By Cindy Hounsell, JD, President of Wiser

I thought I’d begin with a little story on how I happened to get involved in this aspect of women’s retirement. About 12 years ago I was invited to speak at a big Aging Conference in Pittsburgh. The people there said to me that it’d be great if you could talk about how these issues affect caregivers’ retirement security.

At the end of the hour session over 200 people stood in line to thank me for bringing up the fact that – and many of them told me their story over the years how they quit their jobs, moved home to take care of their mother or they’ve taken care of their husband. All the money was gone by the time their moment came and then they had nobody to take care of them.

With that, we started developing materials just so that people could make the consideration not telling people what they should do, but making this an issue that if your siblings live at the other end of the country and you’re the one doing the caregiving, you need to talk to them about the cost for you personally either through your job or through money that you’re spending all the time. With that, that’s my caveat. I’ll start to get into some of these statistics.

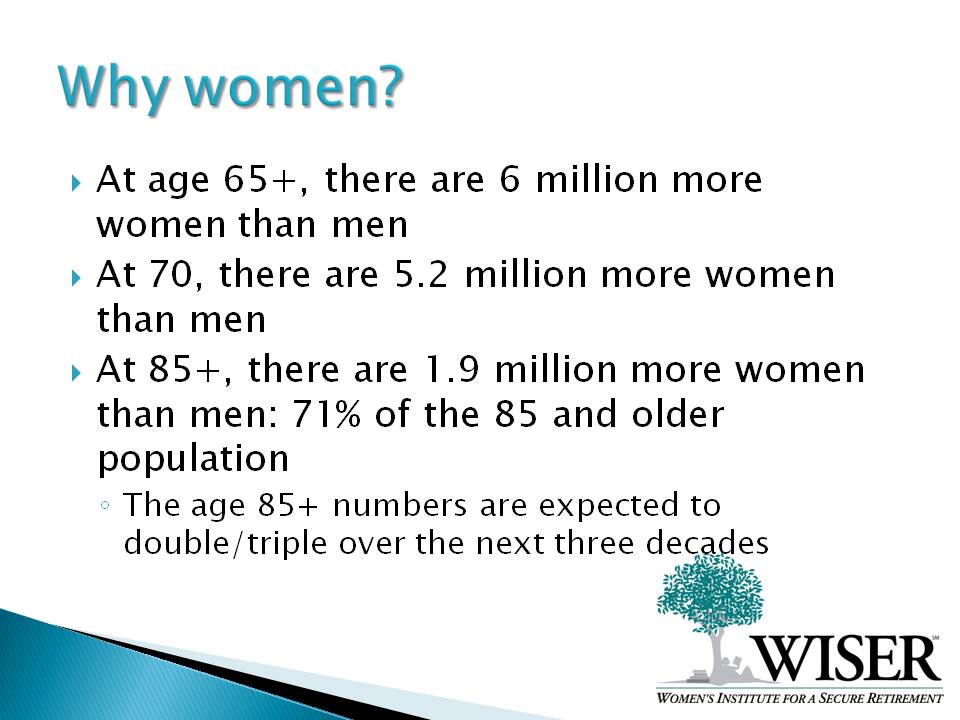

One of the things they often don’t take care of is their own finances, which is an important aspect and why we hope that a lot of planners will start making this point very directly with women. A lot of times people say to me is. “Why women? Don’t men have many of the same problems?” Yes, many of them do and many men are caregivers, but the issue is that there are so many more women than men and at age 65 as you can see from the slide, there are six million more women than men. At age 70 there are 5.2 million more women than men. At 85, there’s almost two million more women than men.

Seventy-one percent of the age 85 and older population are women. Many of them are single as opposed to the majority of men who are still married if they’re living at the age of 85. The reason that has great significance is with the baby boomers, the age 85+ numbers are expected to double and triple over the next three decades. We’re going to have millions of women that will need help and may not have the money to finance that help. We’re trying to address these issues that put women at significant risk of poverty in retirement. What I like to tell people is that these issues affect us all.

