely assets the most missed on the retirement balance sheet. First off, it isn’t easy to pinpoint the value. Many of the advisors I know use rough estimates. However, the rule of thumb is to ask your clients how much they think their business is worth and suggest that they do an appraisal. For example, several years ago, I was working with a client who happened to be a four-partner financial planning firm. I asked them when the last time they had their business appraised was. Let me repeat this question again. Instead of asking clients, “How much do you think your business is worth?” ask, “When was the last time you had your business appraised?” This question will get them thinking about not only doing an appraisal of their business but also how much it is worth.

On the right side, you will see estimated future fixed and discretionary expenses. Contingency expenses are also calculated for the future, as well as their future legacy goals. Together, these components complete the picture of a retirement balance sheet. Please take stock of your client’s information and place it into a retirement balance sheet so you will have a better understanding of which assets need to be matched to which liabilities.

On the right side, you will see estimated future fixed and discretionary expenses. Contingency expenses are also calculated for the future, as well as their future legacy goals. Together, these components complete the picture of a retirement balance sheet. Please take stock of your client’s information and place it into a retirement balance sheet so you will have a better understanding of which assets need to be matched to which liabilities.

How much you’ll be able to access home equity depends upon the interest rate. The current interest rate is relatively high, meaning that the HECM portion will be much smaller compared to a lower interest rate environment.

It is important to remember that default with a reverse mortgage is not the same as with a typical mortgage. The default in a HECM or reverse mortgage is typically past due on homeowner association or property taxes. If your clients want to consider a HECM, just make sure that they pay for their homeowner association and property taxes and keep the home maintained.

The key point to remember is that with the reverse mortgage, nothing is repaid until you die. If anything is left, it will go to your heirs.

Many advisors think reverse mortgages are unique to the U.S., which is incorrect. Reverse mortgages are available worldwide in selected countries. Why do I want you to know about that as a planner? Your clients might own real estate outside of the U.S. If they do, they can take a reverse mortgage on the home they own outside the U.S. The United Kingdom, Canada, and France are a few other countries that I listed in my published research in 2022.

The reverse mortgage was established in the 1980s in the U.S., but the HECM began in 1961 in the private sector and became federally backed in the early 1980s. Canada started its reverse mortgage in 1961, and the U.K. started it in 1965. I absolutely love France’s approach. Why? One option in France is that you can sell the reverse mortgage to desirable investors and live in that home as long as you survive.

Of course, there is government oversight regarding reverse mortgages. The Department of

Housing and Urban Development (HUD) is the oversight authority in the U.S. In Canada, it is the Franchise Consumer Agency of Canada. The U.K. is an investors’ compensation scheme. France is under the Ministry of Economic Finance and Recovery. Unlike the U.S., you can use a selected list of approved vendors or lenders. Canada has two banks you can use. In the U.K., like the U.S., you can use any approved lenders. In France, it is just willing investors. When doing this research, I had to find someone who read French to verify the information accordingly.

The reverse mortgage market in Asia is more significant than you’d imagine. Most Asian countries have higher homeownership percentages than the U.S. Here is a list of countries with reverse mortgages: Australia, Singapore, China, Taiwan, New Zealand, South Korea, China, Hong Kong, and India.

You will only know if a client owns homes in other countries if you ask. A client may be thinking about buying a villa in Italy or somewhere else for retirement. You can also help them with this option if they need additional retirement income.

How much you’ll be able to access home equity depends upon the interest rate. The current interest rate is relatively high, meaning that the HECM portion will be much smaller compared to a lower interest rate environment.

It is important to remember that default with a reverse mortgage is not the same as with a typical mortgage. The default in a HECM or reverse mortgage is typically past due on homeowner association or property taxes. If your clients want to consider a HECM, just make sure that they pay for their homeowner association and property taxes and keep the home maintained.

The key point to remember is that with the reverse mortgage, nothing is repaid until you die. If anything is left, it will go to your heirs.

Many advisors think reverse mortgages are unique to the U.S., which is incorrect. Reverse mortgages are available worldwide in selected countries. Why do I want you to know about that as a planner? Your clients might own real estate outside of the U.S. If they do, they can take a reverse mortgage on the home they own outside the U.S. The United Kingdom, Canada, and France are a few other countries that I listed in my published research in 2022.

