A client wants to know, “How much do I have to save for retirement? When can I retire?” It is based upon this idea of an expectation and on the concept of retirement age timing. This gets to kind of the concept of what retirement age certainty means for a financial plan. A financial plan is a combination of hundreds of assumptions, and they’re not all going to be correct. But the goal is to make them as accurate as possible as we’ve moved towards using more complex financial planning tools such as Monte Carlo that utilizes random returns.

If you add in retirement age uncertainty into a financial plan, what does that mean for the average person when it comes to saving for retirement? Think about all the things that you could control to affect someone that is not on track to retire successfully. They can work longer, they can save more, or they can live off less when they retire.

How do consumers feel about time and age as a variable to improve their outcomes? We’ve done surveys where we ask people, “Assume that you aren’t on track to retire successfully. What would you be willing to change?” Is retirement age a lever that individuals want to use to possibly improve their outcome?

(See the research David Blanchett has published on this topic at right.)

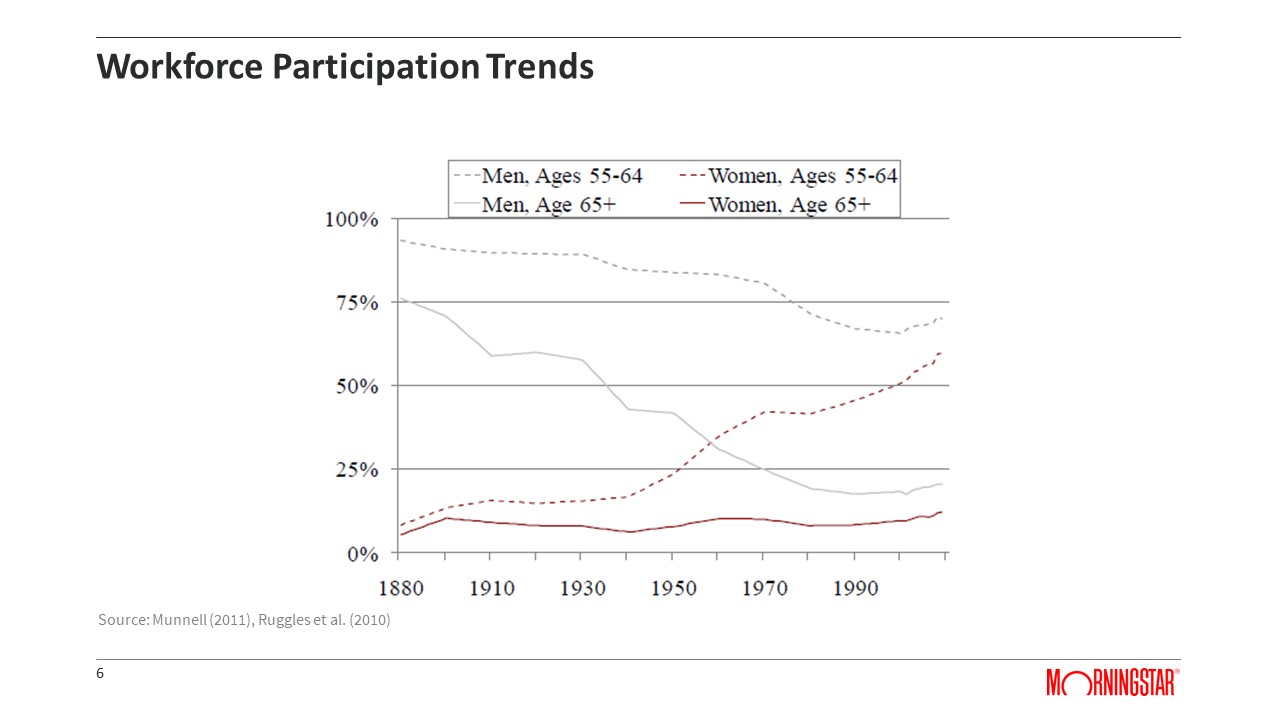

Retirement Age Trends

This is an interesting graphic that shows the percentage of individuals still in the workforce between the ages of 55 and 64 and ages 65+ (our focus here

is on the dotted line for men and the dark gray line).

