It is well known that women earn roughly 80 cents on the dollar throughout their careers compared to men, reducing the amount women can save for retirement. It makes sense then that they receive Social Security benefits that are, on average, 80% of what men receive. So, there is this retirement income gender gap.

Women are also more likely to be widowed than widowers. In the U.S. in 2020, there were more than three times as many widows as widowers. In addition, women are the caregivers throughout their lives and are more likely to leave the workforce or take part-time jobs to accommodate caregiving responsibilities. This also contributes to lower Social Security benefits and lower total retirement income. During the pandemic, about 2 million women left their jobs needing to care for children, with schools being shut down. Caregiving.com has found that women earn $324,000 less in wages and benefits during their lifetimes because of caregiving.

Women are nearly four times more likely to care for their spouse or partner in older age. We’ve all seen situations where mom takes care of dad, and then dad dies, so who will take care of her?

There has also been an increase in grey divorce, which can have an outsized impact on women’s overall retirement assets.

It may come down to genes and/or social upbringing, but women feel greater pain than men when they lose money. Women tend to shy away from stocks more than men do. This makes sense because stocks are more volatile and unpredictable than bonds or cash, so women generally shy away from them. Perversely, it is the wrong direction, as stocks have outpaced inflation over long periods versus bonds and cash, so women need a slightly higher exposure to stocks.

Research Promoted by the Academy for Home Equity in Financial Planning at the University of Illinois.

The Academy has collected research that answers the following:

- Is the reverse mortgage safe? No one wants to recommend something that will impact your clients negatively.

- Is the reverse mortgage affordable?

- Can a reverse mortgage actually improve retirement?

The thing to keep in mind here is that older women are homeowners. In 2023, about 80% of people in America who are 65 and older were homeowners. When older men and women are surveyed, around 85% of them want to age in place in their homes.

Home equity represents about two-thirds of the net wealth of the average American. There is this huge illiquid asset that needs to be taken into consideration in planning for a secure retirement, particularly for women.

There are several ways people monetize their home. You can:

- Rent it as an Air BnB. We have heard from the Air BnB folks that older women are their No. 1 population of hosts.

- Do a Golden Girls situation where you rent rooms. Bring in some girlfriends to live with you, sell and move.

- Probably the least popular, at least with the kids, maybe, is moving in with the kids.

- You can monetize your home via a new mortgage requiring a monthly payment. You could do a refinance for a cash-out or a lower payment. You can get a home equity line of credit (HELOC), but the caution here is that older homeowners tend to be denied mortgages.

- You can monetize your home without mandatory payments with a reverse mortgage.

How Has the Modern Reverse Mortgage Evolved?

It is common for financial products to get better over time. Credit cards, annuities, and insurance products have been improved over time by the companies that produce them or by regulators.