The reverse mortgage was established in the 1980s in the U.S., but the HECM began in 1961 in the private sector and became federally backed in the early 1980s. Canada started its reverse mortgage in 1961, and the U.K. started it in 1965. I absolutely love France’s approach. Why? One option in France is that you can sell the reverse mortgage to desirable investors and live in that home as long as you survive.

Of course, there is government oversight regarding reverse mortgages. The Department of

Housing and Urban Development (HUD) is the oversight authority in the U.S. In Canada, it is the Franchise Consumer Agency of Canada. The U.K. is an investors’ compensation scheme. France is under the Ministry of Economic Finance and Recovery. Unlike the U.S., you can use a selected list of approved vendors or lenders. Canada has two banks you can use. In the U.K., like the U.S., you can use any approved lenders. In France, it is just willing investors. When doing this research, I had to find someone who read French to verify the information accordingly.

The reverse mortgage market in Asia is more significant than you’d imagine. Most Asian countries have higher homeownership percentages than the U.S. Here is a list of countries with reverse mortgages: Australia, Singapore, China, Taiwan, New Zealand, South Korea, China, Hong Kong, and India.

You will only know if a client owns homes in other countries if you ask. A client may be thinking about buying a villa in Italy or somewhere else for retirement. You can also help them with this option if they need additional retirement income.

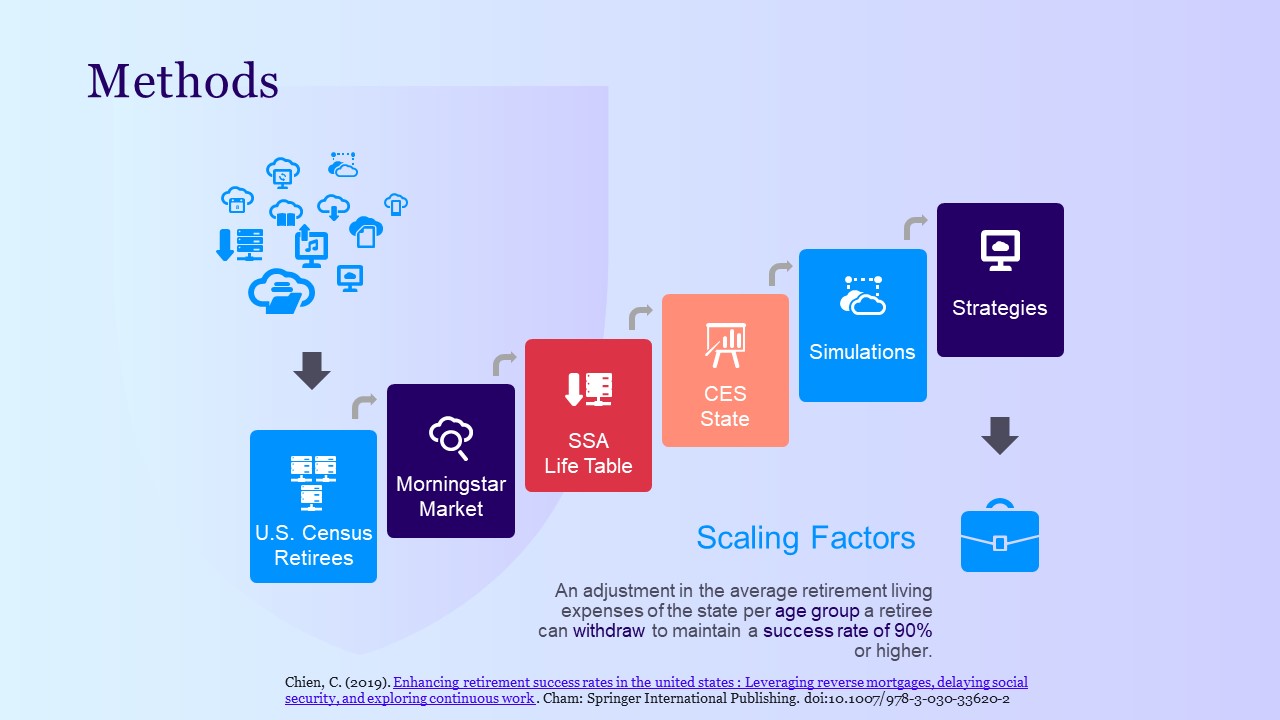

The U.S. Census dataset has retiree household asset information, including their Social Security retirement benefits, which tie directly to the Social Security Administration. I also used the Social Security Administration live table, which means that the mortality rate is calculated up to age 120 because I do not know when they are going to die.