What’s interesting about this slide is if you go back to 1880, 75% of people over the age of 65 were still working. At that time, life expectancies at that age were probably no more than ten years.

Back, then we didn’t have this idea of working for 30 or 40 years and then living for another 10 to 30 years in retirement. Things have obviously evolved. Looking at the solid gray line (men aged 65+), we went from a 75% workforce participation in 1882 to about 20 percent in 1990.

What’s interesting about the effect of this change is that it’s occurring as life expectancies are increasing. Suddenly not only do you have the opportunity to retire, but you have a more extended period to enjoy it. So, while there was this decrease in workforce participation for men from the years 1882 to 1995 or so, people are starting to work more at older ages.

This is actually a global phenomenon. It hasn’t occurred exactly in the US as it has everywhere, but the average age of retirement for the 20+ countries in the OECD had also been declining. For both men and women, retirement ages declined since the year 1972 to about the year 2000, but it has ticked back up again. So, there is this kind of new global effect where individuals who were retiring earlier and earlier and earlier are now retiring later.

One of the most apparent reasons for the increase in retirement age is the declining availability of defined benefit plans. Fewer and fewer organizations, both domestic and globally, are offering pensions, forcing individuals to save themselves, and we all know that people don’t do a very good job saving for retirement. What will be curious is how this effect plays out in the future.

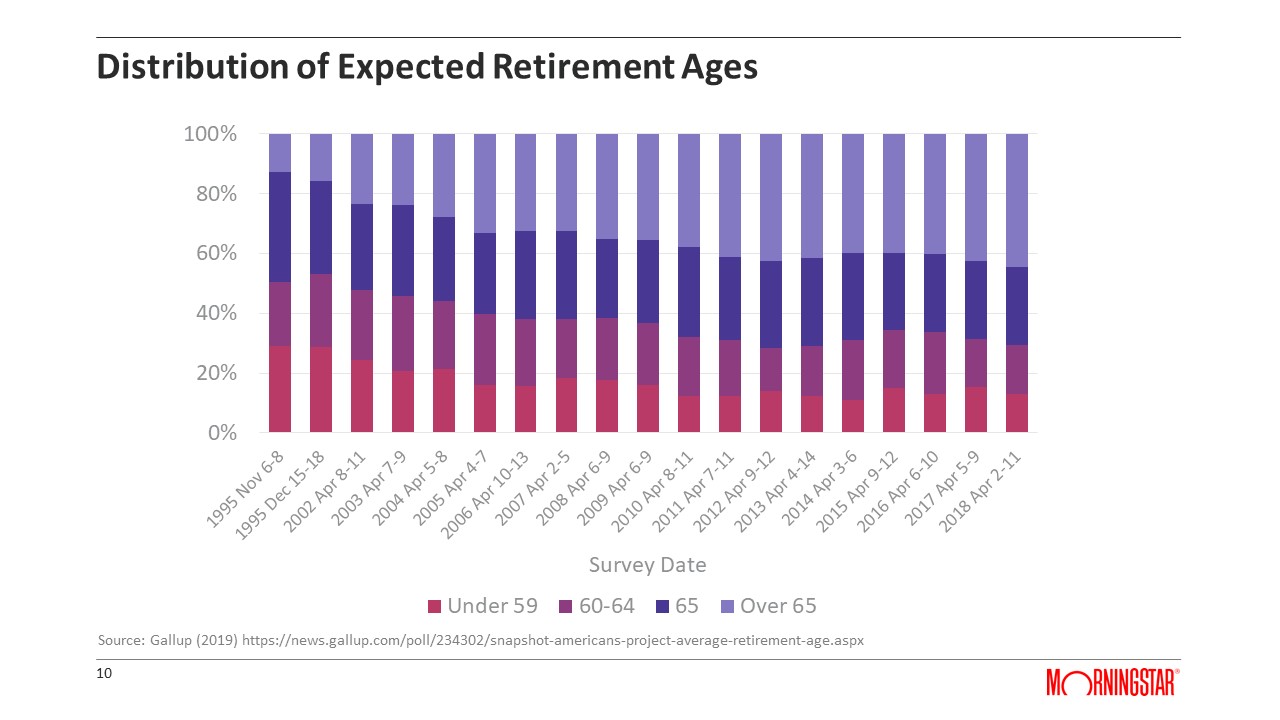

At What Age Do People Expect to Retire?

