If it’s good for the government to put people into Medicare Advantage, it’s good for the carrier to get them to Medicare Advantage, and it’s good for the agent to get them to Medicare Advantage, it typically is not good for the consumers. It’s critical to understand that if you follow the money trail, you can understand better why it’s portrayed the way it is and why many people walk away with Medicare Advantage.

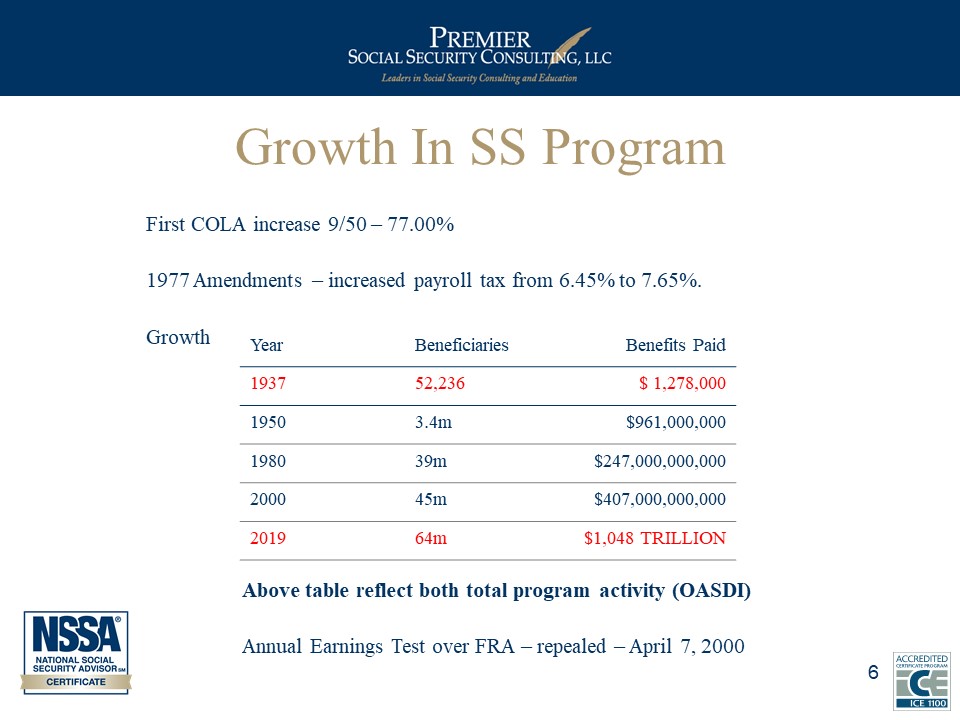

Since the year 2000, the number of beneficiaries has increased by about 19 million people. Still, the amount of money paid out has more than doubled from $407 billion to over a trillion dollars. So, it’s a huge program. It’s essential for many people, and it’s something that many people are going to depend on when they do retire.

Ida May was the first recipient of a monthly benefit of $22.54 in January 1940. She lived to the ripe old age of 100. It is a lifetime benefit, and people are living longer. According to the Social Security administration today, a male in his 60s has a life expectancy of right around age 84, and a female in her 60s has a life expectancy around age 87. The other thing they tell us is that about half of those people can expect to live to their upper 80s or early 90s, and a quarter of those folks live to be 95 or older.

Situational Social Security Overview

Regardless of their situation, people have different options available to them when they can start their benefits. Single folks probably have the fewest. We’re looking at 62, full retirement age, maybe age 70.

For married folks, we’re looking at a lot of different scenarios. Are they close in age? Are they far apart in age? What are their earnings? Is one a higher earner, and the other one was a stay-at-home mom or dad? Or are they both higher earners or one’s higher earner and the other middle income? So, there are all sorts of situations, which will determine when they will start their Social Security benefits.

In many cases, we’ll have public employees involved. In many states like Ohio, for instance, public employees have opted out of Social Security. They have their own retirement program, but many of these folks are still eligible for retirement or benefit from someone else’s work record. That public employee pension will affect those Social Security benefits.

For married couples, if one was born on January 1, 1954, or earlier, they can take advantage of the restricted application. The restricted application allows them to receive a monthly benefit payment based on their spouse’s record while they’re waiting to start their own benefit, be it at age 70 or whatever age they’re considering.

Minor children under the age of 18 can also collect benefits, such as a child still in high school between 18 and 19, or, and this may be the one that’s the most common, a disabled child. Suppose a child was disabled before the age of 22. In that case, they are eligible to draw benefits off of their parent’s work record, whether the parents are receiving retirement disability or that parent passed away.