I calculated the rolling market return using the Morningstar historical record, including equities and bonds.

The important thing I created was the Scaling Factor, which you can see in the graph below. The Scaling Factor is based on how much retirement will cost on average in a particular state. Every state’s average spending is different. Retirees in my state and age group typically spend $1,000 a month. If I have a higher income and net worth and want to spend $3,000 monthly, my scaling factor is 300%, or 3x my state’s spending average. This is what the scaling factor is for. Either you spend 100% of the state average or more than that average in terms of the calculation.

The research aimed to determine at what point scaling factors will always achieve at least 90% retirement success, meaning that no one runs out of money from their financial portfolio assets. If the scaling factor is less than 100, the retiree generally needs more retirement assets to maintain their standard of living at the state average and will eventually need help making ends meet.

Let’s look at the following graph.

The U.S. Census dataset has retiree household asset information, including their Social Security retirement benefits, which tie directly to the Social Security Administration. I also used the Social Security Administration live table, which means that the mortality rate is calculated up to age 120 because I do not know when they are going to die.

I calculated the rolling market return using the Morningstar historical record, including equities and bonds.

The important thing I created was the Scaling Factor, which you can see in the graph below. The Scaling Factor is based on how much retirement will cost on average in a particular state. Every state’s average spending is different. Retirees in my state and age group typically spend $1,000 a month. If I have a higher income and net worth and want to spend $3,000 monthly, my scaling factor is 300%, or 3x my state’s spending average. This is what the scaling factor is for. Either you spend 100% of the state average or more than that average in terms of the calculation.

The research aimed to determine at what point scaling factors will always achieve at least 90% retirement success, meaning that no one runs out of money from their financial portfolio assets. If the scaling factor is less than 100, the retiree generally needs more retirement assets to maintain their standard of living at the state average and will eventually need help making ends meet.

Let’s look at the following graph.

