By Carol Bogosian, ASA, EA, MAAA, President of CAB Consulting

The common theme in this research compared to other research that is conducted in the industry is that it was formed with this end in mind: what do consumers and advisors need to be able to act on for what we find in these research projects? We’ve used an applied research approach versus an academic approach, and we focused on those parts of what we felt the industry needed to know in order to better serve the mid-market, whether they were consumers or participants in employer-sponsored plans.

Our goal in this research is to expand the understanding of how to prepare for the post retirement years by shifting the conversation from management of assets for retirement income, to how to help those in danger of running out of money manage their longevity, health and other post-retirement risks.

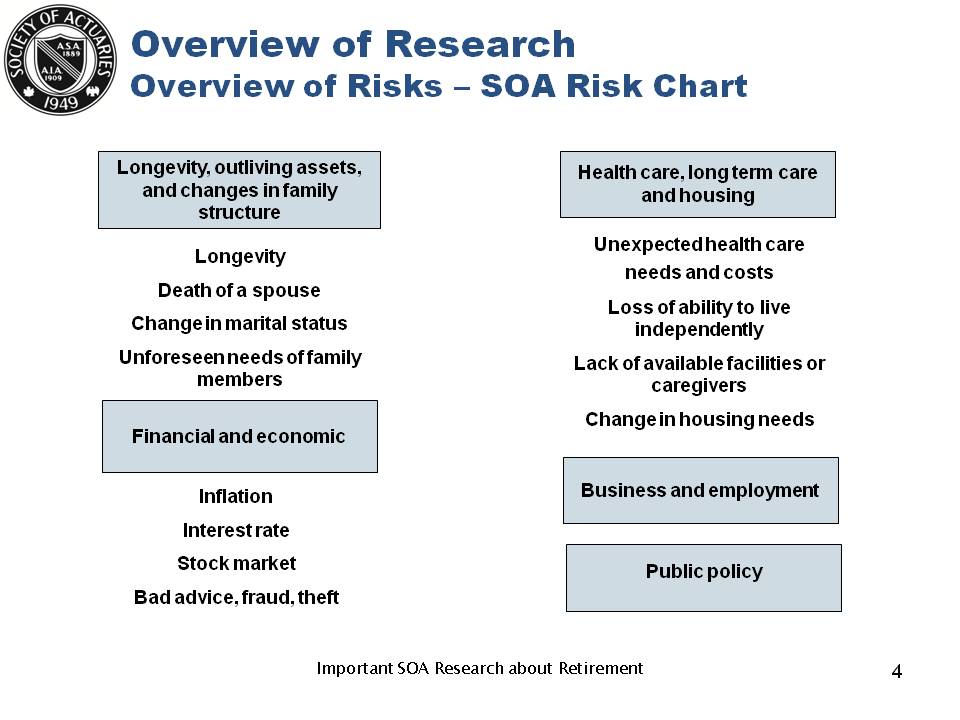

When we first started this committee, we looked up and said, “Gee, we’re actuaries, we understand risks. That’s what we really are trained to do – is look at risks and opportunities in risks and find ways to mitigate it.” So the first thing this committee started off with was to define what risks are. Below is the chart that addresses it. There are about 16 risks that people face in retirement. If you think facing these risks pre-retirement is bad enough, think about facing them when your income is more limited, more constrained and you have less options to mitigate some of these risks.

So when you look at this chart, things like longevity, the death of a spouse, unexpected healthcare costs, inflation . . . all of these are risks that are faced both pre-, but especially in retirement. These risks do change over time. On occasion there are new ones added. You never see them depleted. But these are the key risks that we defined as what we consider the post-retirement risks that we need to find a way to help people through.

As a committee, we came together over 15 years ago. As Betty said, she and I have been on the committee just about as long as it’s been in existence. Our foundation was managing these post-retirement risks. Our focus is on those who are aged 50 and over. And you may say, gee, 50’s awfully young to retire, and boy do I agree with you! However, we do realize that if we waited until 60 or 65, somewhere in the range that people are retiring today, that’s too late. As you know, planning has to start at least a decade to two decades before a key event in someone’s life.

Consumer Focus Groups on Retirement Decisions

In 2013, we held consumer focus groups on how they made their decision to retire. I was very surprised, to tell you the truth at their responses, and at times I couldn’t even sit in my chair. I’m very much for women to be involved in their retirement and their financial issues, and I’m also very aware that some aren’t. I was a little surprised by some of the things I saw come out of this, both from the men and the women.

One, the decision to retire was based more on career and life events rather than well though-out reviews or process. Something happened at work in their career, in their lives, and they decided to retire. There was not a great deal of forethought, such as “I have saved enough or I have enough pension income that I know I’m ready to support myself for the rest of my life.”

Second, the analysis of the retirement financial adequacy is little to none. That wasn’t what drove their decision to retire.

