I wrote about the snowbird concept in my column in Forbes in 2020. The three things I get into in that article is deciding where you will locate. Where do you want to go: Florida, Texas, Arizona? Those are the three traditional ones because they are southern, and there is no income tax. However, you now see Tennessee, North Carolina, and people still go to California. Some people do the opposite, where they have a lake cabin in Minnesota. We see a lot of that in Des Moines.

So, where is your location? Are you going to buy or are you going to rent? Is this for business or pleasure? We are mainly talking about people who are retiring and want to live in two places: one that is close to the kids and one that does not have as much snow.

The concept of renting is an option. I am not going to get into a second home as an investment. The idea here is for people who want to live in two places.

The ”How” Versus the “Where” of Snowbirding

The first consideration is: Do you own, or do you rent? Particularly, if you are going to own it, how do you finance it? A big topic that people think is simple is how to establish residency. “Well, you stay there six months and one day.” That is not the answer.

There are additional expenses and financial management that come with having a snowbird home. There is budgeting that needs to happen to make it work right.

It may not seem as apparent as it is, but you should think about healthcare because you are talking about people as they are retiring. They are probably in their age 60s or 70s.

There are also estate planning consequences that come from having a snowbird home, as these people are not spring chickens. They really must think about the eventual estate issues.

Also, where do you need your advisors to be? How do you work with your advisors?

Finally, what things do you need to think about in case you will not be living in two places for the rest of your retirement because you have a disability or some other issue?

For example, say your clients are Jan and Dean Beach. Let us say they are both 64, and they have been living in a lovely house in Chicago that is near family, such as kids and grandkids.

The situation is that Jan is retiring this year. Dean has a job where he can continue his job remotely. They have been saving to be snowbirds. They would like to spend seven months a year in a Florida condo, enjoy the good weather, and then come back in the summer to enjoy the pleasant summers in Chicago and see the kids and grandkids. They would be happy to do that in a condo; they do not need the big, drafty house anymore.

When they come to you, their concerns are what you would expect. First of all, “You are my financial planner. Do we have enough adequate finances to sell the big house and then purchase a condo in Florida and a condo closer to downtown Chicago?” Secondly, “Do we have the cash flow?” In other words, “Can we carry these two residences without cutting into our retirement plan because we do not want to enjoy this and then run out of money too soon.”

Now, let’s take each of those topics I brought up earlier and break it into more detail. “Do I own it, or do I lease it?” Maybe Jan and Dean are thinking, “Well, maybe we are going to own one and maybe lease one.” What are the advantages and disadvantages?

The advantage of leasing one of those residences is that you do not have maintenance and repair. If something needs to be worked on, you get a hold of the landlord and the property manager, and that is it. Second, you do not have a mortgage. Who wants to take on a mortgage just as they are going through the process of retiring and losing their human capital? It is an easier exit. If it does not work out and we do not like it, or we become frail, it is not that hard not to renew the lease.

However, there are disadvantages to leasing. One is that they want to establish a legal domicile in Florida. Why do they want to do that? Because the state taxes and income taxes are much lower than in Illinois. So, they would purchase in Florida and lease in Chicago if they really wanted to establish a domicile for income tax purposes. Otherwise, the Revenue Department of Illinois would like to dispute that.

Second, cash flow and equity issues. Meaning if you lease it, you are not leaving the legacy. In other words, you are paying all this money, and you do not get anything for it, versus if you bought the condo and it has the opportunity to grow. This could be something that you could leave to the kids or grandkids as part of your legacy. You cannot do that if you lease it.

This is a good question to ask your clients, mainly because, at first, many might be inclined to think, “Well, you know the way I am going to pay for this is to rent it when we are not there.” Okay, but is it going to feel like home? This is just a rule of thumb, but if they are going to spend more than, let us say, two months out each year, do they want to set it up in a sterile mode so they can do a Vrbo, or that kind of thing? This is the big picture.

You could test drive. My job is such that I can work anywhere. So, for four years, we went to Florida. The first two years, we spent a month in St. Augustine, Florida; we loved it. We do not have anybody come to visit us because it is already too crowded. We stayed for January for the first two years. The following two years, we stayed for January and February. That was when my wife finally said, “Why do we not just buy something?”