This first slide shows you the distribution of retirement expectations for different surveys that have been done by Gallup for the last 23 or 24 years. There’s a noticeable change in that upper blue region when someone says they are going to retire after the age of 65. Back in 1995, that was only around 10%, but now it’s over forty percent.

Source: Average American Expects Retirement at Age 66, Gallup.

This is a considerable change in retirement expectations over the last 20 or so years. What’s interesting though, is who among us have these expectations.

The latest EBRI Retirement Confidence Survey looks at when do people expect to retire based upon their current age. Twenty-five percent of Millennials want to retire before the age of 60. Only one percent of individuals aged 55 plus say they’re going to retire before the age of 60. Older Americans, all of a sudden, realize that a lot has happened over their lives. Maybe they got a divorce, they weren’t able to save as they wanted, or they had to pay for college; there are financial issues that have affected their ability to save, so they have to delay their retirement.

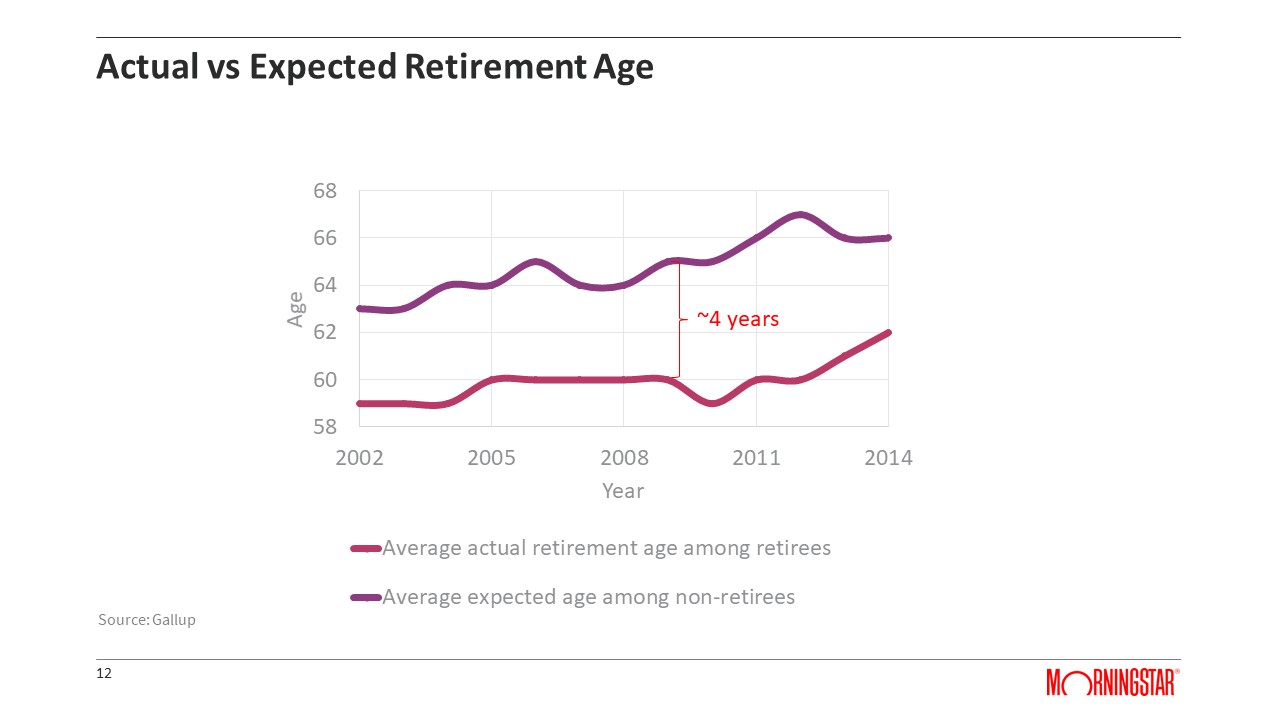

The trend is that the actual age of retirement is increasing, but it is rising along with expectations.