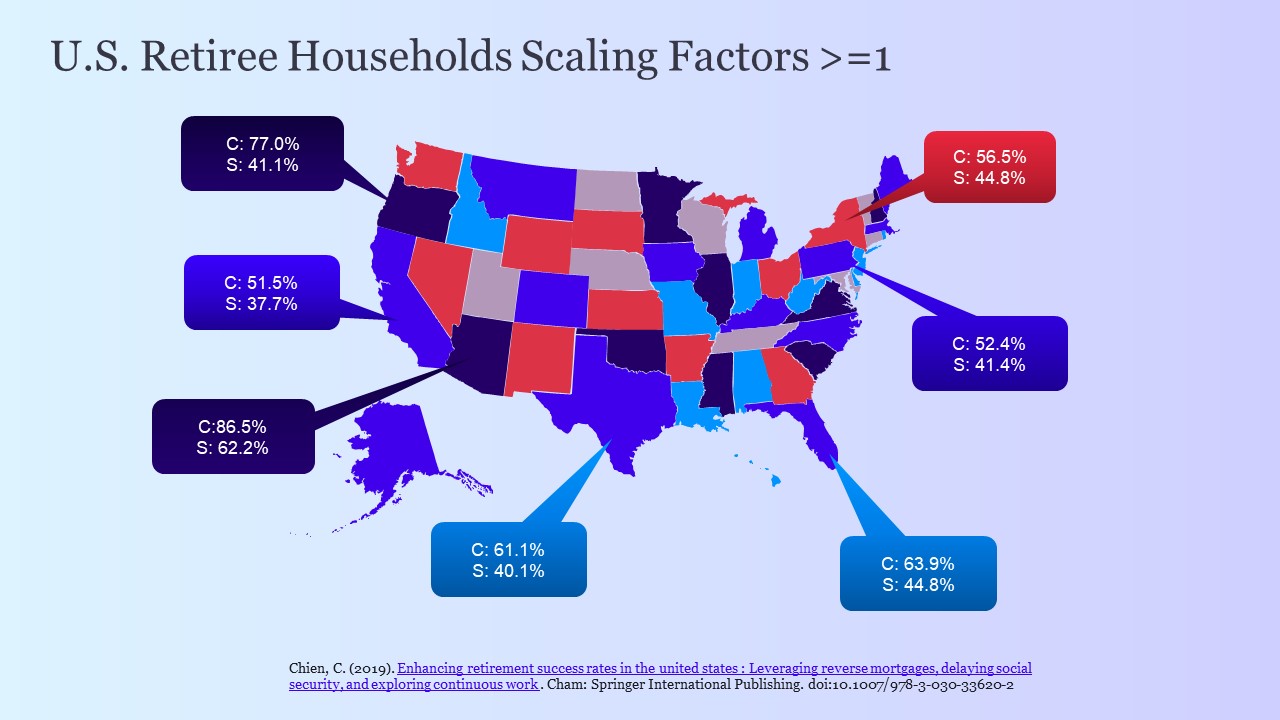

For households with couples in California, only 51% of the population will be successful in retirement. Only 37% of single households in California will be successful. Now, California has such a high cost of living. Look at Texas, where couples have a 61% success rate and single households 40%. Pennsylvania has a 52% success rate for couples and 41% for single households. Florida has a 63% rate for couples and a 44% success rate for single households. In New York, 56% for couples and 44% for single households. Arizona does better: 86% for couples and 62% for single households.

This tells you that most U.S. retiree households will not be successful in retirement. What does this mean? They will run out of money, and somebody must pick up those costs. That means you and I, the taxpayer, will always subsidize those who cannot make it.

When I talk about single households, I would like you to think about not just someone single because it could be divorcees, widows, and widowers. Think about that. We always want to help our clients plan for the last survivor. If you do not plan well, the last survivor will have a higher chance of failure when the other spouse dies.

