The Shadow Caregiving System

The Shadow Caregiving System is a bumpy journey. Do we expect it to grow? How will it influence your clients and individuals in your practice?

In a new 31-page report entitled Valuing the Invaluable, AARP paints a very vivid picture of the current state of family caregiving in the US. It is an update of their 2019 survey. The organization’s public policy institute found that in 2021, about 38 million family caregivers in the US provided an estimated 36 billion hours of care to adults with limitations in daily activities like the ones we just mentioned. The estimated economic value of their unpaid contributions was approximately $600 billion. And that is up substantially from their 2019 survey.

By 2034, AARP notes that adults aged 65 and older will outnumber children under 18. And that is for the first time. Why is that important? That tells us that there will be a continuation of a shrinking number of caregivers because the relative number of older adults who potentially need long-term care will outnumber the number of younger adults available. In addition, family caregivers will continue to face the dual demands of employment, planning for their retirement, and caregiving responsibilities. That is when we often hear about the expression sandwich generation. However, most of us are talking about panini. As you will see, with longevity, many more generations are living a longer time.

What exactly do I want to say about the caregiving system and the caregiver’s role in that system? It does not happen in a straight line. And I am sure that some of you have had this experience. It is unique to each person. It is unpredictable. And it is quite personal. Many of your clients will have to take on the role of caregiving. And they will have to act, even if they hire someone to help. They are still going to have to act as an information coordinator. They will have to try to understand the confusing maze of medical and financial complications that continue to develop and change. Many studies say that when there is a financially stable plan in place, it can provide caregivers with the feeling of a more emotionally close relationship to the whole experience and a sense of purpose.

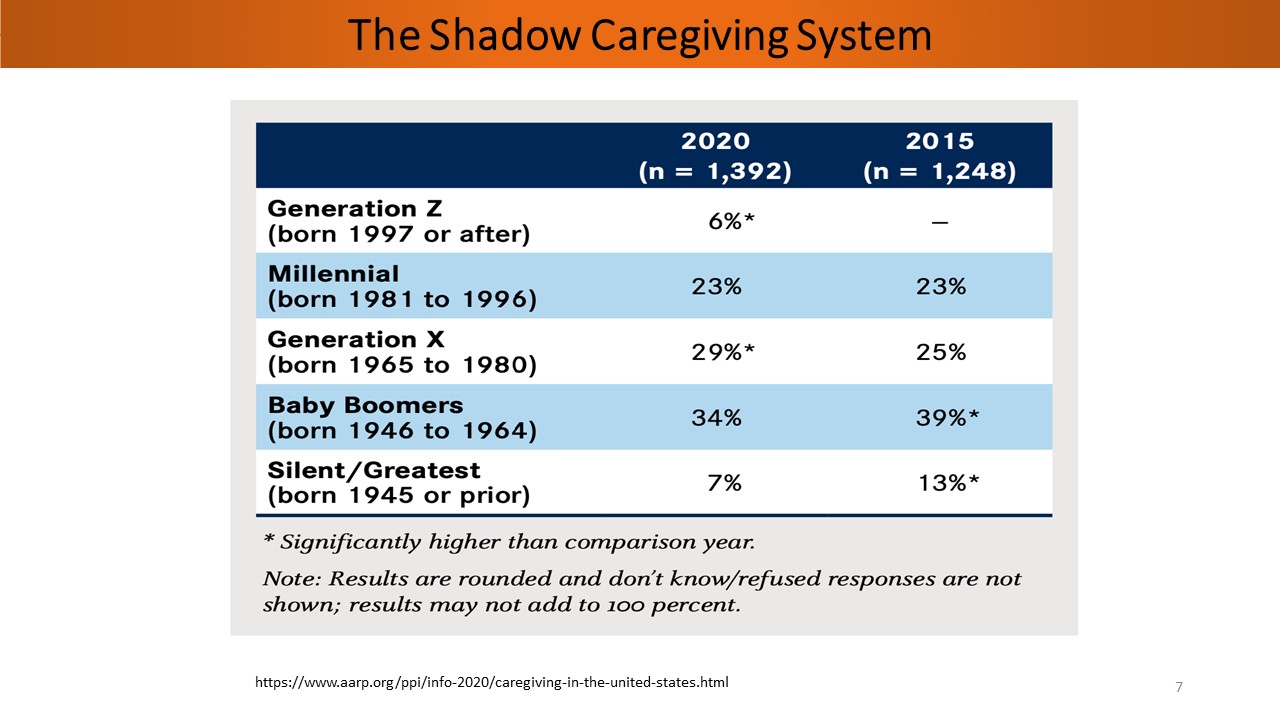

This chart tells a great deal about the Shadow Caregiving System. Who among your clients, family, or friends do you think are participating in the Shadow Caregiving System? There are now four generations participating in the system.