You may have clients that are divorced. They may be able to draw off more than one ex-spouse, and they may change from one ex to another.

Your clients may be surviving spouses. They can collect from one or more deceased spouses or one or more deceased ex-spouses.

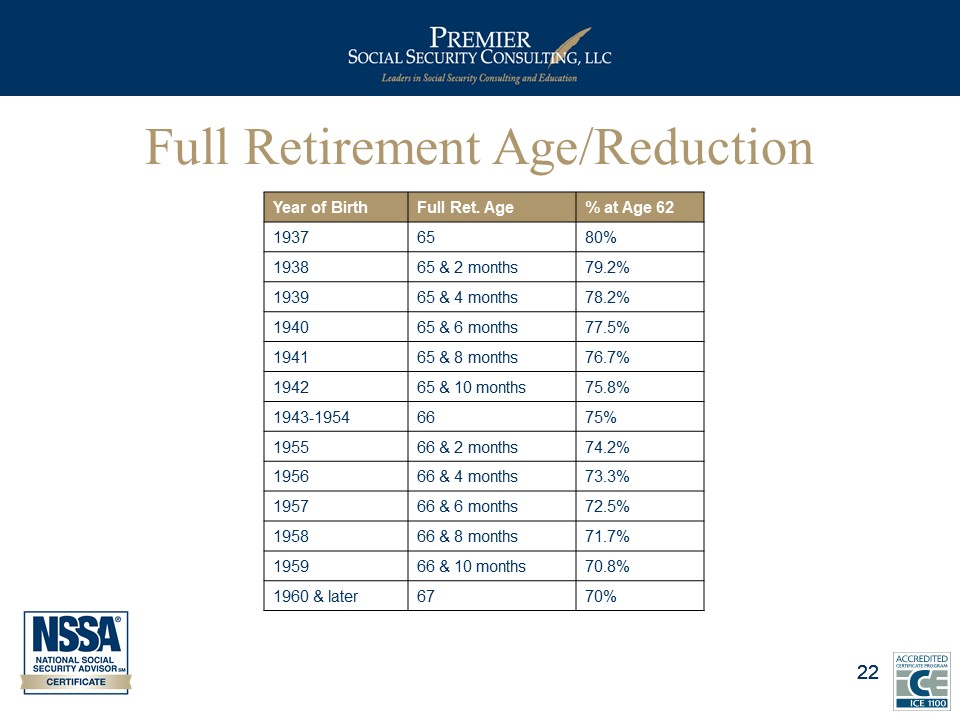

There’s also an opportunity to receive a nice lump sum check. Six months’ worth of retroactive benefits is available to folks after reaching full retirement age. If you have a client that is age 67 or 68, they can file for benefits effective six months prior and get a nice lump sum check. Full retirement age ranges from age 66 and 2 months to age 67.

How Can You Help Your Clients Maximize Their Benefits?

Remember that Social Security may be a joint lifetime benefit. Generally, upon the passing of the husband, the wife will step in his shoes. If he took benefits early, that reduction would last two lifetimes; if he waits beyond full retirement age or goes up to age 70, that increase may last two lifetimes also.

Can your clients file that restricted application? Are your clients single? Married? Are they survivors? Are there kids involved? Are your clients divorced? How do you coordinate your client’s spousal benefits? This is what we call thinking outside the box.

The restricted application must be in your Social Security toolbox for those born before January 1, 1954. The restricted application allows you to file off your spouse’s benefits, leaving your benefits to grow by earning delayed retirement credits. Let’s say I’m eligible for $2,000 off my work record. Let’s also say I can get $1,000 off my wife’s. I can file a restricted application at my full retirement age and collect $1,000 a month. Then at age 70, I turn my benefits on, which might have grown by delayed retirement credits from $2000 to $2,640 a month. So I’ve collected $48,000 in spousal benefits, and I’ve earned delayed retirement credits.

Strategies for married couples include:

- One spouse waits to age 70 to collect benefits. It very well could be both, but generally, it’s going to be the husband. Only about 4% of people wait to age 70 to collect their benefits. So, it’s not likely that all of your clients will wait to age 70, but more of your clients than the general public may wait to age 70.

- Maximizing surviving spouse benefits. The later the higher earner can wait from age 66 to 70, they can maximize surviving spouse benefits.

- Coordinating of Spousal Benefits.

If you have a married couple that might be five-plus years difference in age, maximizing surviving spouse benefit probably makes more sense. If you have a married couple where one was born by 1954, then the restricted application needs to be on the table.

You might have a married couple that is closer in age. If so, maximizing surviving spouse benefits may not be as important. If the wife is older than the husband, we’re probably not even looking to maximize surviving spouse benefits.

