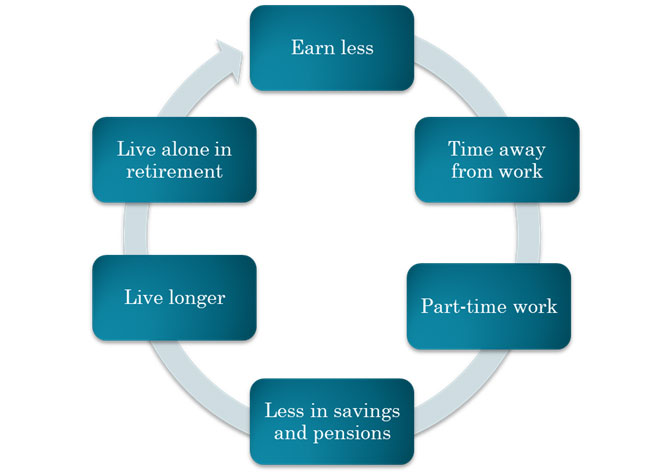

Women usually end up taking on most of that care. This results in less savings, less opportunities for pensions, defined contribution plans, other plans they might have had access to at the workplace.

Women live longer, anywhere from two to five years depending on which statistics. Because they end up living alone in retirement, by the time they’re in their 80s, they end up living in poverty. That’s the sad story.

How Divorce and Widowhood Affect Women in Retirement

Two devastating effects for women are often divorce and widowhood. Early divorce is something that women may never catch up from but at least there is more opportunity if divorced when younger than with grey divorce. Grey divorce is now a key issue for a lot of older people. The numbers for people divorcing post age 50 is double; 27% of grey divorced women are living in poverty.

If the divorce lawyer or mediator is not primed on learning about retirement issues, clients may lose out in many ways, such as survivor benefits, which are pretty important. Getting people primed on some of the things to be asked for or getting a divorce expert to consult is really important. Often, people just want to get through divorce and especially women often put their kids first. It’s hard convincing them that maybe they shouldn’t keep the house which they’re not going to be able to afford in a couple of years, that they have to pay attention to the assets that will actually give them cash later on. Make sure you know the rules, because every state has a different rule on splitting spousal benefits.

Half of all women who are widowed over age 65 end up living ten years longer, 15 years more is not uncommon. It’s something that needs to be prepared for. Women lose one Social Security benefit or 50% of the pension. Planners who help people look at the realities of the future are doing a great service. If you’re relying on a retirement system, know the rules. There glitches that can keep people from getting benefits.

All of this should be an ongoing conversation so that there’s full disclosure with the children, other family members, or the financial manager; other even than your financial planner, because many times people have benefits they don’t even know they have. You hear the stories that people find out that the parent actually bought long-term care insurance but nobody knew.

With pensions, know the system that you’re relying on. A lot of times there can be more than one company plan, since people change jobs all the time. An agency in Washington, the Pension Benefit Guarantee Corporation, has a list of company plans. Search their database and find if you were ever covered by a plan.

Make sure that clients are up-to-date on what they’ve earned throughout their lifetime, and whether either spouse is vested in a traditional plan or any matching contributions. A lot of times people leave a job and don’t realize that they needed to stay another year, so they weren’t eligible for the matching contributions.

There are situations where the traditional plan is integrated with Social Security, which may mean the earnings are subtracted, resulting in a lot less than expected. That’s true in the airline industry as well as retail. Unfortunately, most people only ask the question when they’re getting closer to retirement, or leaving, “Oh, I wonder about that retirement plan, if I’m covered or if my spouse is covered?” Knowing the rules of the systems is key, depending on the state laws and how benefits are divided.

People tell me, “My ex-spouse is about to retire and I need to know what I should do to go get part of his retirement benefits.” This needs to be part of the property agreement. If it isn’t written into the agreement with a court order stating the right, you will not receive those benefits. Knowing where the benefits are coming from will make a huge difference in what somebody will be collecting for the rest of their life. It’s good to have the benefits valued by an actuary or an accountant.

How Caregiving Affects Women’s Retirement Security

Caregiving is a huge issue for many women, who frequently take on more of the caregiving responsibility. There are many caregivers who just take leaves of absence. Family Medical Leave, depending on where you’re working, is obviously an opportunity, but still many get so overwhelmed they just end up leaving their job totally, one of those shocks that has a pretty devastating effect because it’s not so easy to get back into the system once you leave.

