Charitable planning tools can also be utilized to diversify assets.

Ninety-seven percent of high-net-worth individuals say they give to charity. Seventy-one percent of high-net-worth individuals agree that discussing philanthropy with their advisor is important. Fifty-nine percent of high-net-worth individuals want their advisors to utilize a team approach when something outside their advisor’s wheelhouse; that includes charitable, tax, legal, and other aspects. Your clients want you to talk about philanthropy even if they are not considered high net worth.

The New Provisions in SECURE Act 2.0 for Charitable Income Strategies

The SECURE 2.0 Act was passed on December 29, 2022. It is designed to enhance retirement security for Americans. It stands for Setting Every Community Up for Retirement Enhancement. It includes a Qualified Charitable Distribution (QCD) from an IRA.

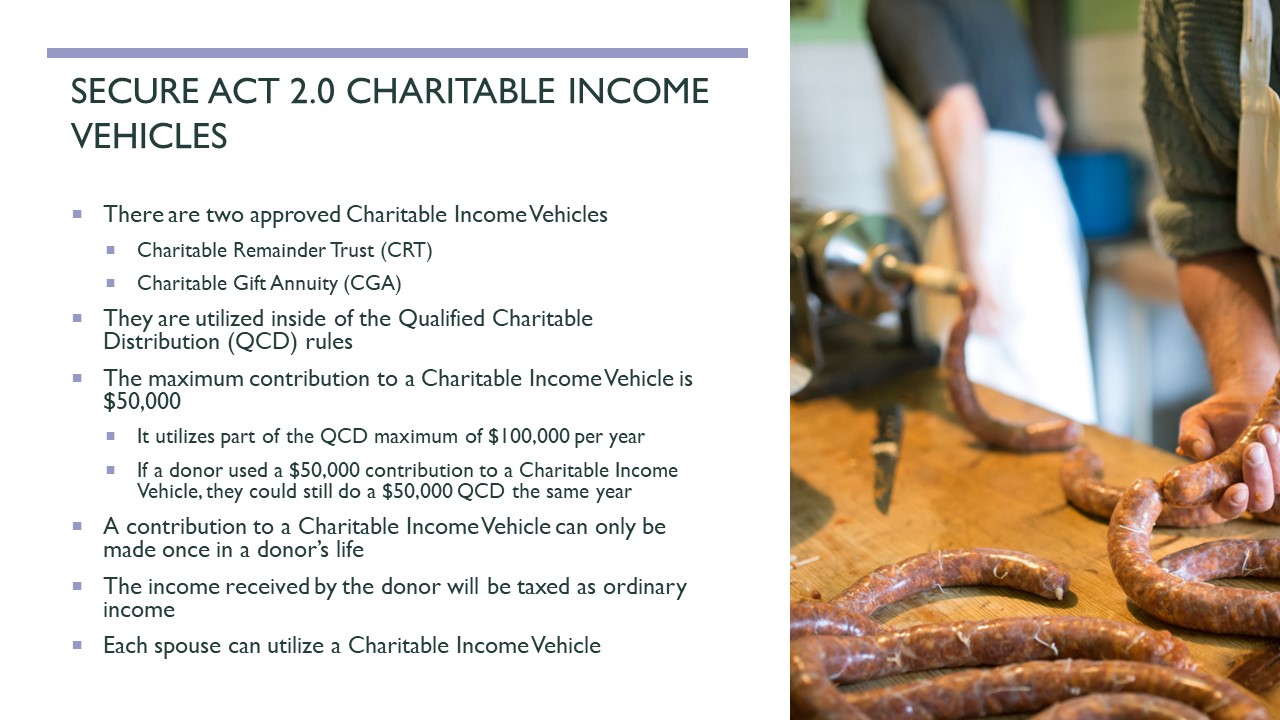

SECURE 2.0 Act allows for an investment of up to $50,000 into a charitable income vehicle. That could be a Charitable Remainder Trust (CRT) or Charitable Gift Annuity (CGA). When you look at it, $50,000 is not much money. Lobbyists asked for a $250,000 limit for this type of gift. We got what we got. We are happy with $50,000. However, it is available to use only once in a lifetime.

Before we hop into the CRT and CGA, we will discuss what a qualified charitable distribution does. How does it work from your IRA?