Now, let’s compare leasing to owning. In our case, we own both. There are many advantages and some disadvantages. The advantages are certainly state and homestead. When you buy in Florida, you get to homestead without state income tax. Florida is very favorable on homestead rules. I know some other states, but it would be a consideration for Jan and Dean because they are talking about Illinois with an income tax and Florida without one. I do not know the homestead rules in Illinois, but I know the Florida ones are favorable.

Equity: obviously, you are building up something that you may want to leave for your kids, eventually, and that is your legacy that you are leaving. That could even be a condo. I have seen that in the complex we are in. Some people will leave their condo when they pass on, and the kids are excited about that. It is a great chance to get a foothold.

There are disadvantages or, at least, challenges. You have the issues of maintenance and repair costs. That is very real to someone in their 50s, 60s, or 70s because I was never any good at it. Some people watch HGTV and think they have it all figured out and will repair it. Notice that many of those people are in their 20s, 30s, and 40s, not in their 60s and 70s. So, do you really want to do that?

Then, finally, you have the exiting issue. What happens when you exit either because of frailty, you go into a retirement home, or because you die? How do you deal with probate and some of those things? This can really complicate the situation and be a burden on your kids, but if you handle it right, it can be dealt with. However, if you do not handle it in advance, that is a disadvantage.

One of the most significant disadvantages is how on earth will you afford it? How are you going to finance it if you are going to buy it? You have the embedded cost of moving retirement growth assets to home equity when you buy a place. If Jan and Dean have built up $2 million in net worth and then cut out $300,000 for a place in Florida, can you treat that as a retirement asset anymore? In other words, if you are taking out a systematic withdrawal of four percent a year, you are now taking four percent out of the equity of your newly purchased condo. You are moving some retirement capital if you are financing your own deal; you are cutting into your own capital.

So, you could do a mortgage. There is a good case against not doing this now that mortgage rates are the highest in 20 years. Something that we teach at the RICP program is, in many ways, that a mortgage in retirement is a negative bond. What we are saying is that each year, you are essentially paying seven percent on the mortgage (so you are the bond), and the bondholder is the bank. You are paying them seven percent each year, so you need to make seven percent on your other assets. Otherwise, you will lose on the deal. You need to make seven percent on your retirement capital to be there, and you may be at a stage of life where you want to be in a situation where you are minimizing your risk.

So, if you were able to get rid of a mortgage or not take on a mortgage in the first place, like in this case, it is like a seven percent, risk-free asset. In other words, before, you had this obligation to make seven percent of your money, and now you do not because you are not paying a mortgage, so that is risk-free. Think about this negative bond; it is not a good time in one’s life to do it.

Some will say. “Oh, well, yeah, but the interest is tax deductible.” Let’s do a reality check. First of all, you are not working, so your income is at a lower level, so it is not as big of an issue. Second, so many people will take the standard deduction because, at 65, you get an increased standard deduction. If that’s the case, you do not need the mortgage deduction.

The kind of mortgage that could work is a reverse mortgage. That could be a financing tool and where it fits. You can only do a reverse mortgage if you are 62 or older; they are meant for older people. People sometimes need to understand that there is a reverse mortgage for purchase. This is not where you take out a reverse mortgage against the equity of your home, and it pays you like an annuity payment. This is where you take equity in your home and use that to finance a purchase or to pay off a mortgage. You will have the challenge of upfront costs and maintenance expenses, and you must keep the place up. You would, presumably, do that anyway.

Reverse mortgages are great as a long-term financing tool. They are not suitable for a short-term strategy because you must pay some upfront costs. For example, let’s say Jan and Dean could get $600,000 for their home in Chicago, and they want to buy a $300,000 condo in Chicago and a $500,000 condo in Florida. With their $600,000 in proceeds, they pay all cash for the Chicago condo. Instead of paying all cash for the Florida condo because they do not want to cut into any more of their retirement capital, they use the remaining $300,000 as a down payment on the Florida condo and use a reverse mortgage for purchase to finance the remaining $200,000. Sometimes, people have a hard time wrapping their heads around this, but what you are doing is instead of making mortgage payments on the $200,000 as you would for a conventional mortgage, you are paying off the remaining $200,000 out of the future value of the condo. That is certainly a doable idea, and it can apply to many people in the right situation.

By the way, you have to be careful at the tax level to make sure that you file timely so that you get the income tax exclusion on the gain of the primary residence, which, because they are a married couple, would be $500,000, you want to make sure you do that.

