Longevity is fixed expenses; lifestyle is discretionary expenses; liquidity covers contingencies, and legacy covers legacy.

How do you deploy assets to best meet goals in an efficient and effective manner?

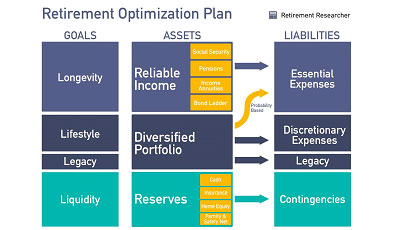

This diagram shows how people traditionally think of things, with home equity falling in the “Reserves” category. It doesn’t necessarily have to be a reserve.

Uses for Reverse Mortgages

How can a reverse mortgage be used? There are four different categories of uses with 14 different ideas – the spectrum of potential reverse mortgage uses – ranging from uses that tend to use the home equity more quickly, to items that will tend to use the home equity more slowly, or possibly never at all.

Portfolio and debt coordination for housing

- A reverse mortgage can be used to pay off an existing mortgage to get that expense out of the budget. It can make that retiree less vulnerable to sequence risk by taking that fixed mortgage expense out of the budget, which helps to reduce the withdrawal rate. That’s a way to manage sequence risk.

- Transitioning from a traditional mortgage to a reverse mortgage is subtly different from just paying off an existing mortgage. Basically, you could voluntarily make your mortgage payments to pay down the loan balance on the reverse mortgage, but you would then have the flexibility that if there is a market downturn or if something else comes up, you could skip payments. You don’t have to pay that loan balance down in advance, and you have more flexibility than with a traditional mortgage where you don’t have the option to not make a monthly payment.

- Home equity could be used to fund home renovations to better allow for aging in place, such as a bathroom or a bedroom on the first floor, a walk-in shower, a handicap-accessible entrance, etc., that allows that person to stay in that home for longer, because most retirees do tend to want to stay in their homes.

- A “HECM for Purchase” is where a reverse mortgage can be used to purchase a new home.

Portfolio coordination for retirement spending

- Spend home equity first. You’re essentially trying to let the portfolio grow for longer before you start to spend from it. If the portfolio doesn’t grow, you’ve created greater risk for yourself.

- Less risky strategies have some sort of mechanism to coordinate spending from the reverse mortgage on occasion – perhaps when the portfolio is in bad shape however that may be defined – to help reduce sequence-of-returns risk by reducing the need to take distributions when the portfolio is down, or when assets would need to be sold at a loss.

- Reduce the need for portfolio withdrawals and turn on the tenure payment, which is a monthly income. It behaves a lot like an income annuity with one very important caveat that needs a big asterisk, which is that it may not be a guaranteed income for life; it’s a guaranteed income for as long as the individual is eligible for the reverse mortgage. Eligibility basically means living in the home and making sure they pay their property taxes and keeping the home in reasonable shape with homeowner’s insurance and so forth.

Funding source for retirement efficiency improvements

- For a retiree to pay a little bit more in the short term to have better outcomes in the long term, they need a resource to be able to pay those short-term higher expenses to benefit over the long term, and that’s where the reverse mortgage can fit. Rather than purchasing an income annuity, use a tenure payment from a reverse mortgage.

- Delaying Social Security is a great way to extend retirement sustainability. The reverse mortgage can be used as a source to fund the ability to delay Social Security.

- Roth conversions and tax bracket management is about making sure you fill up the lower tax bracket so that you can avoid ever falling into a higher tax bracket in retirement. That might involve paying a little bit higher taxes in the short term to have significantly less taxes in the long term.

- A reverse mortgage could be used to help fund traditional long-term care insurance premiums to not lose the policy – not necessarily to buy a new policy. They tend to get lapsed a couple of years before they could have been used, and part of that reason may be cognitive decline, but another reason for that may just be traditional policies have seen large increases in their premiums, and maybe the retiree really doesn’t feel like they can afford it at that point.

Using the reverse mortgage as an insurance policy

- Opening a reverse mortgage early on to let the line of credit grow, and only then spend from it if the portfolio is depleted to cover retirement spending.

- A reverse mortgage could be used to protect the value of the home. Once it’s opened, the initial appraised home value is relevant for how much the initial line of credit can be, but after it’s set up, the line of credit grows at a variable rate that’s completely unrelated to the value of the home. Reverse mortgages are non-recourse loans, so if at the end, the loan balance due is greater than the appraised value of the home, the borrower or their estate is not on the hook for paying that difference. That’s what the mortgage insurance fund is there for. It can create a potential windfall, and in that regard, it’s a put option on the home.

