It’s also very helpful to think about the mid and late phases of retirement. The mid phase is such a critical point. All these years they’ve been planning to be able to retire, and hopefully, they’ve achieved that objective with your help. But now it’s time to really start looking at a different kind of planning, and that’s planning for the later phases of life.

If clients that are in the mid phase of retirement, ages early to mid-70s, they’re probably still independent, maybe still very active and able bodied. It’s a period when they need to be thinking about, “What’s very important to me if in the future my health should decline dramatically? What do I want to avoid?”, which can happen suddenly or sometimes it can happen more gradually. “What are the discussions we need to be having now with our advisor, with our family members, doctors, and others to make sure that to the extent possible, there’s a plan in place for that later phase of retirement when health begins to decline?” Too many families in our society, and even many advisors, simply don’t address this in the capacity that they should, and it often leads to crisis types of situations within a family, scrambling to figure out the options. Siblings often have bitter disputes, and it’s just not a good situation.

A few years ago Merrill Lynch and Age Wave asked people over 65 about their biggest concerns about living a long lifetime. They said:

- Serious health problems

- Not being a burden on my family

- Running out of money to live comfortably

- Being lonely

- Not having a purpose

- Having nothing to leave the children and grandchildren.

The thing that is important in these survey results is that four of the six don’t have much to do with money. Furthermore, these four can be impacted in a dramatic way by where someone lives as they transition through the phases of retirement.

Retirement Living Choices

When we talk about the different choices your older clients have, there are really two overarching choices. The first is certainly to stay in their own home. Most people want to stay in their own home. You’ve probably seen the statistics that 80 to 90 percent of people say they want to remain in their own home, and there are some very good, perfectly understandable reasons as to why they would want to do that. The alternative if they don’t stay in their home is to move to some sort of retirement community.

What are some of the positives for staying in the home? If you were to ask some of your clients, some of the things you might probably hear are:

- My home is comfortable and familiar

- I have an emotional connection with memories of raising kids and grandkids

- It’s less expensive (though that is not always the case; it depends on the specific situation and the needs, particularly if someone has healthcare issues).

- It avoids the hassle of moving. For a lot of people, one reason why they never make a decision to look at some other options that could potentially be better for them in the long run, is that they don’t want to deal with their stuff.

- I don’t want to leave my home because I don’t want to lose my independence.

There is an awakening going on in our society right now, where people are starting to realize that maybe staying in the home isn’t always the best choice. Aging in the Right Place was written a few years by a professor of gerontology at the University of Florida. The title is a play on the term “aging in place,” which generally means staying in the home. The point of his book can be summed up when he says, “The concept of aging in place has become a mantra in recent years that might prevent older adults from seeking healthier and more holistic alternatives.” Another article in the New York Times a couple of years ago was titled, “At Home, Many Seniors are Imprisoned by Their Independence”.

Emotions are important; people need to feel good about wherever they live. But it’s also important to think about the practical, or even the impractical implications of things, such as:

- Possible home modifications, depending on whether there are stairs, the height of the cabinets, width of the doorways and hallways; things like that which may not be a big deal at all right now for somebody in that mid phase of retirement. For some clients, it may require significant modifications; for others, maybe very limited. I saw an article that a financial advisor had written about spending almost $200,000 renovating his mother’s home because she really wanted to stay there. Within six months or a year, she ended up moving to a skilled nursing facility. So even with all that money they spent to help keep her in her own home, she ended up having to move anyway. Then the house was not as marketable because of the modifications that had been made.

- Maintenance of the home. Interior and exterior maintenance can become quite burdensome over time and be an expense.

- The risk of social isolation. As people age, their mobility becomes more limited. Over time, the risk of social isolation for someone staying in their home is much greater than it would be in a community setting. How to maintain social engagement is important because social isolation has a dramatic impact on somebody’s health with everything from depression to heart disease. I just saw a study that mortality rates have increased 26 percent for those who are socially isolated versus those who stay more actively involved and engaged socially. It’s becoming a very big health issue.

- Maintaining purpose kind of goes along with that; everybody needs a purpose in life. With staying in the home, it’s important to ask what am I going to do to wake up every morning and maintain purpose, or find renewed purpose? What’s going to give me that sense of purpose in my life? A lot of times, where somebody lives can really impact that, and who they have around them.