We interviewed men and women separately. We didn’t go into it expecting what we found, but we did find significant differences in their concerns, their expectations and their attitudes. Women address the issues differently than men. They are more into caregiving as a primary consideration of why they retired and of concern about how they may need to spend their money in retirement. Overall, they’re more generally concerned about their financial adequacy. Men tend to feel that they can handle it, but they rely more on others for financial advice for the women. And they don’t necessarily know for sure the qualifications of that financial advisor.

Financial Planner Focus Groups at the FPA May 2012 Retirement

In 2012, we worked with Financial Planning Association on their retreat and we did a set of focus groups with the financial planners that were there. The participants we looked at were the FPA members that actually serve the middle market. One of the things that we really noticed from the focus groups was that middle market is not necessarily being served.

One of the goals was to determine how these FPA members reach out to the market and why the middle market may not be using their services as often as we wish. Some of the key issues that came out of this was that serving the mid-market requires:

- Managing spending. I don’t think that surprises me. Their assets are a lot less available than the high net worth.

- Reducing debt. This is one of my key concerns about people moving into retirement today. I’ve been in the industry over 30 years and all of those studies, the retirement inadequate studies, do not take into mind that debt may be in existence. If you look at debt right, it’s a net against whatever assets they have to determine whether they’re adequately ready for retirement. Reducing debt before retirement is a key issue in the mid-market.

- Lack of investable assets. A lot of the mid-market has assets, but it’s not in a cash position or an investable position. We’ll talk a little bit about that on later.

- Making working with the middle market profitable. I know we’re all professionals and we need to make our livings, but finding a way to make the mid-market profitable was a key issue there, too.

Some of the practice management solutions for working with the mid-market included:

- Build efficiencies into the process, driving towards that profitability issue;

- Improve technology, which will help both servicing them, as well as profiting from them be more efficient;

- And then focusing on cash management as a specific issue that they face.

Bi-Annual Retirement Risk Research Survey Results by Issue

Every two years since 2001, we’ve looked at retirement risks. There’s a persistent gap in the knowledge and the understanding of retirement needs, and I’m talking financially here. Top risk concerns after 15 years of doing this bi-annual survey are inflation, health and long term care. Those three are really key drivers of the ability for the middle market to be able to afford their long-term retirement.

There has been a lot of stability in our six surveys over that 15 year period. There is also an overall consistency with other work that is out there. So this speaks, in fact, that we are getting to the right people; that we are asking the right questions. What it doesn’t speak to the fact is that we may not be getting the right answers. Their answers are worrisome.

We do find that in general through all these years, pre-retirees are more concerned about retirement risks than the retirees in all of the years. Although in 2011, the retirees seemed to step forward on their level of concern.

Since the survey started in 2001, we’ve had two major periods of stock market decline. We had a lot of instability and volatility during this time. Last but not least, the interest shown in buying financial products, risk management products, is low.