Then the other huge shift is that there are more single women than ever before. That just means that you don’t have other people to help you out. This number has tripled and we’ll have, obviously, enormous implications for the future. The issues you may have heard before is women live longer and they earn less over their lifetime. They take time away from work for caregiving, and they’re twice as likely to work part-time as men do. They have far less income from pensions and other retirement plans. Over a lifetime, they’ve earned less, and many of them have much less in savings and assets as well as in their retirement plans. There’s always glimmers of good news that women are beginning to do better and bad news for men because of the economic crisis.

It’s happened at different times since 2008 over who’s doing better from the jobs in the economy. They’ll be a big spurt of men doing better and then in the next economic segment women do better.

Preparing to Protect Your Retirement is the Key

Women need to reshift their thinking. I live here in Washington, D.C. and I think there’s a lot of talk about what to do about these problems, but there’s no big plan coming down the road that people can agree on.

The health care costs are estimated at $250,000 for a couple during retirement, although that includes your Medicare premiums which are probably likely to keep going up and all the different premiums that you paid for Medigap insurance. I think if people buy also the right types of insurance, they’re protecting their assets in another way. A lot of people think they can self-insure and you need a lot of money to do that.

The reason I started telling that story in the beginning is that a lot of times people don’t realize they are caregivers. I have a friend who said to me, “That’s the craziest thing I’ve ever heard.” He said, “How can you not know you’re a caregiver?” I showed him the checklist of who is a caregiver, and he realized that he had been a caregiver when his wife who had breast cancer, had passed.

It was like he just did all these things not thinking that this was having any kind of an impact on him until, he saw the list of things and it was like yes, that’s what happened to me too. The other piece of this not only does it have an impact on all the other issues we’ll talk about, but it’s the financial impact that people have to really be aware of, and impact on families. When one person is taking on the burden, that needs to be shared somehow with the others who can’t take it on, family then needs to help pay for what that other person is doing especially if there’s money to do it.

Real Financial Consequences

There are a number of recent studies that show that especially women caregivers to elderly parents are much more likely to end up living in poverty. These are the stories that we hear most often.

What some states are doing now when the parents end up going on Medicaid benefits because they’ve spent down and they have no more assets and they go into a nursing home, the state then will take the house. The adult child who’s been doing this care may think, “I’ll sell the house; at least I’ll have something, since I gave up my job.” I get a lot of middle-age women telling me that we have to create more materials for younger women, because younger women are quitting their jobs in their 30s to go home and take care of mom and dad, and they’ll never find another job in this economy, especially if they have benefits.

It’s just part of the same thing, but we’re hearing much more of the end of the baby boomer – the tail end of the baby boomers who are already involved in this. Women caregivers, who are on the lower end of the educational spectrum, are three times more likely to live in poverty and ten times more likely to be on supplemental income, which means you’re very poor.

The Cost of Lost Opportunities

In August (2013), we’re going to be reissuing our booklet called Financial Steps for Caregivers. We have budget fact sheets for the person who’s the caregiver, as well as for all the caregiving expenses.