- Transportation challenges. I think it’s a little too early to tell right now, but at some point, it will be neat to see what groups and ridesharing programs can help older adults that could make an impact. As it stands now, a lot of times when someone is unable to drive, that can lead obviously to less independence and not more independence.

- People need to consider how they’re going to maintain a balanced, healthy diet in their own home. I saw with my own grandmother; she tended to fix the same canned foods over and over, every day. It’s just not the best thing to do from a dietary standpoint.

- Delaying a move. A lot of times, people who want to say in their home end up having to move at some point because of a health concern, and the problem is that it becomes a needs-based move rather than a move made of preference. Usually, the person making the decision is not the person who needs to move. At that point, it’s usually a family member. It can become a very difficult situation, and the older someone is and the longer it is before they make a move, the more difficult it can be. It can be a very dramatic issue for them emotionally and physically. That’s particularly a problem in the case of couples. If one is independent, what happens if one of us has a stroke or heart attack and we need care, and the other one is still independent? How is that going to work? They might be separated.

- In-home care where a person stays in their home and brings in care. Of those who stay in their homes, about 90 percent of older adults are cared for by loved ones in this country. There are 44 million unpaid caregivers in our country, and they’re providing the equivalent of $300 billion per year for the care of loved ones. Up to 70 percent of unpaid family caregivers have clinical signs of depression. They have chronic health conditions at nearly twice the rate of non-caregivers. 50 percent of caregivers say caregiving takes time away from friends and family members. Many times, a caregiver must take time away from their own career. Maybe it’s even retiring early. It’s becoming a big deal in the corporate world right now; how do we deal with this growing trend where more and more of our staff are having to take time away from work to care for an aging loved one? Loss of wages also means that’s less than I can contribute to my retirement accounts, and it also can have an impact on Social Security benefits. When you take the present value of that loss of future benefits and wages, it comes to about $304,000 on average. So people may think it’s less expensive to have family help, but that the cost is getting indirectly passed on to the next generation in the form of lost wages and benefits.

Planning for Cost of Care and Access to Care

It’s important to keep in mind as you talk with your clients that there is a difference between the cost of care and access to care, and both need to be planned for. If we think about the cost of care, we know what care costs. Whether it’s assisted living, nursing care, in home care; we know those costs can be exorbitant in many cases. Many people end up on Medicaid because they have gone through assets paying for care.

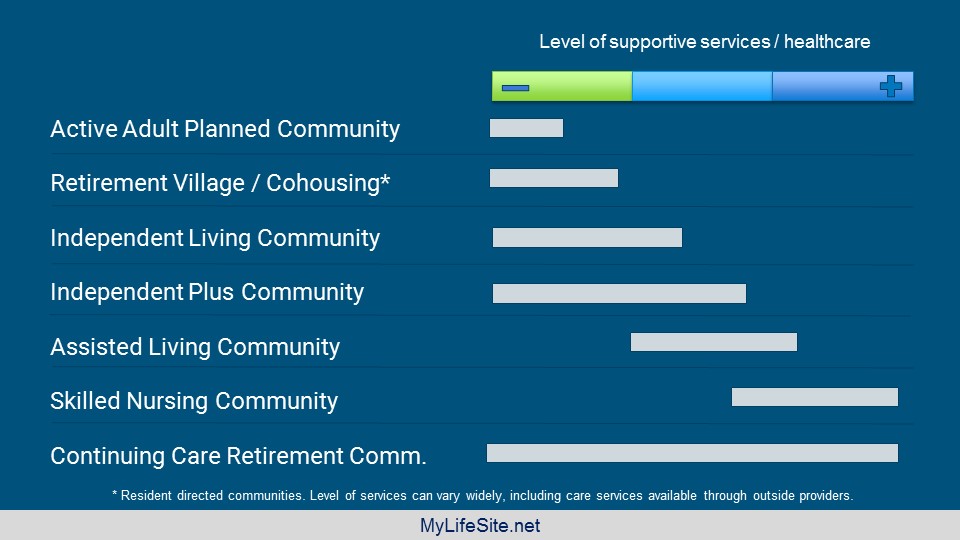

There is a broad spectrum of retirement communities. It is important to help your clients narrow down the choices and think about what’s often called the continuum of care.