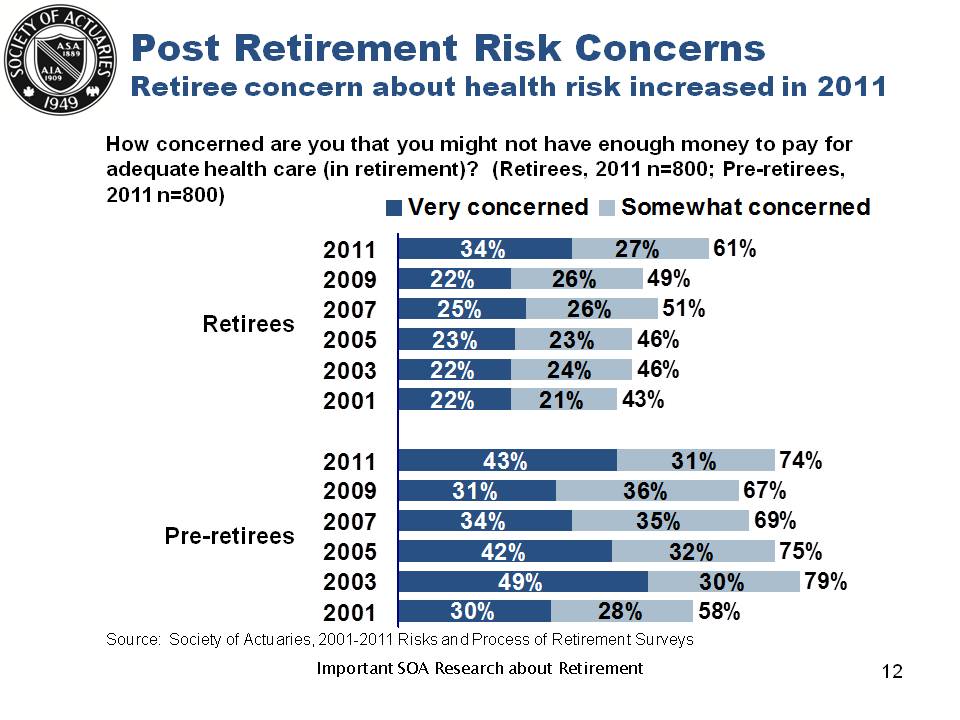

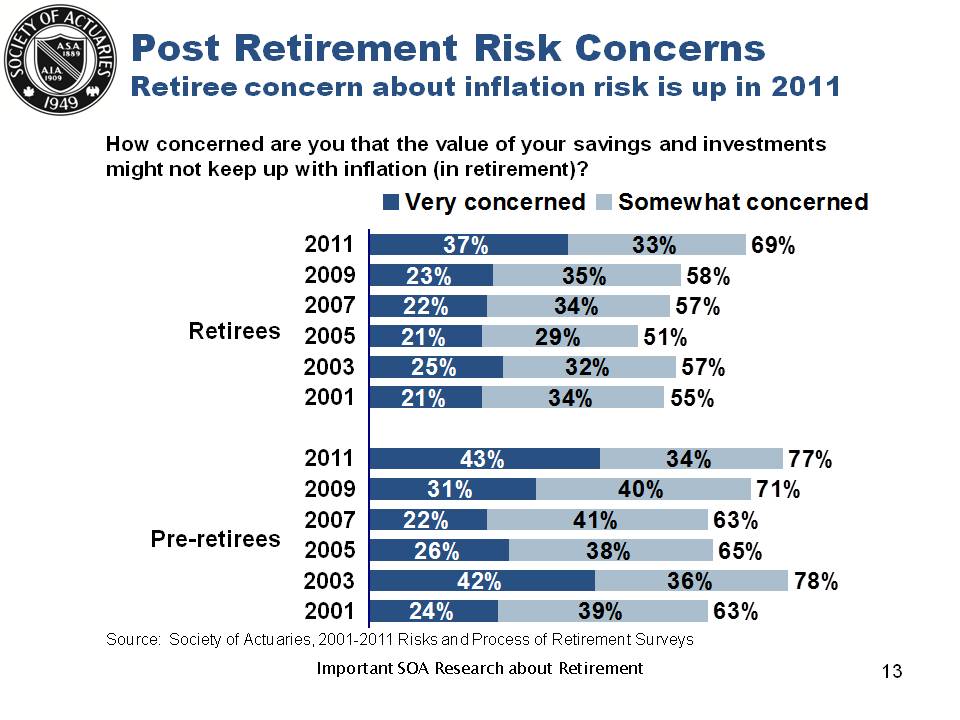

2011 Post Retirement Risk Study Results

Let’s look at a few charts that actually come out of the bi-annual SOA risk surveys. This one is addressing health risks concern increased in 2011 for both groups, but primarily look at the retirees. In the retiree pool, 61 percent in 2011 are concerned that they’ll have enough money to pay for their adequate healthcare in retirement. It was 49 percent in the survey two years prior.

The second issue is inflation. In 2011, the retirees concern increased significantly. This is understandable because if they’re really in retirement position and they’re using a lot of fixed income to protect their assets, obviously their income levels came down. So as inflation goes up and interest rates change, they become very concerned about what’s going to happen to their buying power and assets. The pre-retirees, again, were more concerned in the very concerned category than they were in overall.

What We Find About How and When We Retire

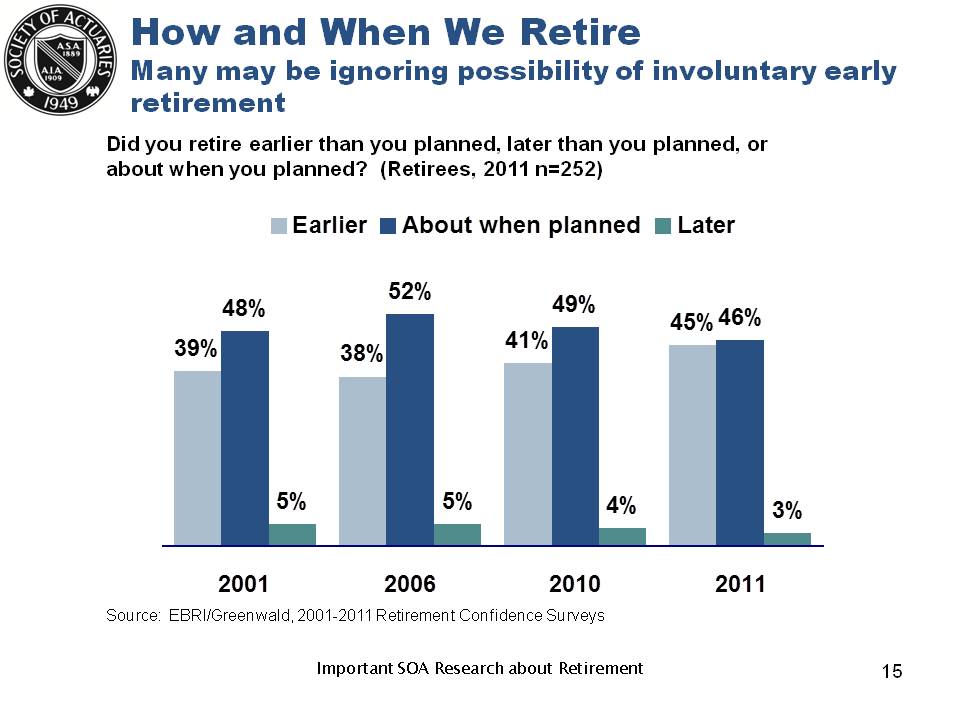

One of the other things we looked at in the 2011 Retirement Risk Survey is how and when we retire. How do people make the decision to retire? Retirement ages have gradually been increasing. We still aren’t seeing the majority of people retire at full retirement age. It’s still in the low age 60’s, but they are gradually increasing.