CRT income vehicles must be done using a qualified charitable distribution. Assets need to be from an IRA. They can be rolled over from other retirement accounts. The donor must be 70.5 years old. I realize that is no longer the required distribution age, but the youngest age for making a qualified charitable distribution is 70.5 years old.

Before clients must take their RMD, they can do a qualified charitable distribution from their IRA, allowing up to a $100,000 distribution to charity per person per year. The SECURE 2.0 Act also made that amount indexed for inflation starting next year. A client can give to multiple charities. I am always talking to donors about IRA assets being one of the first assets they give. When we can reduce the required minimum distributions, we can also reduce other tax rates. We are reducing their adjusted gross income.

Distributions from qualified plans will be taxable to their heirs and the next generation. Why would you not gift from the pool of assets taxed as ordinary income to the donor, their spouse, and their children? It is the best asset to give because most other assets will get a step up in basis if they are under the estate tax exclusion amount. It can also help avoid double taxation. If you have large IRA accounts, you pass away with them, and are in the estate tax realm, it qualifies for double taxation.

The one thing to note is that the qualified distributions must go straight to charity. If the check is made out to the charity, the donor could deliver the check, but that is it. It is better to ACH the distribution and keep the donor out of the interaction.

For example, say we have a 73-year-old with a $500,000 IRA. Their required minimum distribution is slightly over $20,000, but we will simplify it. They are in a 25% tax bracket. Currently, they are giving $10,000 to charity. Before the qualified charitable distribution, we take the $20,000 RMD. We pay our 25% tax on it. That leaves us with a $15,000 net distribution. We make our charitable contribution of $10,000. It leaves $5,000 in the client’s pocket.

Let us compare this to utilizing a QCD. We have the same RMD requirement. Instead of taking a distribution, we will distribute part of that to charity. We increased the charitable amount from $10,000 to $13,000. When we do tax-advantaged strategies, we can give more. That leaves us with a $7,000 net distribution that, when taxed at the same 25% tax rate, leaves the client $5,250 versus $5,000 if they took the RMD and made their charitable contribution.

There are other results. The charity receives 30% more. The client has five percent more back in their pocket. We lowered their taxable income. We lowered their adjusted gross income, which helps them save on Medicare tax, Social Security tax, and possibly net investment income tax. When we lower the taxation, we can also save on other taxes.

Secure Act 2.0 Charitable Income Vehicles

As I mentioned, there are two approved vehicles: the charitable remainder trust (CRT) and a charitable gift annuity (CGA).

The maximum contribution to one of these charitable income vehicles is $50,000. I mentioned that the qualified charitable distribution (QCD) has a maximum of $100,000 per year per person. A $50,000 charitable income vehicle gift utilizes the QCD maximum. If someone were to contribute a $50,000 charitable gift annuity this year (a once-a-lifetime contribution), they could also do a $50,000 qualified charitable distribution straight to the charity.

The income received from a CGA is ordinary income. Those familiar with charitable remainder trusts or gift annuities know that the income distributions can be partially tax-advantaged. However, if it comes from an IRA, it passes through that same taxation. When future distributions come from these income vehicles, they are fully taxed as ordinary income, just like the required minimum distribution is taxed. Each spouse can utilize one of these vehicles.

Tools and Strategies for Retirement Income Planning

Charitable trusts are the Swiss army knife of planning. They can be applicable even if our clients are not charitable.

Three types of trusts are generally used for charitable income planning. Charitable trusts came into the tax code in 1969.

- The charitable remainder trust is approved in the qualified charitable distribution. It is for capital gains tax assets. It saves on capital gain tax, net investment income, state tax, depreciation recapture, and estate taxes. When I use a charitable remainder trust, I am looking for capital gains tax assets to put inside the trust or to help with income tax issues.

- A Grantor-Charitable Lead Trust is for income tax issues.

- A Charitable Lead Trust is for estate tax issues.

Here we will focus on the Charitable Remainder Trust and discuss the Charitable Gift Annuity later.

Here is a quick explanation of how they work. We have an asset, say an apple tree, which produces income (apples). The donor can put the tree inside a charitable remainder trust for a term of years or until the end of life for multiple lives if the calculations work out correctly. They can:

- Get the income for life.

- Get an income tax deduction for the future gift of the tree to charity.