All of this ends up having big financial consequences for caregivers. There are a number of bills in Washington trying to give new tax breaks to caregivers because of their out-of-pocket costs. Caregivers who take care of elderly parents are much more likely to end up living in poverty. When we talk to women, we say to them that they’ve got to share this experience with others in the family.

Caregiving has costs that are outside of the normal thinking: the cost of losing a job plus losing the opportunity to save and invest and compound returns, the ability to do other things such as finance home improvements that can increase the resale value of a home, the loss of promotional opportunities. We all know those stories.

Many assisted living residents believe that Medicare or somebody else is paying for their long term care, and it’s most often the adult children that are paying for a good part of their assisted living care. There are filial responsibility laws such that some states are talking about going after adult children if they haven’t stepped up to the plate and helped parents, so the state is having to pay for them. There are 28 states now that have these laws.

Develop a family strategy to get people involved early. Set up a personal care agreement on how to manage caregiver responsibilities within the family, and make it clear who’s paying what so that one person is not bearing the burden of the whole care. Caring.com is a good resource for information needed to help avoid some of the money mistakes that caregivers make, and our own website which includes sample forms, www.wiserwomen.org.

Mary Beth Franklin – Why Proper Claiming of Social Security is Crucial to Women

Social Security benefits are incredibly important for your female clients. Of people 85 and older, two third of Social Security beneficiaries are women. Nearly half of all elderly unmarried women, and that includes those who are divorced and widows, rely on Social Security for 90% or more of their income, meaning about $1,200 a month as total income.

How Women can Collect Social Security Benefits

Women can collect Social Security benefits in several different ways:

- They may have benefits they have earned on their own work record.

- If they are married or an eligible divorced spouse, they may be able to collect as a spouse.

- If they are the caregiving parent of a child who is under 16, or permanently disabled and their spouse is collecting a benefit, they may be able to collect a spousal benefit regardless of their age if they’re taking care of these minor or permanently disabled children.

- If they are a surviving spouse or an ex-spouse, they’re entitled to survivor benefits.

Strategies for people to claim based on age and marital status:

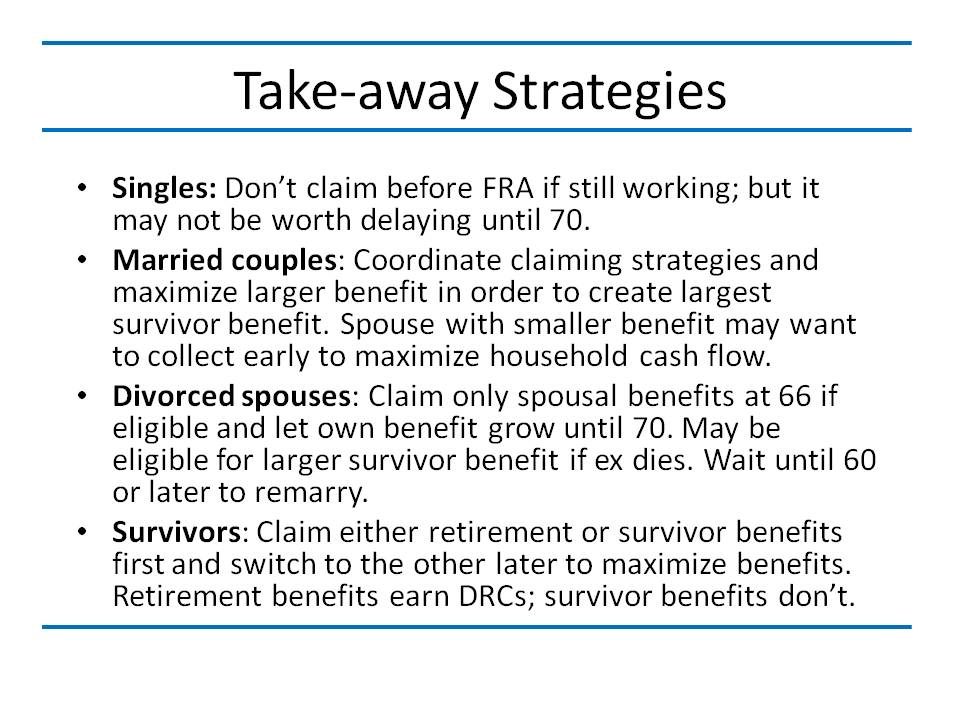

- If you are entitled to Social Security benefits as a spouse or on your own record, you can claim benefits as early as age 62, but they are permanently reduced.