What we see here is about a spread of four years between the expected age of retirement among non-retirees (the purple line) and the actual age of retirement (the pink line). If we look at the year 2000, the actual retirement age was 59 and the expected age was 63.

We’re in a lot better space today based upon the point in 2014. The actual retirement age is increased three years to age 62, but so too has the expected age. From my perspective, what we have here is a constant gap of three or four years. This gap is pretty scary. The reason it’s scary is that if you don’t retire when you expect to do so, it creates the possibility for a significant difference in the amount you have saved for retirement and what you’re going to need right now.

This works both ways. If individuals were expecting to retire at age 60 but retired at age 63 or 64, they’re going to have a lot more than they probably need when they retire.

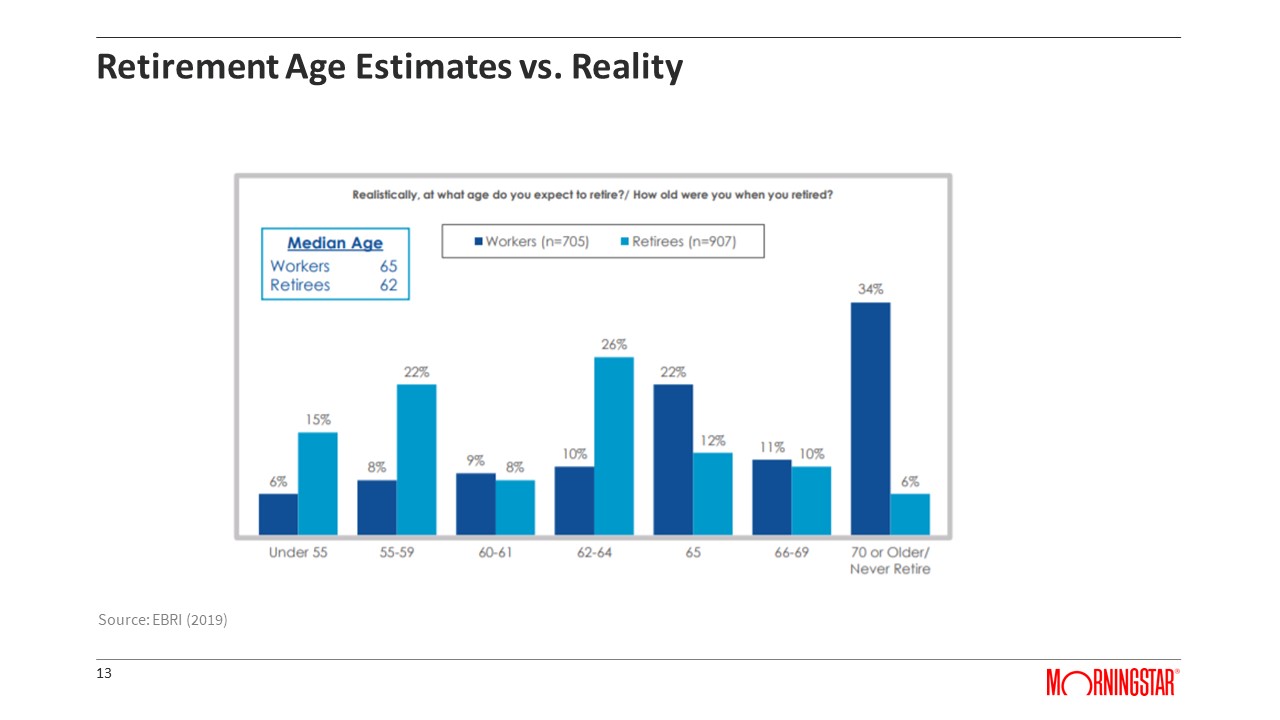

We see this effect where retirement ages are not necessarily reliable indicators of when someone is going to retire. The median age a worker today thinks they are going to retire is 65; the median retirement age is 62.

