Also, let us say you work for a state agency, city, county, or local government agency that only offers a defined contribution plan as your primary benefit. This is considered “a pension” from Social Security’s perspective. So, the term “pension” in Social Security’s world means an employer-paid retirement benefit like a 401(k), 457, 403(b), or traditional pension.

If a worker pays into Social Security as shown on their paystub, they are paying FICA taxes. If they have paid in for at least ten years, they have earned 40 credits, so they are now eligible for some Social Security retirement benefit. In 2021, if you were earning at least $1,470 a quarter or roughly $6,000 over the course of this year, you would earn four Social Security work credits for the year.

Social Security calculates your worker benefit based on your highest 35 years of earnings. This is very different from the way pensions are calculated. Many pensions may look at your high three years, or high five years, of earnings to calculate your benefit. This can be an eye-opener for members in your retirement systems who do not understand how Social Security works.

Remember that Social Security started in 1935 as a welfare program to provide more income for lower-income workers and less income for higher-income workers. It was not designed to be a primary retirement benefit. It was designed to be a supplement to provide a safety net. The Windfall Elimination Provision addresses the workers who look like they are low income if they worked for an employer who doesn’t withhold Social Security taxes from salaries.

Let’s say you have a worker who only has 15 years of Social Security earnings and has worked the rest of their career for a county that doesn’t participate in Social Security. They are going to look like a low-income person to the Social Security system. If you only have 15 years of earnings, Social Security averages in 20 years of zeros. Divide that all by 35, and that is going to pretty much look like a low-income benefit.

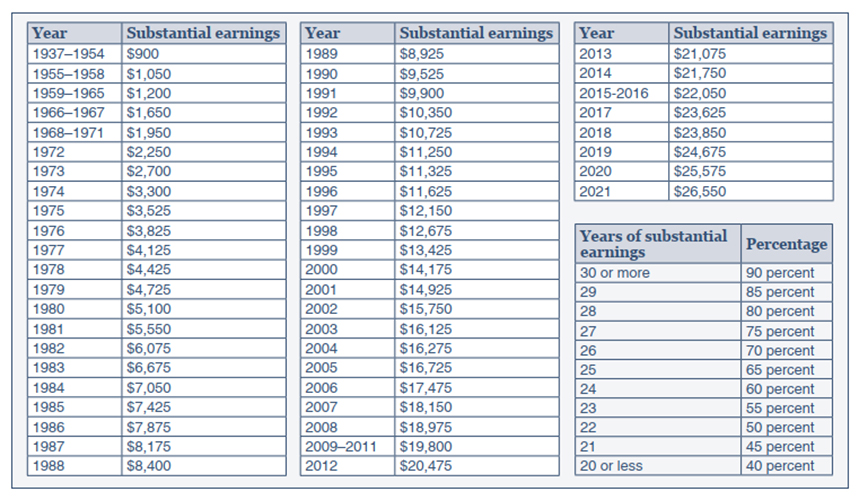

Now, some good news. The WEP does not impact the benefit provided by your agency; it only affects the Social Security benefit itself. In contrast to the high 35 years of income used by Social Security to calculate a benefit, the WEP is based on the number of years of “substantial earnings.” Each year, Social Security defines what substantial earnings are for that particular year.

For instance, in 2021, to have a year of substantial earnings, you would have had to have earned more than $26,550 in a job that pays into Social Security or where you are paying FICA taxes. 2020 it was roughly $1,000 less. The same goes for the year 2019. They adjust the dollar amount each year for inflation.

To have a year of substantial earnings, you must meet that specific year’s minimum in a job paying into the Social Security system. Note that “substantial earnings” are not the same as the earnings credit. Earnings credit is relatively small to qualify for, let us say, four quarters of earnings credit. Substantial earnings are very, very different; a different dollar amount as you see listed above.

Where can you find how much your earnings were for a particular year? Your Social Security statement. Here you can see for each year what your income was for that particular year, as reported by an employer. This is going to match whatever is on that member or that worker’s W-2 statement. For instance, someone who has worked from 1976 up through 2002 has 27 years of paying into Social Security. 2003 came along, and suddenly there are no additional taxed Social Security Earnings recorded.

When does WEP Apply?