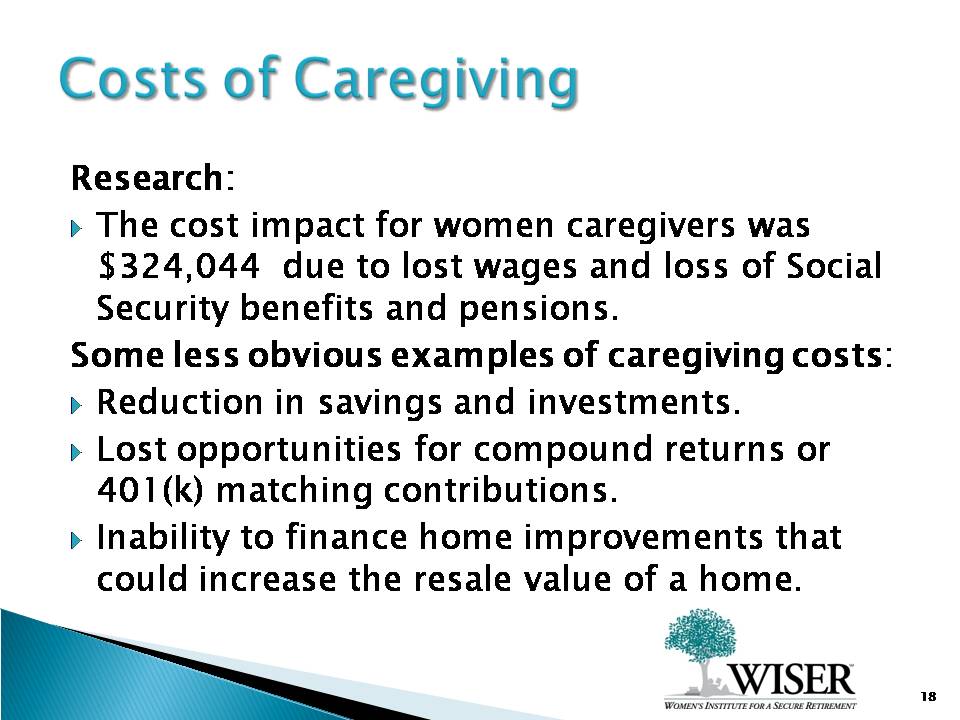

One of the most important studies found that caregiving costs women $324,000 due to lost wages and lost Social Security benefits and pensions. There are all these indirect losses that people just don’t even think about. You’re not able to save and invest. Lost opportunities also include compound returns and contributions to a 401(k). Simple things like the ability to finance home improvements that could increase the resale value of your home are also a hidden cost. Those are the first things that go.

Promotional opportunities: A lot of times people give up the job at the next level because it’s going to require travel or require more hours and they just don’t have it in them to take on something else. I’ve known lots of women that have done that just because they couldn’t do anymore than what they were doing other than taking care of their parents.

I’m an only child. My dad died first and then my mother died three months later. He said to me, “do not, do not, do not leave your job.” He was the first person who said, “There’s money for your mother and she has people to take care of her. You have nobody else to take care of you. Do not leave your job.” It was the best advice, which is why I pass it on to other people, but my mother wasn’t happy about that.

She would have liked me to have quit my job, come down and basically sat with her. She could get around. She had her own network of people. It was clear to me – I had just started a new job with benefits and a whole career change and if I dropped out of the workforce at that point I don’t know that I would’ve ever been able to return. People just need to weigh that what they’re doing is the right thing. I was lucky my dad gave me that permission. I never would’ve seriously thought of it myself. I probably would’ve just left and gone there.

When you’re leaving your job, you also have to think about your retirement plan and whether you’re vested or not. A lot of times people just don’t take that into consideration. They’re freaked out and there are so many issues. There are emergency hospitalizations and they just can’t take it anymore. If you can at least help people to think about it, you can do their thinking for them.

The good news is that we have the year-by-year earnings and the Social Security statements, now so people can really at least look at that and pull it out. Granted it’s not mailed to you anymore like it was. If you put in a zero in terms of what you’re saying your best 35 years are, that’s going to really bring the benefits down.

Other Resources

One of the other great places where you can get help is the Eldercare Locator (1-800-677-1116 or www.eldercare.gov), which is sponsored by the Administration on Aging, if you need to hire a home health aide to go in and help immediately. I have a lot of friends who do this with aunts and uncles. I’ve heard them say, “Thank God for that Eldercare Locator because it’s just a place to send people where you can really find emergency help all over the country.”

They’ve been running this for a long time. They have a whole vettedsystem state by state. It’s pretty trustworthy or they wouldn’t be doing this. If it’s not vetted because of where it is in the country, they tell you that in the first place. There’s a pretty good network out there. As I said, I see a lot more of these. I think people are seeing this as a business opportunity to start home health care agencies.

I have a friend that bought into a franchise where they provide this kind of thing. Her dad passed and her mom just needed some help a few hours a week not necessarily with health care, but also just basic stuff like grocery shopping, paying the bills and companionship and there are a lot of people that are moving into that. It’s a great service.