- Having the line of credit open for spending shocks, to afford things like in-home care. It’s not to pay for a nursing home, because you have to live in the home to be eligible for the reverse mortgage, but to pay for in-home care to avoid having to go to a nursing home, or to pay for other health expenses. There are also some interesting ways to use a reverse mortgage as part of a divorce settlement.

How Does a HECM Work?

(Editor’s note: It’s important to understand how reverse mortgages work. Please see Wade’s book, available at Amazon.com for more detailed explanations than what is covered below.)

The image of reverse mortgages has been changing. They still often have a negative image, but there’s been a lot more positive press coverage over the last couple of years. In the old days, reverse mortgage stories were usually focused on someone feeling like they were ripped off by the reverse mortgage. More recently, the story is much more that this can be a helpful part of a responsible retirement income plan.

There has been an effort in public policy to eliminate some of the problems that did exist in the past. The HECM program, Home Equity Conversion Mortgages, is run through HUD (The Department of Housing and Urban Development) and the FHA (Federal Housing Authority). They developed the rules around the program. They have worked over the last couple of years to slow down the rate of borrowing from the reverse mortgage so it’s harder to deplete the home equity for questionable reasons.

They also have created protections for non-borrowing spouses who are too young to be a borrower. In the past, if the borrower left the home, that left the spouse in a bad situation. There’s now protections for that.

With a HECM, the home title is never turned over to the bank. That’s a common misunderstanding – the idea that you lose the title to your home with a reverse mortgage. That was never the case.

One other point: There is an ongoing concern that the initial costs of setting up the reverse mortgage could be in excess of $10,000, but the ability to securitize the loans has made it possible for lenders to lower the up-front cost dramatically in the past couple of years. It is now possible to get a reverse mortgage set up for much less than someone may have seen in the past, but it does require shopping around. There’s not a central clearinghouse to see reverse mortgage quotes, so you do have to talk to different lenders, but it is possible in this day and age to get a much lower up-front cost on a reverse mortgage.

The borrower needs to be 62 or older. They need to have full equity in the home; there can’t be any other lien on the property. They can use the reverse mortgage to pay off the balance on an existing mortgage if there’s enough funds within the reverse mortgage to do that.

They need to demonstrate that they have financial resources to cover property taxes, homeowner’s insurance, and home maintenance. They need to go through a counseling session with a counselor approved by the FHA. They need an approved FHA home appraisal. It does have to be the primary residence, so a reverse mortgage can’t be used for a second vacation home.

The lending limit is based on FHA rules at$636,150, which is to say it’s not that you can’t have a reverse mortgage if the home is appraised as worth more than that, it’s just that if your home is worth more than this $636,150, the reverse mortgage is based on the smaller of the home’s value or this number.

Now, there’s a lot of jargon for reverse mortgages, but the keys are:

- the principal limit, which is the borrowing amount that you’re eligible for

- the principal limit factor is the amount you can borrow as a percentage of the home value

- the expected rate is the interest rate used to determine how much you’re initially allowed to borrow

- the effective rate is the variable interest rate that will grow the principal limit in subsequent years.

So, the expected rate determines the initial principal limit. The effective rate determines the subsequent growth of that initial principal limit.

The Benefit of Opening a Reverse Mortgage Early in Retirement

The reverse mortgage is basically the only retirement income strategy that benefits from lower interest rates, so with HECMs, interest rates are much more important than age. With everything else, lower interest rates make retirement more costly, but because it’s essentially a present-value calculation, lower interest rates for HECMs mean a higher present value, or a higher percentage of the home’s value, can be borrowed.

On my website, I have a calculator that can be used to play around with different home values, interest rates, and so forth to get an idea of how much can be borrowed from a reverse mortgage, and also tenure payments and term payments if those options are chosen.

The key is: What if you open it but you don’t borrow? The amount of credit you subsequently will have grows over time that the loan balance would have grown. This equation always holds, and this is the secret sauce for why all this recent research is showing the value of a reverse mortgage line of credit as part of a retirement income plan.

It’s always going to be the case that opening the line of credit early will allow you to have more credit available than waiting until later to open the line of credit. After opening the line at age 62, at about age 87, the line of credit can actually bigger be than the value of the home. That’s where this idea of a non-recourse loan comes into play. The amount due is never going to be larger than the value of the home, but if somebody waited – this is a more extreme case – until after age 87, they’re getting a windfall if they then take from the line of credit in excess of the value of the home.

Again, low interest rates favor HECMs. The lower expected rate leads to a larger initial principal limit, and even though the subsequent principal limit growth would be lower because interest rates are low, if interest rates do eventually increase, that will accelerate the subsequent growth of the principal limit.

Portfolio Coordination for Retirement Spending

This is where most of the research has been focused since 2012.