If you only have wages from jobs you have paid into Social Security, the WEP does not apply. Typically, nearly all private-sector jobs, most federal jobs, some state and local government jobs pay into Social Security. It depends on the state and local government and whether they pay into Social Security or not.

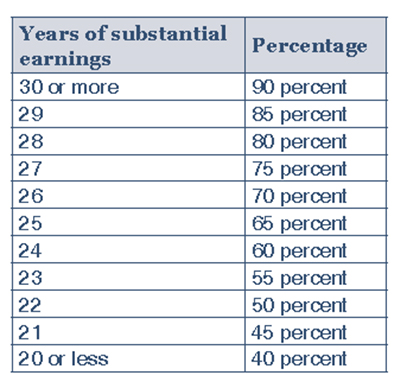

Again, good news. Folks who have paid their entire careers into the Social Security system by paying FICA taxes have no worries whatsoever as the WEP is not going to apply to them whatsoever. It gets tricky when someone has some years where they paid into Social Security, but other years where they have not. It depends, again, on whether the agency is Social Security exempt. It also depends on the number of years of substantial earnings. Once you have 30 or more years of substantial earnings, the WEP does not apply whatsoever.

So, let us look and compare. Let us look at an average calculation for a worker’s Social Security benefit, and then we will look at how the WEP might impact it. Social Security identifies your high 35 years of earnings to calculate AIME or your average indexed monthly earnings. There are three what are called bend points, or three buckets if you will, the Social Security formula uses to calculate the worker benefit. For 2021, a worker gets 90 percent of their first $996 of monthly earnings. If they have averaged, say $4,000 or $5,000 a month, they receive 32 percent of up to the next $6,002 in monthly earnings. If they have earnings beyond that, such as average monthly earnings of $8,000, they get 15 percent of the remainder past $6,002. Add all that up, and that is the worker Social Security benefit.

The WEP comes into play on that first bucket or the first $996 of earnings. After that, the dollars are treated the same, just like someone who has paid into Social Security their entire career. What determines whether someone is going to receive 40 percent or 90 percent of that first $996? It is their years of substantial earnings. Let’s say someone has only 12, or 14, or 17 years of substantial earnings. They will only receive 40 percent of that first $996 in Social Security benefits. The more years of substantial earnings you have, the smaller the WEP reduction is going to be.

Once you get to the 30-year mark of substantial earnings, there is no more reduction as far as the WEP is concerned. You get treated just the same as someone who has paid into Social Security their entire career.

How is the WEP Social Security Benefit Reduction Calculated?