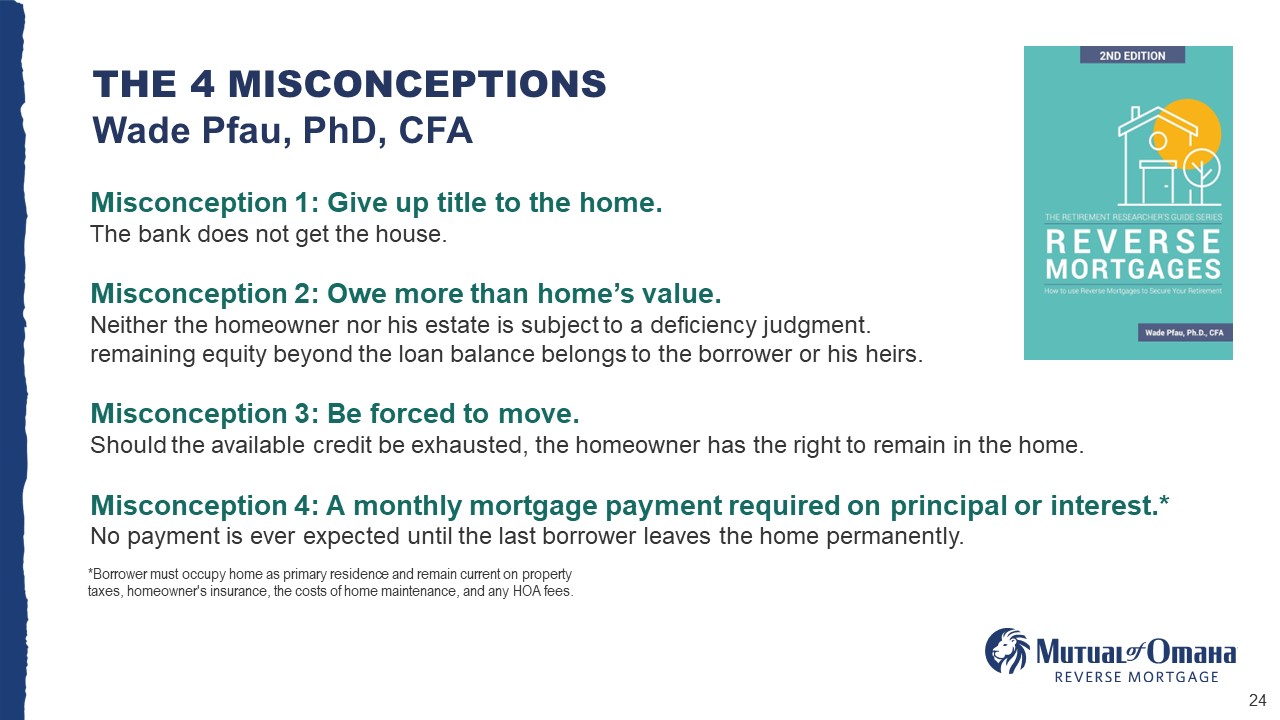

That is what has happened with the reverse mortgage. However, the modern reverse mortgage has some persistent myths still attached to it. Dr. Wade Pfau points out the following in one of his books on reverse mortgages.

Misconception 1, and the number one thing you have to help clients understand is that you keep the title to the home. You are not trading in your home and giving title to the bank. You have a mortgage on it, and the lender will wait to be repaid. So, the home’s title and control are not forsaken to take on a modern reverse mortgage. It used to be that way 30 years ago but has changed in the last three decades.

Misconception 2, if your loan balance exceeds the house’s value, you would be subjecting your kids to a deficiency judgment. That is not how it works. For the modern reverse mortgage, the house is the sole collateral for the loan. You can never owe more than the house brings at fair market value. And if there is remaining equity, it belongs to you or your estate.

For Misconception 3, Dr. Pfau points out that even if you use all the money and it is exhausted, the lender has no right to come in and tell you, “Whoops, it’s all over,” and kick you out to the curb. Nope, it is your house. As long as you keep your taxes, insurance, and maintenance up, and if there are any HOA fees current, just like any mortgage in the United States, it is your house, and you cannot be forced to move.

Misconception 4 is that a monthly mortgage payment is required on principal or interest. No monthly principal or interest payment is due until the last homeowner dies, moves, or sells. One of a couple can go to a nursing home, and the other one has every right to stay in the house. They have not given up the title to the house.

How Do Modern Reverse Mortgages Generally Work?