Source: 2019 Retirement Confidence Survey, EBRI.

According to the 2019 EBRI Retirement Confidence Survey, 34% percent of people think that they’re going to work to age 70 or never retire. Here’s the thing: only six percent did. This is significant. If they’re basing their retirement savings on that assumption, they’re going to be terribly wrong.

Only about 5% of Americans retire later than planned about 45% retire about when they plan to do, so about 50% retire earlier than expected. Again, there’s this significant effect here where the errors around the expectations for retirement are not random.

Why Do People Retire Early?

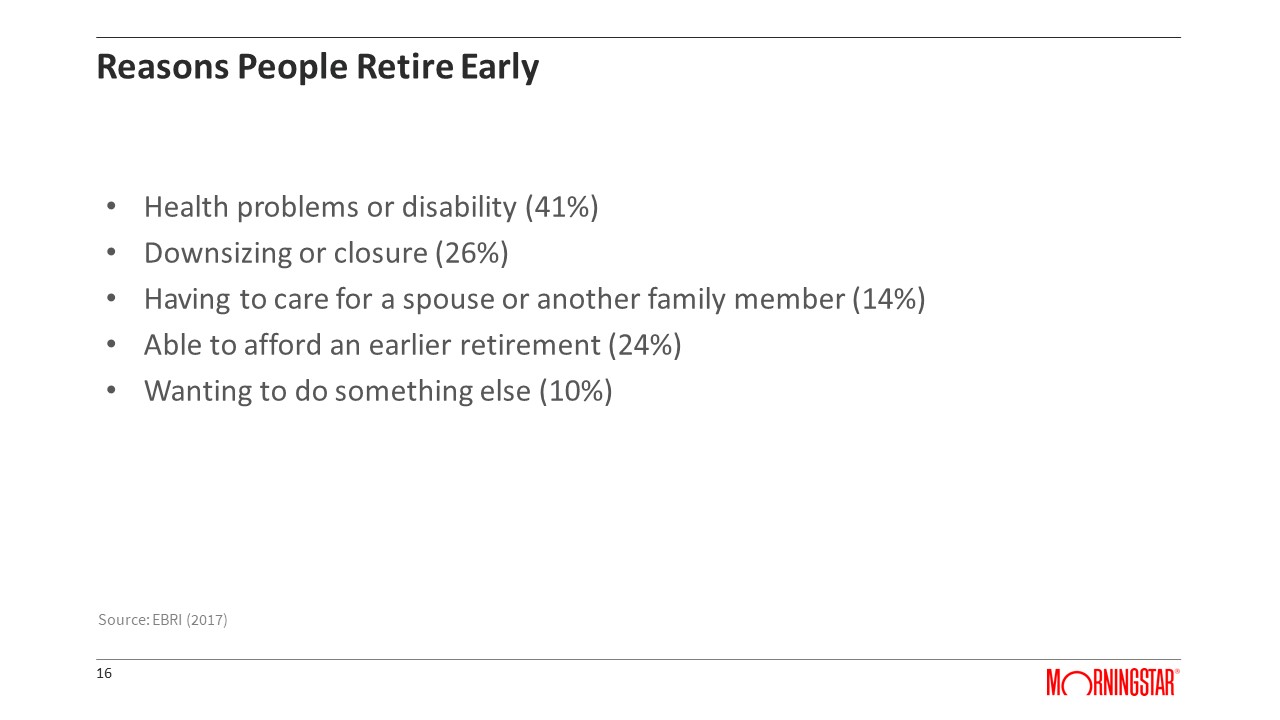

Half of Americans retire earlier than expected. This has significant implications for saving for retirement. Why does this happen? When an individual retires early, is it because they choose to retire early or because they have to? This is important in the context of things like retirement saving.

The number one reason for early retirement is health problems or disability. Forty-one percent of retirees have something happen that effectively prevents them from working.