According to a US Bureau of Labor statistic, by 2031, most of the workforce will be comprised of the Millennials and Gen Z generations, with Millennials making up 40% of the labor force and Gen Z making up around 30%. You must help your clients, family, and friends get ahead of this curve. If you look, you will notice that in 2020, there was a shift in caregiving from the Silents and from the Boomers as well to the Millennials and the Gen Xers and Generation Z. Now, if we saw that shift in 2020, what do you think we’ll see by 2023 or 2029? It will continue to go that way.

The point is that the Shadow Caregiving System is comprised of people who are working. Family caregiving is America’s other Social Security, noting that family members provide more than 95% of nonprofessional care for older adults who do not live in a nursing home. And if you look at the third bullet down, 64% of them work full time.

Let us assume for the sake of argument that your client or family member can afford to hire a professional or semiprofessional caregiver. Remember, there are still a lot of coordination and psychological aspects to an unpredictable, bumpy, if you will, care journey. For example, a caregiver oversees the organizational aspects of the care recipient’s finances, such as paying bills, managing investments, preparing taxes, handling insurance, monitoring accounts, and so on. Looking at the last bullet on the slide, they are also at the same time trying to save for their retirement and their plans. It is complicated by the fact that many are helping to provide support to their families or family members.

So, some of your clients may be doing more than just handling the finances of care recipients. They may be quietly spending their own money on caring for or providing care for someone. According to the Age Wave Caregiving White Paper, 52% of caregivers have no idea about the total amount that they have spent to date on caregiving-related expenses. And I can tell you, when I was a caregiver, I did not keep track. Some of these expenses included homecare, transportation, and paying bills. They were everyday household expenses. Just the general upkeep and even costly medical expenses it was too much to write it all down. And add to that career disruptions that unsettle a person’s retirement and investment plans. It is just not a pretty picture.

The Complexity of the Shadow Caregiving System

Even in the case of long-term marriages, for example, boomers are more likely to be alone in their later years. It may be through divorce, widowhood, or they were never married. There is a decrease in the number of children that boomers had compared to previous generations. What is the result of that? A shrinking caregiver pool.

Now, let us look at the gender split. Women fill and are likely to continue to fill most of the caregiver roles. There is an AARP 2020 study that is significant to mention because it reports that women now own 51% of small businesses. Well, that translates to over 12 million businesses that employ over 10.1 million workers.

However, there are some differences in how men and women handle the role of being a caregiver. In general, now, men hire out more of the personal, physical aspects of caregiving, like showering their mom or that sort of thing. And regardless, that can directly impact their work performance. When you hire someone, you still have to make sure they show up, are doing what you expect them to be doing, and that the person you care about is comfortable with having that person in their home and helping them.

Then there is the financial aspect. The bottom line is whether your client or your friend is a male or a female, they will likely be a caregiver or a care recipient. When talking with them and asking them for information, I have found that many caregivers feel their glass is half empty. But as a financial professional, if we acknowledge and discuss financial issues that they encounter, you can make them feel, frankly, that even if the glass is half empty or worse, it is refillable. There are options.

Cost of Shadow Caregiving Trends

Longevity and demographics play a significant role in the growing Shadow Caregiving System. And the effect of those two realities also plays an increasing role in the cost of care.

According to the US Department of Health and Human Services Administration on Aging, we know or we suspect that the average woman needs long-term care for 3.7 years and men for 2.2 years. But I want to caution you that you need to keep in mind that before moving into, say, an assisted living community or upgrading to a skilled nursing facility, these people are likely to have had some homecare, probably provided by a family member or a combination of a family member and a paid caregiver. So, the numbers here are influenced by the complex makeup of today’s caregiving system.

For example, these numbers can be varied based on married versus solo ages. The one thing that I suspect everyone has in common is, of course, the desire to age in place. COVID-19 made everyone aware of staffing shortages and family challenges, especially regarding facility challenges. Even those who self-insure, which is not really insurance since insurance is a pooling of money. However, in this case, it is your client’s pool of money. But even if they are willing to deplete that personal pool of money, one has to ask, “Will qualified or trained help be available for hire?” And the minimum number of hours that they require is growing. Why?

