Remember, we used to say to IRA owners and plan participants, “Name your young grandchild as your beneficiary, and if they have a life expectancy of 60 years, then the account can be stretched over a 60-year period because it can continue with a successor beneficiary.” Not anymore. That’s why you hear that SECURE Act 1.0 killed the stretch. No more stretch for the entire life expectancy of the original beneficiary if either the original beneficiary or the successor beneficiary dies after 2019.

Before SECURE Act 1.0, a 35-year-old beneficiary had a life expectancy of 50 years. Now they are only ten years, right? That is quite an impact. Congress said, “Listen, this is not your retirement account. It is just gravy for you. So, you should not be accumulating tax-deferred amounts for years.”

Now, I want to add a note of caution here. And there are many notes of caution that we need to add when it comes to IRAs. But one of the most important ones is not assuming that a particular rule applies to a beneficiary regarding distribution options if the participant or IRA owner died before their required beginning date. By the way, when I mention IRA owners, I also mean those with employer plans. But for ease, I am going to just say IRA owners. And if an exception applies to employer plans, I will also say that.

So, let us assume that the IRA owner died before 2020 and before their required beginning date. Many assume that the beneficiary is subject to the life expectancy option, but that is not necessarily true. That is the default provision under the RMD regulations. Still, the terms of an IRA or plan document could say that even though the life expectancy rule is an option, we will default to the five-year rule because we want to avoid them stretching the distribution over their life expectancy. So, you want to check for that for both pre-SECURE Act death and post-SECURE Act death. Post-SECURE Act death applies to a different class of beneficiary, which I will discuss in a second.

SECURE Act 1.0 also created eligible designated beneficiaries. Who is an eligible designated beneficiary? You are an eligible designated beneficiary if you are the surviving spouse of the IRA owner, a child of the IRA owner who has not reached the age of 21, disabled, chronically ill, or not more than ten years younger than the IRA owner.

Now, the status of the eligible designated beneficiary is determined at the time of the IRA owner’s death. Why is that an important distinction to make? Let us say, for instance, someone died today, and their beneficiary is not an eligible designated beneficiary. But tomorrow, that designated beneficiary was involved in an accident and became disabled. Are they eligible designated beneficiaries? No. Why? Because they were not an eligible designated beneficiary at the time of the IRA owner’s death.

But here is what I did for you. I broke it down into What if the account owner died before the required beginning date and died before 2020? What if they died after 2019? And if they died before the required beginning date?

So, here you have a high-level summary of the options. We know there are no pre-2020 rules for eligible designated beneficiaries because a new class of beneficiaries became effective in 2020. So, please use this table.

And here is something that you want to make a special note of. Compare the designated beneficiary option, right? It is the five-year rule or the beneficiary’s life expectancy if the account owner died before 2019 and before the required beginning date. As I said before, do not assume that one applies. Double-check to make sure, especially if you did not have the account and it is just coming over to you. You want to find out was the beneficiary subject to the five-year rule or the life expectancy rule? If the death of the account owner occurred on or after the required beginning date, it is the longer of the decedent’s or beneficiary’s life expectancy.

And you will see here on the SECURE Act 1.0 that it is just a 10-year rule. If they died before the required beginning date or over the beneficiary’s life expectancy, they can’t go beyond ten years if they died on or after the required beginning date.

Now, for eligible designated beneficiaries, if the account owner died before the required beginning date, there are two options: the beneficiary’s life expectancy or the 10-year rule. And if the account owner died on or after the required beginning date, it is the longer of the beneficiary’s life expectancy or the decedent’s remaining life expectancy. The options for non-designated beneficiaries, like estates and charities, remained unchanged.

Now, pay attention here. When I said for eligible designated beneficiaries, there are two options, right? The life expectancy or the 10-year rule. That is one of the traps that I talked about. Say Jane inherited her brother’s 401(k) account. She is 60; he is 65. That is not more than ten years younger. So, she is an eligible designated beneficiary. And now you are saying, “Oh, Jane, that is $500,000. You can stretch it over your life expectancy to help mitigate the income tax.” And then the plan administrator says, “No, we are not offering her the life expectancy. She is subject to the 10-year rule.”

What do you do in that case? You have Jane process a direct rollover to a beneficiary IRA where she can take distributions over her life expectancy. And that direct rollover must be completed by December 31st of the year following the year the participant died. So, that is one of the traps you want to look for and make sure your beneficiaries’ clients don’t fall into.