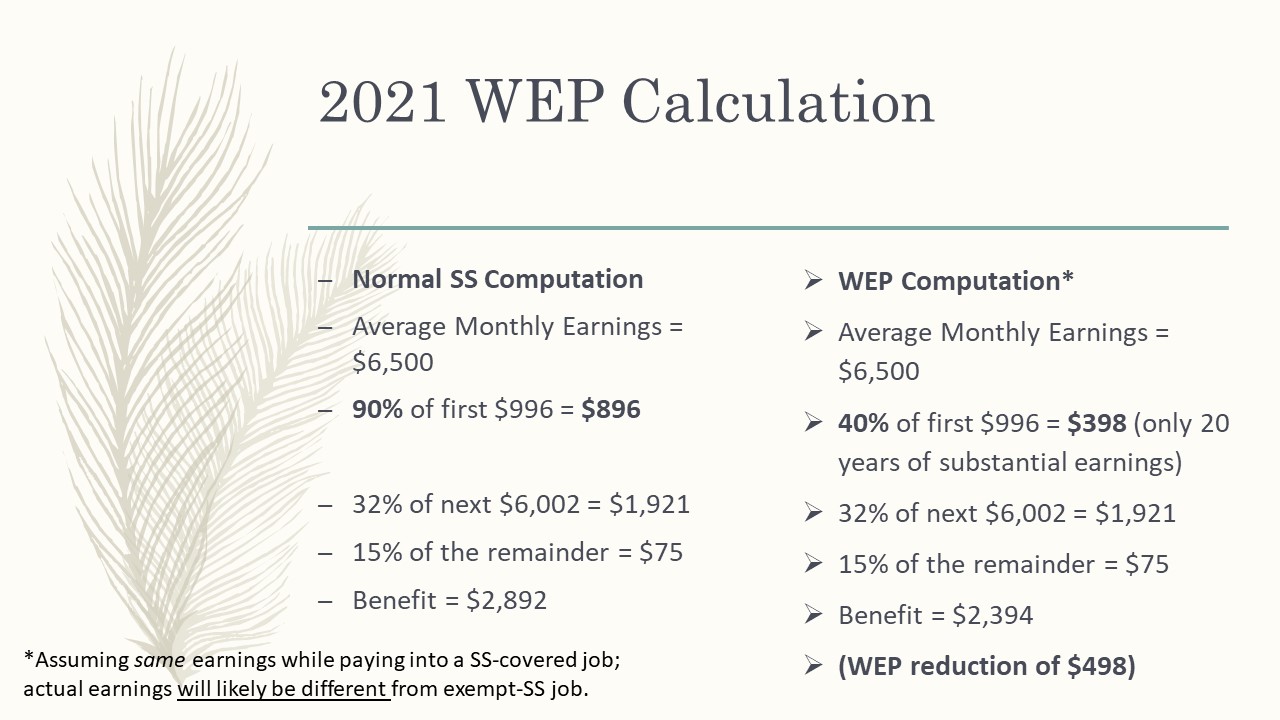

Let’s look at an example of someone who has average monthly earnings of $6,500 and has 30 or more years of substantial earnings. To calculate their Social Security benefit, we start with 90 percent of their first $996 in average monthly earnings, or $896. They will also receive 32 percent of the next $6,000, and then 15 percent of the remainder, for a monthly benefit of almost $2,900.

Let’s say instead of over 30 years of substantial earnings, someone has only 20 years. The significant impact is on that first bucket or the first $996. Instead of receiving $896 (90 percent of $996, the full benefit Social Security worker would receive for the first bucket), they only get $398, or 40 percent from that first bucket. After that, they are treated just like everybody else in the Social Security system. The bottom-line benefit for the partially exempt worker here is around $2,400. The maximum monthly WEP reduction in 2021 is $498 a month or roughly $6,000 a year.