How to Establish Residency in a New State

This is a topic that I find interesting. People say, “You must live there for six months and one day, right?” It is more complicated.

I learned this ten years ago when I was asked to speak for a well-known high-end or high-net-worth broker/dealer. They were having a fancy lunch at a fancy steak place for potential clients. I was speaking about general retirement planning concepts, and the other speaker was a Florida attorney who covered how to establish residency.

How do you prove to the state that you are no longer in full-time, like New Jersey, New York, Illinois, California, or all of those with some taxes, so they do not come in on audit and say, “Oh, no? You do not only have to pay for your new residence; you have to pay us as well!”

Here are the things you would need to do to prove residency. Get these all prepared in advance, so if they give you the call, you shower them with paperwork, and they will leave you alone. With Jan and Dean, if they decide that they are not going to do a reverse mortgage and they are going to lease one of them, you would want them to own the one in Florida.

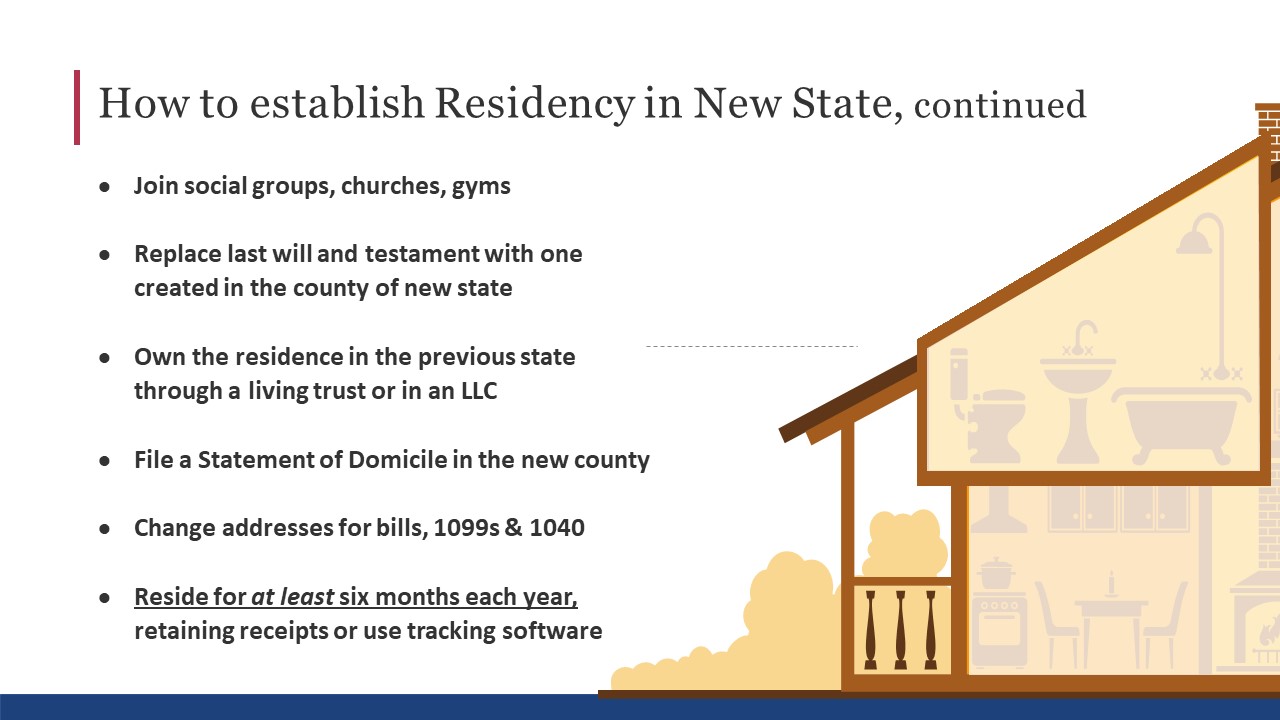

Change your car registration, your license plates, and your driver’s license. So, during the pandemic, that was one of the first things we did when we moved down to Florida because we wanted to get the clock ticking immediately. The other obvious one is voter registration. Be careful because everyone is so sensitive about where you are voting these days. Make sure you get voter registered in the new residence, domicile, wherever you are, and then, obviously, do not double vote.