But here is what I did for you. I broke it down into What if the account owner died before the required beginning date and died before 2020? What if they died after 2019? And if they died before the required beginning date?

So, here you have a high-level summary of the options. We know there are no pre-2020 rules for eligible designated beneficiaries because a new class of beneficiaries became effective in 2020. So, please use this table.

And here is something that you want to make a special note of. Compare the designated beneficiary option, right? It is the five-year rule or the beneficiary’s life expectancy if the account owner died before 2019 and before the required beginning date. As I said before, do not assume that one applies. Double-check to make sure, especially if you did not have the account and it is just coming over to you. You want to find out was the beneficiary subject to the five-year rule or the life expectancy rule? If the death of the account owner occurred on or after the required beginning date, it is the longer of the decedent’s or beneficiary’s life expectancy.

And you will see here on the SECURE Act 1.0 that it is just a 10-year rule. If they died before the required beginning date or over the beneficiary’s life expectancy, they can’t go beyond ten years if they died on or after the required beginning date.

Now, for eligible designated beneficiaries, if the account owner died before the required beginning date, there are two options: the beneficiary’s life expectancy or the 10-year rule. And if the account owner died on or after the required beginning date, it is the longer of the beneficiary’s life expectancy or the decedent’s remaining life expectancy. The options for non-designated beneficiaries, like estates and charities, remained unchanged.

Now, pay attention here. When I said for eligible designated beneficiaries, there are two options, right? The life expectancy or the 10-year rule. That is one of the traps that I talked about. Say Jane inherited her brother’s 401(k) account. She is 60; he is 65. That is not more than ten years younger. So, she is an eligible designated beneficiary. And now you are saying, “Oh, Jane, that is $500,000. You can stretch it over your life expectancy to help mitigate the income tax.” And then the plan administrator says, “No, we are not offering her the life expectancy. She is subject to the 10-year rule.”

What do you do in that case? You have Jane process a direct rollover to a beneficiary IRA where she can take distributions over her life expectancy. And that direct rollover must be completed by December 31st of the year following the year the participant died. So, that is one of the traps you want to look for and make sure your beneficiaries’ clients don’t fall into.

Proposed RMD Regulations, February 24, 2022

Now, let us move on to the Proposed RMD Regulations published on February 24, 2022. If you called me on February 23, 2022, and asked, “Denise, what are the distribution options available to a designated beneficiary who inherited an IRA after 2019?” I would stand on the mountaintop with a microphone and say, “I will put my salary on the line that the options are the 10-year rule where distributions are optional for years one through nine until year 10, when the entire account has to be distributed. However, when the proposed regulations were published, the IRS said, “Well, you are only half right, Denise. That is true if the account owner dies before the required beginning date. But if they died on or after the required beginning date, the designated beneficiary is subject to a 10-year maximum where they must take annual RMDs for every year of those ten years.” The proposed regulations also relaxed the excise tax that applies to RMDs for the year of death, which is not taken by the end of the year. That excise tax is automatically waived as long as the RMD is taken by the IRA owners’ tax filing due date, plus an extension for the year of death. What does it mean to be ten years younger or not more than ten years younger? Because we know that traditionally when the IRS talks about ten years, they look at it on a calendar year basis, but when the proposed regulations were published, they said, “No, we are counting these things in days.” For instance, if Susie’s date of birth is October 1st, 1953, then Susie’s beneficiary is at most ten years younger if the beneficiary was born on or before October 1st, 1963. You might have to review any conversations with an eligible designated beneficiary classified as such because they were not more than ten years younger. If it is close, we need to go back and see whether they fit into that category, or did we exclude anyone that should have fit into that class of beneficiary? The “at least as rapidly rule” or ALAR applies to every beneficiary. Under ALAR, if the IRA owner was required to take RMDs at the time of death, then the beneficiary has to continue taking distributions at a rate at least as rapidly as the rate at which the IRA owner was taking distributions. This created quite a fuss in the industry. During the comment period on the proposed regulations, practitioners and taxpayers all wrote to the IRS and said, “Listen, so what you are telling me is that if I am subject to the 10-year rule and I am also required to take annual RMDs, I did not because of what you told me? Then what are we supposed to do now? Because by my reading of the regulations on the tax code, I now owe you 50% of the amount that I did not take because the language in SECURE Act 1.0 clearly said that I did not have to take it. But now you are telling me that my interpretation is wrong because SECURE Act 1.0 did not say that we should have taken into consideration.” The IRS said, “You know what? You are right. So, here is what we are going to do. If you are subject to the 10-year rule and you are also required to take annual RMDs, we are going to waive the 50% excise tax for 2021 and 2022 because those are the years that we feel have been impacted the most now that we are telling you know what steps you need to take going forward. So, for clients subject to the 10-year rule and inherited accounts in 2020 or 2021 who did not take RMDs for 2021 and 2022, there is an automatic waiver of the 50% excise tax. This also applies to successor beneficiaries, whose original beneficiaries took distributions over their life expectancy and died after 2019. And the successor beneficiary is subject to a 10-year maximum period during which they have to take annual RMDs.What is SECURE Act 2.0?