Source: Employee Benefits Research Institute (EBRI).

The next largest is downsizing or closure of the company (26%). In theory, these individuals could go back to work, but it isn’t very easy to find a good job for lots of people who are 65 years old. Other things can happen to you have to care for a spouse or a family member who has health issues (14%). There are a few folks that choose to retire early. If you look at the reasons people retire early, it is not related to choice. It’s because they have health issues, or they get laid off, and they simply can’t go back to work.

Overwhelmingly people delay retirement because

- they can’t afford to retire

- they don’t believe that Social Security will provide them with an adequate benefit

- they have concerns about health care costs, or

- they want to have a comfortable retirement.

All these reasons point back to a lack of savings, and therefore they can’t afford to retire.

Only about 30% of retirees work for pay after they retire. In theory, working in retirement could be a great way to help your savings last longer. But we’ve just not seen individuals work much in retirement.

Working in retirement has significant positive financial and psychological benefits. When someone works and stays active, it helps with cognition. It helps with happiness. There are lots of reasons why working can help someone prolong their retirement. If you can work, there is evidence that the wages are pretty good for retirees.

If I’m married in retirement, I’m going to be 5% happier on average that if I’m single. Happiness appears to rise with age, so if I’m age 65 to 69, I’m about 10% happier. People that have a defined benefit plan and a defined contribution plan are five percent happier on average if than if just a defined benefit plan.

People who are forced to retire are 30% less happy than those that retire their own free will, and individuals that are partially forced to retire are 20% less happy than individuals that get to retire of their own free will.

What is the one thing that I can do to improve my clients’ retirement success? Delay retirement. Delayed retirement gives you one more year to save, one more year for your savings to grow, one more year to delay claiming Social Security, and one less year to plan for retirement. Early retirement has the opposite effect. We know though that people tend to claim Social Security as soon as they possibly can.

We also know that households with higher income levels are living longer and longer, potentially two to four years longer than the average American. This idea of early retirement affects them even more because if they retire early and only live for 15 years, it’s no big deal, but if they retire early and live for 30 years, it will have a huge effect on retirement needs.