Out of Pocket Monthly Costs for Caregivers

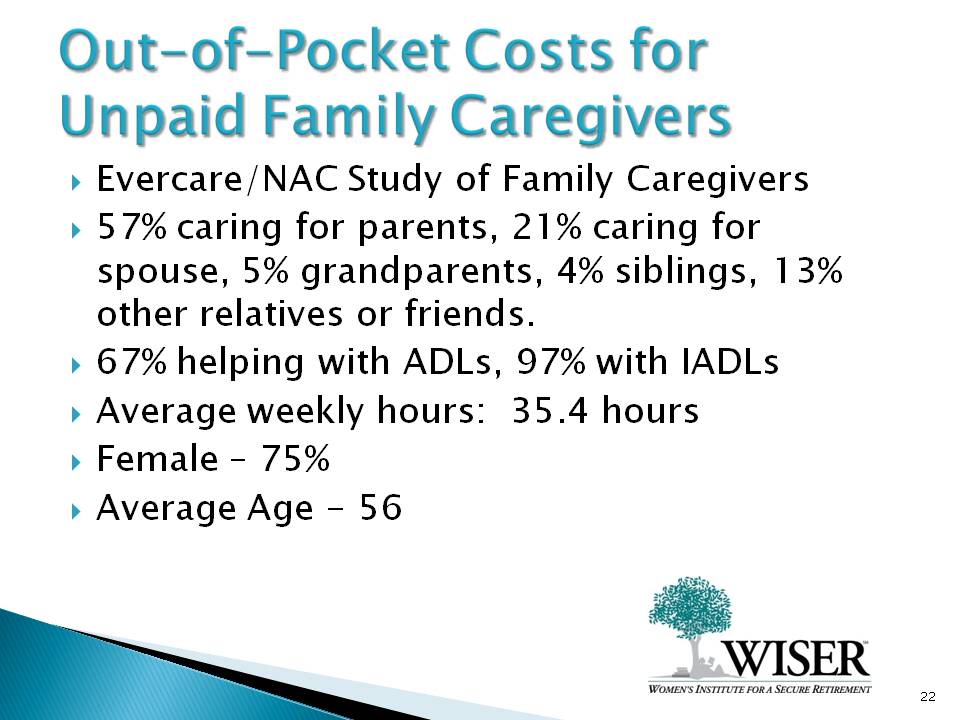

This is an area that I think is really important for people to know about as well. The National Alliance for Caregiving broke down what people were doing, how they were helping, the average number of hours a week, and then looked at the out-of-pocket cost. You can see the average age there, 56, one of the prime ages for saving for retirement for most people and also the large group of people that are predominantly females.

ADLs are activities of daily living – bathing, dressing, helping someone with their bathroom needs. The IADLs (instrumental activities of daily living) are just sort of instances where somebody would be able to get out of bed and wouldn’t need that help. They just need help with other things.

That’s one of the things that’s tricky with a lot of the long-term care insurance: a lot of times the clauses in the long-term care insurance says that they’ll pay for home health care only for certain activities of daily living. That’s something people need to know also. We’re not really getting into that in this session. You’re able to get some help from their long-term care insurance and maybe the things that are the problem with your mother or father are not the things that are actually covered.