In 2012, the Journal of Financial Planning published two articles written by two different sets of researchers who did not know each other. Basically, both had the same idea at the same time, and that idea was the thesis that strategic use of a reverse mortgage standby line of credit can create retirement income efficiencies through its contribution to managing sequence-of-returns risk in retirement. They used different strategies to draw from the line of credit, but they both basically had some sort of mechanism in place where if the portfolios seem not to be in good shape, then draw from the reverse mortgage and draw from the portfolio when it’s in better shape.

Barry Sacks and his brother came first, and then later in the year, this team from Texas Tech University – John Salter, Shawan Pfeiffer, and Harold Evensky – making the very similar point, but with a more sophisticated mechanism for deciding when to draw from the reverse mortgage.

Last year I published an article in the Journal of Financial Planning that put a lot of this past research together, comparing everything with one set of market return assumptions and so forth. We’re now going to look at seven different strategies for using a reverse mortgage:

- The first ignores home equity. You’re obviously going to run out of money sooner if you ignore home equity, but that just gives us a baseline.

- The conventional wisdom is home equity as a last resort: Don’t touch reverse mortgage until your portfolio’s depleted. Then, open the reverse mortgage. The point here is when you do it, you’re going to have a lower line of credit than otherwise, but this is the only one of these remaining strategies when you don’t open the line of credit as soon as possible. You wait until you first need to use it.

- The final five strategies all open the reverse mortgage at the start of retirement, and then you can:

- Spend home equity first

- You could use the Sacks and Sacks coordination strategy, which is simply that when the markets are down for a year, in the subsequent year, you draw from the line of credit. If markets were up this year, then next year, you draw from the portfolio.

- Another possibility is the Texas Tech coordination strategy, which is where you create a glide path of how much wealth you should have each year of retirement to make sure your wealth lasts long enough, and then if your actual wealth exceeds that glide path, you draw from the portfolio. You can even pay down your loan balance if you’ve drawn anything from the reverse mortgage before. When your remaining wealth falls below that critical threshold, then you draw from the reverse mortgage instead of the portfolio.

- Use home equity last. So, a common question is, “How is ‘use home equity last’ different from ‘home equity as last resort’?” The answer is they’re spent down in the same way. The reverse mortgage is spent at the same time and in the same way, but the difference is “use home equity last” opens the line of credit at the beginning of retirement. “Home equity as last resort” waits until the portfolio is depleted before opening the line of credit.

- The final option is to set up a tenure payment on the reverse mortgage.

Comparing the seven strategies over 40 years for a 4 percent desired withdrawal rate post-tax, for a $1 million portfolio and $500,000 home:

- Distributions from the IRA are taxable, so if the full amount is taken from the IRA, it would be a 5.33 percent withdrawal rate to pay taxes at a 25% rate and then have 4 percent left over. So, that’s definitely higher than a safe withdrawal rate and you’re just spending from the investment portfolio. It’s the only one of these strategies that’s not comparable because you still have a $500,000 asset that you haven’t touched.

- The next six strategies are all comparable because they use both assets, just in different ways.

- The conventional wisdom is the worst way to coordinate spending with a reverse mortgage. Using home equity as a last resort, waiting to open a line of credit, leads to the worst improvements and worst probability of success. Opening that line of credit early really pays off to improve probabilities of success in retirement.

- The other five strategies are all just different ways of opening the line of credit at age 62, but different ways of spending from it. “Use home equity first”, the tenure payment, and the coordinated strategies behave in a very similar way. “Use home equity last” gives you the most potential to have the line of credit grow before you first tap into it, which ultimately helps to pay off with the highest probabilities of success because then, when the portfolio is depleted, you have more line of credit to continue to draw from.

Takeaways for Advisors

- The conventional wisdom – the idea of opening a reverse mortgage only after everything else has failed – hurts retirement sustainability. HECM should not be a last resort.

- The media coverage is more positive. You will have more clients asking you about reverse mortgages.

- The strategic use of the HECM program can improve retirement sustainability and support a larger combined legacy. It works because it helps to manage sequence-of-returns risk, and because of that growing line of credit.

- Low interest rates favor the reverse mortgage, unlike pretty much every other retirement strategy.

- HECM is something that’s really going to be helpful to the middle-class/middle-income market.

- It can be beneficial to wealthier individuals, too, but it’s comes down to the ratio of the value of the home to the value of the portfolio. If someone has a $6 million IRA and a $600,000 home, they can still benefit, but the benefits are increasingly greater if they have a $500,000 portfolio with a $500,000 home. The ratio of those two numbers is what matters, and the bigger of the value of the home relative to the portfolio, the greater the benefit of the reverse mortgage.

The HECM definitely has the potential to help the middle class, and responsible use of it can improve retirement income efficiency.