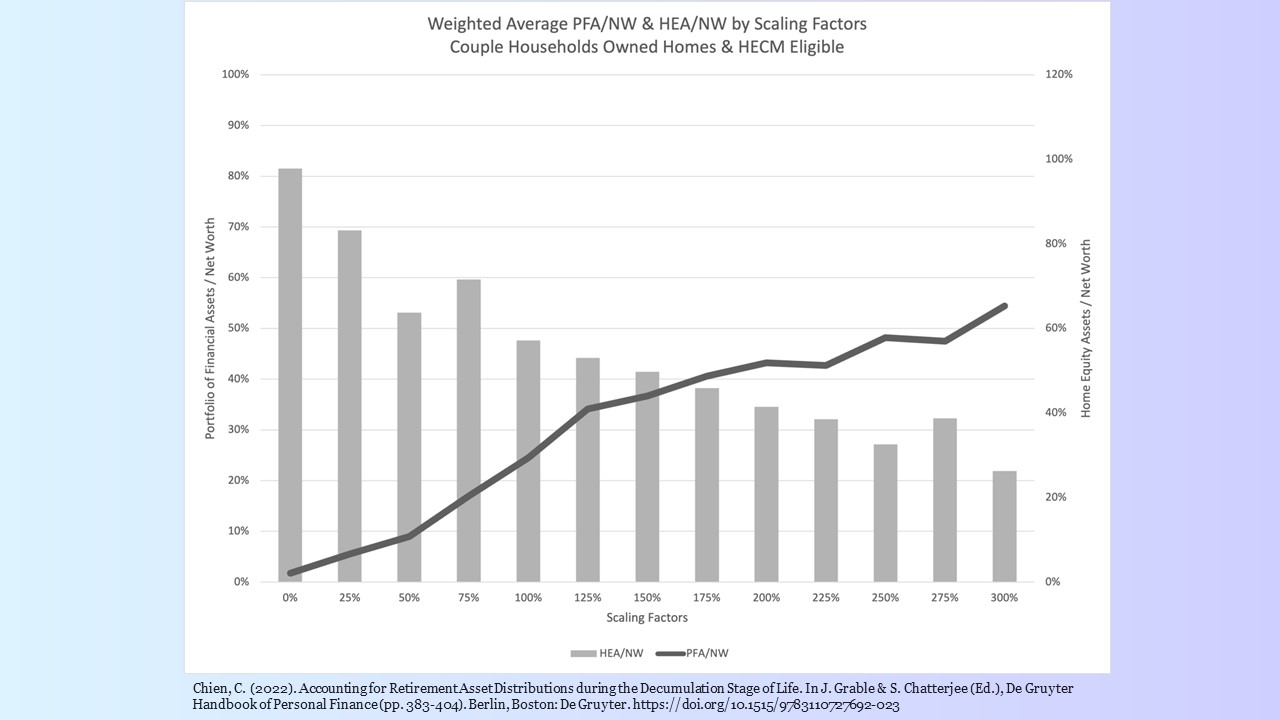

On the right-hand side, I use the percentage of their home equity divided by net worth. That will give us a percentage for comparison. I use the scaling factor in the horizontal area or the bottom of the chart, which is how much they want to spend. This can range anywhere between zero percent of the state’s average retiree spending and more than 300%, based on every state’s different average and different age group.

The more you want to spend (i.e., 300% of the state average), the more liquid assets you will need to be successful in retirement. And the more you want to spend, the less home equity assets (which are illiquid) you want as a percentage of total net worth.

It is more expensive for single households, such as singles, divorcees, widows, and widowers, to survive through retirement. Lower net-worth families tend to be house-rich and cash-poor. Higher net worth families tend to have lower home equity and higher liquid assets as a percent of total worth.

First, let’s look at what we call human capital assets. Human capital assets mean someone may continue to work full-time or part-time. Take my husband as an example. He is 60 years old, although he wants to retire like yesterday. But I encourage him to continue to work full-time. His goal is to work for another five years before he retires from his current job.

We expect him to continue to work part-time after he retires from his full-time job. He is not going to do completely nothing, and doing nothing during retirement may or may not be good for his mental and physical health.

Discuss human capital assets with your clients. Your clients must also be physically and mentally able to continue working full-time or part-time. Remember to explore these options, and remember that it is a blessing and a privilege to continue working full-time or part-time in retirement.

Home equity is the most overlooked asset in retirement income planning. What do I mean by that? Americans are very good at building their housing assets. Most people desire to purchase their home at a very early age and stay in their home for retirement. Therefore, home equity assets ought to be explored with clients as well.

Portfolio financial assets are probably the most familiar area that practitioners typically discuss. This includes checking, savings, brokerage, and retirement accounts such as Roth, IRA, 401k, you name it, and even insurance annuities accounts.

Social capital includes Social Security, retirement benefits, Medicare, company pensions, and potentially family and community supports. In some cases, people may not have sufficient Social Security retirement benefits or a company pension. They might need to rely on family or communities for support. For example, many of you probably are familiar with the sitcom Golden Girls, in which older women cohabitate with other women in the same household complex.

Rental real estate assets are one of those assets that clients often talk about, but financial planning practitioners need help with what to do with them. Many of my clients have rental real estate assets, so we talk about it, but I do not recommend that they take specific actions. I recommend that they explore other alternatives with their CPAs and realtors to make sure some things are considered. Therefore, take inventory of your client’s real estate assets because often, it could be a lot, especially for those who do not necessarily know how to invest in a portfolio of financial assets as they tend to invest in what they know, such as real estate.

For those not specializing in succession or exit planning, business assets are likely assets the most missed on the retirement balance sheet. First off, it isn’t easy to pinpoint the value. Many of the advisors I know use rough estimates. However, the rule of thumb is to ask your clients how much they think their business is worth and suggest that they do an appraisal. For example, several years ago, I was working with a client who happened to be a four-partner financial planning firm. I asked them when the last time they had their business appraised was. Let me repeat this question again. Instead of asking clients, “How much do you think your business is worth?” ask, “When was the last time you had your business appraised?” This question will get them thinking about not only doing an appraisal of their business but also how much it is worth.