- If you are entitled to your own record and that of a spouse, and you claim before your full retirement age, Social Security must pay you your own benefits first, reduced for early claiming. If your spousal amount is higher, they will layer that extra amount on top, also reduced for early claiming.

- If you’re entitled to benefits as a surviving spouse or surviving ex-spouse, you can claim benefits as early as age 62, reduced compared to claiming at your full retirement age.

Full retirement benefits are available at age 66, 100% of what you have earned on your own record or up to 50% of your spouse’s benefit for people who were born from 1943 through 1954. If you’re younger than that, your full retirement age is higher. It could be as high as 67 if you were born in 1960 or later.

If you claim Social Security benefits before your full retirement age, and you continue to work, your benefits may be reduced or completely eliminated by the earnings cap. There’s a huge incentive to delay. For every year you postpone claiming Social Security benefits beyond your full retirement age up until age 70, you earn an extra 8% per year. It may make more sense for some people to tap their 401(k) or their IRA first as a way of allowing them to afford to delay collecting Social Security benefits until they’re worth the maximum amount at age 70.

If you claim Social Security benefits before your full retirement age and have earnings from a job – in 2016, if you’re under full retirement age and you earn more than $15,720 annually, you will lose $1 in benefits for every $2 earned over that limit. If you earn more than $47,000 you are going to forfeit all of your benefits. Once you reach your full retirement age, which is currently 66, any benefits that you have forfeited to the earnings test in prior years are effectively added back in. It’s not a permanent penalty but if you claim before full retirement age and continue to work, not only will you temporarily lose benefits but you may blow the opportunity to use one of the remaining claiming strategies, and you must wait until the age of 66 to do that.

There is a higher earnings restriction in the year you turn 66. In the months leading up to your 66th birthday, you can actually earn up to $41,880 and you would only lose $1 in benefits for every $3 earned over that limit. Once you get to the age of 66, you can collect Social Security benefits even if you continue to work and not forfeit any Social Security benefits through earnings cap.

Women and Social Security Spousal Benefits

There were two major changes to Social Security claiming rules as a result of the Bipartisan Budget Act of 2015:

- Eliminated the strategy known as “File and Suspend” allowed people once they’ve reached the age of 66 to file for their benefits and then immediately suspended them, which means they didn’t receive pay. But this triggered a benefit for a spouse or possibly a minor dependent, or a permanently disabled adult child.

- Ability to claim only spousal benefits when you turn 66, and allow your own benefits to keep growing up until age 70. That claiming strategy of filing for spousal benefits only will continue to be around for another eight years, but it is only available to people who were born on or before January 1, 1954.

Beginning April 30, 2016, people can still suspend their benefits at 66 but no one (spouse or child) can collect benefits during the suspension. Also, the lump sum payout option is no longer available. This is a loss for single people who were the ones who were most likely to say a couple of years later, “I have a medical condition. I may not live a long time; please pay me all my suspended benefits in a lump sum.”

I want to stress how valuable this remaining creative strategy of being able to file for spousal benefits only is to both currently married clients and eligible divorced clients. To be eligible as an ex-spouse to collect on a former spouse’s record, you must have been married at least ten years, divorced, and currently single. As a result of this new legislation, only people born on or before January 1, 1954, will be able to claim spousal benefits only when they turn 66.

Here’s an important planning point. Within currently married couples, only one spouse can claim spousal benefits. The other spouse either has to be collecting benefits, which triggers a benefit for the spouse, or have filed and suspended before the April 29 deadline.

What’s different for divorced couples is each ex-spouse can claim on the other spouse’s earnings record. They had to be born on or before January 1, 1954 in order to exercise this strategy of claiming spousal benefits only when they turn 66. This is a great opportunity to be able to collect only spousal benefits which are worth 50% of the worker’s amount while their own benefits continue to grow.

Social Security Benefits for Single, Divorced and Widowed Women

For single women, just like single men, in order to be eligible for Social Security benefits, you must work at least ten years in covered employment, meaning you’re paying FICA payroll taxes. But your actual benefit amount is based on your top 35 years of indexed earnings. It’s not necessarily sequential; it’s the top 35 years. If you worked fewer than 35 years, Social Security is going to consider those years zero years.

