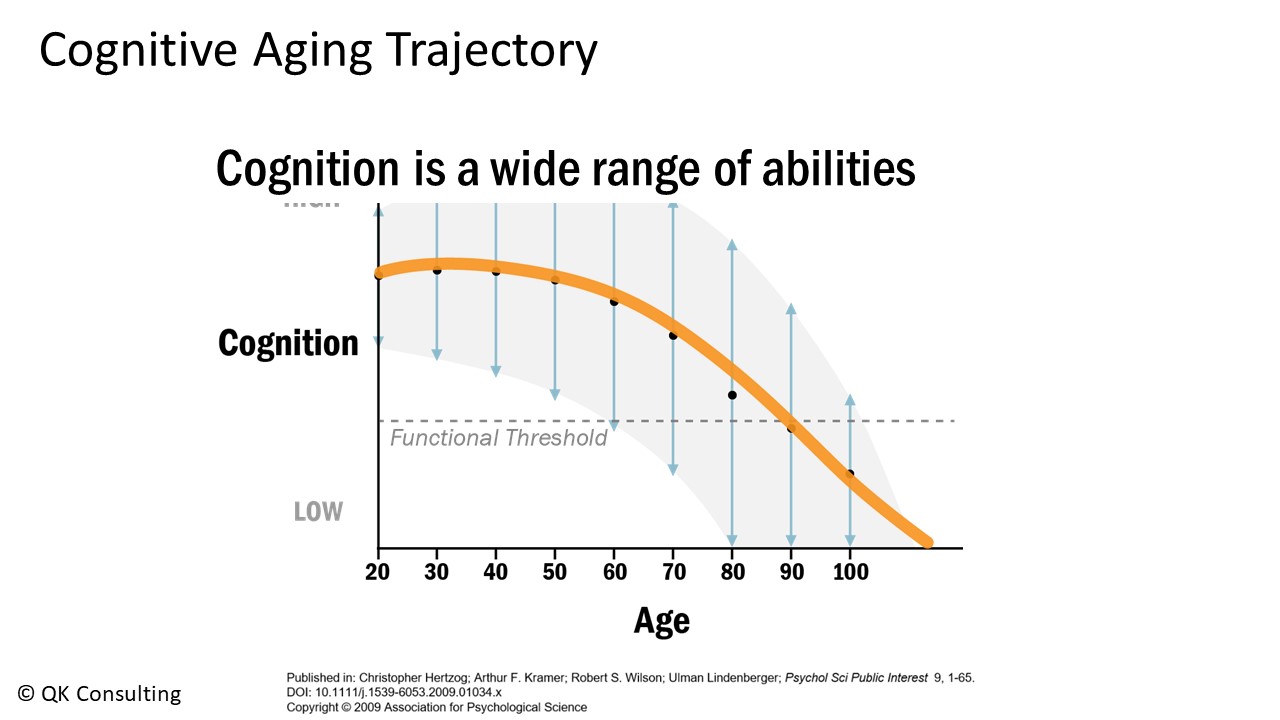

What you see here is a graph that you can find in any scientific journal article looking at how some of these cognitive abilities change over the adult lifespan. The orange line represents the typical trajectory. Starting in our 40s and 50s, we may notice subtle changes in how fast our brain works and how well we retain short-term information. These changes become more pronounced with each passing decade. This dashed line near the bottom is what you think it is; it is the point at which there has been so much decline that this person cannot function independently anymore.

The gray area with the up and down blue arrows represents the enormous variability from person to person, both in how adept we are, to begin with, on any of these abilities and how long we maintain that good cognitive function.

What are the financial implications of cognitive impairment? I will start with a term that I call “financial autonomy.” In our society, autonomy, the ability to act on your values and interests and control your affairs, has been a key component of psychological well-being—financial autonomy is having control over your financial decisions and behaviors. For example, deciding to sell your home would be considered a financial decision, and completing the paperwork on that sale would be a financial behavior.

Imagine how you would feel if you needed formal authorization or approval from a relative or fiduciary to sell your home or to access a certain portion of your savings. All of us would be pretty unhappy about losing some of our financial autonomy. As we will see, cognitive function impacts our financial autonomy in our later years. As we see in the graph above, as we get older, we are more likely to experience cognitive decline and impairment.

A recent report from the Alzheimer’s Association indicates that about 25% of adults aged 65 or older have been diagnosed with either mild cognitive impairment, which is often a precursor to Alzheimer’s or other dementias, or they have been diagnosed with Alzheimer’s. About 12-18% of adults have been diagnosed with MCI, mild cognitive impairment, and about 11% with Alzheimer’s disease.

As you probably know from your professional experience, the rate of undiagnosed dementia is very high. It is estimated that 63% of community-dwelling older adults who have dementia are undiagnosed, meaning that they are still living at home rather than in an assisted living or nursing home. What these statistics mean is that if your business has 100 clients aged 65 or older, about 25-30 of them may have some level of diagnosed or undiagnosed cognitive impairment.