One of the biggest things that came out of SECURE Act 2.0 was the new schedule for the RMD age. When a client asked, “When am I supposed to start taking RMDs?” we would say the year you reach age 72, or if you reach age 70½ before 2020, we would say the year you reach age 70½. But now we have to take out our calculator and say, “Well, what is your date of birth?” Because, based on your data, your birth date will determine when you are supposed to start taking RMDs. So, let us quickly take a look at that. You ask your client, “Were you born June 30th, 1949, and earlier? In that case, you should have started for the year you reach age 70½ and continue for every year after that. If you were born July 1st, 1949, to December 31st, 1950, it is age 72. If you were born July 1st, 1951, to December 31st, 1959, it is age 73. And if you were born July 1st, 1959, and after, it is age 75. And right now, I know some of you are saying, “Denise, I think you made a mistake because you have 1959 in both the age 73 and the age 75 category.” And this time, I will tell you, no, it is not my mistake because that is precisely how it was written in SECURE Act 2.0. Now, it is expected that mistakes will be made when we have these new tax laws. It is a lot. And so there are usually opportunities for them to issue technical corrections. The good news is that we do not have to worry about this for some time because it only affects individuals born in 1959. But we expect the IRS to issue technical corrections to state the intent clearly. Individuals who reach age 72 in 2023 do not have an RMD for 2023. Why? Congress had to decide when to make this go live; when do we make this effective? SECURE Act 1.0 was passed on December 20th, 2020, and many provisions became effective a week later. SECURE Act 2.0 was passed on December 29th and became effective in some provisions immediately. The change in RMD rules was one of those, and here is how it affected some of your clients. IRA custodians must send out RMD notifications for clients who are supposed to take an RMD for the year. This only applies to inherited IRAs if the custodian wants to do that. But the obligation rests with IRAs that the individual owns, said and simple, as long as the custodian held the account on December 31st of the previous year. So, some custodians needed more time to change their system. So come January, those notices went out to clients who reach age 72 in 2023. Now, they should not have gotten those because of the new rules. They do not have an RMD for 2023. Here is the problem. Some of them are like me. When I get a bill, I pay it right away because I do not want to wait, get it, pay it, get the RMD noticed, and take the RMD. The problem is, now they are contacting their advisor and saying, “Listen, I took what I thought was an RMD, and now I am being told it is not. What should I do?” In that case, you can have the client roll it over. The rollover generally should be completed within 60 days of receipt. But this is one of those cases where they qualify for an automatic waiver under the self-certification option. This is explained in Revenue Procedure 2020 46, and most IRA custodians have a procedure for that. So, you contact the IRA custodian and say, “Listen, my client took what they thought was an RMD because you told them to. Now they want to put it back. It is past the 60-day deadline. How do we proceed?” But there is another issue. What if the client took a distribution from an IRA and rolled it over within 60 days? They can do that only once in 12 months. So, if your client already did an IRA-to-IRA rollover, they cannot roll over this non-RMD to their traditional IRA because they will break that rule. What do you do to help the client in that case? If they participate in an employer plan, they can roll it to the employer plan if the plan allows. If not, the only other solution is to roll it to a Roth IRA as a conversion. And right now, you are saying, “But Denise, that will be included in income.” It will be included in taxable income but would have been included if they did not roll it over. In this case, the difference is that it will go into the Roth, where it will grow tax-deferred, and eventually, the earnings would be tax-free. So, those are the two solutions. I hope the IRS comes back, looks at this, and says, “Let us just waive all the restrictions that apply to the rollover of this particular amount.” They did that in 2020 under the Cares Act. But we must not be complaining loudly enough about this, or maybe it did not affect enough people, so they do not hear the noise and haven’t done anything. So, for now, those are the only two options. And I am keeping my fingers crossed that they will provide some concession for these amounts. Under SECURE Act 2.0, spouse beneficiaries may now