The important thing to note is that regardless of your age, even if you continue to work beyond your full retirement age, and you have earnings from a job, it is quite possible those earnings will be added into the calculation and result in a larger Social Security benefit in the future.

If your full retirement age is 66 and you claim at 62, your benefits will only be worth 75% of your full retirement age amount. If you claim benefits before full retirement age and continue to work, those benefits could be forfeited to the earnings cap.

The maximum benefits are available at age 70. They could be worth 32% more than full retirement age benefits. But there is a breakeven point. You’re probably going to have to wait until about 83 to make it worthwhile to have waited until age 70 to collect. Someone who has longevity in their family may want to delay. It’s an easier decision for married clients because they’re spreading that breakeven point over two lifetimes, and someone’s going to end up with the survivor benefit.

That is not the case for single women. Married women, if they wait until 66 and were born on or before January 1, 1954, have this incredibly valuable opportunity of being able to claim only spousal benefits at 66 and switching to their own at age 70. Even if someone collects retirement benefits early and those retirement benefits are permanently reduced, they are still entitled to survivor benefits if their spouse dies. And if they are at least full retirement age at the time they collect those survivor benefits, they will still be worth 100% of what their late spouse was collecting or entitled to at time of death.

In fact Social Security has more than 2,700 rules that govern benefits. One of the many exceptions is that if you’re divorced at least two years, and if both ex-spouses are at least 62 years old, you can claim on your ex-spouse’s record even if he or she has not yet begun collecting. That’s known as being an independently entitled spouse to benefits.

Don’t forget the kids. Many people do not realize that if a parent is claiming a Social Security benefit or disability benefit, and they have a minor dependent child defined as under age 18, or 19 if still in high school, or a permanently disabled child, that child is also entitled to a benefit worth 50% of the worker’s benefit amount. However, the entire family is subject to something called the Family Maximum Limit, generally 150 to 180% of the worker’s full retirement age amount. If the family breaches that limit, the dependent benefits will be reduced on a pro-rata basis but the worker’s own benefit is not affected.

Survivor benefits are the most important thing for planning in married couples. The main goal is how to maximize the survivor benefit, by having the spouse with the higher Social Security benefits wait at least until age 70 to collect the maximum benefit.

Generally if you remarry, you lose the right to collect Social Security benefits on an ex. But if you wait until age 60 or later to remarry, you still lose the right to collect spousal benefits on a living ex, but you retain the right to collect survivor benefits on a deceased ex.

Anyone who collects any type of Social Security benefit has a right to change their minds within the first 12 months of claiming benefits. They can withdraw their application for claiming benefits, but there’s a catch: They have to repay any of the benefits they have received. But the benefit is it wipes the slate clean. It’s as if they had never collected they would be able to start benefits as if they had never claimed, at a higher rate.

If you miss that 12-month window, there’s another opportunity, but you have to wait until the age of 66 to suspend benefits. You do not repay them. But you can start earning the extra 8% per year in delayed retirement credits. You can’t collect anything during the suspension, and no one can collect on your record. But it’s a great way of rectifying an early claiming decision.

If you have any questions, everything I just said here is available at investmentnews.com/MBFebook.

Betty Meredith, CFA, CRC®, CFP® – A Case Study: Options for Improving Women’s Retirement Security

We can improve the retirement security of women.

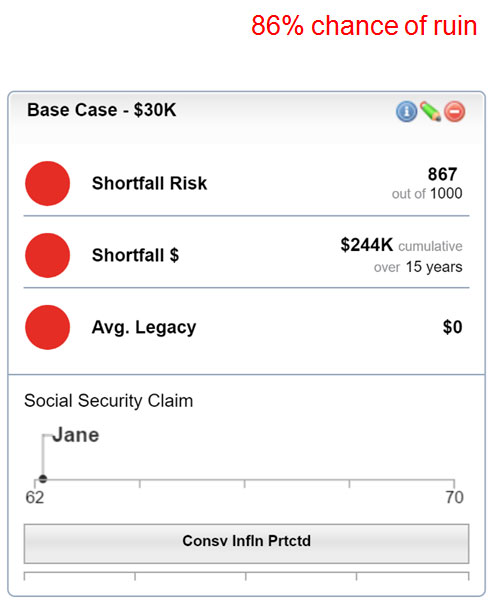

We have a case study with Jane Davies, age 62. She was married 30 years and she’s been divorced for eight years. She makes $40,000 a year in income, and she’d like to have $30,000 in retirement that will include her benefits of her ex-spouse’s Social Security. She has $248,000 in assets and her current allocation is 60% bonds, 30% stocks and 10% cash so she’s conservatively invested.