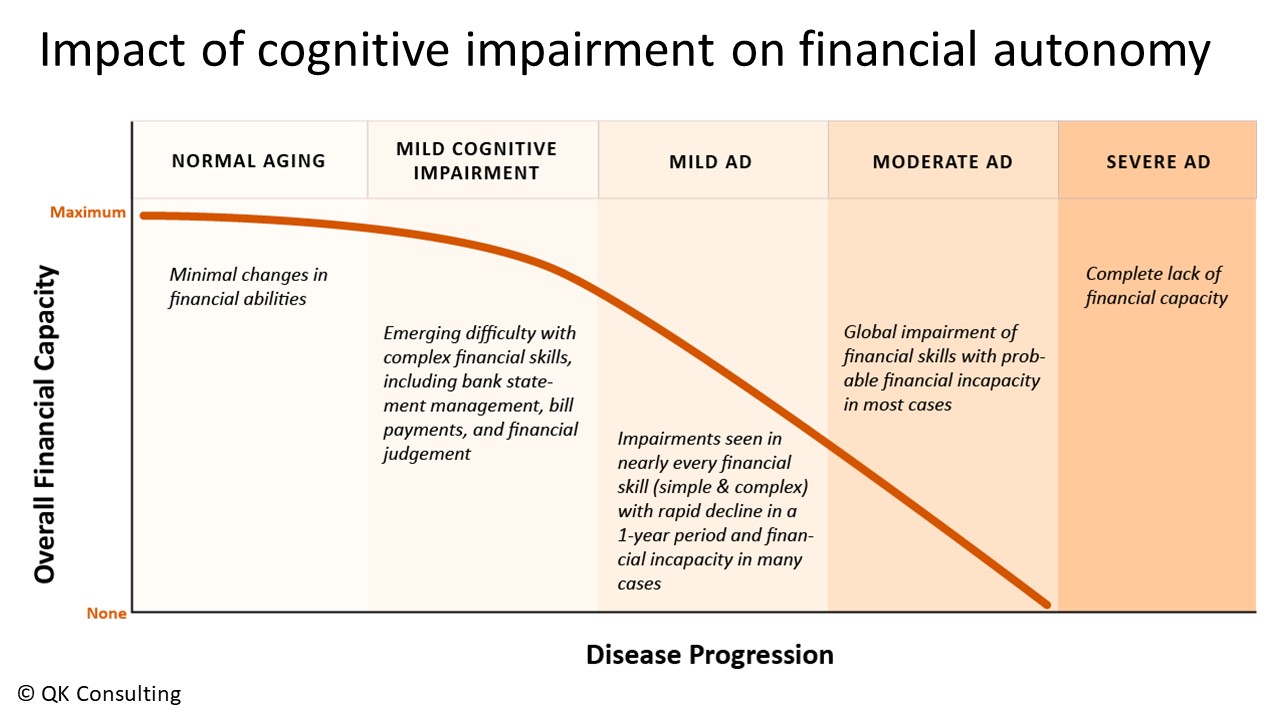

This graph illustrates how decrements in cognitive function manifest themselves in terms of financial autonomy.

We generally maintain full financial autonomy when we have our typical age-related changes. If somebody is diagnosed with mild cognitive impairment, at this point, they may get into trouble for not paying bills on time or overdrawing from their bank accounts. Here, they would maintain most of their financial autonomy, but even at this early stage, they can be susceptible to financial exploitation.

Moving into the mild stage of Alzheimer’s disease, here they may need assistance with everyday finances in terms of paying bills and so forth, but they may still be able to make financial decisions that are consistent with either their previous decisions or with statements that they made when they were cognitively healthy. At this level, they can maintain some financial autonomy.

Between the mild stage and the moderate stage of Alzheimer\’s disease, there can be much variability in the remaining level of financial autonomy and in which areas. Then, starting with the moderate stage of Alzheimer\’s disease, at this point, they maintain little to no financial autonomy. They really cannot handle financial decisions or behaviors. As you can imagine, determining a client’s current financial autonomy level can be challenging. Having a trained geropsychologist conduct a financial capacity assessment is a good idea.

Let us put some of this information into more of a real-world context. First, cognitive decline in and of itself is associated with wealth loss. One longitudinal study found that a 10-15% decline in cognitive function is associated with a 15-18% wealth loss, and older adults with cognitive impairment are more than twice as likely to experience wealth loss as those cognitively healthy. This wealth loss comes about presumably due to decreased decision-making abilities.

Financial Elder Abuse: Red Flags in Our Client’s History

We all know that older adults are popular targets of financial exploitation, but perhaps not the prevalence. A recent Consumer Finance Protection Bureau report found that older adults filed 80% of suspicious activity reports with a mean loss of $34,000, which many older adults cannot afford to lose. Very sadly, this exploitation was often done by someone known to the victim, and in 19% of the cases, the perpetrator was a fiduciary. Older adults with cognitive impairment are three times more likely to experience financial exploitation than cognitively healthy older adults.