There is an evolving thinking about this third age, the retirement age, and this period of easing into retirement. This is how retirement is being redefined: How do we define it while I’m in it, how do we define it while I’m going towards retirement? There still is a gap, though, between the retirees’ action and what the pre-retirees expect. Many people still retire involuntarily, and one of the surprising things out of the focus group that we had was that people thought they retired, they referred to themselves as having involuntarily retired, when in actuality when you ask them for the reasons and delved in deeper, it really was not an involuntary retirement, where they were moving towards something they wanted to do differently.

Disability is a real driver for why a lot of people retire. It’s a key issue to think about with your clients. It is a key risk to protect people from going into retirement. Disability cuts off not just your earnings; it cuts off your savings and it starts using your assets earlier. It does not necessarily give you Social Security benefits and Social Security Medicare, so it is a real issue for people to think about is how to protect themselves in disability.

Let’s look at a few things from the actual survey. We asked people, “Did you retire earlier than you planned or later?” Here’s one of our first key misperceptions and gaps comes in. Forty-five percent of the retirees said they actually retired earlier than they planned. Working two to three more years longer can make a significant effect on retirement security from the studies that I’ve seen.

So almost half – 45 percent of the population – say they retired earlier meaning that they had to shorter their savings horizon and lengthen their spending horizon off of their retirement savings.

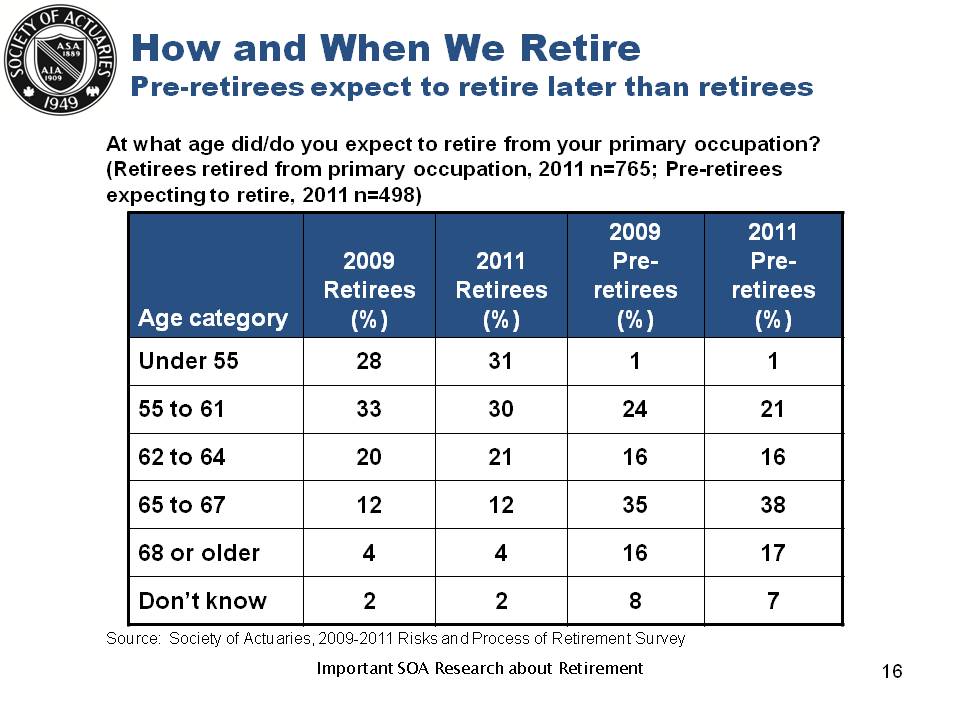

Secondly, pre-retirees expect to retire later. Looking at this chart, if you add up the numbers in the 2011 study, 38 percent of the pre-retirees actually expect to retire prior to 65. Only 38 percent! What happened?

Look at the retirees now. Eighty-two percent of the retirees actually retired prior to 65. We have a real gap in expectation versus what actually happened. So what does this mean? Large gap in expectation versus reality between retirees and pre-retirees. Obviously, that’s going to affect the planning horizon, or should.