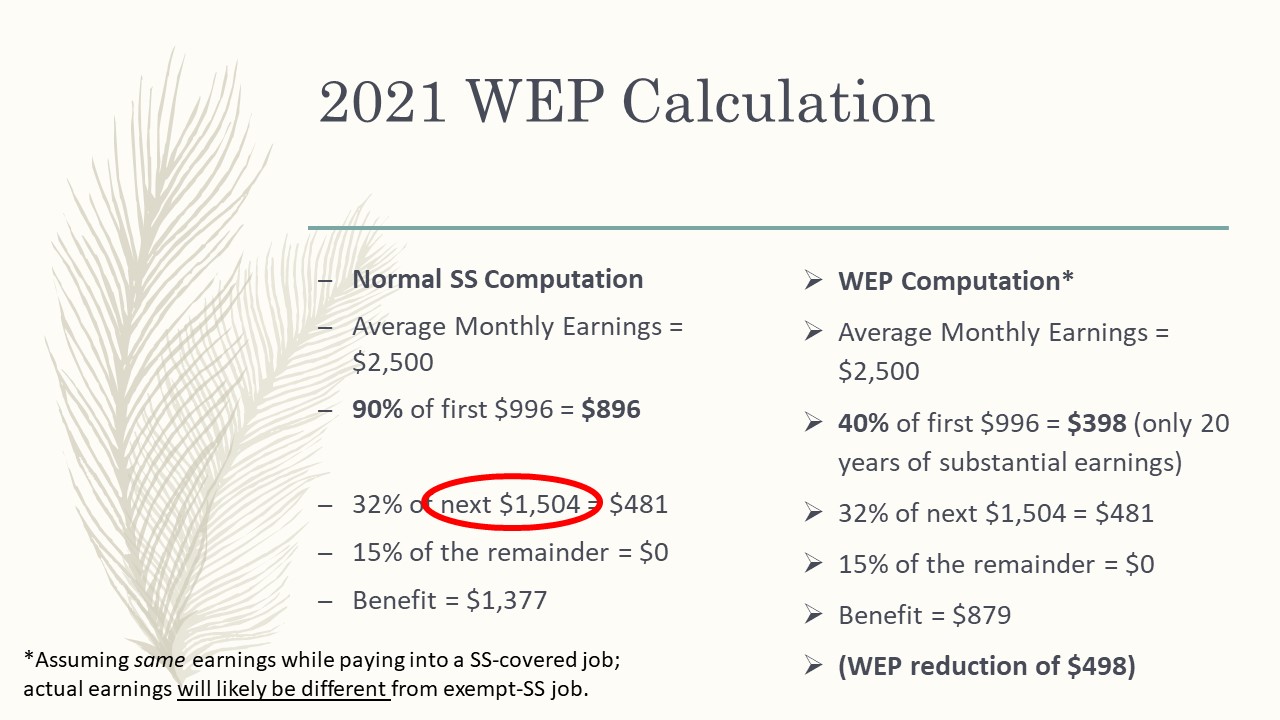

What about a lower-income worker whose average monthly earnings are only $2,500 a month or roughly $30,000 a year. Same formula, right? They received 90 percent of the first $996 and 32 percent of the next $1,504, capping them at monthly earnings of $2,500, or $481.

Suppose they worked part of their career for a Social Security exempt agency and had only 10, 15, or 20 years of paying into Social Security with substantial earnings. In that case, the dollar reduction is still the same, or $398. Their WEP reduced benefit is now $879. Instead of getting maybe almost $1,400 in Social Security monthly benefit, they are down to $879.

The longer someone waits to start Social Security, the bigger their benefit is in dollar terms. This also means that the Windfall Elimination Provision reduction might be higher in terms of dollar amounts. These will offset each other to some degree.

What if you want some information on this that you can share with your agency employees if you are the employer? Or that you can look at yourself? There is an excellent little two-page publication on the Social Security website. They update it every year because they list the substantial earnings amount for each year. There is also a WEP calculator that is probably the best tool to estimate the WEP impact.

Limits to the Windfall Elimination Provision (WEP) Reduction

The maximum WEP reduction is limited, though, to a maximum of one-half of your pension from what is called “non-covered employment.” Non-covered employment means, “I am working for a Social Security exempt agency where I receive a pension, 401(k) or other retirement benefit.”

Let’s say someone worked just a few years for a Social Security exempt agency. For most of their career, they were paying into Social Security. Maybe they have a $400 a month pension coming from those few years of working for a Social Security exempt agency. Instead of the maximum $498 a month reduction, the WEP reduction is limited to one-half of their $400 monthly pension, or $200.

When will Social Security know that you had exempt earnings working for a Social Security exempt agency? Not until you file for that Social Security benefit. Social Security is going to assume you have not been working for an exempt agency. If it turns out you have, the WEP will apply. You do not want to rely on your Social Security statement as the benefit will probably be overstated. If you want a rough ballpark estimate, knock the benefit down $500 a month. However, to be more precise, use the WEP calculator and the SSA.gov website.

What Can I Do to Minimize the Windfall Elimination Provision (WEP)?

Let’s say you have a supplemental plan such as a 457, 403(b), or 401(k) from non-covered employment. It is not the primary benefit from that agency, but maybe it is a voluntary option where either the employer could put money in, or the employee could put money in. The WEP calculation will not include your supplemental plan if it only contains your employee contributions. Say your employer puts matching money in a 401(k) on your behalf instead of paying into Social Security. Those employer contributions will be counted as a pension, as far as the WEP is concerned.

Theoretically, it could make the WEP reduction larger as well. So, word to the wise: If your employer is putting money voluntarily for you into a 401(k), if you have it, then make your employee contributions to the 457 plan. As long as that 457 or another plan has employee contributions purely, it is invisible as far as the WEP calculation is concerned.

Now, the question sometimes comes up: My employer does match to a 401(k) plan. I also have a 457 plan. Should I put money in the 457 and give up that match? I would say no. Any time you get an employer match, depending on what the match is – 50 percent or 100 percent – that is free money from the employer. You do not want to give that up. Even if it does result in getting dinged by the WEP a little bit more, mathematically, in nearly all cases, if your employer is offering a match contribution, take advantage of it. It may ding you a bit in terms of the WEP. Overall dollars, you will come out ahead in the long run by taking advantage of those matching contributions.

What else can you do to minimize the WEP? You have probably already drawn some conclusions yourself. Just work more years in a job that pays FICA, pays into Social Security, and earns enough each year to qualify as substantial earnings.