Again, we know that older adults can be susceptible to undue influence, but did you know that in 40% of undue influence cases, the victim has dementia? Going back to your 25-30% of cognitively impaired clients, these clients are at a very high risk for wealth loss due to poor financial decision-making, as well as financial exploitation and undue influence. The silver lining with these statistics is that they can be mitigated if your client has a solid social support system with at least one person vested in your client\’s best interest.

How can you help your clients from financial elder abuse and financial exploitation? One way is to be familiar with the red flags in your client’s history that can increase their risk. The first is social isolation; unfortunately, many older adults in the United States live alone, and their family members, if there are any, either live far away or are inattentive. Socially isolated older adults are especially vulnerable to romance scams. Similarly, if you have a client who is going through a recent bereavement, this will also make them emotionally vulnerable to scams and financial exploitation.

Suppose your client is dependent on someone else for their care. In that case, this can put your client in a position where they feel they have no choice but to see to their carer’s demands because the carer obviously can withhold medication; they can become physically abusive or emotionally abusive. If an older adult suffers from any substance abuse or mental illness, this can also impair judgment and magnify that emotional vulnerability. Of course, cognitive impairment will exacerbate each of these risks.

Here are some red flags to pay attention to while interacting with your client. I suspect that you are all already quite familiar with these. The main thing here is a noticeable change from their past behavior. One thing to keep in mind is that often, financial exploitation is also accompanied by physical and/or emotional abuse. Financial exploitation is what we observe, but there is also often physical or emotional abuse happening kind of in a hidden way at home. The “See something, say something” adage is really, really important here.

I also want to bring up a couple of subtle red flags regarding family members. First, about 50% of family caregivers handle their parent’s or other relative’s finances without legal authority, which can lead to problems. If you believe the family member has your client’s best interest at heart, then you should recommend that your client give them legal authority to that family member. If you do not trust the family member, then you should act as though they are a possible perpetrator of financial abuse.

This leads to the second point. A very insidious type of financial elder abuse is committed by family members who are unaware that they are exploiting their parents or relatives. This could be the adult son taking care of Mom and giving himself a caregiving stipend with Mom’s money or buying himself a fancy new car to “take her to her doctor appointments.”

He does all of this without talking to Mom about these financial arrangements. He is doing this all without getting his Mom’s permission. This person feels entitled to their Mom’s money and does not need their Mom’s approval. This is a really tricky one to detect. When you meet with your client, try to determine if this is occurring; you should talk with the family member.

Resources to Help When Clients Show Signs of Cognitive Impairment

The Alzheimer\’s Association is the go-to spot for familiarizing yourself with exactly what Alzheimer\’s is, what dementia is, and so forth. They have all these great sections regarding what exactly Alzheimer\’s disease is, what dementia is, and the difference between them. What I appreciate the most is this resource, “Know the 10 Signs.”

For each of the ten early signs of dementia, they describe what a typical age-related change is and when it is a cause for concern. There is also this wonderful handout from the Alzheimer\’s Association with some general guidelines for having that difficult conversation with your client, how to broach it, and so forth.

Now, you had that conversation with your client; it went well. Next, you can recommend that they go to an Alzheimer\’s disease research center for a comprehensive memory evaluation. These Alzheimer\’s disease research centers are in many states across the country. Most of them are affiliated with a university or a medical school. You could find the one closest to your client and recommend that they make an appointment there, or you could make that appointment for them.

I live in California, and I know that the Alzheimer\’s disease research centers in California provide that memory evaluation for free. That is our state taxes at work. I am not so sure about other states, but I encourage you to have your client go to an Alzheimer\’s disease research center rather than going to their GP because these people are trained. This is exactly what they do all day long.

Moving on with your client, let us say they went, they got this comprehensive memory evaluation, and they have been diagnosed with mild Alzheimer’s disease. What can you do next? Go to a site such as this one, the Older Adult Nest Egg, and you go under the \”For Professionals\” tab. You will see that they have things about “Financial Vulnerability assessment” and so forth.

I recommend hiring a trained geropsychologist for this financial capacity assessment. This is one where, again, as you all know, in terms of being a financial planner, it is so much better to have someone who is an expert in that particular field assess someone who has not been trained for many years. You can get a trained geropsychologist to do this assessment and they will be able to tell you and your client in which areas that person can maintain financial autonomy and in which areas they need a little support.

Now, you have the National Institute on Aging as a happy, general, wonderful resource. If you go to the \”Health Information\” section, you can see they also have information about Alzheimer\’s disease and brain health, and here, they have these short articles written for everyday people on these various topics. Another really great part of this website is this part over here called Get Print Publications.

The National Institute on Aging has created over 70 different fact sheets, pamphlets, and booklets on different aspects of aging. Some of them have been translated into Spanish, and you can download or request hard copies of any of these publications, and even the shipping is free. I encourage you to browse through these publications. I would be surprised if you did not find at least one relevant or helpful to your clients. This is, again, a wonderful, general resource on different aspects of aging.