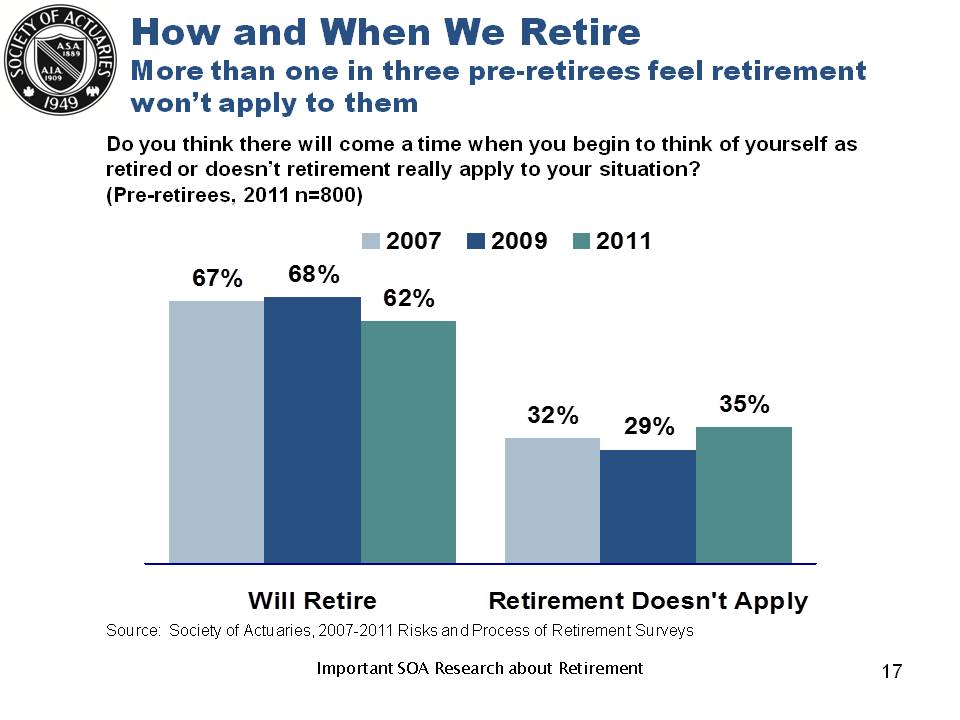

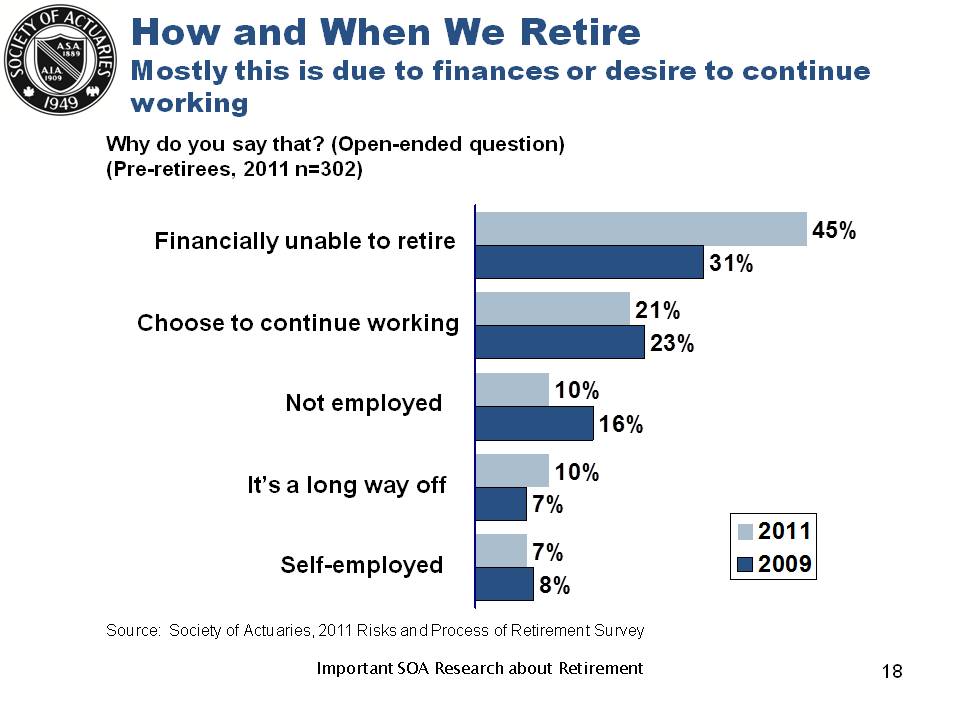

In the next slide, we look at that one in three pre-retirees feel retirement won’t even apply to them.

And 45 percent feel that they are financially unable to retire.

That increased substantially from 31 percent in 2009 to 45 percent in 2011. Clearly what happened in 2008 to 2010, the recovery wasn’t well in their minds by the time we did this. That’s clearly affected how people feel that they can retire.

Working in Retirement

I worked so many years in my career promising people that they’ll get to retirement, taking every chance I could to help plan sponsors and participants understand that. And to suddenly hear the phrase “work in retirement,” I said the nomenclature’s wrong! Retirement’s supposed to be not working! However, that’s not the way we see retirement going forward. This is part of the new definition of retirement.