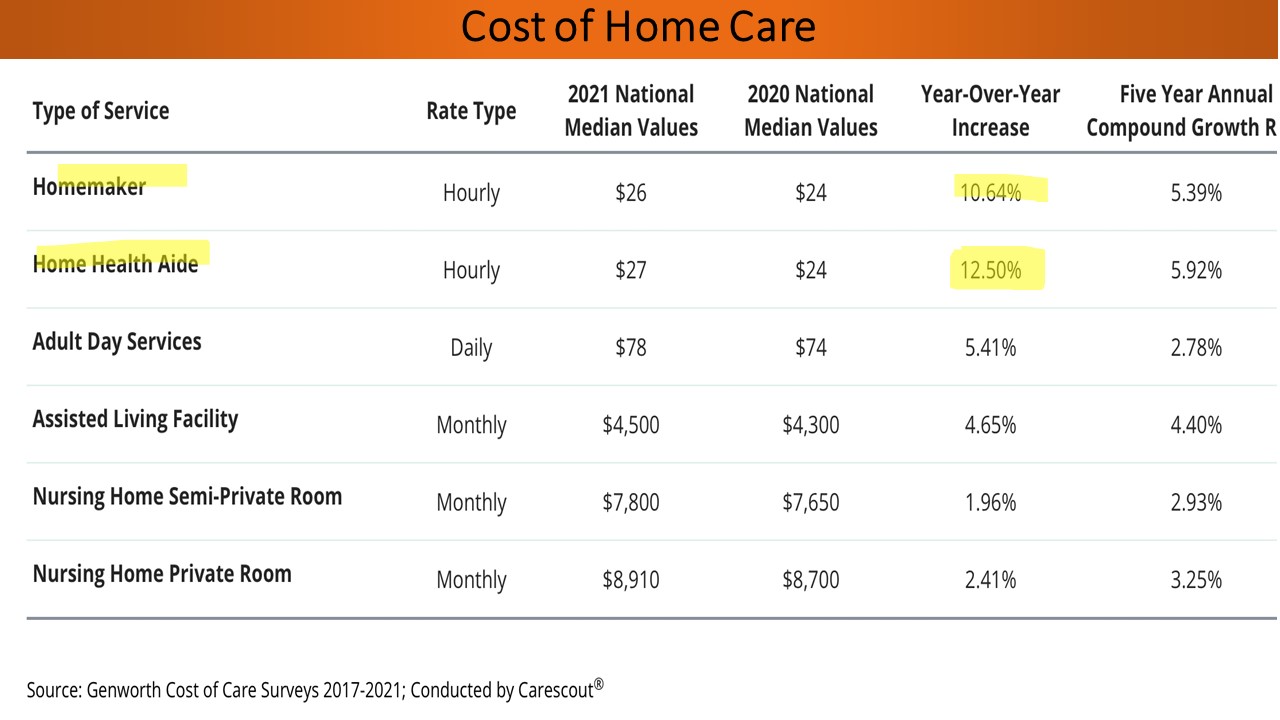

None of us are surprised by the increased cost of hiring help. Looking at the chart below, we see that for a homemaker, it has increased to 10% year over year between 2020 and 2021.

For a home healthcare aide who can participate in a telehealth conference or take blood pressure, costs increased by 12.5% in one year. Even looking at the last column on the right, the five-year annual compound growth, we are looking at, in terms of home healthcare, just flirting with six percent. And for a homemaker, well above five percent. It outstrips all of the other cost of care increases. I could assume a four percent increase for 2022. On an annual basis for either the home healthcare aid or maybe for an assisted living facility (ALF), you are looking at $60,000 as an average now, with no further increases, pulling from that pool of money every year.

There was a financial wealth management fellow, David Johnson, who works with a firm in New Jersey. It was worth sharing his quote with you. “You can borrow money to buy a home, a car, and for college. There is no bank on the planet willing to lend money to finance someone’s retirement.” And I want to add to that, “or finance their long-term care needs.”

Federal and State Initiatives, Studies, Commissions, Tax Incentives, and Legislation

The federal government and especially the states are facing a growing financial shortfall in funding the costs of care and extended long-term care.