- Save on taxes.

- Still nurture the tree. They can be the trustee. They can fertilize it and choose how it is invested.

A charitable remainder trust is an irrevocable trust. The assets may be in an irrevocable trust, but the donor still has much say in managing the assets if that language is contained within the charitable remainder trust document.

With a charitable remainder trust, your ideal client is someone who has a capital gains tax asset or an appreciated asset. They could be selling a business. They might want to do a Roth conversion. The unique thing about a charitable remainder trust is that they do not necessarily have to be charitable. The other two income vehicles we will discuss, the charitable gift annuity and a pooled income fund, only work if someone is charitable.

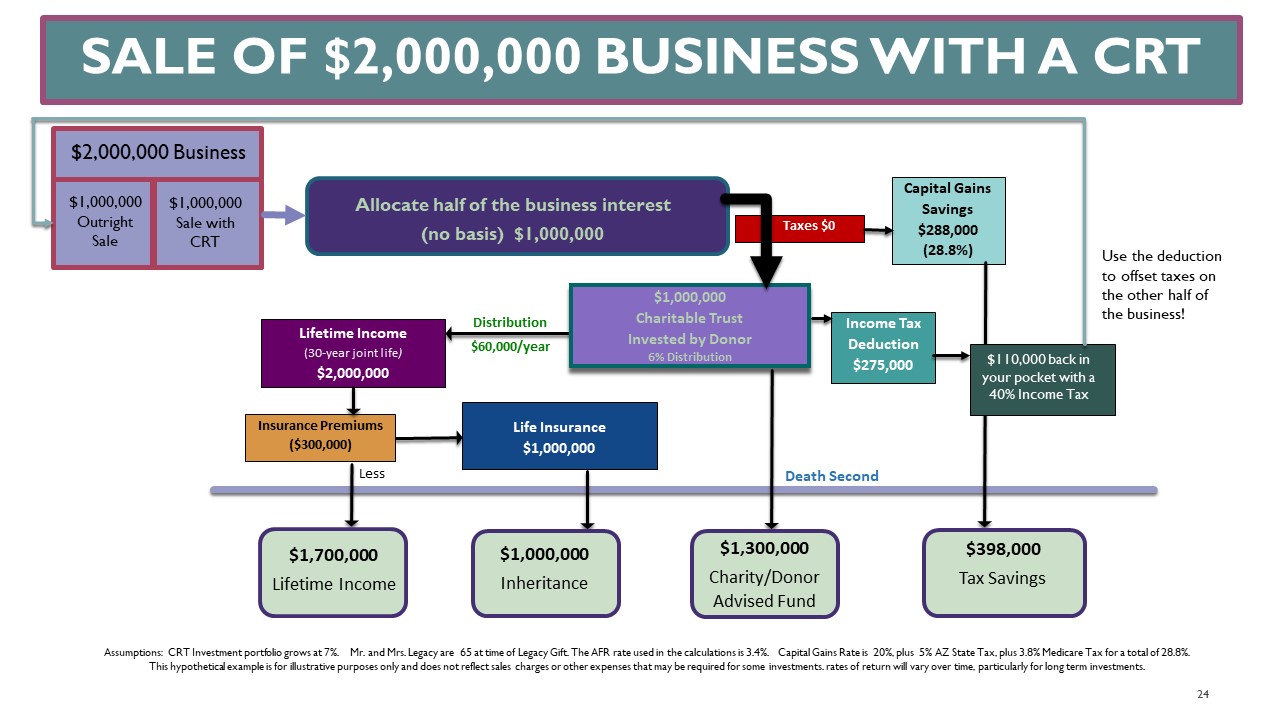

For example, say you have a client who sells their business for $2 million without basis. When I do a CRT outside an IRA, I recommend not utilizing more than half of the asset. We want to keep our tax planning strategies as small as possible, giving our other assets more flexibility. The client can change their mind in the future and do other things. So, we will split a $2 million business in half and allocate $1 million to a charitable remainder trust.