Now, continuing with your client, who has now been diagnosed with mild Alzheimer’s disease, let us say the family does not know what to do. Again, I would return to the Alzheimer’s Association’s “Help and Support” section. Scroll down to see a section called \”Programs and Support.\” First, they have a 24/7 helpline, and if you look at the upper right-hand corner of the website, that phone number is always listed there. It is also listed on one of your handouts. You can see they have local resources; they have support groups for caregivers, they have support groups for people living with dementia, and they have education programs. You can ask your local Alzheimer\’s Association chapter to come to your office and give a talk about Alzheimer\’s disease and what people can do to reduce the risk for your staff and your clients. Again, this is an incredible resource for any question or issue with Alzheimer\’s disease and dementia.

Let us say that your client’s family is struggling with taking care of your client; then, you can refer them to the Aging Life Care Association. These people are experts in geriatric care management. Let us talk about the worst-case scenario. Let us say that before you can help your client get diagnosed and do that financial vulnerability assessment, they were scammed and lost most of their money and resources. In these dire situations, the United Way has a 211 hotline and provides basic needs services. In desperate times, this could be a good resource for your clients. Similarly, if your older client has been exploited by someone they know, you can help find an elder law attorney in their area.

The Good News – You Can Boost Your Cognitive Reserve

Now, onto the good news. While it is great that there are some actions you can take to help your clients once you notice problems, it is even better to be able to provide proactive support to your clients by sharing with them information on how to maintain cognitive function in their later years and therefore reduce their risk for financial exploitation.

Until now, as I mentioned, I have been focusing on the depressing part of this graph, underneath the orange line. Now, I am going to focus on the positive part of this graph, which is above the orange line. All of us here would like to maintain good cognitive function for as long as possible, and that leads to the question, are there things I can do to help my cognitive aging trajectory stay flat rather than decline? The answer is yes.

There are many things that you can do. While the methods I will discuss will help you maintain good cognitive function at any age, they will be most effective if implemented in your 40s and 50s. Our 40s and 50s are pivotal times in which our everyday habits dramatically impact our cognitive function and brain health in our 70s, 80s, 90s, and 100s. I will frame these methods within a theoretical framework called cognitive reserve.

Yaakov Stern developed the concept of cognitive reserve at Columbia University. He defines it as the extent to which we use our brains efficiently and flexibly. I like to think about maximizing the brain you have right now. The background behind how he developed this theory is interesting. Cognitive aging scientists ask middle-aged and older adults to visit labs periodically for several years. Each time participants come to the lab, they complete a whole bunch of cognitive tests and other things.

Some participants very generously donated their brains to the scientists upon the participant’s death, and when the scientists did the brain autopsies, they found that some of these brains had moderate to severe nerve pathology, indicating that they had Alzheimer’s disease. Then, the scientists went back to see how these people performed on those cognitive tests, and they found that some of these people performed normally for their age and education level despite having moderate to severe nerve pathology.

This led to the question, well, how can it be that these people performed normally despite having moderate to severe nerve pathology, despite having Alzheimer\’s disease? Yaakov Stern theorized that these people had high cognitive reserve. They maximized the brain that they had. There have probably been hundreds of studies to support this theory. Some of the recommendations from the National Institute on Aging, the Alzheimer\’s Association, and even AARP are based on evidence coming from this theory.

Today, I will focus on the evidence from engagement in certain types of everyday activities. While these methods will be most effective when implemented in your 40s and 50s, studies show you can boost your cognitive reserve even in old age. The bottom line is that having a high cognitive reserve can help compensate for age-related neurophysiological changes and neuropathology.