Let’s start with the federal picture. For over 30 years, federal policymakers have put forth various public insurance plans for LTSS. (Remember, it is the government. So, I am using their terminology). None of these proposals, such as the 1988 Long-Term Care Assistance Act, the 1988 Life Care LTC Protection Act, the 1990 Pepper Recommendations, or the 1993 Clinton Health Security Act, made it out of Congress. More recently, on a federal level, the Class Act was passed as part of the Affordable Care Act. But it was subsequently repealed in 2013. So, the federal government has been unable to move forth with a national program.

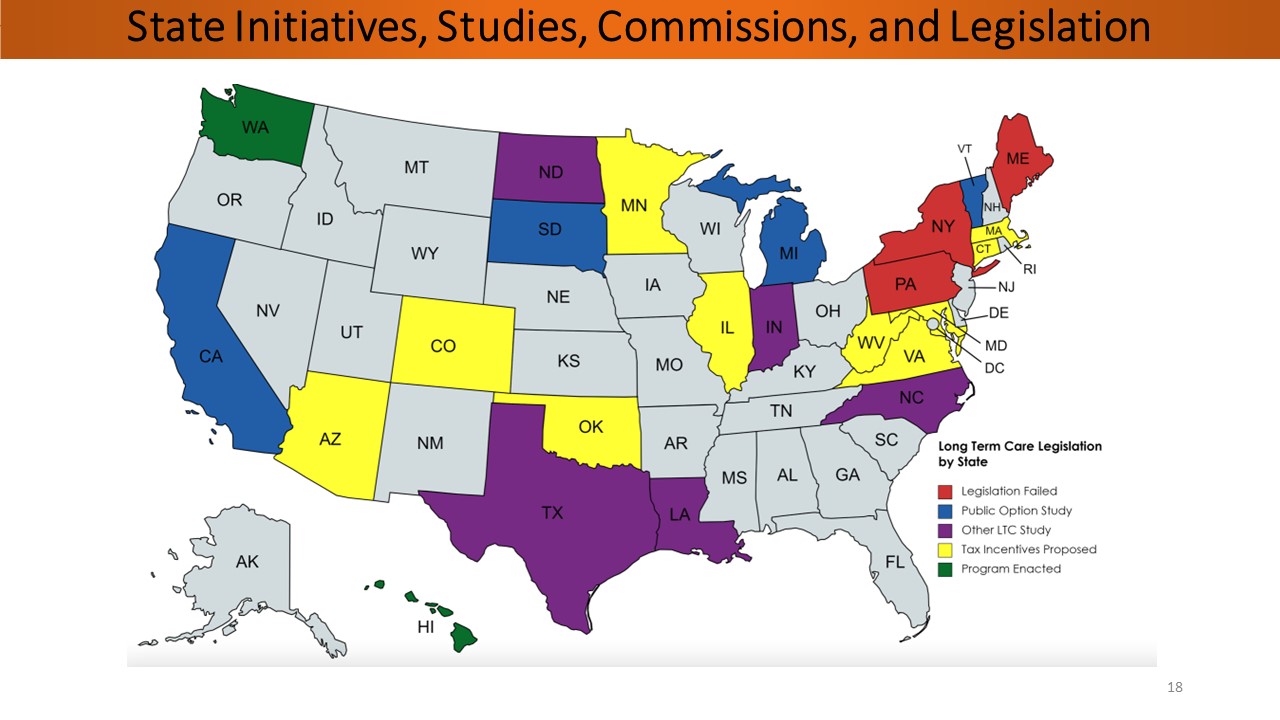

Now, let us look at what the states are doing. This map speaks volumes.

There are various and different approaches from coast to coast. As you can see, about 24 states are at some point in dealing with funding the long-term care needs of their constituents. Certainly, concern for the Medicare budget impact is beginning to affect state budgets. At NAIFA, I handled the limited and extended care planning centers. It is one of the centers where we have a subgroup called the Legislative Working Group (LWG), which is made up of quite a variety of carriers, brokerage agents, and advisors.

At NAIFA, we have a tool that tags long-term care issues. There were 27 tax and incentive bills in April 2023, and now there are 73. The most exciting part, for me, on this entire slide is the product innovation. We have eight different product innovations that help increase care in states, for consumers, for all of us, for FAs, and for those who want to see people plan. That is very, very encouraging.