treat an employer plan as their own. If that sounds familiar, they can already do that with IRAs. But be aware of that terminology because with an IRA, when you treat it as your own, you can make your regular IRA contributions or rollover contributions to that account. This is only for RMD purposes, where instead of the single life expectancy table, the uniform lifetime table can be used to calculate the spouse beneficiary’s RMD on their own employer-sponsored retirement plan. This will be effective in 2024. How is this done? We have yet to find out. How do you make such an election? We are still waiting on the IRS for guidance. Understandably they need some time, but I suspect they will just piggyback off of rules already there. They still have a year or a half to figure that out because it is June. Hopefully, that is sufficient time. Now the spouse beneficiary has to make an election to choose this option. So, when your client converses with you, part of what you will say to them is, “Well, did you get some paperwork about the election options and which option did you choose?” And if the client says no, offer to get on the phone with them and we figure that out. So, that helps to protect your spouse beneficiary client by having them take a lower RMD than the RMD they would have had to take under the single life expectancy table. They can always take more. But with the single life expectancy table, they are locked into a higher amount. RMD aggregations with annuities are another huge change. Here was the problem with that. If you have multiple IRAs or 403(b)’s or multiple accounts under a 401(k) plan, you can calculate the RMD amount separately and take the total from one or more of those accounts, right? Be careful because you can only aggregate between traditional SEPS and SIMPLEs or between 403(b)’s or multiple accounts under the same 401(k) plan. You can’t cross borders. For instance, you cannot cross borders and aggregate 403(b)’s and IRAs. Right? Even though I said, using IRAs as an example, you could calculate the RMD separately for two IRAs, total the amount, and take it from one or more of those IRAs; however, you couldn’t do that if one were annuitized. And the problem for the IRA owners is that the annuity amount is usually so huge that it could cover the RMD for the regular IRA anyway. And by regular, I mean non-annuitized. But now, under SECURE Act 2.0, they can. There is still an outstanding issue because annuitized IRAs do not have an account balance. How are we going to figure out what the RMD is? For now, the SECURE Act 2.0 says, “Use your best judgment”, and we will be fine. So, use your best judgment if you have a client who wants to aggregate an annuitized annuity and a non-annuitized IRA. SECURE Act 2.0 also reduces excise taxes on RMD shortfall. I was talking about this earlier because the 50% excise tax was so steep, right? Someone should have taken an RMD for $50,000. They owe the IRS an excise tax of $25,000. Oh, man. So, now the IRS says, listen, or SECURE Act 2.0 says it is reduced to 25%, effective 2023. And guess what? It is reduced to 10% if corrected during a correction window. Great news. Now, let me tell you what I am hearing people say. Oh, because it is reduced to 10%, it’s unlikely the IRS will waive the excise tax if the deadline is missed. I don’t entirely agree with that because the language in SECURE Act 2.0 did not override the current language in the tax code that says you can request a waiver of the excise tax if the deadline was missed due to reasonable cause. So, unless the IRS comes out and says clearly that they are not accepting any request to waive the excise tax, regardless of why the deadline was missed, my recommendation is to soldier on for your client and file those forms. The IRS will likely honor the request to waive the penalty. The only time the IRS has denied a waiver request is when the form wasn’t filled out correctly. And everything was copacetic once the CPA brought it to me, and we helped them fix it. SECURE Act 2.0 also now allows for RMDs not to be required for designated Roth accounts. It made sense that Roth IRA owners are not subject to RMDs. So, why were Roth 401(k), Roth 403(b)s, and Roth 457(b)s – collectively known as designated Roth accounts – why were they subject to RMDs? It made no sense whatsoever. And they probably heard us complaining about that. They agreed, and now, after December 31st, 2023, designated Roth accounts are no longer subject to RMDs. Be careful, though, because if your client is supposed to take an RMD in 2023, their first RMD, they can take it as late as April 1st of the following year. That will be in 2024. However, that is not a 2024 RMD. That is a 2023 RMD. So, it does not qualify for this waiver.Distribution Options for Classes of Beneficiaries