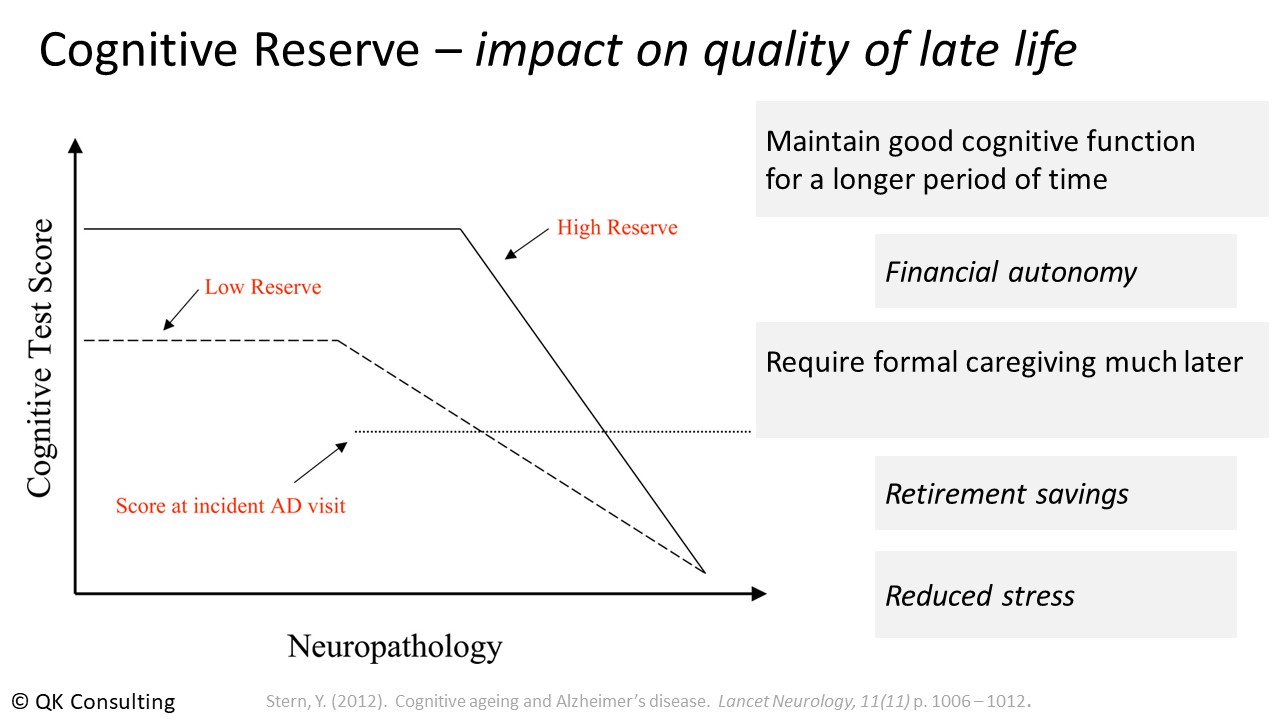

This graph illustrates how cognitive reserve impacts the quality of late life, and for only having three lines on it, it packs much information, so I am going to spend some time walking through it.

On the y-axis, we have performance on the cognitive test; let us say it is a short-term memory test, and on the x-axis, we have the amount of neuropathology that is building up in the brain over the last 15 years of life until death. Already, this is a little depressing. I am talking about death.

Here we have Michael, who has a low cognitive reserve, and here we have Henry, who happens to have a high cognitive reserve. For simplicity’s sake, we will assume that Henry and Michael have the same amount of neuropathology at the beginning of this time frame and that it accumulates at the same rate over those 15 years of life until death. I am going to start with Michael.

Michael performs well on this cognitive test, and despite the accumulation of neuropathology building in his brain, he can maintain that good cognitive function for about seven years. At this point, he starts showing cognitive decline. About halfway between the start of the decline and when he goes to see the doctor is probably when family and friends start noticing and paying attention. That dotted line is when Michael is willing to see the doctor about it, and soon after, some level of caregiving kicks in, increasing to 24 hours until death. Michael spends the last eight years of his life in cognitive decline and needing increasing levels of caregiving during the last five.

Let us move on to Henry. Henry, as you may suspect, performs better on this cognitive test, and again, despite the accumulation of neuropathology building up in his brain, he can maintain that good cognitive function for about ten years. At this point, he, too, succumbs and starts showing signs of cognitive decline. Henry is probably good at hiding his cognitive decline, so it is going to take a while for family and friends to start noticing. Again, that dashed line is when Henry is willing to see the doctor, and probably immediately after, some level of caregiving kicks in, increasing to 24 hours until death.

In comparison to Michael, Henry spends the last five years of his life in cognitive decline and needing increasing levels of caregiving for about the last two and a half years. What this graph depicts, therefore, is that having high cognitive reserve allows you to maintain good cognitive function for a much more extended period, which means maintaining your financial autonomy. It also means that your clients will require that formal caregiving much later, which impacts their retirement savings, a point I will return to in a moment. It also means they are probably walking around with less stress, not feeling they are burdening their spouse or adult children.