I now want to turn to the only state that has enacted legislation. The WA Cares program in the state of Washington encountered several serious challenges, and it caused a delay in starting the premium assessment collection. I give the state of Washington much credit for bringing forth the rather serious financial shortfalls that states are facing in funding Medicaid., and let their constituents and residents know their concerns about the caregiving personal shortages and the need to coordinate caregiving services and supports. Because this is an employee-funded plan, employees had until November 1, 2021, to apply for an exemption. There was a tremendous number of people who applied for an exemption. This caused some of the carriers to curtail their program or to stop entirely to be able to issue policies by that November 1, 2021 deadline.

As of July 1, 2023, they are going ahead with the premium assessments or .58% of all W-2 income. There is no cap or limitation. When I say all income, I mean including commissions, bonuses, or stock options. If, for some reason, a client is growing in their career and moving up and up in the amount of compensation that they are earning, and they look at the maximum lifetime benefit of $36,500 (adjusted annually by the CPI), you could see why some of them wanted to say, “I want to compare private insurance to this publicly-funded program.” Thus, many of them did.

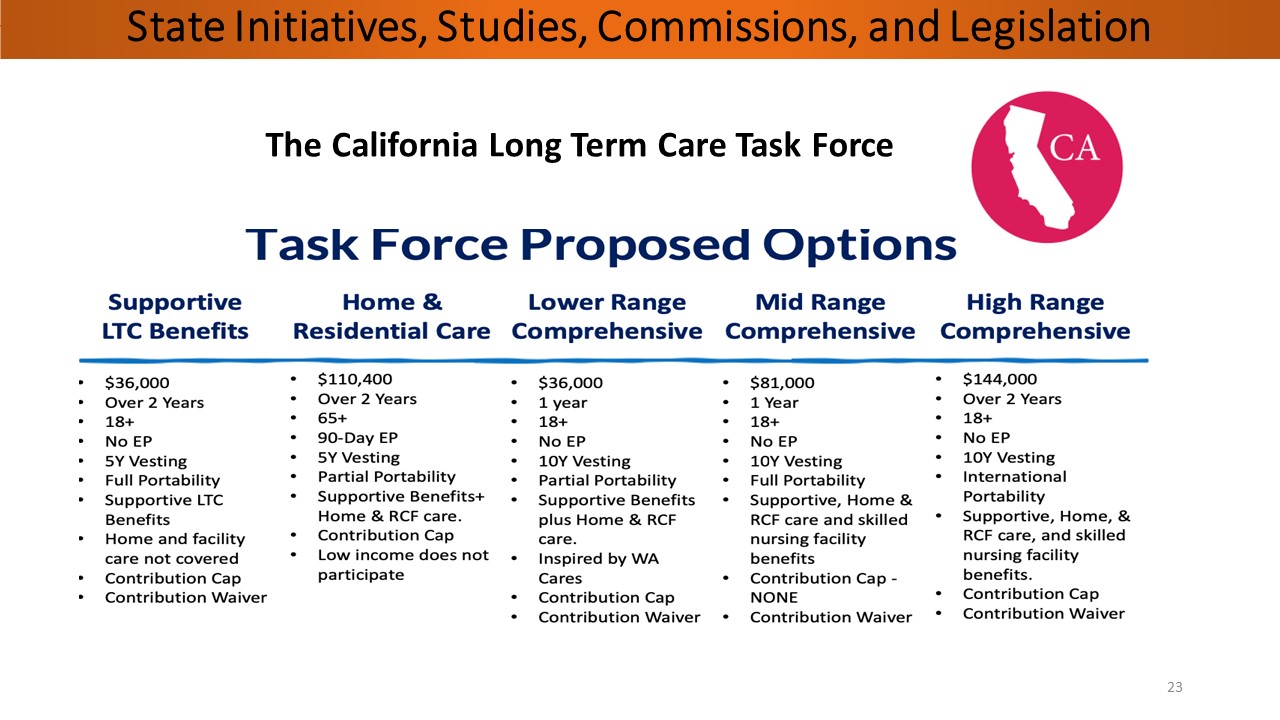

Now, I want to move on to the California Long-Term Care Task Force. Many people in California are worried about funding long-term care, especially if they did not start early or have yet to work with a financial advisor to know their options and how to go about it. Governor Newsom signed AB 567, establishing the California Long-Term Care Task Force. They have been charged with coming up with options to deal with the many complexities of a publicly-funded long-term care program.