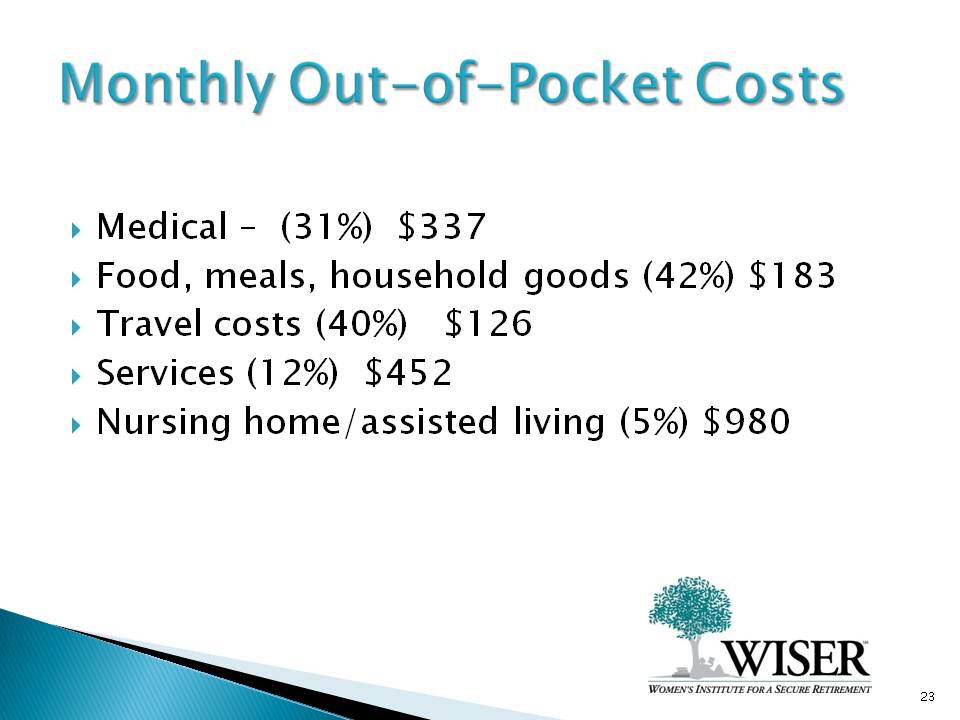

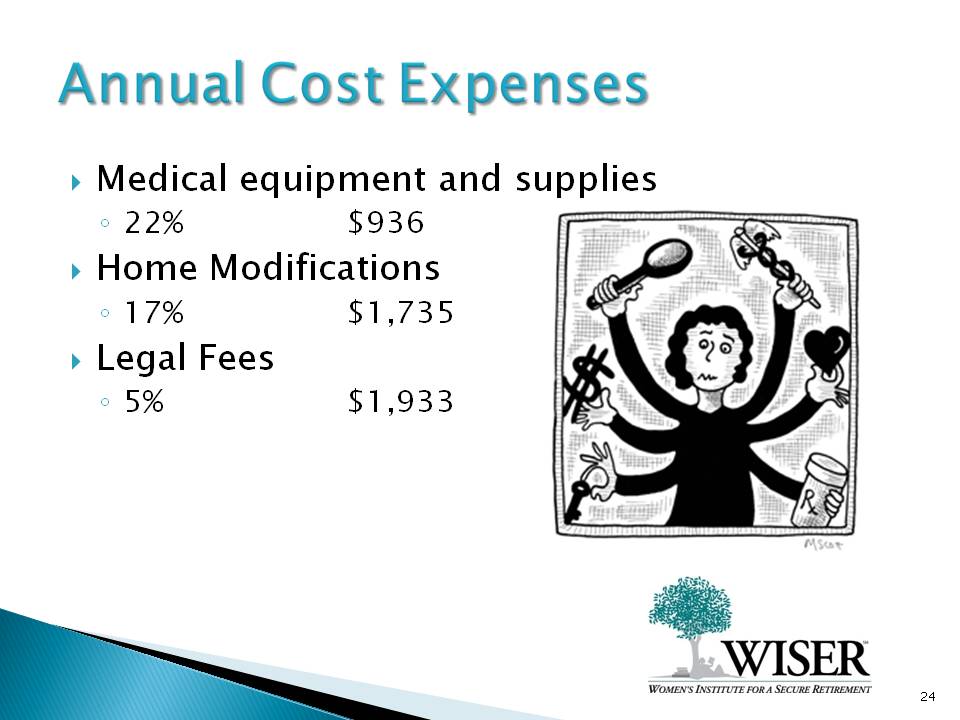

The medical costs to the caregiver are obvious – $337 a month for things like travel cost, gas and things like that – things that people aren’t thinking about. The other things are food and also paying for medication. A lot of times people just go and then they pay for it because they’re in a hurry and they’re not even thinking that this is all going to add up at the end of the year or the end of the month. These annualized costs such as the medical expenses overall, transportation and groceries add up to real money.