On the top bar, at far left you’ll see a minus sign, the green section, that represents independent living. If any of your clients in retirement are they’re living on their own and maybe still very active, they would be on the far left of this scale. Then let’s say over time they start to develop some needs; maybe an hour or two of help around the house during the week. They then would be moving towards the right side of the green bar.

The aqua color in the middle represents assisted living. Maybe they need help with bathing, dressing, eating and other activities of daily living. Then as you move on across to the right, you really get into more advanced needs; maybe in some cases needs that can’t even be provided in the home, at least not practically. The far right would represent 24-hour skilled nursing care. This represents the full spectrum.

The reason this is important is that as your clients are looking at the different types of retirement communities out there, some providers focus on certain aspects of this continuum, while others may focus on other aspects. For example, an active adult planned community is a 55 and older development with clubhouse style amenities, maybe a pool, and maybe even a golf course. Residents own their home and everybody lives mostly independently. If a resident in a community like this develops assisted living or skilled care needs, it will not be equipped to provide for those needs.

Independent-plus are rental retirement communities. There’s a month-to-month rent that includes meals, some housekeeping, and other services. In some cases, it might provide personal care services in their own home if they need it. Others may even have some assisted living units onsite, and even memory care units. That’s also called independent-plus because they have independent living plus some assisted living or memory care.

But there again, if they have advanced healthcare needs, acute types of needs or skilled nursing needs, that’s not going to be available within those communities. At some point, somebody living in one of these types of communities may have to move again. That’s something important to understand because these kinds of moves can be difficult.

Then you have assisted living and skilled nursing communities, they’re not even retirement communities even though they’re often referred to as retirement homes. More and more people under 65 actually have to move into skilled nursing communities just for disabilities they have and 24-hour needs.

Lastly, continuing care retirement communities are unique in that cover the full spectrum; everything from independent living all the way to skilled care. Residents typically move in when they’re healthy or independent, and as time goes on if they need services such as assisted living, memory care, or nursing care, those services are available in one location.

Continuing Care Retirement Communities (CCRCs)

About 75 percent of CCRCs require an entry fee and are the only type that provides contractual priority access to the entire continuum of care. Many offer refundable entry fees or a declining balance contract where a person can receive some portion of that back if they move out within the first three or four years. If they’re living there for five, six, seven years or longer, no refund remains. CCRCs are normally considered higher end; usually, the services and amenities offered at a CCRC are going to be pretty nice compared to what you might find in some other places.

There are also monthly fees based on facility size, location, etc. Suppose someone needs assisted living for a couple of years starting in year eight, and then skilled care. Their monthly rate may not change dramatically. It can change for inflationary purposes; maybe there are some ancillary charges. But you won’t see a big spike in their expenses once they begin receiving care because they have a “life care” contract. A lot of CCRCs offer this. In many ways, it works like a long-term insurance policy. In other words, you’re prepaying for care that you may or may not need in the future.

To contrast that, other communities may offer something called a “fee for service” contract. So if we’re comparing two choices, one with life care and one with a fee for service, the client will pay less while living independently. But when they require care, costs will go up and they’ll pay the full market rate for those services. So they pay less now but then have unlimited exposure out of pocket when they need care later.

Which is the best choice? If you can tell me how long you’re going to live and how much care you’re going to need, I can tell you exactly which one to choose.

There are other CCRC contracts that are hybrids; it’s a modified contract where if I need care later, maybe I get that care at a discounted rate. Maybe I only pay 70 or 80 percent of the market rate for those services. Every community may have their own sort of contract and the way it works. But conceptually, you either pay more while you’re healthy and less later, or pay less while you’re healthy and more later.

Evaluating a Continuing Care Retirement Community (CCRC)

It brings peace of mind to people to know they have that extra support if they need it. Obviously, the community needs to be maintained or managed financially in a very prudent way in order to be able to do that.

If your client is looking at a continuing care community, there’s more that needs to be evaluated because it’s really a big commitment.

- Understand the contract details.

- The financial viability of the community is extremely important; how well managed are they financially? What’s their track record?

- What’s the business’ diversity, the diversity of their board, and so forth?

- How long have they been doing it? You can often get audited financial statements and review those, or have the client’s accountant review them. You want to make sure the community is financially in a position to meet the commitment to your client over the long-term.

- Is your client going to be happy there?

- Is it a community that’s going to help them live the life they want to live?