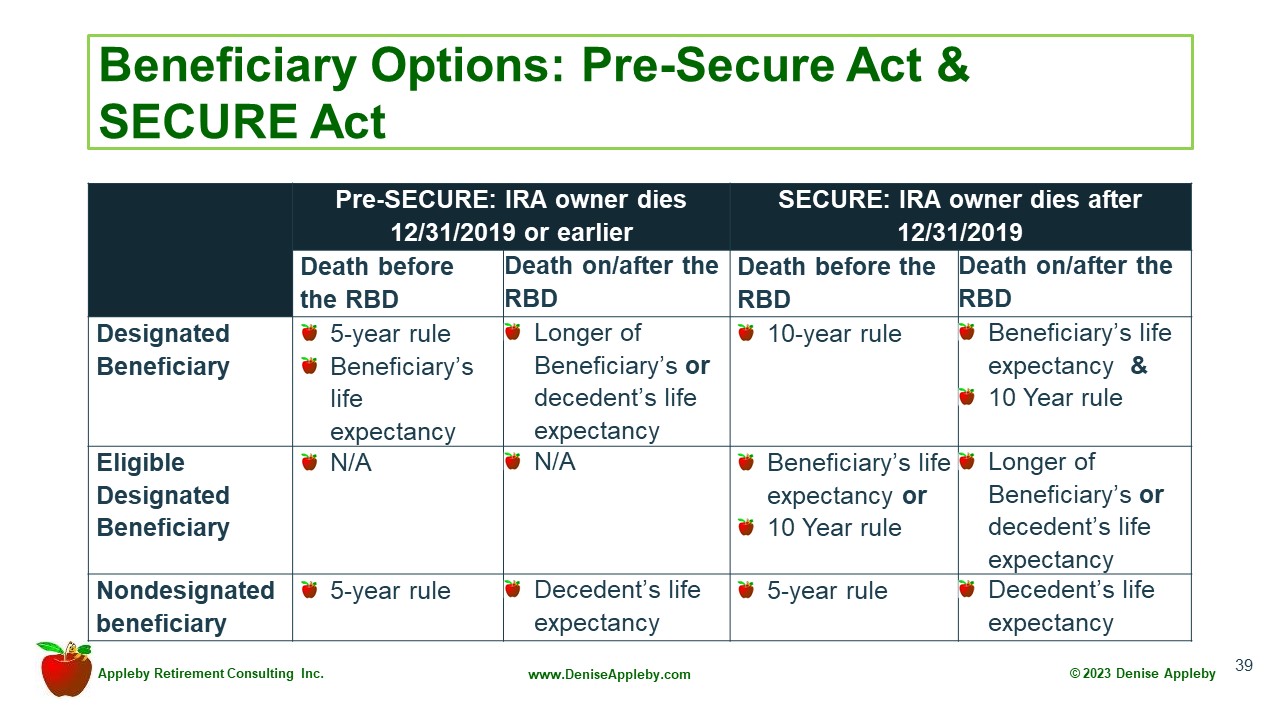

I am going to address distribution options now in more detail. And I want to remind you that for what we talk about here, everything will be separated into when the account owner dies before the required beginning date versus when the account owner dies on or after the required beginning date. For Roth IRAs, because there is no RMD for the Roth IRA owner, whether the Roth IRA owner dies at age 10 or 800, the rules are the same, right? Traditional IRAs are different. Now, one of the things you have to do when the client tells you they have an inherited account is to find out what class of beneficiary they are. We covered all of those earlier except successor beneficiaries. Who is a successor beneficiary? That is the beneficiary that is not the original beneficiary. You need to find out if your client is a successor beneficiary. One of the primary mistakes I see is an advisor or financial institution assuming that a beneficiary is a primary beneficiary when they are just a successor beneficiary. And when you make that kind of mistake, the RMD you tell them they must take is incorrect. The first thing you must determine when explaining the distribution option is whether the account owner died before the required beginning date. What’s the required beginning date? Earlier, we talked about the first RMD year. The required beginning date is April 1st of the year that follows that year for the IRA owner. Now, if they participate in an employer plan, the plan can provide that their first RMD year can be deferred past that year until retirement if they are eligible. If you have a client with a solo 401(k) plan, they are not eligible. Why? Because they would be a 5% owner. Anyone who owns less than 5% of the business is eligible for that deferral. And even if they are not, do not assume that they are because the plan does not have to offer that option. So, you want to tell the client, let us get on the phone, talk to your plan administrator, and find out if you can defer taking your RMDs past your applicable RMD age. So, what options apply to the beneficiary? You got to ask them a bunch of questions. And my recommendation to you is to create an intake sheet. Feel free to use some of the information that we cover here today. You want the date of birth and date of death of the IRA owner, the date of birth of the beneficiary, and the date of death of the beneficiary if the beneficiary died. Ask that question because that will help you determine if your client is a successor beneficiary. Is the beneficiary a spouse or any other class of eligible designated beneficiary? And were there multiple beneficiaries on the account? That could change the determination of whether the beneficiary is a designated or non-designated beneficiary. RMD for the year of death. If the account owner died on or after the required beginning date, you want to ask, “Well, did the owner take the RMD for the year of death?” Why is that? Because if they did not, it has to be taken by the beneficiary. And if the beneficiary misses the deadline, they are the ones who owe the IRS the excise tax or excess accumulation penalty. Now, that RMD is calculated as if the owner lived through to the end of the year. But here is good news. SECURE Act 2.0 acknowledges that when someone inherits an IRA, they think about things other than the deceit and take their RMD, right? And some IRA owners leave it to the end of the year to take it for different reasons. So, by the time they scramble around instead of the beneficiary accounts, et cetera, et cetera, it is well past the deadline. It is unfair to these individuals to ask for a waiver due to reasonable cause. And they agree. And in this case, they said, “Listen, the deadline is technically the end of the year, but as long as the beneficiary