What do pets have to do with it? Well, the reason this is important is because of a very noted case that came out a few years ago. A fairly wealthy person was establishing a move from New York to Texas. They were going through all of the kind of stuff that I am talking about right here, but the judge very clearly in the opinion noted that the person had registered his beloved dog in Texas. He commented, “Wherever the dog truly is is your domicile.”

If you are going to work part-time or volunteer, do it in the new state. Let’s say Dean is still going to work. He should make it clear with all his business stationary or cards and that kind of thing; they should carry the Florida address so he can make it clear that is where he is working as well.

If you have a client that still owns an operating business, maybe in the other state, you have to review how that works. You must show that they are just investors or can do this remotely, and the local managers can handle it. If you run into this, you should get the help of the local estate planning council.

Otherwise, for people who have built up some high net worth, the Californias or the Illinois’ of the world are going to go after you saying, “Well, yeah, you did all that other stuff, but the fact is you still own this business that pays most of your bills and that is in our state.” So, you have to be careful.

Join social groups, churches, and gyms. It is obvious, but that is just more and more indicative that if you get attacked by the old state, you got it, and that way, you do not have to go to court. Here’s my proof.

Here is an important one: you want to replace your last will and testament with one created in the county of the new state. You want to do that irrespective of duking it out with the state authorities because your will will be probated where your true residence is. So, that is something that you should do anyway, even if you do not have a state that wants to charge you income tax.

We are on the 5th floor of a high-rise in Des Moines. I looked at the ownership of the different people there. More than 50% of condos are owned through a living trust. You could do a living trust in both states, but you particularly want to have it in the state you are moving from.

In Florida, you can file a Statement of Domicile in the new county. We filed a notarized Statement of Domicile that we want to be in that county, and that is our residence, and that is where we will do our homestead.

Now, the state you are coming from might say, “We do not care what Florida’s opinion is; we are telling you that you are not.” But by having that and saying, “Look, we filed this, so why are you bugging me a year later? We have proof.”

I missed this one. My 1099 still showed up as being in Iowa. I had not changed those to indicate that my address was Florida versus Iowa. Indeed, on the 1040 you file the following year, you want to show it as the new state.

And finally, reside for at least six months each year in the new state. The six months is not hard and fast; obviously, if you are there more than six months, you have proven to the world, “Well, that is where we spend most of our time.” So, what do you do? You retain your receipts or, more realistically, take your Visa bill and that kind of thing to show, “Look, I spent money at such a restaurant starting in October and went through May.” That will help indicate six months.

Expenses and Financial Management

What about transportation: are they going to fly back and forth? Are they going to drive? What are they going to do? They also have to maintain both households, even not being there.

Smart apps allow you to change things like your thermostat and Ring cameras so you can check to make sure the home is in good shape. However, it would be best to have a Wi-Fi connection in both places to pull that off. Wi-Fi is not free.

You’ll have property taxes on two homes and homeowners’ insurance that can be higher in the non-six-month state because that is not your primary residence. We discovered that many property and casualty insurers charge more because they worry you are not there to monitor water and mold if you did not put the air conditioner on low enough, etc.

If you have two condos, your homeowner’s association fees are high, so as long as you budget it, fine. If you do not have an HOA, then you pay separately for lawn care, snow removal, security system, your Ring cameras, or ADT home security. Then, property management, especially if you are one of those who will rent one of your residences while you are gone, to help cashflow some of this. You might also have to pay for property management to come in, check it out, and prepare it for renting out on Vrbo.

Just as an example for us, in Des Moines, we did have someone who cleans the building come in once every two weeks and flush the toilets and run the water because these are old pipes and, otherwise, they can get stiff if you do not run water.

Healthcare and Two Homes

The big question is on healthcare insurance: do you have original Medicare, or do you have Medicare Advantage? In many cases, if you are going to live in two residences, it might make more sense to use original Medicare. Because if the Medicare Advantage program is geographically centered in a place, the copays and deductibles for out-of-coverage care could be very expensive.

Also, you must consider your part D pharmaceuticals because will you have the same pharmacy? So, you could do it through a local one in Chicago and a local one in Florida. Is that going to work with your part D, or do you go the mail-order route? They all have solutions, but you have to think through it.

One thing I want to point out is that sometimes people under-budget for their Medicare costs. Your clients who make more than $246,000 a year will pay twice the Medicare Part D and Part B premiums than someone who makes less than $194.000. For example, a couple making less than $194,000 might, for Medicare purposes, budget $2,300, whereas if they are making a quarter of a million, they might have to budget $4,700.