Working in retirement, whether it’s part-time or in some other capacity, is going to have to factor into people’s minds, whether that’s working longer or working during. About 50 percent of the retirees actually work in retirement or have what we call bridge jobs that get them from their full time career to their secondary career. Often these are different roles and on different schedules. They may even be moving around the country and working at different locations for the same organization. They may be working into a part-time or a contract position, but clearly about 50 percent of retirees do work in retirement.

However, the second part of this is virtually no phased retirement, formal phased retirement programs, are really out there in the private sector. There are ad hoc programs, there are agreements made with individuals, but there really is no formal phased retirement in our U.S. structure.

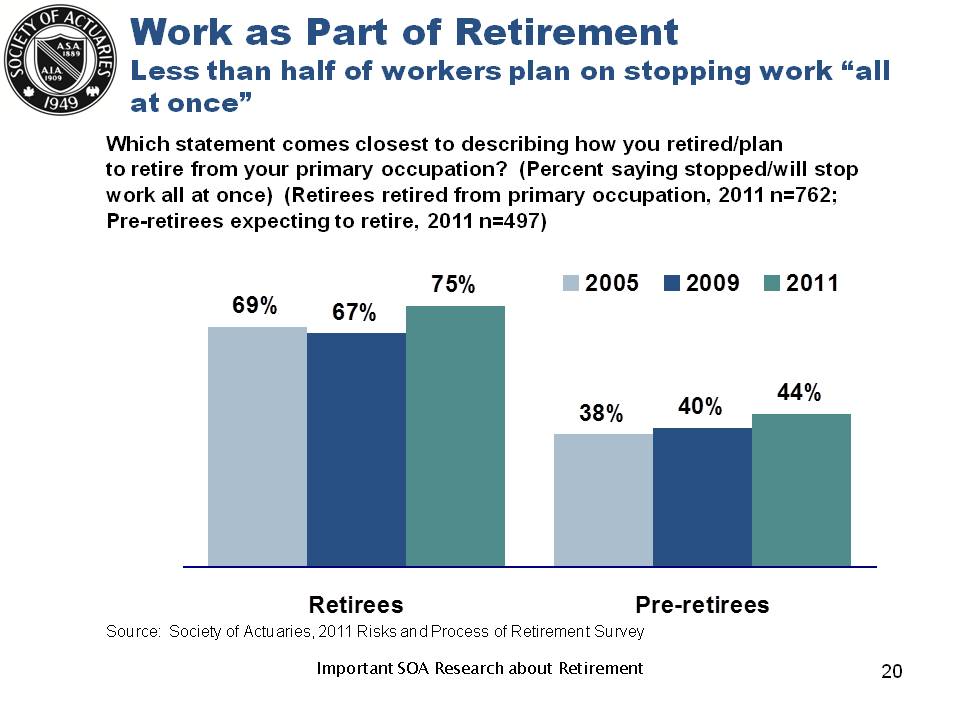

Less than half of the workers plan on stopping work all at once, meaning they walk away from whatever career they’re in or job they’re in. But look at this perception gap between retirees and pre-retirees. Seventy-five percent of retirees actually stop working all at once, but only 44 percent of pre-retirees actually expect to do so.

What does this mean? It shortens your planning horizon to build the assets and it lengthens the period in retirement that you’re going to need to spend the assets.

We also find that one-third of the retirees actually return to work once they retired. I do know from anecdotal experience sometimes that is boredom, sometimes that is necessity. If it’s boredom, great. If it’s necessity, we need to plan better.

Key Findings About How We Plan for Retirement

These are some of the key things that we have discovered when we ask questions and surveys and do focus groups around planning for retirement.

- Planning horizon is of great concern.

- There’s little focus on the risk management products.

- There are big gaps in understanding.

- The death of a spouse; what does it mean to the financials?

- The impact of working longer; how important is that?

- Social Security claiming.

Social Security claiming is a key driver of success of someone’s retirement. It is a household decision that’s key to understand. People approach it from, “I’m an individual and I need to retire so I want my Social Security.” If there’s a spouse involved, it is very important to understand how to make an informed decision and how important claiming is to the household.

Many people do not understand longevity. This goes to the heart of me being a pension actuary, having studied longevity for this many years. They don’t understand the variability of it. They don’t understand and tend to underestimate their longevity. Now another one of those obvious statements that must be said: People who live longest will have the problems. Our older ages will be the ones that experience the problems. You don’t run out of money the day after you retire. You run out of money 20 years after you retire and you have none to limited resources to help yourself and you’re facing maybe some of your biggest expenses in retirement. Running out of money is an older-age issue.

Housing is a significant portion of middle income assets. I mentioned earlier how we have non-investable assets; this is the largest one for the middle income. It’s excluded in most retirement planning. I know it’s not included in the retirement adequacy studies I have conducted. It is not included in a lot of the financial plans that I have looked at. It is a key driver for the middle market and to service the middle market you have to be open to addressing housing, not just where they live now, where they’re going to live in the future and how to work the housing equity into not just their estate planning issues, which most think of, but their lifetime living income issues.