Blanchett’s Rule of 61

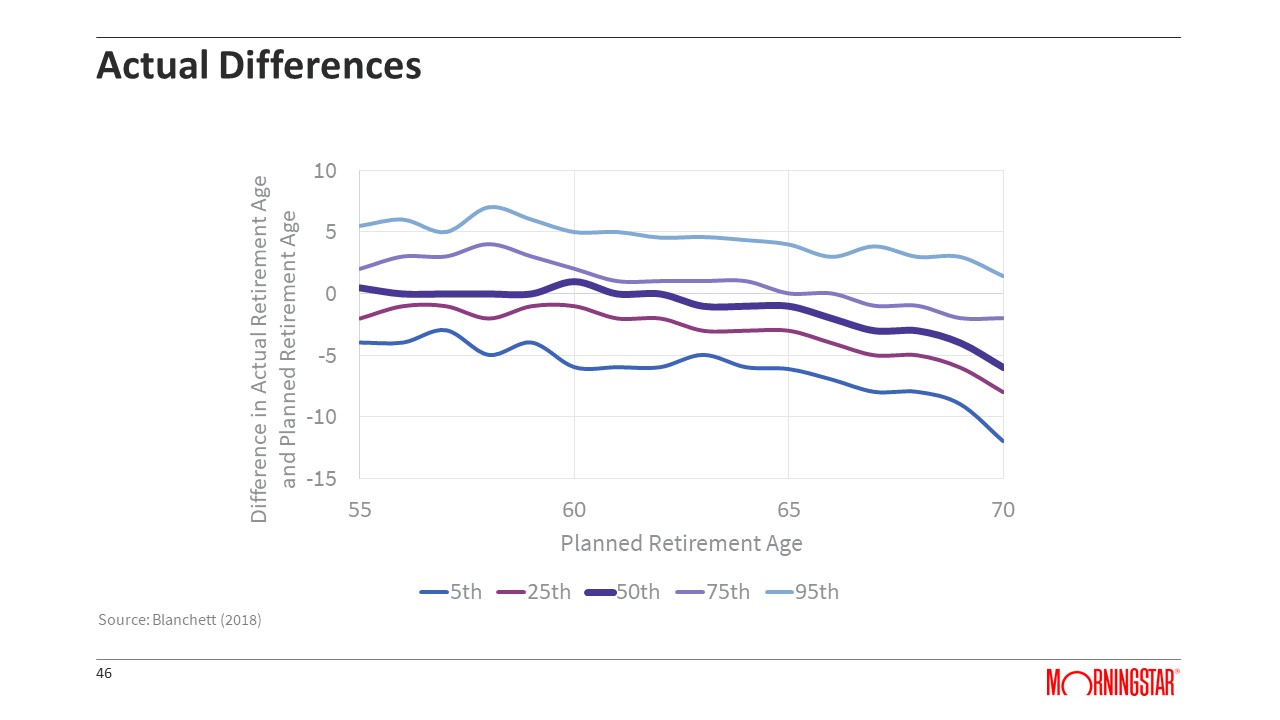

For my research and analysis, I looked at data from the Health and Retirement Study over different waves. What’s interesting about this data set is that it tracks people over time, i.e., it goes back to the same households every two years and asks them tons of questions. This data set asks people when they expect to retire, and it documents when they retired. There has been a definite increase in the expected retirement ages among households over time.

While several variables were statistically significant, the key driver that I found of the differences in success in retirement was based upon the expected age of retirement.

On the horizontal axis is the age that someone is planning on retiring. On the vertical axis is the difference in the actual retirement age versus the planned retirement date. If it’s above zero, they retired later than expected.

For example, if someone is age 59 with a value of positive five, they retired at age 64. If it’s below zero on the vertical axis, they retired before the expected age, so if they are age 59 with a negative 5 for planned retirement age, they retired at age 54.

The bolded line the 50th percentile shows you that people were pretty good with their expectations until around age 61. After age 61, there’s a noticeable decrease in the planned retirement age.