The Liability Side of the Retirement Balance Sheet

The liability side of the retirement balance sheet is different from the traditional balance sheet. With today’s advanced medical treatment, people can live 20, 30, 40, or even 50 years in retirement. You want to help your client identify their current spending, collecting data such as fixed expenses, discretionary expenses, contingency expenses, and legacy goals. You also want to ask your clients how long they think their retirement will last. Is it age 90, age 95, or age 120? The Social Security Administration estimates people living up to 120 years old. My father-in-law passed away late last year. He was 96. People do live a very long time. Ask your clients about their family health history. Several life insurance companies have their policy set at a certain age, which means that if your clients did not die before that age, they will not pay death benefits and will potentially pay out the cash value. Check for those critical ages in the life insurance and how long the client thinks they might live. Here is the entire retirement balance sheet. On the left-hand side, you will see human capital assets, home equity assets, a portfolio of financial assets, social capital assets, rental real estate assets, and business assets.

On the right side, you will see estimated future fixed and discretionary expenses. Contingency expenses are also calculated for the future, as well as their future legacy goals. Together, these components complete the picture of a retirement balance sheet. Please take stock of your client’s information and place it into a retirement balance sheet so you will have a better understanding of which assets need to be matched to which liabilities.

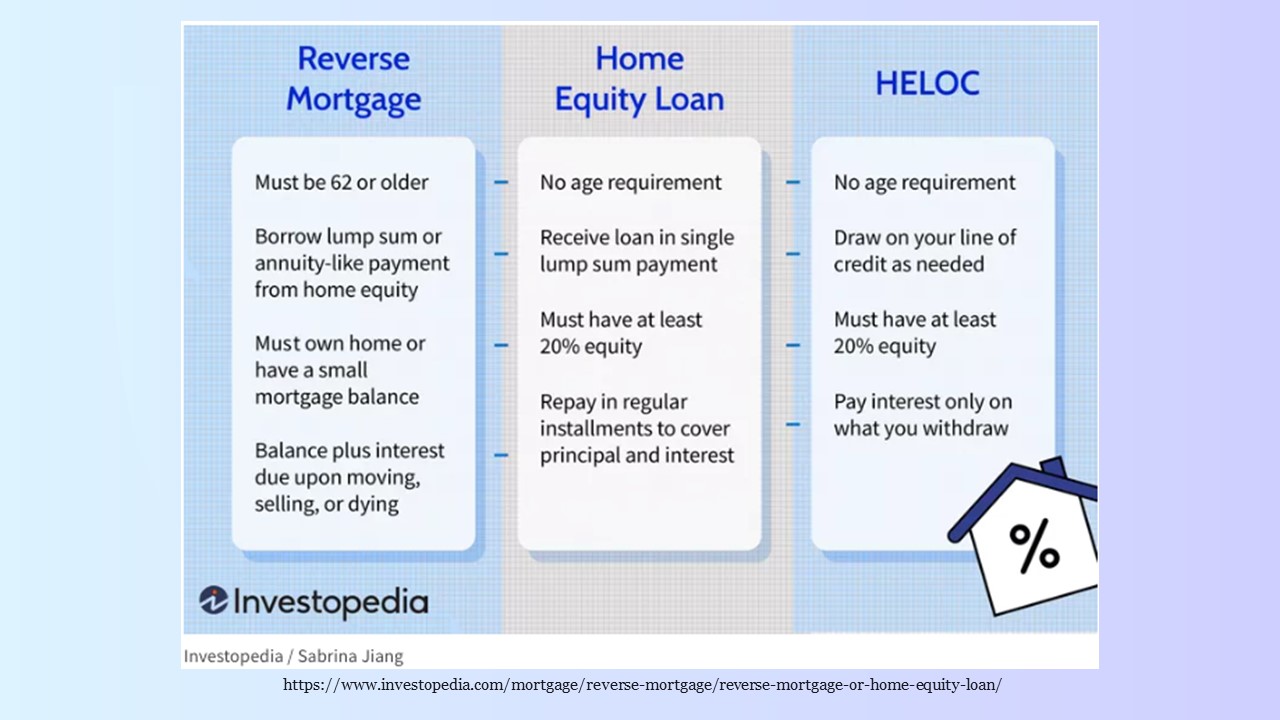

Home Equity, Reverse Mortgages, and the Retirement Balance Sheet

There is a critical correlation between scaling factors (to be defined), financial assets, and home equity in retirement planning. The use of a reverse mortgage can potentially bolster retirement spending and success. In this section, we’ll explore how home equity assets could potentially help with retirement income planning. Home equity is your home’s market value minus any outstanding loan balance. Many retirees or pre-retirees have their homes paid for, so their home equity becomes an asset that is just sitting there and not generating any income supplementation. I do not necessarily directly advocate that people consider home equity conversion mortgages or HECMs. However, I encourage clients to evaluate if it is necessary to tap into their home equity. For example, home equity could be a line of credit used for contingencies, especially for those who did not necessarily get a chance to invest in long-term care insurance. If your client’s home is paid for, it is also worthwhile to consider a Home Equity Conversion Mortgage (HECM) Line of Credit as a potential source for long-term care. Below is a high-level summary of the requirements for obtaining an HECM line of credit.

How much you’ll be able to access home equity depends upon the interest rate. The current interest rate is relatively high, meaning that the HECM portion will be much smaller compared to a lower interest rate environment.

It is important to remember that default with a reverse mortgage is not the same as with a typical mortgage. The default in a HECM or reverse mortgage is typically past due on homeowner association or property taxes. If your clients want to consider a HECM, just make sure that they pay for their homeowner association and property taxes and keep the home maintained.

The key point to remember is that with the reverse mortgage, nothing is repaid until you die. If anything is left, it will go to your heirs.