A married couple might have children you want to factor in, such as kids up to ages 18 or 19. A child may be eligible for benefits once a parent begins their benefits.

What is the Significance of Full Retirement Age?

People turning 62 this year, meaning they were born in 1959, their full retirement age is 66 in 10 months. For people who turn 62 next year, their full retirement age is 67.

Full retirement age is the age where you can collect 100 percent of what Social Security calls your PIA, Primary Insurance Amount, which is also 100 percent of your benefit. If you’re 62 or older and want to retire, they’re going to use your full retirement age, month, and year of retirement to determine how many months early you are applying for benefits. This will tell us how much of a reduction you’re going to see in your benefit amount. Also, if you delay past full retirement age, you earn delayed retirement credits, so your benefits will be increased. The number of months would be determined by the number of months you wait past your full retirement age.

Reaching full retirement age also ends the annual earnings test. The earnings test applies to folks who want to take their Social Security benefits, who are under their full retirement age, and who also work. But once you reach full retirement age, this earnings test will no longer apply to that individual, and they can work and earn as much as they want and still draw all their Social Security benefits.

Thirty-five years of earnings are used to compute your Social Security benefit. Social Security indexes those wages for inflation. They’ll bring all the wages you earned starting with that very first job you had at Wendy’s or McDonald’s through the year you attain age 59. They’re going to apply an inflation factor to that. This doesn’t mean your earnings starting with the year you turn 60 aren’t counted. They are counted, but just for whatever it is that you actually earned and not indexed for inflation. The return on investment for paying FICA taxes, folks, is generally very low, and many times it’s zero. So, don’t assume that if your clients continue to work while they’re receiving a benefit, their benefits will go up. If they go up, they go up by pennies or dollars, but they won’t go up by a whole lot.

This chart shows you the percent of full retirement age benefit you’ll receive at age 62. For your clients who are turning 62 this year, they would receive 70.8 percent of their benefits.

If somebody starts their benefits early, does their benefit go up to 100 percent at their full retirement age? No. The whole point was, if you take your benefit at 62, wait to full retirement age, or even wait till age 70, the amount of money you receive in Social Security on average should be about the same. Once you take a reduced benefit, it is permanently reduced.

Anytime you’re receiving a benefit before full retirement age, there’s a limit as to how much you could earn before Social Security withholds some of your benefits. This is called the Annual Earnings Test. At age 62, the earnings test is $18,960 a year. For every $2 you earn over that amount, you’ll lose $1 in benefits. If your clients lose benefits due to the earnings test, when they turn forward with time and age, Social Security will recompute their benefits and give them more money each month, so the benefits withheld are not really lost. You do get that money back over time. This annual earnings test goes away the month that you turn full retirement age.