Her home is valued at $200,000, is paid off, no reverse mortgage. Her ex-husband earns around $130,000 so she’ll collect his Social Security benefits, half of her divorced spouse benefit and then his survivor benefit when he passes. The assumption is that he passes at age 86. She is in good health and no children.

What are her risks? She could live a long time and possibly have healthcare issues down the road without long-term care. She doesn’t have kids that she can rely on. She’ll have issues with inflation over time increasing her expenses. And she’s earning less right now so her own Social Security benefits and ability to save will be lower. She wants to retire at 62.

How would it help if she increased her portfolio risk from conservative to moderate? That tends to be the first line of attack, and might not be the best thing. We’ll look at what if she delayed her Social Security to age 66, then moved it to a more moderate asset allocation with 40% of her portfolio – 20% in a fixed annuity, 20% in the immediate annuity. The higher lifetime income from the annuity because of the mortality credits, and the reduced sequence of returns risk could really help because she doesn’t have to take as much risk with the rest of her portfolio.

Another option is if she works until age 70 and collects Social Security later; still collecting it at 66 but if she phases her income maybe where she has more income in the first phase and lower in the second. We will be able to reduce her risk tremendously if we do these things, using Discovery Software for this demonstration.

Look at the upper right hand corner where we have the “percent chance of ruin”. If she were to retire at 62 and take the reduced Social Security benefit at 62, she has an 86% chance of ruin. She would need $244,000 more than she has in her portfolio to live on and she would have nothing left over for legacy. If the first thing she does is increase her portfolio risk from conservative to moderate, she can reduce her chance of risk from 86% to 69% again using 4.5% withdrawal, which is good, but still way too much risk for her to take. If then she delayed her Social Security to 66, she gets the biggest drop from 86% chance of ruin down to a 10%, allowing Social Security to build. She gets the delayed retirement credit and she’s not taking out of her portfolio any earlier as well.

The Income Discovery software used in these models has the ability to run an optimize scenario. If the client wants to retire at 62 the software can identify what would be the best solution, for example. In this case, it assumes that she would take her Social Security at 66, still work, and purchase a fixed index annuity and a SPIA with 40% of the assets being the single premium immediate annuity. Then she can go back and reduce the rest of her portfolio risk from moderate to more conservative asset allocation. In this case, she’s reducing her risk of ruin from where we started out at 86% down to a 6% with an income of $30,000 a year.

Finally, if she were to work until 70, collect the spousal benefit at 66, and purchase the two annuities, she could phase her income, taking $40,000 a year at the beginning when she’s traveling and wants to do things, and then reducing it towards the end of life.

There’s danger to having just one approach, assets under management, taking a percent of income out of the portfolio every year. If that’s the approach used, the individual is forced to self-insure. They’re taking on the longevity risk, the fact that their portfolio could run out, and that they could have sequence of returns risk with what’s happening in the market. That’s not the right solutions for the mid market.

Encourage your women clients, family, and friends to work as long as possible and delay Social Security if they’re in good health. Traditional methods of generating income are less effective for the middle market because they have other assets. They get to retirement and there is this whole other asset with their home equity. Same thing with Social Security; by delaying they get a huge increase in the present value of assets that can help with their lifetime retirement income. A combination of options works best.

The order in which those options happen also makes a difference in how risk is reduced. The biggest thing is that adding more lifetime income addresses is the sequence of returns risk, which is a big bomb that can put people off course early in retirement. But watch because there are diminishing returns: The more you annuitize, the less overall because those assets are overall less returns except for Social Security, and also, you don’t have the inflation protection from the annuity products unless you choose it as a rider.

Our point is to provide a way that gives clients permission to enjoy retirement and lifetime income, knowing that they don’t have to be worried about what the markets are doing, having some money in the markets but also a good base of income to cover their fixed expenses.