Paying for home modifications and then legal fees are also pretty big expenses.

I’m sure people that are on this call here as well have done it for family members. You love them, you want to take care of them, and you just don’t realize what’s happening. When you pull out your credit card and you write that check out of your own pocket, especially if you have other family members that really should be helping out, it all kind of gets lost in the shuffle because you’re in the middle of trying to take care of them. From a behavioral finance perspective, all those things that you know that you should be doing kind of go out the window.

We have a whole fact sheet that shows you a budget where you can include these costs if there are other family members. Once the person is deceased and you start looking at what’s left, it’s important for people to be able to show this is the money we spent on this. It gives you a record of showing this is where the money went because that’s where the problems come in for a lot of families.

Legal Agreements for Families and Caregivers

I don’t know how much people have heard about this, but it’s a pretty big issue where a lot of families are now doing this. It’s a formal contract. It states what the care is to be provided, how much the caregiver will be compensated and can be used whether or not the caregiver is a family member. There are a lot of programs that allow the family caregiver to be paid. If that family caregiver is paid, then it’s really more important for the other family members to know where the money is going.

I usually tell the story about a person who called herself good ole Becky, who had taken care of Mom. One brother was a lawyer in New York and the other one a doctor in San Francisco. These two brothers were I think younger than she was, but not a lot. They had always been very competitive. They started just fighting over the china for the grandchildren. She came in and she just said, “Boys, boys, boys. Dad will be eating for the rest of his life. You’re not taking the china and it stays here.” Four or five years later her dad got sick and she sat the brothers down. This was before she made her own agreement. She said, “I was tired of being good ole Becky.” So she did was she made them pay for her retirement. She threatened them by saying, “I’m going to put dad in the nursing home,” and of course, they were furious about that. They wanted her to take care of him. Then she got them to pay her and pay her well. It was the first time I had ever heard anybody talk about that.

I think there are lots of ways a personal care agreement can be worked out. It brings out every family issue that’s been happening, and is brought out when these stressful situations play out and money is involved.

Meredith: What state was it? Massachusetts or Rhode Island or maybe another one where they allowed family members to be paid caregivers from this state system?

Hounsell: There are a lot of states that do that now. That’s been a big change in the last three to five years. It depends on which program you’re getting paid out of. There are certain states that are partnership states that have long-term care and insurance available. There are just a lot of different things I think people need to know about the state wherever their parent is or the person that they’re caring for. You need to try to find the rules as best you can.

There are also geriatric social workers. That will be the first thing if I had to do it over again. I did it all myself running back and forth and setting up the care for my parents. Like today there probably would be a geriatric social worker who would come in, make the assessment and be able to tell you from looking at their income exactly what they would be eligible for. I have someone who I know here who works on Capitol Hill she and her sister did that for their mom in Ohio. She told me that story and it was pretty incredible.

She said we could never have given my mother the care that she needed. We would have never have found out any of this in time. It’s just another opportunity. Looking at the money mistakes that women caregivers make is not making their own finances a priority, using money for everyday expenses such as purchases at the grocery and drug store and trying to pay for everything when you really can’t afford it.

If you can’t find it in your own family, find it someplace else like either through the National Area Agency on Aging which is one of the resources that we would recommend. Every state has them, even, though a lot of their funding gets cut. There are people there that can tell you what services are available and what programs are available.

The Family Caregiver Alliance is another resource that has been around for a long time and they run programs. They’re based in California, but they run programs that train caregivers and provide respite for caregivers. They have a great website. The National Alliance for Caregiving mainly does studies. They fight for all of these issues here with policy makers. They have really put the issue on the map. AARP has recently made caregiving a really big part of their current agenda. You can go and check that out too. I think they have a map where they provide help for every state.