Many advisors think reverse mortgages are unique to the U.S., which is incorrect. Reverse mortgages are available worldwide in selected countries. Why do I want you to know about that as a planner? Your clients might own real estate outside of the U.S. If they do, they can take a reverse mortgage on the home they own outside the U.S. The United Kingdom, Canada, and France are a few other countries that I listed in my published research in 2022.

The reverse mortgage was established in the 1980s in the U.S., but the HECM began in 1961 in the private sector and became federally backed in the early 1980s. Canada started its reverse mortgage in 1961, and the U.K. started it in 1965. I absolutely love France’s approach. Why? One option in France is that you can sell the reverse mortgage to desirable investors and live in that home as long as you survive.

Of course, there is government oversight regarding reverse mortgages. The Department of

Housing and Urban Development (HUD) is the oversight authority in the U.S. In Canada, it is the Franchise Consumer Agency of Canada. The U.K. is an investors’ compensation scheme. France is under the Ministry of Economic Finance and Recovery. Unlike the U.S., you can use a selected list of approved vendors or lenders. Canada has two banks you can use. In the U.K., like the U.S., you can use any approved lenders. In France, it is just willing investors. When doing this research, I had to find someone who read French to verify the information accordingly.

The reverse mortgage market in Asia is more significant than you’d imagine. Most Asian countries have higher homeownership percentages than the U.S. Here is a list of countries with reverse mortgages: Australia, Singapore, China, Taiwan, New Zealand, South Korea, China, Hong Kong, and India.

You will only know if a client owns homes in other countries if you ask. A client may be thinking about buying a villa in Italy or somewhere else for retirement. You can also help them with this option if they need additional retirement income.

The Critical Correlation Between Scaling Factors, Financial Assets, and Home Equity in Retirement Planning.

How do you know who the best candidates are for a reverse mortgage? I have conducted research to determine benchmarks to better identify the most qualified candidates. In my 2019 research, I wanted to understand how well U.S. retirees were doing regarding retirement success. I used U.S. census data to calculate the assets retirees had left in the previous year, subtract what they needed this year, and estimate their potential balance at the end of the year. There are so many assumptions to make, just as you must make assumptions in your commercial financial planning software. Every little change will make a big difference in the simulation. For example, how do you know how long your client will live? Are you going to be using age 120? (This is what I used in my research.) What assumed return should I use? I did not use an average return; instead, I used rolling returns from the historical record, starting from 1927 and continuing until 2018. We’ve had a significant increase in inflation in the last two years. Because every year is different, I used rolling inflation based on CPI coming through the government data. I also further estimated inflation based on healthcare, housing, etc. The calculation is far more in-depth than just one inflation number. Retirement success depends on how much a retiree spends. The U.S. Census Data does not necessarily ask each household how much they spend in retirement, so I used the Consumer Expenditures data set. I took a number based on each state’s average and broke it into different age groups. For example, you spend more when you retire between ages 50 and 60 than when you are 70 and 80. Over age 80, you are likely to spend more on healthcare. None of these assumptions are fixed. Everything is dynamic, and in the simulation, everything was based on a rolling schedule, rolling returns, rolling spending, and rolling inflation. To perform the simulation, I used four different major datasets.