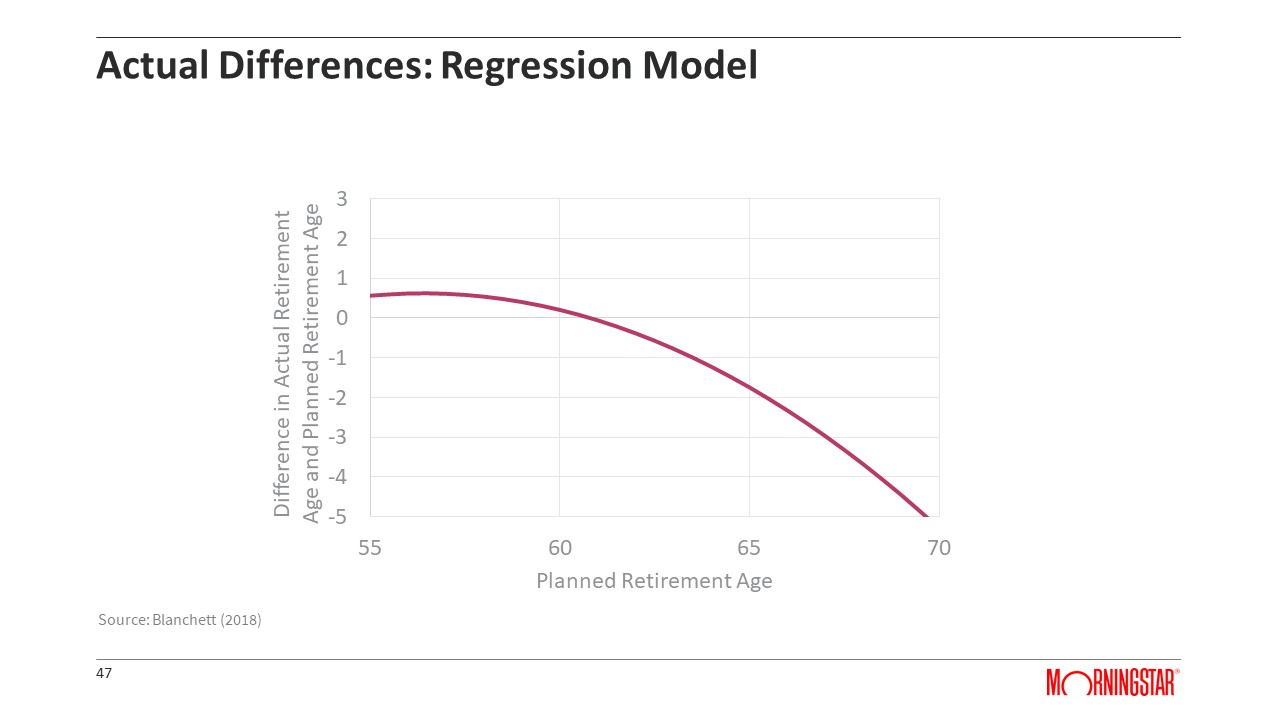

This is what this looks like if you collapsed it all together into a single model.

The red line crosses the 0 on the vertical axis at the age of 61. So if someone retires at 61, they hit the bogey and retire when planned. If they retire past age 61, there’s a negative difference, or they retired earlier than expected. If they before 61, they retired a bit later than expected. This is what I call the “Rule of 61”.

What the Rule of 61 does is help you kind of figure out the actual retirement age based upon their projected retirement age. For example, if you target a retirement age before the age of 61, you tend to retire about one year later on average. If I have a targeted retirement age of 58, I’m going to retire at 59 on average.

If I target age 61, I retire about when I expect to. After age 61, it’s usually about a half year for each additional year of planned work past age 61. The example here is if a client thinks they’re going to work until age 69. On average, they will retire at age 65, four years earlier than expected (age 69 – age 61 is 8, divided by 2 for years).

One thing that I learned was that you don’t have to model retirement uncertainty at all. If you can incorporate the Rule of 61 in your analysis, random retirement doesn’t matter. If you again incorporate the fact that people tend to retire earlier than they expect to retire after the age of 61, there’s no need to have retirement age is another random variable projection.

Here’s a really important thing: if you ignore retirement age uncertainty, if you ignore the assumption that someone retires early, it can have a devastating impact on their retirement. If a client says they’re going to retire at age 70, plan for them to retire at age 66 or so on average to maintain the same level of happiness in retirement. Retiring four years early increases the amount of savings needed almost 50%. If someone is saving expecting an age 70 retirement and they retire early, they’re going to be in huge trouble. You’ve got to tell them there’s a good chance they’re not going to work to age 70. We’ve got to model this like you’re going to retire sooner and not be surprised.

If you incorporate this idea of random retirement, it requires more savings – at least 25% more. For every client out there that says hey I’m going to retire at age 65 and retires at 63, they need to be saving more for retirement. If you don’t educate them on that possibility that very real possibility, we’re going to end up in a very kind of dangerous place when they do eventually retire.

What are the Overall Conclusions for Today’s Financial Plans?

Financial planners should consider showing clients the implications of early retirement to potentially get them to save more than they would be using a more traditional approach where retirement age is treated as certain, because:

- Your financial plan is going to be wrong. This is an absolute certainty. There are hundreds of assumptions that go into these plans, and life happens. You can’t just use historical long-term averages in a projection. You’ve got to use expected returns. No one knows what’s going to happen. I don’t know what the markets are going to do. A financial plan is only as good as assumptions.

- As an industry, we overwhelmingly get the retirement age wrong. People are retiring earlier than expected across the board; half of the people retire earlier than expected. Use this Rule of 61, especially for folks who are targeting retiring working until age 70. It’s not going to happen for most people. If you ignore this uncertainty around retirement age and the implications of early retirement, it is going to have a significant negative impact on many retirement outcomes.

- When you run financial plans, also model retiring earlier. If your client is targeting age 67, rerun the numbers and see what that looks like for their annual required savings rate.