takes it by the beneficiary’s tax filing due date plus extension, there is an automatic waiver.” How do you determine the distribution options that are available to the beneficiary? Here is the first question that you ask. Are you the primary beneficiary? And if they say yes, you want to know, did the owner die before 2020? Did the owner die before the required beginning date? Is the beneficiary a non-designated beneficiary? Designated beneficiary? Eligible designated beneficiary? When someone calls me and says, “Denise, I have a client who inherited an IRA. He’s 59. What are his distribution options?” I am like, “What?” That is not even half of the information. There are ten more questions that I need to ask you because if I do not have the answers to them, we cannot even begin to give you the answer. Now this is a table here that I created. It is only a high-level summary. More details are needed to drill down. We may have a new webinar focusing on this table, which could fill an hour.

But here is what I did for you. I broke it down into What if the account owner died before the required beginning date and died before 2020? What if they died after 2019? And if they died before the required beginning date?

So, here you have a high-level summary of the options. We know there are no pre-2020 rules for eligible designated beneficiaries because a new class of beneficiaries became effective in 2020. So, please use this table.

And here is something that you want to make a special note of. Compare the designated beneficiary option, right? It is the five-year rule or the beneficiary’s life expectancy if the account owner died before 2019 and before the required beginning date. As I said before, do not assume that one applies. Double-check to make sure, especially if you did not have the account and it is just coming over to you. You want to find out was the beneficiary subject to the five-year rule or the life expectancy rule? If the death of the account owner occurred on or after the required beginning date, it is the longer of the decedent’s or beneficiary’s life expectancy.

And you will see here on the SECURE Act 1.0 that it is just a 10-year rule. If they died before the required beginning date or over the beneficiary’s life expectancy, they can’t go beyond ten years if they died on or after the required beginning date.

Now, for eligible designated beneficiaries, if the account owner died before the required beginning date, there are two options: the beneficiary’s life expectancy or the 10-year rule. And if the account owner died on or after the required beginning date, it is the longer of the beneficiary’s life expectancy or the decedent’s remaining life expectancy. The options for non-designated beneficiaries, like estates and charities, remained unchanged.

Now, pay attention here. When I said for eligible designated beneficiaries, there are two options, right? The life expectancy or the 10-year rule. That is one of the traps that I talked about. Say Jane inherited her brother’s 401(k) account. She is 60; he is 65. That is not more than ten years younger. So, she is an eligible designated beneficiary. And now you are saying, “Oh, Jane, that is $500,000. You can stretch it over your life expectancy to help mitigate the income tax.” And then the plan administrator says, “No, we are not offering her the life expectancy. She is subject to the 10-year rule.”

What do you do in that case? You have Jane process a direct rollover to a beneficiary IRA where she can take distributions over her life expectancy. And that direct rollover must be completed by December 31st of the year following the year the participant died. So, that is one of the traps you want to look for and make sure your beneficiaries’ clients don’t fall into.

What Options Are Unique to Spouse Beneficiaries?