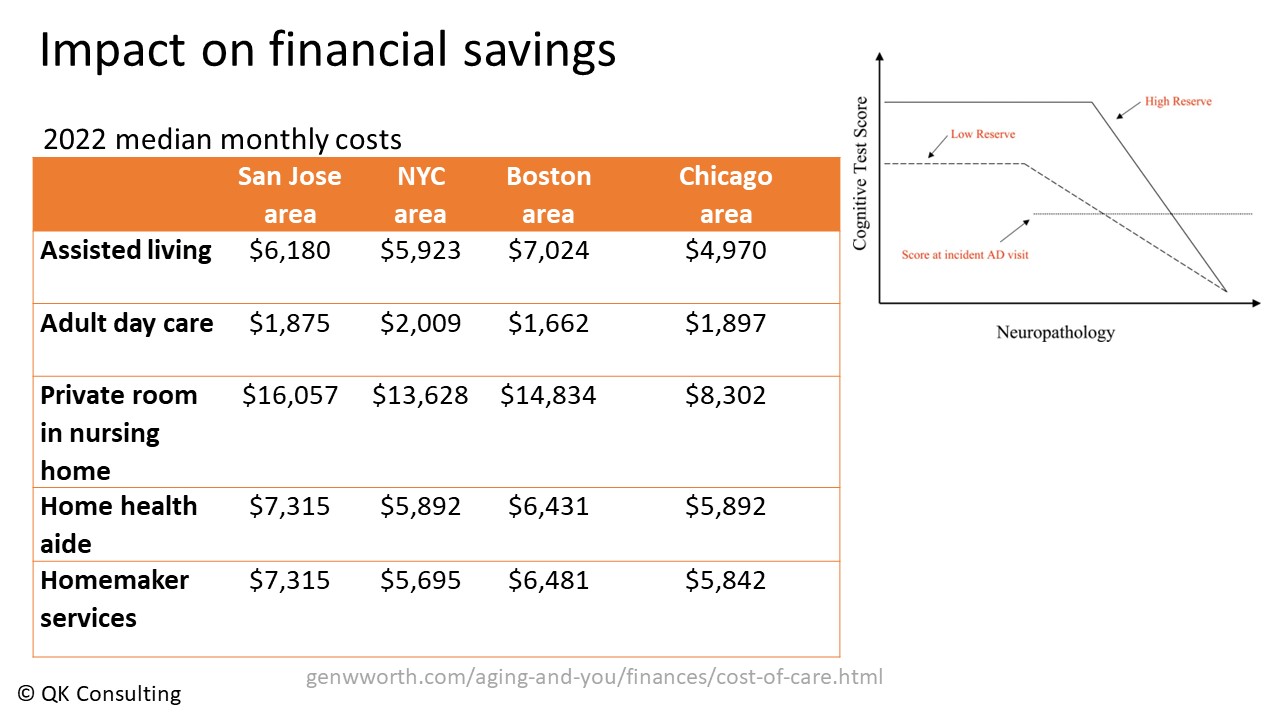

Getting back to that comment I just made about retirement savings. Here are the median monthly costs for various formal caregiving services for different areas of the country.

Staving off the need for adult day care assisted living or a home health aide for three or four years or even longer can significantly impact your client’s retirement savings. Again, most of us would like to have high cognitive reserve rather than low cognitive reserve, and again, this leads to the question, are there things I can be doing to boost my cognitive reserve? Very happily, the answer is yes.

Here are some keyways to boost your cognitive reserve. The first one is physical exercise. Regular physical exercise is a fantastic way to boost your cognitive reserve. Regular physical exercise has a double-whammy protective effect on our brains. On the one hand, it increases neural connectivity and cerebral blood flow, which are really good for our brain. On the other hand, it reduces the likelihood of things like cardiovascular disease, chronic stress, and poor sleep, all of which are risk factors for dementia.

Many studies have shown this association between regular physical exercise and cognitive function; today, I will focus on one. It comes from the Wisconsin Registry for Alzheimer\’s Prevention or WRAP study.

This is a large-scale longitudinal study of over 1,500 participants who are aged 50-70 years at the initial assessment, and 70% of the participants are at high risk for developing Alzheimer\’s disease because either one or both of their parents had a confirmed diagnosis of Alzheimer\’s, or they had the genetic risk factor for Alzheimer\’s, APoE4, or sadly they meet both of those criteria. These people are at high risk for developing Alzheimer\’s, but they are not yet showing signs of cognitive impairment.

Now, we know that the cognitive impairment that we have seen in loved ones is the eventual external expression of neuropathology that has been building up in the brain. These WRAP researchers examined the association between exercise and the amount of Alzheimer \’s-related neuropathology in the brain. They used two different methods to address this question. The first method asked their participants to complete a survey about their exercise habits. In the second method, they asked a subset of participants to complete a VO2 max test, and as you all know, a VO2 max test is when you get on a treadmill or stationary bike and are hooked up to monitors. It is an excellent, quantitative, objective measure of cardiovascular fitness.

The researchers found similar results from both methods. Among people who reported being somewhat sedentary and who did not have good cardiovascular fitness, the researchers found the expected presence of neuropathology in their brains. However, when they looked at the people who reported exercising regularly and who had good cardiovascular fitness, not only did these people perform better on cognitive tests compared to their more sedentary counterparts, but they also had no significant presence of neuropathology in their brains.

This is a remarkable, remarkable finding. Among people who are at high risk for developing Alzheimer’s disease, those who exercise regularly and who have good cardiovascular fitness have managed to stave off the beginning of the neuropathology that eventually leads to the disease. For those of you who already exercise regularly, give yourselves a huge pat on the back; you have been doing wonderful, wonderful things for your brain and your cognitive function.

How much exercise do I need to do to get these amazing cognitive and brain benefits? The answer is 150 minutes a week of moderate to vigorous exercise. It would help if you were breathing harder when doing this exercise than when going about your everyday activities. And if you or your client finds 150 minutes a daunting number, you can think about it as three 50-minute exercise classes a week, five 30-minute walks or jogs, or even a daily 21-and-a-half-minute walk around your neighborhood.

I spend about 21 and a half minutes getting my coffee in the morning, so most of us can find 21 and a half minutes in the day to exercise. Cardiovascular exercise is probably the best thing you can do for your late-life cognitive function and brain health.