We will transfer the title into a charitable remainder trust document prepared by an attorney. We can transfer that tax-free. We can sell it inside the trust completely tax-free. This trust has its tax identification number, and it is a charitable trust. All assets inside this trust will grow and compound tax-free as well. We saved a lot in taxes by transferring the asset and selling it inside the charitable remainder trust. You can see my assumptions and disclosures at the bottom. We are looking at $288,000 in tax savings at a 28.8% tax rate. We are looking at the 20% federal capital gains tax rate with $1 million. We are looking at a 3.8% net-investment income or Medicare tax and 5% on average for state taxes. After death, the funds from the remainder trust will go to charity. It could also go into a donor-advised fund.

Donor-advised funds are a wonderful way to teach philanthropy to children and grandchildren. It creates a unique family culture of values. A donor could have this trust for their and their spouse’s lives. Their family can manage which charities get those funds over time. They could do that with only part of the assets. They could give it all to one or ten charities if it goes to a qualified 501(c)(3) organization. Their charitable intent can be met.

Case Study of a Charitable Remainder Trust vs. No Trust

For example, let us say we have a 65-year-old married couple, Mr. and Mrs. Legacy, selling their business for $2 million. What might be the results of using a CRT to generate retirement income and pass on assets to their children versus not?

Assumptions:

- CRT investment portfolio grows at 7%.

- The AFR rate (applicable federal rate (AFR) is the minimum interest rate that the Internal Revenue Service (IRS) allows for private loans) used in the calculations is 3.4%.

- Capital gains rate is 20%

- 5% AZ state tax

- 8% Medicare tax

For a total of 28.8% assumed taxes. (This hypothetical example is for illustrative purposes only and does not reflect sales charges or other expenses that may be required for some investments. Rates of return will vary over time, particularly for long-term investments.)

First, they will allocate only half of the business interest in which they have no basis to a charitable remainder trust. Because this is a future gift to charity, they get an income tax deduction today of $275,000.

Let us look at the income. The client will distribute six percent or $60,000 a year. Over their 30-year joint life expectancy, they will receive $2 million in retirement income.

What about the kids? We can add in a 10-year premium life insurance that costs $300,000 for $1 million of life insurance. That completely replaces the asset inside the CRT. Their lifetime income after paying life insurance premiums dropped to $1.7 million. The children will get a $1 million inheritance.

Now let us look at the income tax deduction on the right. Mr. and Mrs. Legacy are in a 40% tax bracket this year. The gift of $1 million to a charitable trust gives them an income tax deduction today of $275,000. At a 40% tax rate, this provides $110,000 in tax savings back in their pocket. When added to the $288,000 capital gains, state, and Medicare tax savings because $1 million of the business asset is sold from within the charitable remainder trust, that is nearly $400,000 of tax savings of money working for them and not the IRS. We can then utilize the $275,000 deduction to help offset the taxes from the $1 million of the business share sold outright and not put in the charitable remainder trust. It can work the same to offset a Roth IRA conversion.