They did learn a lot from the WA Care program. They tackled things like portability. In Washington, you have to live there to access the benefits. But only some people want to retire to the state they live in. They also tackled the ability of the self-employed or gig employees to participate, coordination with supplemental private long-term care policies, and the impact on various insurance riders. Here are the five proposals they came up with.

I want to call your attention to the home and residential care (see the third bullet down) because it is the only one that begins for a person aged 65 or older. For the others, eligibility to access the program benefits start as early as someone turns 18.

There are tremendous differences in these programs. However, they are being analyzed for the fiscal viability and sustainability of each of these options. And we expect to see a report around January of 2024.

Minnesota is one of the first states that spent quite a bit of time feeling that educating their constituents, their residents, was very significant in helping them to understand that they need to plan for long-term care or extended care. “Well, the problem is that we have many people who will live a long time. And they have not prepared in terms of their planning and the financing of that long life.” Minnesota issued a very comprehensive RFP. Three excellent companies are exploring various options for middle-income residents. They also created a Minnesota LTC consulting panel. I am pleased to mention that I am participating in that panel.

Maine decided to go a different direction and had a ballot initiative. They thought from early polling that this would pass. Their approach was to have it funded not only by individuals with income over a certain amount, but employers would also be funding it and a tax-on-investment income reduced by a payroll tax paid. Even though they thought the ballot would pass, it failed in November 2018. But it does not mean that other states may or may not consider that route.

Another way of approaching the whole issue of funding and helping and providing care is the way Hawaii approached it. They focused on funding the caregiver as opposed to the care recipient. It focused on expanding home and community-based services. Their program is designed so that a caregiver who worked a specific number of hours outside the home and a specific number of hours taking care of an aging person could receive a stipend to supplement their income. Of course, the program never got off the ground because it was supposed to start in 2019.

Working with Multigenerational Families

Now, let’s focus on the present. What approach will help you become a multigenerational financial professional? What will help individuals plan for family care? Remember, your client, your brother, or your sister is part of the family, no matter how they define family. As we move through life stages, family members care for one another. And caregiving does not happen in a vacuum.

What are you seeing in your practice? What are we seeing in our families? Family caregivers who provide care for 21 or more hours a week report that managing the caregiver’s finances is highly time-consuming. I had that experience.

Caregivers across all ages, among both high and low-income caregivers, among all marital statuses, and among those who had a choice and those who did not have a choice in providing care, report they have significantly worse health. Most caregivers recognize that it impacts their financial future.

So, how do you approach, start, and continue the conversation? Caregiving storytelling is most effective.

My story is about the Jones family. There are four generations in this family. And typically, the ones who approach needing care are silent agers. It is often a taboo family topic. Every generation worries about it. Many caregivers feel it will be a half-empty glass, if not worse. Storytelling is how you can make them feel that it is refillable.

Let’s look at how this would work. Jodie is a Boomer with parents who are part of the generation that doesn’t want to talk about aging. Her parents do not talk about it and how she is helping them. But neither does Jodie talk about it. It is not uncommon.

Many of your clients and friends may not tell you that they are or expect to be a caregiver. Often, a caregiver starts as a casual helper. But it morphs into a more significant role. And as it morphs into a more significant role, there is usually real difficulty in starting the conversation. This is the reason I developed the following three steps:

- The Care Guide

- The Care Squad and

- The Care Planning Team.

I do not care if you use any or all of them. But I hope you will personalize them, and one way or another, it will eliminate people trying to plan without discussing and without any cooperation.

Let us start with the care guide as a picture of the present and a window into the future.

Nicole, who is the granddaughter, discovers that Grandpa is very ornery. He is not going to participate. He says, “You know, I have been able to manage this for grandma and my whole life.” And she says, “But grandpa, that is the point. You have been in control. If you do not share anything, how will we know how to keep you in control or respect your wishes?” And so, Grandpa starts to think about that.

Then her brother says, “Well, what if it is you who needs care? Does grandma know where all the passwords are and the information and documentation?” Grandpa begins to internalize this and realizes that I must do something here. And then they close off with, “Let us all do it. Let us make this a family project.” And that pulls him over it.

The second step is the Care Squad. Grandpa says, “Okay. If we are all doing it, I will do it.” With the care squad, it is straightforward. When family members have an assigned responsibility, there is considerably less stress and more cooperation. Grandpa shares a story about a friend who told him that when family members visited him, they sucked all the oxygen out of the room because they did not have anything to contribute other than their stress.