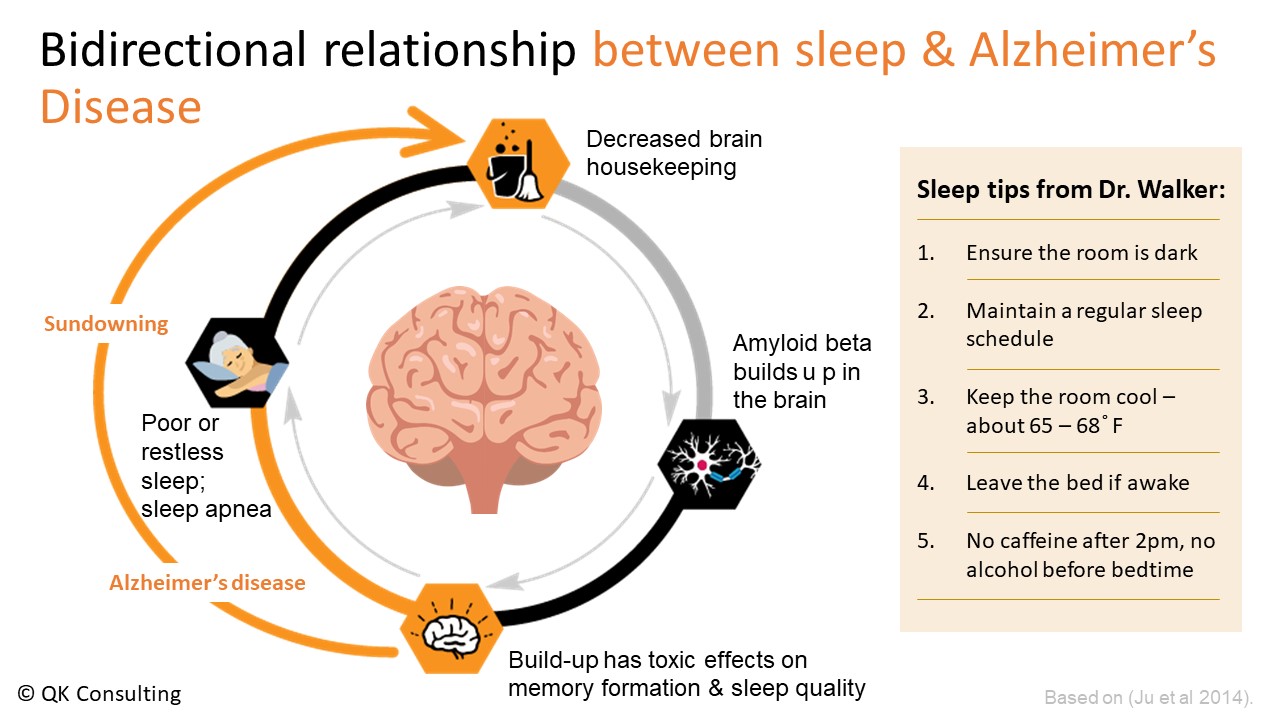

The second one is that getting seven to nine hours of sleep regularly is the second-best thing you can do for your late-life brain, and this is really a Goldilocks and the Three Bears situation. Getting less than seven hours definitely increases your risk for dementia. Getting more than nine hours regularly also modestly increases your risk.

What happens is that when you regularly have poor or restless sleep, it prevents your brain from doing some important housekeeping, where it clears out all the bad stuff from your brain. Because it decreases the brain\’s housekeeping, amyloid beta builds up in the brain, and amyloid beta is one of the building blocks of Alzheimer\’s disease. It is what forms the plaques in Alzheimer\’s.

Unfortunately, some of this amyloid beta builds up in some of the sleep centers of the brain, meaning it makes it harder for you to get good sleep, which decreases the brain housekeeping, which leads to even more buildup of amyloid beta, and so on, and so on. This vicious cycle kicks in, and eventually, it happens often enough that it leads to Alzheimer\’s disease, and then this leads to sundowning, which is basically when your night and day get shifted. These are when people are up at night and sleepy during the day.

While we cannot control how many hours we sleep or the quality of our sleep, we can control our sleep habits. You see above some sleep tips from Dr. Matthew Walker, a sleep scientist from UC Berkeley. You are probably familiar with most of them.

The new one might perhaps be the last one about no nightcaps. If you struggle to get seven hours of sleep, you must remember that you must go to bed at least seven hours before you get up the following day. You need to allocate at least seven hours of bedtime to achieve seven hours of sleep.

The third best thing you can do for your late-life brain is to have a healthy diet. Eating a healthy diet is important in our late-life cognitive function and brain health. Scientists have ascertained that some food groups, like green leafy vegetables and whole grains, are brain-healthy, and these food groups block that amyloid beta, as well as something called neuroinflammation, which is also bad for your brain. Scientists have also ascertained that some food groups are brain unhealthy, like fast, fried foods and sweets. These food groups increase the amount of amyloid beta in the brain.