Spouse beneficiaries are a very special breed. They have options that are not available to other beneficiaries. One of the traps you want to look out for is the 10% additional tax or early distribution penalty. Why is that? Because a spouse beneficiary, in addition to keeping the inherited assets in their account, can keep it in a beneficiary account. They can roll it over to an employer plan. And one of the mistakes I see often is, “Oh, I can put it in my account. Let us move it to my account.” Sometimes that is good, sometimes not so good. Why is that? Because if they put it into the spouse beneficiary’s account and the spouse beneficiary is under age 59½, then any distribution they take will be subject to the 10% early distribution penalty. You avoid that by keeping it in a beneficiary IRA because those distributions are death distributions and are automatically exempt from the 10% early distribution penalty. So, ask your client, “Oh, you are a spouse beneficiary. Are you under the age of 59½? Then you better keep it in a beneficiary account until you are safe. Then you move it to your account.” One of the questions for the spouse beneficiary is, “Do you want to move it to your account now?” And one determinant factor is was the decedent younger than the spouse beneficiary? And if so, did the decedent die before their required beginning date? Because in that case, then you can keep it in the beneficiary account until the decedent has reached their RMD age. Then you switch it to the spouse beneficiary’s account. I know that is a lot, but here is the objective. If they keep it in the beneficiary account, they can start taking RMDs once the decedent reaches their RMD age. But switching it to the spouse beneficiary account starts when the spouse beneficiary reaches their RMD age. And if the spouse is older, the surviving spouse is older, that date comes quicker. So, you want to push that off until as long as possible. Then why do you want to switch it to the spouse’s account when the decedent would have reached their RMD age? Because if you keep it in the beneficiary account, distributions would be taken over the single life expectancy option. If you move it to the spouse beneficiary’s account, the uniform lifetime table will be used, producing a lower RMD amount. There is now no 10% penalty on beneficiary IRA distributions. The single life expectancy option can be used, and they can move it to their own IRA. And RMDs, when they move it to their account, it is just like their own IRAs. Before the proposed RMD regulations, when could you move it to your own IRA? We used to say, “Oh, do not worry about that. There is no deadline on that.” Now, the proposed RMD regulation says there is a new deadline. The deadline is later in the calendar year when a surviving spouse reaches their applicable RMD age and the calendar year following the year of the IRA owner’s death. So, now we have a new deadline. But fear not, because if your spouse beneficiary client misses the deadline, they can move it using the rollover method to their own IRA. So, now we have to be careful how we move these accounts. Because sometimes it has to be transfers, sometimes it has to be rollovers, and we want to avoid running afoul of these rules, right? So, another item to add to your checklist. What is the anti-bait and switch provision? Well, here is what some people have been doing. Some people have been saying, “Listen, you know what? If the account owner died before the required beginning date, I will choose a 10-year rule.” Remember, I said the spouse beneficiary is an eligible designated beneficiary, or I said eligible designated beneficiaries could choose between a 10-year rule and the life expectancy rule, right? And the spouse beneficiary is an eligible designated beneficiary. So, some spouse beneficiaries and their planners have doing are, “Here is what you are going to do. You are going to choose a 10-year rule. And then later on, when you are supposed to start taking RMDs, you switch to your account and avoid taking life expectancy distributions.” So, you are gaming the system. And what many people do is when they come across these strategies, they talk about it in the big media, and Congress looks at the big media and says, “Okay, that is what you are talking about. Well, it is not going to happen under my watch.” That is why when you know these unique strategies, you keep them to yourself and do not talk about them in big media, right? So, because of that, they have this new provision that says if the account owner died before the required beginning date and you choose a 10-year rule and later choose to move it to your account. As a result, you avoid taking RMDs that you would have had to take had you chosen the life expectancy method. Guess what? That RMD amounts are not eligible to be rolled over. So, now you have some complex calculations that you have to do to make sure it is not included in the rollover to the spouse’s account.The Determinant Question and Answer