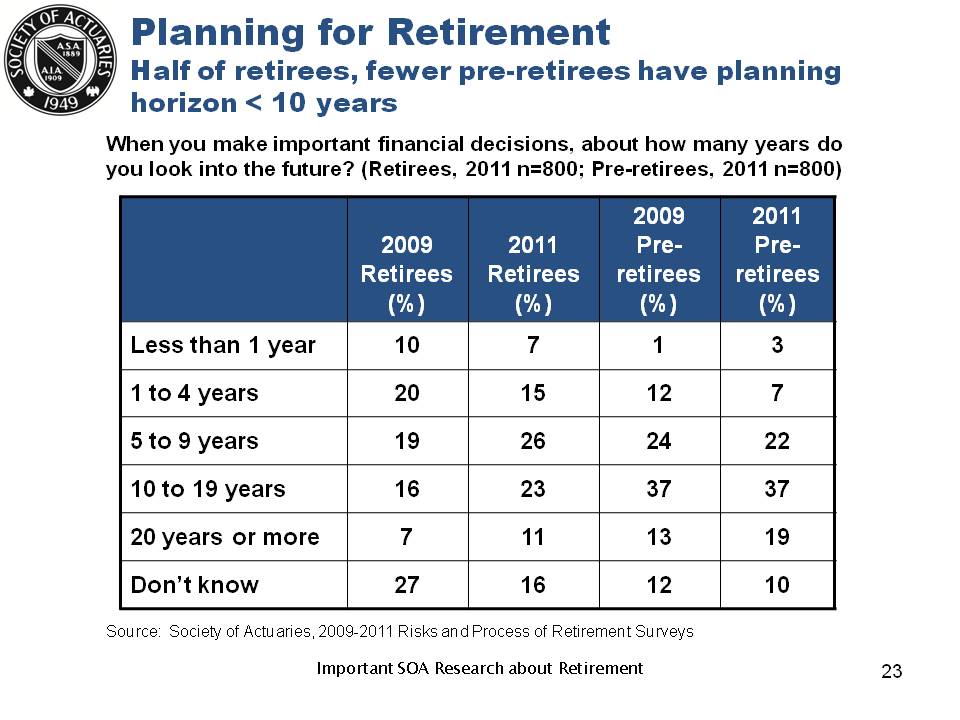

Retirement Planning Horizon

So let’s look at one slide and some of the detail from the survey. Half of retirees and fewer pre-retirees have a planning horizon of less than 10 years.

Look at this, 48 percent of your retirees and 32 percent of pre-retirees have planning horizons less than 10 years! How can you plan for what I mentioned earlier was a 20 year decision going in, 20 year decision in retirement, possibly longer if you’re lucky on both ends of those, and yet only plan for 10 years? However, I understand most people don’t plan their finances for even five years of their personal living while they’re working, but we need to get past that and start looking at longer term planning horizons.

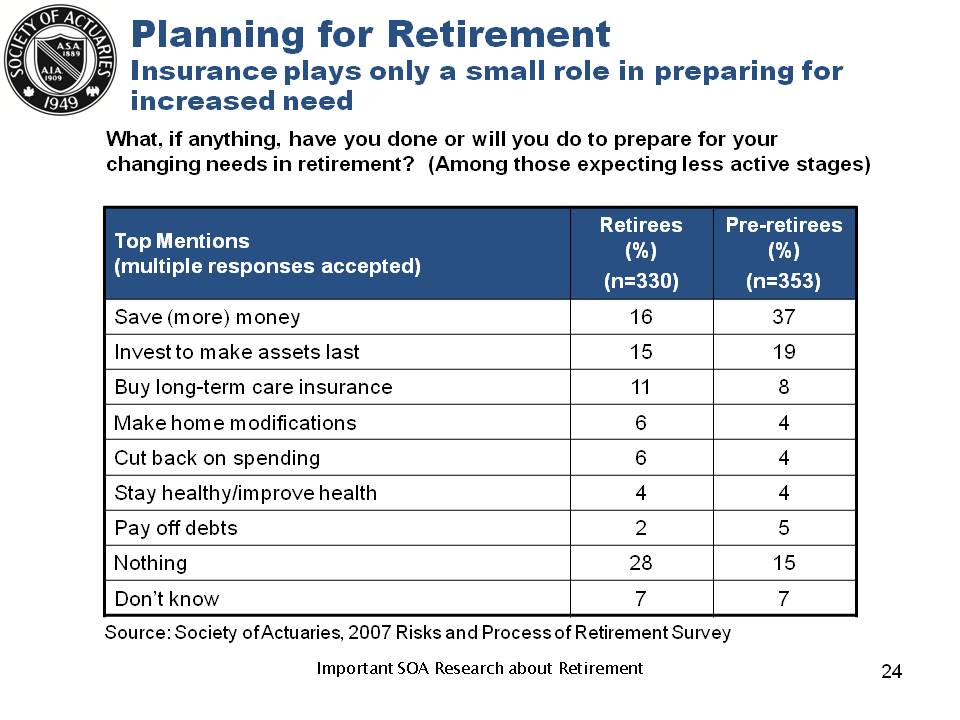

Insurance plays a small role in retirement planning. Thirty-seven percent of pre-retirees say if they prepare for changing needs in retirement, they’re going to save more.