Delayed Retirement Credits and Social Security

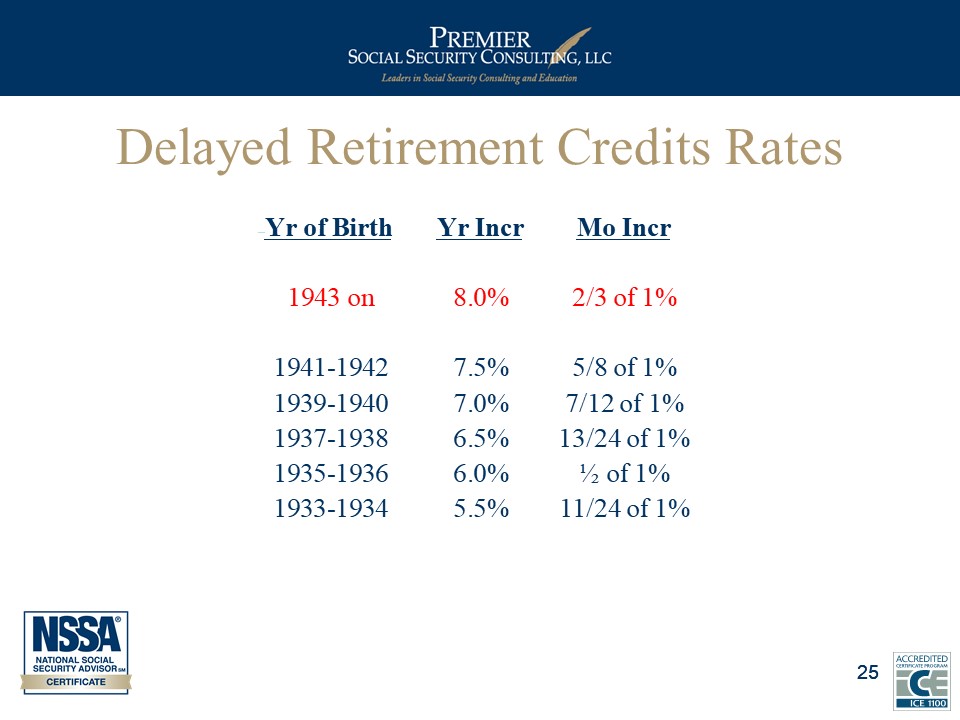

If you wait to collect your Social Security benefits beyond full retirement age, you get 8 percent more per year. This is a permanent increase in benefits. When you pass, you increase the survivor benefit as well.

You don’t have to wait till your birthday to get a percent more. For each month you’re beyond full retirement age, your benefits go up by two-thirds or 1 percent per month. So, if your full retirement age is 66 and you claim at 62, it’s a 25 percent haircut. If your full retirement is age 66 and you wait to age 70 to collect, you get 32 percent more benefits from delayed retirement credits. Waiting till age 70 from 62 is a 76 percent increase in your Social Security benefit.

Spousal benefits should be a primary factor in deciding when to claim benefits. For my wife to collect off my work record, she must be at least age 62. I must be receiving either a retirement or a disability benefit. I could be receiving a disability benefit at age 55. As long as my wife is age 62, she can collect off my work record as long as I am receiving a benefit.

What if I want to wait to age 70 to get those delayed retirement credits? Then she has to wait until I’m 70 to turn my benefits on before she’s eligible for a spousal benefit off my work record. How much are spousal benefits? It’s 50 percent of the PIA. The PIA, the Primary Insurance Amount always equals what you would receive at your full retirement age.

Divorced Spouse Benefits

There are a couple of categories of divorced spousal benefits. For the first one, Social Security wants to know if you are single. If you’re married, you cannot draw off from benefits based on your ex-spouse. But if your ex is married and you’re not, you can still draw off of them if you are age 62 or older. You had to be married to your ex-spouse for ten years or more. This has to have been continuous, with the only exception being if you’re divorced in one year and remarry that same person by the end of the following year, they’ll disregard the divorce. But otherwise, it’s got to be continuous. Your ex-spouse also has to be receiving either retirement or a disability Social Security benefit.

There’s a second category called the Independently Entitled Divorced Spouse. A lot of the requirements are the same. You still have to be single. You still had to be married to your ex for ten years or more, but now both of you must be age 62 or older. If you’ve been divorced for two years or longer, you can file on your ex-spouse’s record, even though they haven’t applied for Social Security benefits. So, if your ex is still working and has no intention of applying for Social Security benefits anytime in the near future, you could still draw off of their work record and receive an ex-spousal benefit.

Surviving Spouse Benefits

Widows, widowers, and surviving divorce-spousal benefits are available. You will receive one hundred percent of what the deceased was receiving or eligible to receive when you reach your full retirement age.

If you file at age 60, it doesn’t matter your full retirement age; you take that 28½ percent reduction. You can take the survivor spouse at 60, switch to your own benefit at age 62 if it’s higher, but you could also wait through your full retirement age. You can even wait as late as age 70, earn your delayed retirement credits, but still, in the meantime, you have money coming in.

Now, if the survivor benefit is the higher of the two, you can take your own at 62, taking a reduced retirement benefit. Then at your full benefit age, switch to the survivor benefit and still get 100 percent of what the deceased was receiving/you’re eligible to receive. The one thing that people need to keep in mind when they’re thinking of these situations is that the earnings test does apply. So, if the individual wants to file for survivor benefits at age 60 or their own benefits at age 62, if they’re still working, they will have to be aware of the earnings test.

It is actually possible to draw the widows, widowers, and surviving divorced spouse benefits as early as age 50 if you become disabled within seven years of your spouse’s death. The 28½ percent is still the maximum reduction. But if you wait until full retirement age, you’ll receive one hundred percent of the benefit. Now we call it full benefit age. There is a difference between full retirement age for retirement and widows and widowers benefits.

Key Takeaways

- Everyone’s Social Security situation is unique and different. We want you to know the main rules and strategies for single, married, divorced, and surviving spouses. Understand the questions to ask to open up opportunities. You need to ask the right questions.

- The biggest question that we went over that you need to ask is, “When were you born? By 1954?” Then you know, the restricted app is available to you.

- Learn the language of baby boomers. Understand that if you want to connect to baby boomers, understand that Social Security is their universal language.

- Ninety percent of recipients do not maximize their benefits. They have no clue what their options are.