That might be easier said than done. For instance, say you are a full-time worker at a Social Security exempt agency. Maybe you are in a school system that does not pay into Social Security, and you are a full-time teacher. You must earn more than $26,550 in substantial earnings in 2021 during the year or maybe during the summer when you are off. Earning enough to count as a substantial year sounds like a great idea, but it is a high hurdle to overcome.

Does the Windfall Elimination Provision (WEP) Affect Spousal Social Security Benefits?

WEP itself does not affect a worker’s spouse’s own Social Security benefit. Let’s say I am married and work a Social Security exempt agency. I have worked some years in the private sector, some years for this exempt agency. The WEP affects my Social Security benefit. However, if my wife has worked her entire career in the private sector, it has no impact on her own Social Security benefit. The WEP only affects me directly when I have years of income earned in Social Security and out of Social Security.

Sometimes people think they’ll get around the WEP if they don’t take their pension, but instead a lump sum payout, so now they don’t have a ‘pension.’ Nope. Social Security is on to that game. They will consider that lump sum amount and make an estimate of your life expectancy and what the monthly equivalent benefit would be. That is what they are going to call your “pension.”

As far as a spouse who has paid into Social Security in the private sector their entire lives, they can start their own Social Security benefit when they retire. If a spouse never worked outside the home, they would be entitled to the spousal benefit, which is one-half of mine at my full retirement age. This is a whole other issue as well.

Let us assume, to keep things simple, that my benefit is $2,000. My spouse would get half, or $1,000. If I worked part of my working years paying into Social Security and part of years not, the WEP affects my worker benefit, reducing my Social Security benefit. When my spouse takes a spousal benefit, their benefit is now going to be reduced as well.

How do things change when I pass away? Logically, you might think, “Well, the WEP was reduced for the spousal benefit while I was alive. Wouldn’t the same happen to the survivor benefit?” As it turns out, Social Security essentially ignores the WEP when this happens. Let’s say I collect a $1,502 per month WEP-reduced benefit, where the benefit should be $2,000. Instead of my spouse receiving just a $1,502 survivor benefit when I die, they receive the total $2,000 a month benefit.

Other Earnings Situations

The other question that comes up sometimes is, “What if I do not have enough earnings in a particular year to count as substantial earnings? Was it a waste? It did not count; it did not help me reduce the WEP.” What happens to those dollars that I paid into Social Security, say on a part-time basis? Assume we have a schoolteacher who works nine months out of the year for an exempt agency that does not pay into Social Security. Before becoming a teacher, this person worked 13 years and had substantial earnings working in the private sector. They now have a side gig doing construction in the summer when they have June, July, part of August off and earn $15,000 a year. This $15,000 is way below the $26,550 for substantial earnings in 2021, which did not help as far as the WEP is concerned. What happens to those Social Security dollars based on that $15,000 income? Do they disappear? Does that go into the system and benefit someone else?

Remember, Social Security looks at your high 35 years earnings when they calculate your Social Security benefit. In this person’s case, they already had 13 years of substantial earnings. Now they have a year with $15,000 of earnings, eliminating a zero from their 35-year calculation. The $15,000 easily qualifies for quarterly earnings of credit. It has boosted their Social Security benefit ultimately. It is just not going to help them when it comes to reducing the WEP adjustment itself.

Let’s say we have a Social Security exempt worker. They have worked their entire career for an exempt agency. They have a stay-at-home spouse who has never worked outside the home. There is no WEP. Why not? They never paid into Social Security, so they will not be entitled to a Social Security benefit.

Key Takeaways

- The WEP could affect the worker’s own Social Security benefit. It does not affect a spouse’s worker benefit. It is not going to reduce the agency’s benefit.

- To minimize the WEP, work more years in a job where you pay into Social Security. Get those substantial earnings.

- The worst dollar reduction in 2021 Social Security benefit 2021 is $498 per month.

- If you have not yet seen it, Social Security is transitioning to newer statements. Historically, they showed three dollar amounts for three ages: age 62, someone’s full retirement age, and then age 70. The new statement shows benefits for ages 62 through 70. I have been in a few counseling situations with folks who have received these new statements. It has been fascinating to hear their reaction to the new layout. From a behavioral finance standpoint, it will be interesting to see if people change their behavior by waiting to start their Social Security benefit because they know the year-by-year dollar increment for waiting.