- Is it going to not restrict them or feel institutional, but help them maybe open a new chapter in their lives and experience new things?

- Can your client continue to do the things they want to do in that community and have a support network of new relationships? That’s very important.

- What is the quality of care that’s provided in that community, because your client will be depending on that healthcare? Visit their healthcare center; many people don’t like to do this but I think it’s important. Maybe if there are other families you know that have received services there, ask about their experience; would they recommend it?

- What’s their rating if they’re Medicare CMS (Centers for Medicare & Medicaid Services) certified?

Senior Living Planning Needs and Opportunities

How does this pertain to you as an advisor? What can you do? There’s a ton of opportunity here and so often people just don’t talk about this. For me to talk about it with my mother is difficult, and I’m in this line of work. It’s a very awkward conversation. You can have a big impact on a family. You can be a catalyst for really starting some important conversations. The nice thing is that it can also lead to more business.

If you bring this topic up with your younger adult clients, those maybe in the 45 to 55 year range, they may really like to know that you can help with this. That might lead to them bringing their parents in to talk with you, or maybe some other family members to talk with you because those may be conversations that they want to have but don’t know how to have them.

It is extremely valuable for advisors who work with retired clients to prompt the discussion and have a special planning session. I don’t know if I’d call it mandatory, necessarily, but maybe you can put a neat name or build a program around it for clients say, in their 70s and beyond that are still living independently. I’m talking about a one-on-one session, although starting with a group session may work as well.

Some of the things to ask clients during this session are:

- What concerns you about your future?

- What’s most important to you?

- Have you shared these concerns with your children?

- At this point in your life, what does peace of mind mean to you at this stage of your life?

- How is it different from what you might have said ten or 20 years ago?

- Is it your plan to stay in your home for the long term? Why or why not?

- What’s most important to you about that?

- What are some of the contingencies that we need to plan for if you do that?

- Have you thought about what you might do if your health surprisingly declines?

- What steps would you like your family to take?

- How involved do you want your family to be?

For those who want to stay in their own home, if that’s really what’s most important to them, then obviously you need to talk about all the things we’ve mentioned today. In addition:

- Will home modifications be necessary?

- Are they going to rely on their family members if they ever need them for care?

- Begin researching the quality of in-home care providers well advance in the need. Know which in-home care providers are more reputable, and even the local facilities that are nearby if they need that.

- If no family members are nearby, who will make up the support network? Who will manage their needs for them? Somebody else needs to be involved in this process

- What if staying in the home becomes impractical? What are some of the options locally?

- Is long-term care insurance already in place? Obviously, that can be a really big piece of the plan. If not, does a hybrid plan make sense; some type of accommodation, LTC annuity plan or something like that?

- Does it make sense to go ahead and secure a reverse mortgage? Doesn’t mean they have to tap into it, but go ahead and secure that line so it can be there, begin growing over time, possibly to be used in the future even to pay family caregivers.

What about moving to a retirement community? If they want to be somewhere where they can be taken care of if necessary, then:

- What type of care is available?

- How much does it cost? They need to choose an option they might prefer: an independent-plus community or a continuing care community and weigh the pros and cons of each.

- What is the plan if needs advance beyond what’s available in that retirement community? If they go to an independent-plus community and later need nursing care, is that a concern for them? What are some of the options there?

- Is long-term care insurance in place?

- If I’m going to move to a retirement community, it generally means selling the home, and that’s going to free up home equity that can be invested. Some portion of that can be used to cover the monthly fees, maybe for many years depending on how much equity is there.

With CCRCs, again a lot of times with the entry fee, you have that medical tax deduction that’s often available. Not always; obviously they need to consult with their accountant or CPA. But if they do qualify for a medical tax deduction on that entry fee, that might be an opportunity for a Roth conversion. If the entry fee is $200,000 or $300,000 – it could be all over the map – and I can deduct 30 or 40 percent of that, I can get a sizeable Roth conversion out of that in terms of protecting the tax liability on the conversion.

Key Takeaways

- You can be a catalyst for prompting important senior living conversations while also enhancing your practice.

- Staying in a home may not always be the best choice or the most practical choice and your clients need to understand that. At least help them to make a more educated decision and know what to plan for.

- Retirement communities are not all created equally; know what distinguishes one from another and what to look for.

- And finally, recognize planning needs and opportunities tied to the senior living topic and other closely related issues.