The determinant first question is, are you the primary beneficiary? The second question still is, are you the primary beneficiary? What if they say, “No, I am not the primary beneficiary?” Then clarify because sometimes a term like “primary beneficiary” doesn’t mean that to them. Ask, “The person who had the IRA originally – did you inherit it from them, or did they die and someone inherited it, and then you inherited it from that person?” This is the difference between a primary and a successor beneficiary. You want to use the correct terminology but take it further and explain what it means. Some consumers say IRAs when they have a 401(k) because they use the term IRA to mean all their retirement accounts, or they say 401(k) to mean everything. So, in those cases, we must say, “Well, give me a copy of your statement,” because trust but verify, right? However, if the client says they are not the primary beneficiary, we know they are a successor beneficiary. Now the question becomes, what distribution options are available to the successor beneficiary? Did the owner die before 2020, and what distribution options apply to the primary beneficiary? Because whatever applies to the primary beneficiary drives what is available to the successor beneficiary. Did the IRA owner die before 2019, and was the primary beneficiary taking distributions over their life expectancy? What if the primary beneficiary died before 2020? The stretch IRA rules still apply. So, even though they are saying the stretch is dead, it depends. If the IRA owner died before 2020 and the beneficiary died before 2020, and the beneficiary was taking distributions under the life expectancy method, then the old stretch rules continue to apply for each successor beneficiary, right? But suppose the IRA owner died before 2020, and the beneficiary was taking distributions under the life expectancy option and died after 2019. In that case, the successor beneficiary is subject to the successor beneficiary’s 10-year rule, where they have to continue taking annual distributions over the original beneficiary’s life expectancy. The account has to be fully distributed by the end of the 10-year period that follows the year of the primary beneficiary’s death. Now, we will also figure out whether the primary beneficiary was subject to the five-year rule if the account owner died before 2020 or the 10-year rule if the account owner died after 2019. Why is that? Because if you are talking to a successor beneficiary of an IRA owner who was subject to the five-year rule for an account that they inherited before 2020, you need to find out what remains of those five years because they cannot hold the account beyond those five years. The five-year rule still applies. Remember, 2020 was not counted under the five-year rule, right? If 2020 is part of the five-year rule, they have six years because RMDs were waived for 2020 under the Cares Act. Always remember that one, right? Sometimes, even when talking to clients, I must remember when doing my mental checklist. I am like, “Oh yeah, 2020 doesn’t count when we count the five years.” If the primary beneficiary was subject to the 10-year rule and let us say they die five years into that, then the successor beneficiary only has five years left. Now, some of you might be IRA custodians. For those of you who are offering to calculate RMDs for inherited accounts, you are doing a nice thing. People want to avoid calculating those amounts. They get anxious because of all the complexities. But here is what I see happening: many custodians who offer this service are not asking, “Are you the primary beneficiary?” They ask for the account owner’s date of death or birth, and what is your date of birth? They use that information assuming that the client in front of them is the primary beneficiary. What do you think is going to happen then? The calculation is going to need to be corrected. So, when you create your checklist, always include that question. If you have a relationship with the IRA custodian, be sure they include that information somewhere on their system. This means that IRA custodians now have to add to their system the room to collect that information where there is a checkmark that says this is not the primary beneficiary. Their system should spit out that calculation based on that fact.What Should Advisors Do to Plan for Beneficiary Distribution Options?

So, what are some of the things that advisors can do? What are some key takeaways? You will agree that we must create a checklist to develop a beneficiary profile. Otherwise, when the client says, “What are my distribution options?” You are just going say, “Come back and see me. Maybe I need to figure this out.” But if your client is sitting in front of you and you have that checklist, you can get all the information you need, and then you’d be more than halfway to getting the client the information they need. Look for opportunities for tax-efficient distribution strategies. For the spouse beneficiary, do we want to minimize distributions if there is an opportunity to do that? We want to ensure that the spouse beneficiary is not subject to the 10% excise tax by putting the assets in their account before they reach age 59½ if they might take distributions before age 59½. We covered the 10-year rule a lot. One of the questions is, should they wait until the end of the ten years? Many believe the proposed regulations changed our understanding of the rules when the account owner died on or after the required beginning date. My response is, “Well, let us discuss that your client inherited a million dollars. If this is a traditional IRA, do you want to wait until the end of the ten years to take all that? Because you are talking about a lump sum distribution of a million dollars plus earnings.” It may be best to spread it out. That is a conversation that should be had in partnership with the client’s tax advisor, where they are going to look at the client’s profile and say, “Listen, even though you have a minimum amount or no required amount for the year, it serves you best from a tax perspective to take X amount this year, X amount next year, and so on.” And if the client misses the RMD deadline, ask for a waiver if the deadline was missed due to reasonable error. The financial institution made a mistake; the client did not get their RMD notice, somebody was sick, and the client did not get to take the RMDs. There are many options. So, look for those opportunities and submit a request for a waiver of the excise tax, whether it is 50% before 2023, 25% now, or reduced to 10%.