A 10-year longitudinal study in which about 1,000 older adults completed annual cognitive and dietary assessments classified the participants based on whether they had high, moderate, or poor adherence to a brain-healthy diet. People who had high adherence to a high brain health diet had a significantly slower rate of cognitive decline than people who had moderate or poor adherence to this diet.

The difference between the high adherence people and the poor adherence people cognitively speaking, high adherence people are seven and a half years younger than the people with poor adherence to a brain-healthy diet. These researchers found similar results with participants who had suffered a stroke, and kind of as a side bonus, having a brain-healthy diet is associated with a lower risk of depression—some powerful effects of diet on our long-term cognitive function.

The last way I will cover today is on everyday activities. Researchers have found that having high levels of cognitive engagement in everyday activities can also help delay or slow down normal, age-related cognitive decline, as well as reduce your risk for dementia.

Dr. Denise Park and her colleagues theorized that learning a new skill could be one way that people boost their cognitive reserve. She asked middle-aged and older adults to sign up for a course to either learn digital photography, quilting, or how to use all the apps on their iPads. This was a big commitment for these participants because it was a three-month course with about 15 hours of coursework per week—a significant commitment for these participants.

She also had what we call an active control group. These were similarly aged people who spent the same 15 hours a week for three months doing something they already knew how to do. Regardless of the group, everybody took cognitive tests before and after those three months.

What Dr. Park found is that when people learned a new skill, not only did they show significantly greater improvements on those cognitive tests compared to the active control group, but they also showed what she called reliable improvements in memory. She defined having a reliable improvement in memory as showing at least a one standard deviation increase in performance from baseline—a pretty substantial improvement.

What is exciting about this last result is that she found reliable improvements in memory even amongst the oldest participants, who were in their 80s. Learning a new skill is a great way to boost your cognitive reserve. Learning and practicing mindfulness have some wonderful benefits for our aging brains. I was involved in some research suggesting that activities that require good processing speed and working memory may benefit the most. Again, processing speed is how fast your brain works.

Now, just like with exercise, we have that criterion of 150 minutes to get cognitive benefit. We also have a couple of criteria for an everyday activity to be cognitively boosting. First, you must find it interesting; otherwise, you will not do it. Secondly, it must be at least moderately challenging. When doing this task, you are focused; you are making mistakes and must try multiple times before you get it right. To put it in the context of a popular conception, if you regularly solve the New York Times Sunday magazine crossword puzzle, doing more crossword puzzles will not really boost your cognitive reserve. It would help if you shifted to the sudoku or the spelling bee.

The second point I want to make here is that this will be a very personalized, individualized list of activities. What I find interesting and challenging differs from what someone else finds interesting and challenging. There is no generic list of cognitively engaging activities. If you are already a polyglot, learning an eighth language is not going to be as beneficial as someone who is about to learn their second language. It is a very personalized list of activities.

Key Takeaways

- Unfortunately, the number of older adults with cognitive impairment, either diagnosed or undiagnosed, is relatively high, possibly higher than many of you realized.

- Cognitive impairment negatively impacts older adults’ ability to maintain financial autonomy, and again, financial autonomy is the ability to control your financial decisions and behaviors.

- Cognitive impairment also dramatically increases the risk of financial exploitation, undue influence, and wealth loss due to poor decision-making.

- The good news is that there are several steps that you can take to protect your older clients, such as becoming familiar with the difference between typical age-related changes in cognitive function and signs of cognitive impairment.

- You can also hire that trained geropsychologist to conduct a financial vulnerability assessment to determine which areas the client still has financial autonomy and where they need support.

- Finally, encouraging your clients, especially those in their 40s and 50s, to follow a healthy lifestyle can substantially help them maintain good cognitive function in late life and preserve their financial autonomy.

- Research has found that people who follow a healthy lifestyle through regular exercise, adequate sleep, healthy diet, and so forth reduce their risk of dementia by 30-60%.

By Jamie Hopkins, Esq., LLM, CFP®, ChFC®, CLU®, RICP

The best thing we can do to improve our retirement income situation is to make a smart decision about when and how to retire.

Most Americans think they will retire later than they actually do, as two-thirds retire earlier than planned.

Pushing off retirement is very beneficial. We should plan for the uncertainty of retiring earlier than we project ourselves to retire. COVID is a recent example. In 2020/2021, many people were forced into retirement and didn’t really want to retire yet. Now, they have to deal with that from a retirement income sustainability standpoint.

How We Make Decisions

Now, how do we make decisions? We make decisions based on our experiences and knowledge. We really can’t make decisions about anything else. When it comes to retirement, what do we know? What have we experienced? When you think about retirement for most people, what do we learn throughout our lives regarding retirement planning? We learn about saving, not spending, and that we should save more than we spend. If you save more than you spend, you will grow your wealth. And if we keep doing this repeatedly from ages 20 to 65, we’ll end up with enough money to retire. The retirement savings system’s automatic behavior features and nudges that we have created as a society, as public policy, and as employers, revolve around this notion.