The financial professional can gain a good deal of insight into the family structure by helping them create a care squad. For example, Grandpa’s grandson was promoted, and he moved away from the family. He can still have a responsibility. Bills are issued, reviewed, and paid electronically. Nicole, who took on a very big new project at work, can be in charge of the phone tree, which does not require her to take time away from her work. There is no doubt that technology will enhance our ability to age in place. But only some people are comfortable with it. And it can be expensive.

Grandpa’s grandchildren, for example, Nicole and Eric, want to use an app to store the care guide. Grandpa wants to go old school and stick it in an envelope. We are all Zoomed out. But it is a very helpful tool to build relationships with other generations.

Now, the care planning team and, in this case, Jodie’s husband, Jackson, have a long-term friend who lives nearby. As a care squad member, the friend is asked to handle Jodie and Jackson’s home while they are away. The financial advisor gets to know Jackson’s friend, who turns into, of course, a potential client. He also gets Jackson to participate in the Care Planning Team (CPT). The CPT offers the financial professional an opportunity to present and assign different options to different CPT members. For example, Eric has life insurance, but he rides a motorcycle and is the sole breadwinner with two young children. Money is tight. So, the financial advisor can suggest that he look at a term life product with accelerated death benefits, which could be a good fit. The CPT and the financial advisor can also introduce micro-learning modules or gamification and engaging information exercises.

What you are doing during this whole storytelling process is looking for motivators. You can pick them up by listening carefully to what they focus on in the story. How would they change the story? How would they improve whatever was going on in the story? It is a very telling and not difficult way of improving relationships, growing generationally, and, of course, helping people plan.

I am going to quickly, because of time, whip through this cornucopia of planning options. We do not have time today for an in-depth review. However, I am familiarizing you with the expansive options that suit almost any client’s financial or personal healthcare needs. If it is insurance, there are lots of different types. Work groups and workplaces have increased, obviously due to the prospect of publicly-funded long-term care. And life insurance with riders and annuities with riders, I want you to be very careful to understand what those riders do and do not do.

Plan for Care – Avoid Crisis Funding

Can the entire benefit accelerate for long-term care? You need to truly understand whether it is going to be underwritten at the time of claim or whether the benefit is going to be established when the contract is signed. What about specific health concerns? What about some people who do have health issues like veteran’s benefits? Grandpa, as it turns out, qualified for health benefits through the VA. But where they access them and, how long, what type of benefit, can be very complicated. While Grandpa qualifies, Jodie’s husband Jackson, who also served, does not qualify. So, it would be best to look at some things you had not thought about.

The HECM mortgage (home equity conversion mortgage) has come into play now as a funding source for long-term and extended care. Why? Well, there is $12 trillion tied up in home equity. It may be a part of good funding and good planning. You must become familiar with more and more of these potential opportunities for funding care.

Shadow Caregiving System Key Takeaways

Whether you are a sole ager yourself or whether your client is a family member, and no matter how you define a family, they are and will become part of the Shadow Caregiving System.

The Shadow Caregiving System will impact retirement and investment plans. Use the three steps to discuss extended and long-term care planning. Do it before it becomes a crisis, which will limit the options and can have very long-reaching consequences. Not just for the generation getting the care, the care recipient, but also for the caregiver and the generations beneath them.

We know that states recognize the increasing, if not unmanageable, cost of care. That is why we are going to have to follow what is happening in state legislations, programs, and task force initiatives so that you, your friends, your clients, and your family are well-informed and have a chance to figure out what is the best plan for your situation.

There are only planning options that are within reach if you look at the correct ones for every client and every budget. While one size does not fit all, this is an opportunity to help individuals, businesses, and family members understand their options. Of course, as a sidebar, it will help you to become a facilitator and grow your practice as well.

I have mentioned my storybook for families, How Not to Pull Your Family Apart: A Practical Guide to Caregiving and Financial Stability, which became a best seller. And I think it is because of the subtitle, “Caregiving and Financial Stability.” That will be a book that some financial advisors have sent to their clients and asked them, “Do you want to talk about this? Do you see yourself stepping into any of these character’s shoes?”

My first book, How Not to Tear Your Family Apart: 3 Simple Steps to Start Critical Conversations and Help Your Family and Aging Parents Plan a Financially Stable Future is more of a textbook and is written for advisors.

Both books are available through Amazon and Barnes and Noble.