When you are budgeting for healthcare, you have got to think it through. Let us say Jan and Dean are making $200,000. Their Medicare Parts B and D are $3,294 a year versus $2,357 if they made less than $194,000 (the income-related monthly adjustment amount (IRMAA)). Between the additional premium for Medigap Plan G and out-of-pocket expenses of $2,800 a year, it totals $7,700 per person or $15,000 a year they should budget for healthcare. If they plan for a 30-year life expectancy, you are talking about more than $400,000 spent on healthcare during their retirement. Fidelity does an annual study that puts that total around $300,000, but that is ignoring the fact that some people die early, and wealthier clients tend to live longer. These numbers don’t include long-term care, caregiving, transportation, or catastrophic events.

Estate Planning and Snowbirds

First, you want to get your property title right. I teach a course on estate planning, and people need help understanding. For example, Florida has tenancy by the entireties, Iowa does not. If you go to Arizona or California, you talk about community property. You know, how are you titling it, and where will it be your domicile? If Jan and Dean say Florida, they must get a will there.

My wife and I have executed powers of attorney in Florida and Iowa. Now, interestingly, Florida does not allow for springing powers of attorney, and Iowa does, so we have a safe that we carry back and forth in our car. We keep the Florida documents in one place and the Iowa documents in another so that if one of us had to go to a hospital, the other could take a power of attorney from that state. It is not like a will where you can have a will in only one place; you can have powers of attorney and your living wills in multiple places.

You want to have probate only in your state of domicile. So, if you have a place like Jan and Dean in Illinois, they should put that condo in either an LLC or a living trust so that when they die, their kids do not have to hire an attorney to go up to Illinois and probate it. That is important.

Be aware that states like California and New York will chase more high-net-worth people around over the issues of their state taxes. So, you want to have all your documentation where your residence is for that reason, too.

For advisors, this is your opportunity to either turn this into a good thing or a bad thing. If you can show them how to have an online meeting with you, then they will stick with you. You will need to expand your knowledge. Still, you could be the advisor in Illinois, learn a little bit about Florida so that you can, at least, talk in general about it, or certainly if they move to a community property state. You do not have to be an expert on all of this; you want to be conversant on it. So, as a financial person, you can work remotely. As a legal person, well, that is more local because I would not want an Iowa-based attorney to create my documents in Florida; I hired someone local. As far as tax, unless you are getting into very sophisticated state tax issues, usually your tax person can be remote as well.

So, if you are a financial or tax person, it is best to do this right and make it easy for them and get them going on tech. The U.S. Mail is hard to make it work right, but if you do everything electronically, it gets a lot easier.

Planning Your Exit

Your clients’ go-go years are in their 60s, their slow-go years in their 70s, and then, for most, their 80s are their no-go years. You have heard that, but you have to think about that.

So, what about frailty? You know, what are you going to do if it does not work to get back and forth between Illinois and Florida? What happens if Jan dies or if Dean dies? Typically, that changes the plan. What happens if you have financial changes? I mean, your money went south because of some catastrophic thing.

So, it would be best if you were thinking about alternatives. I have given examples of two condos throughout this presentation, but there are things like active adult retirement communities. So, that in Florida would be the Villages or Sun City out in Arizona, those kinds of things, or the CCRCs where you live through stages of independent living and then assisted care and then nursing care. Then, there are naturally occurring retirement communities as well.

Let’s say Jan and Dean use a reverse mortgage with purchase to get their condos in Illinois and Florida. They change their residency. They switched from Medicare Advantage to original Medicare and Medigap; that way, they did not have to worry about it. They keep one car in each locale, then fly back and forth; they find that easier. They still have their financial tax advisors in Chicago, but they have healthcare and doctors in Florida and Chicago, and legal in Florida to do their wills. They are living the good life.

Key Takeaways

- Many retirees want to live in more than one location – to “snowbird.”

- Advisors can help by providing information on the financial, legal, budgeting, and tax issues that otherwise can derail a client’s plans.

- Financial solutions such as reverse mortgages can help finance the ownership of two residences, and multiple tools exist to help maintain these residences.

- With proper planning, advisors can work with retired clients, even though they spend their time in multiple locations.