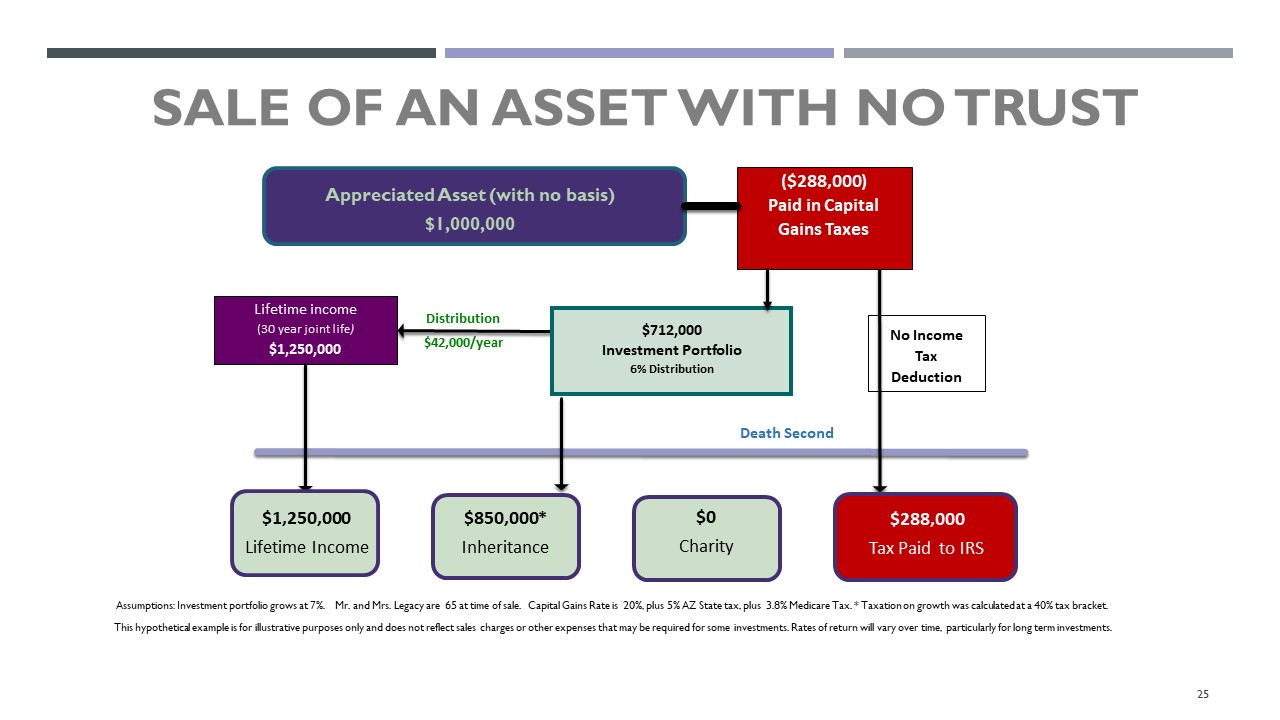

Now let’s look at what might happen to the remaining $1 million asset with no basis.

Mr. and Mrs. Legacy pay their capital gains and state and Medicare taxes and put it in an investment portfolio, leaving only $712,000 working for them. They can manage it in the same capacity as inside the CRT. If they take a six percent retirement income distribution, that only allows them $42,000 the first year. Over their 30-year joint life expectancy is only $1.25 million of retirement income. The kids get an $850,000 inheritance because that $712,000 asset has grown over time. Charity gets nothing.