The U.S. Census dataset has retiree household asset information, including their Social Security retirement benefits, which tie directly to the Social Security Administration. I also used the Social Security Administration live table, which means that the mortality rate is calculated up to age 120 because I do not know when they are going to die.

I calculated the rolling market return using the Morningstar historical record, including equities and bonds.

The important thing I created was the Scaling Factor, which you can see in the graph below. The Scaling Factor is based on how much retirement will cost on average in a particular state. Every state’s average spending is different. Retirees in my state and age group typically spend $1,000 a month. If I have a higher income and net worth and want to spend $3,000 monthly, my scaling factor is 300%, or 3x my state’s spending average. This is what the scaling factor is for. Either you spend 100% of the state average or more than that average in terms of the calculation.

The research aimed to determine at what point scaling factors will always achieve at least 90% retirement success, meaning that no one runs out of money from their financial portfolio assets. If the scaling factor is less than 100, the retiree generally needs more retirement assets to maintain their standard of living at the state average and will eventually need help making ends meet.

Let’s look at the following graph.

How Might a Home Equity Conversion Mortgage (HECM) Improve Retirement Success?

What if we introduce an HECM as a strategy for the same data set of U.S. households who qualify to use HECM? For example, in California, by introducing a HECM into the equation, couples become 10% more retirement successful. The single household success rate improves by roughly nine percent. This is huge when it is considered appropriate to use a HECM. In Texas, about six percent of couples will be more retirement successful; singles become about eight percent more successful by adding an HECM to support retirement spending. Pennsylvania improves about five percent in the couple population and eight percent in the single households. Florida moved from 63% to 72% for married households and 4 percent more for single households using an HECM. New York improved a whopping 10% in the married population, and singles improved by roughly 7 percent as well. In sum, the research found that using a HECM for eligible families can make a huge difference in experiencing a successful retirement. In my 2022 published research, I used the same dataset to determine how to spot clients who can be helped most by introducing home equity or an HECM into the conversation. On the left side of the graph below, which models couple households, you will see a percentage that takes the liquid assets divided by net worth for real household data in the U.S. population.

Identifying Clients Who Can Increase Retirement Success by Utilizing a HECM

So, how do we identify clients who can benefit from this strategy? I had a client who lived in California, so let us look at the California benchmark. Lifestyle spending in California is typically 300% on average, which means liquid assets divided by net worth should be more than 54%, and home equity divided by net worth should be less than 26%. This client’s net worth was $6,000,000. Sounds great, right? However, their lifestyle is 300% of California’s average retiree’s spending. Still, they only have 28% of their net worth in liquid assets, far lower than the liquidity benchmark to support their spending. Their home equity is at 71%, higher than California’s average home equity benchmark. This is a classic house-rich, cash-poor family, a prime candidate for a HECM. If they do not want an HECM, you can discuss potentially downsizing or moving to a place with a lower cost of living. Luckily for this client, we devised a plan for them to migrate to Mexico or Hawaii to meet their lifestyle outside of California. Another client lived in North Carolina. The North Carolina benchmark says that most people will spend about 125% of the state’s average. Their liquid assets divided by net worth should be around 34%, and their home equity should be around 53%. This client’s net worth is more than $2,000,000. Their lifestyle spending is at 125%. Their liquid assets are 82%, or way above the benchmark, and their home equity is only 18%, or way below the benchmark, so they are not a good prospect for a HECM. There is no need to discuss incorporating home equity into their retirement income plan. For clients who are house-rich and cash-poor, we recommend that they relocate, downsize, or adjust their lifestyle. All of these could potentially help their retirement success at some point, even if they do not want to consider home equity or HECM. Consider using a retirement balance sheet to lead your retirement discussions with your clients. A house-rich, cash-poor might be a good candidate for HECM, but you may want to skip HECM for those not in the house-rich and cash-poor category. In sum:- Advisors can use retirement balance sheets to lead discussions about using home equity to improve retirement success.

- Reverse mortgages are available worldwide.

- Consider using benchmarks to spot if home equity is a viable option to introduce.