I would love to see that happening. In reality, I don’t see it come out in any of the statistics around what people are saving in their retirement plans. However, the return is even more disconcerting if they run into problem: what are they going to do? Twenty-eight percent said nothing.

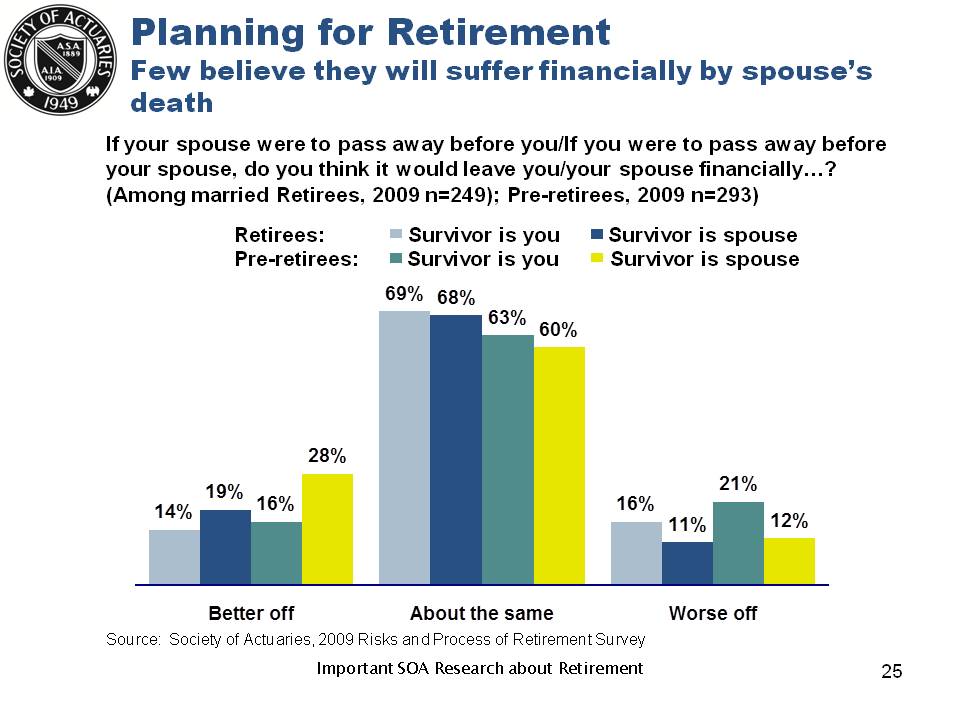

Few believe they’ll suffer financially by a spouse’s death. They’re either ignoring or they’re ignorant of the effect of the first to die spouse on their financial assets. First, income is reduced. Second, the need for health, such as living expenses, helping in paying bills, helping in transportation increased, that takes money to do. This is unbelievable that 60 percent of the people feel that nothing happens when a spouse dies, they’re going to be basically about the same. It just isn’t true. So when planning your clients’ Social Security and retirement benefits, how to spend down their assets, make sure you’re buying the right risk management products so you protect the second spouse that survives.

SOA Research Conclusions

There’s been a lot of stability in our studies on the misperceptions that’s not all good, and so we need to be working on getting people to understand risk management in retirement. People are not utilizing longer term risk management products the way they could. Another point is few workers are prepared for the risk of a sudden and unplanned early retirement, disability being the key driver for that. Disability and long term care needs for family is the second biggest driver.

There’s a low take up for guaranteed income. The widowed and the very old will continue to be our vulnerable population. Not when they first retire, but at the older ages.

A few more insights that we had here is working longer is very important for many people. Two or three years makes a big difference. We’re not saying work until you die, we’re actually in the industry asking people to work until their full retirement age, which is right now around 66 for Social Security, and older. Work until you get those full level of benefits, maximize your Social Security as late as you can, and work while you’re in retirement if you’re capable. It will help you both mentally; it will help you financially.

Education is important, but it can’t be your primary strategy. There are limits what it could accomplish based on people’s financial and math skills.

When you’re looking at financial planning, retirement income adequacy, taxation is also something that is too easily set aside. All of this money that we can save in the DC plans, the majority of it, is sitting there in taxable position, tax deferred. The government’s going to get its money, and people need to be planning for that. I oftentimes will say to someone when I first meet them, “If you have a 401(k), take one-fourth of it away and see if you can retire because you need to pay your taxes first.” I know that’s a broad brush, but it gives them an idea of what that effect is going to be.

The middle market clients need more attention. We’ve noticed they don’t get it. They need it from the financial planning and the retirement professionals. These are your takeaways as professionals. The planning needs to expand to recognize not only longer life, but additional years spent in retirement. Saving more, investing wisely, working longer, appropriately claiming retirement benefits and using the income annuities need to be part of the planning process. They’re all the risk management tools that are available to help them mitigate it. Housing needs and equity, as they change over time, are significant for middle market, must also be part of the planning process.