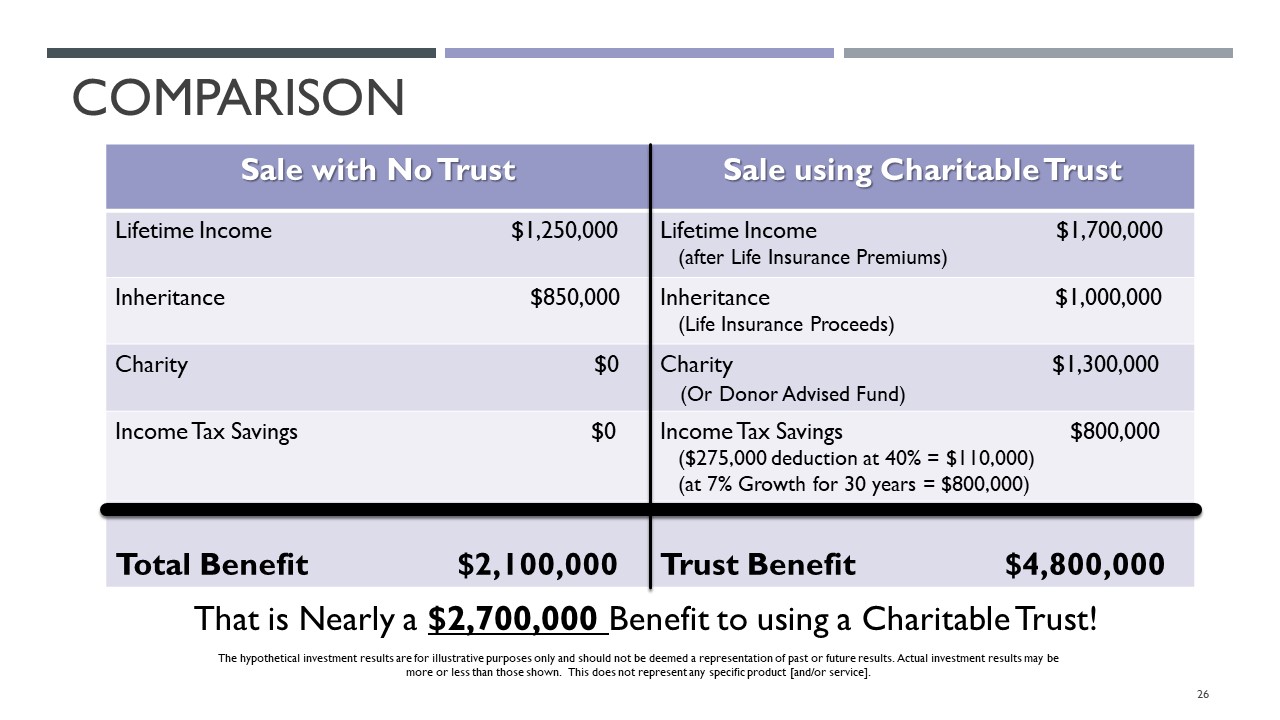

Now let’s compare both strategies in a chart.

On the left, we have a sale with no trust. On the right, we are utilizing a charitable remainder trust. The Legacy’s retirement income goes from $1.25 million with no trust to $1.7 million after life insurance premiums were paid inside the charitable remainder trust. The kid’s inheritance increases from $850,000 with no trust to $1 million with the trust. Charity or donor-advised funds receive $1.3 million from the trust.

How about the income tax savings? Recall that the $275,000 income tax deduction for the $1 million contribution to the charitable remainder trust creates tax savings at a 40% rate, or $110,000, that stays in the trust. That is money they can keep invested and growing for them. If that grows tax-free inside the trust at seven percent for 30 years, that is more than $800,000 in the trust.

The benefit of utilizing a charitable remainder trust with a $1 million asset is $4.8 million. The benefit of the same 30-year life expectancy without using a trust is only $2.1 million. That is a $2.7 million difference, which is significant. In addition, trust assets are free from estate tax assessment and are protected from litigation.

The one area this does not work well is if the donor were to die young. They will not get as much lifetime income if they do not live their 30-year life expectancy. There are some things we can do to work around that. You can do a charitable trust for up to 20 years or a lifetime trust.

Features and Benefits of Charitable Remainder Trusts

I love a charitable remainder trust because it allows you to leave a living legacy now that you can see and share with your friends.

Assets grow with tax-free compounding. There is some asset protection from litigation. The donor can be the trustee. The income payments can be based on life expectancy, a term of years, or both. There is an opportunity to set it up as a unitrust that pays out a percentage of the trust at the year-end value.

You can also set it up as an annuity trust which pays a stated dollar amount each year that does not change. Donors must take at least five percent distribution each year. The attorneys must draft the CRT document, and that adds cost. It works best with capital gains assets over $750,000 unless the donor does it for their actual charitable intent.

Another consideration is that the income tax deduction depends on how much remainder interest will go to charity. That is determined by the AFR rate, which follows interest rates. That rate is utilized in the calculation plus the length of the trust, which could be a term of years or life expectancy. How much income the donor wants to take affects the calculated future gift to charity, which is the amount that determines the income tax deduction today.

At least a 10% remainder interest must go back to charity. What is the highest amount of income a donor can take? It depends on the donor’s age. I had a donor in their early 80s who took out 35% a year in income. However, a 65-year-old cannot take out much more than eight or nine percent and keep the remainder interest intact. You must play with the numbers to get what the client wants.

There are administrative costs, and you do have to file a tax return. This is a tool that is best in a high-interest-rate environment. You can get a 30% adjusted gross income limit, meaning you can utilize a tax deduction of up to 30% of your adjusted gross income in one year. I plan to take the deduction the first year; however, you have up to five years to utilize your tax deduction if needed.

The Charitable Gift Annuity (CGA)

With a charitable gift annuity, we can get an income stream with no volatility dependent on the general claims-paying ability of the nonprofit organization for this income stream for life.

A charitable gift annuity is great for people nearing retirement. Most charities do not want to do this with anyone under age 65, as there is too much risk of needing to pay a longer lifetime income.

Let us walk through how it works. We have the donor with money at hand. They can make a gift of the asset to the charitable gift annuity. In return, they get a fixed income for life plus a potential tax deduction for the gift. They could save on capital gains taxes if this were an appreciated asset. The remainder will go to charity, like the charity remainder trust we talked about earlier. The income payments are fixed and do not grow with inflation. It does not matter what the charity does with the funds; they can invest them, but they are responsible for payments for life regardless of investment performance. The income is partially taxable. It can be on one life, two lives, or someone else receives the lifetime income. I have had donors who wanted to do a gift annuity with their parents receiving the lifetime income.

As mentioned, the charitable gift annuity can be set up with appreciated property. That can save on capital gains taxes. You can get a partial income tax deduction.

The AFR rate comes into play here too. There is a fixed rate for most charities. Some charities will give higher rates than the American Council of Gift Annuities suggests.

Happy people give. Giving helps people live longer. That is a risk for the charity because if the donor lives past life expectancy, they could run out of funds for the gift annuity. Some third-party nonprofits will assume this risk and pay the remainder to the charity for a fee. That is becoming more popular because charities want to avoid handling income risk and administrative duties.

Some financial or other advisors look at the charitable gift annuity rates and think they could do better for their clients with an investment annuity. I find a charitable gift annuity to be the most beneficial when the donor wants steady income and wants to leave something to the nonprofit organization in the future when they no longer need it.

Who likes the charitable gift annuity? Who does not like it? Charities typically do not like charitable gift annuities because it is a claims-paying liability. They must do the administrative work. Advisors realize the income is not adjusted for inflation. Other annuity opportunities could have higher payouts. Donors love these because some donors do not want to mess with the stock market’s volatility. They want to know if they get their check every month or year.

There are third-party, nonprofit, charitable gift annuity sponsoring charities which include community foundations and other private or public nonprofits that will insure the risk. They are proponents of it. You will hear many community foundations talk about charitable gift annuities.

SECURE ACT 2.0 allows a one-time gift of $50,000 to be made to a charitable gift annuity. Let us say we have a donor who is a 75-year-old female with retirement assets inside an IRA. The AFR rate for this illustration is 4.2%. She will receive $3,300 a year for life, which is 6.6%. After she is no longer with us, the remainder goes to charity. There is no income tax deduction because it is coming from her IRA. Her $3,300 will be taxed as ordinary income because that is how it went into the vehicle. Over her life expectancy of 17 years, she should get $56,100 from this gift annuity. Whatever is left over goes to charity.

We mentioned AFR with a charitable trust. With a charitable gift annuity, when we want a significant upfront deduction if not utilizing an IRA, we want to choose the largest AFR rate allowable. This would be for someone who does itemize. We can use up to the last three months’ average AFR. If we do this through an IRA, we want a low AFR in our calculations. That will lower the taxes on the income.

A charitable gift annuity is relatively easy to set up. It can benefit multiple charities. We can utilize a third party. It can be set up for life.

What are Pooled Income Funds?

Pooled-income funds are another type of charitable income vehicle. It is not part of the SECURE 2.0 Act. A pooled income fund is a trust created by a nonprofit organization. With a pooled income fund of over $1 million, many people or a family can pool their assets inside the fund. The funds grow through tax-free compounding, and donors receive income from the funds taxed as ordinary income.

Why have I yet to hear of pooled income funds? Why are we talking about them now? They were established in the tax code in 1969. All income comes out as ordinary income. Other tools can provide more tax efficiency and income. It uses a different calculation to determine the tax deduction. If the fund is brand new, the tax deduction in the first three years is even larger.

The income can come out for a family for multiple generations. The income only pays the gains in the account. We are hearing about these now even though other tools show more tax efficiency because some advisors use them for preferred partnerships, private placement life insurance, and other tools to make it more tax advantageous. That can get quite complex.

Key Takeaways

It might seem complex with CRT, CGA, QCD, and pooled income funds and the terminology. We need to work as a team as advisors.

If you have any questions, reach out to other advisors. Find a planned giving counsel near you. Talk to planned-giving professionals at your universities and hospitals. They are experienced in these tools. There are consultants like me, community foundations, or third-party nonprofits. If you ever need any of those, reach out to me. I will show you the best ones.

You can help your clients be a hero. You can guide and help them unleash their generosity.

- There are many ways to help clients generate income in retirement.

- Charitable strategies can provide income and fulfill client objectives.

- Charitable conversations can grow and enhance your client relationships!

- You are never alone; it takes a team to find the right strategies for the client to optimize their goals!

- It is not as complex as it seems!

I hope you took some things away from this presentation and discovered ways to diversify income through charitable tools and strategies.