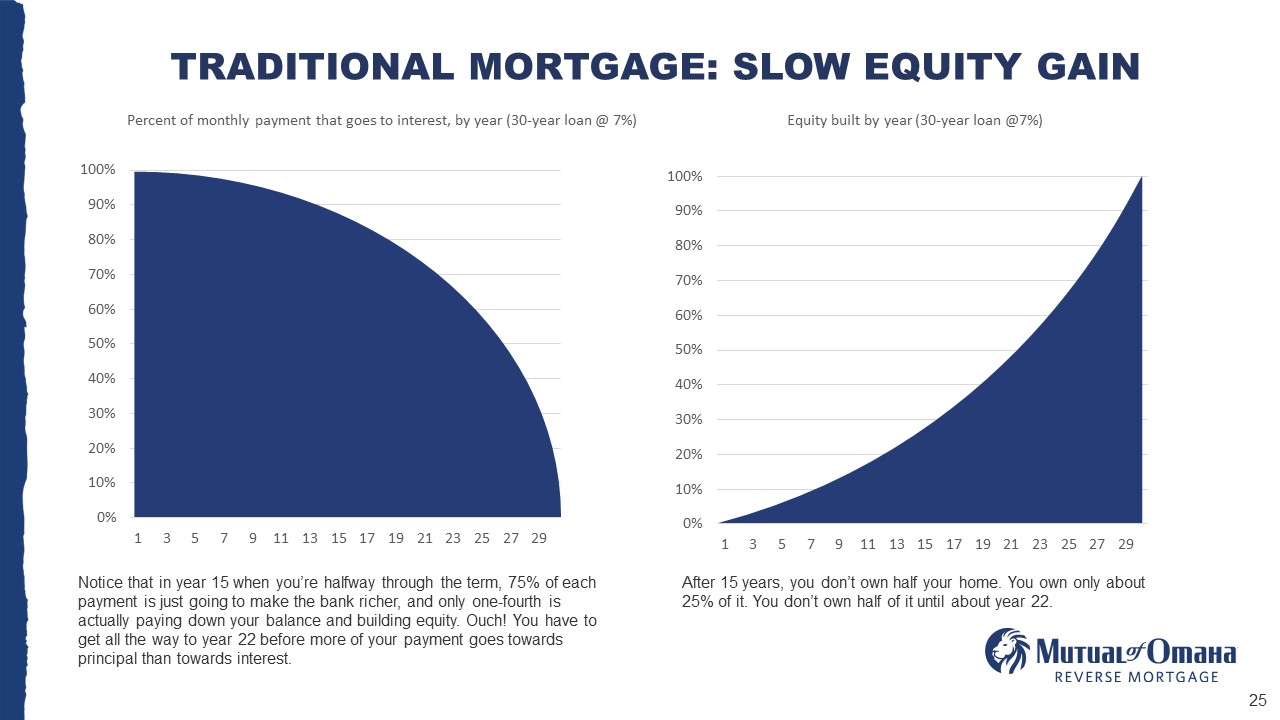

A traditional mortgage is front-loaded on the interest, so equity builds up over time.

With the reverse mortgage, you make payments if or when it suits you. If you choose to make payments, you can make payments just on interest. For example, Dr. Wade Pfau says do not make payments if it is going to, in any way, jeopardize your portfolio. But you can do that if your portfolio is robust and has good returns, and you want to make some payments on your reverse mortgage. But the expectation is that most people will not be making payments.

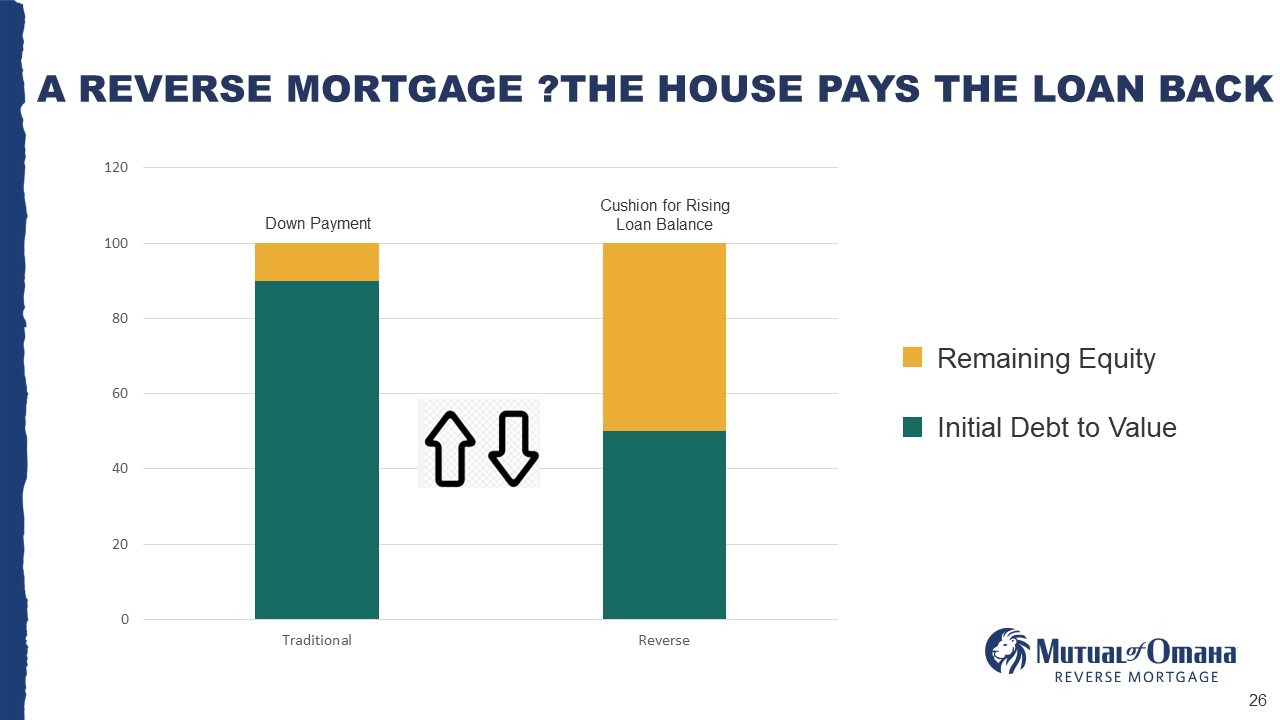

With the traditional mortgage, your equity goes up as you make payments. With a reverse mortgage, your equity will decrease if you do not make payments. So, because of that and because the house is the sole collateral for the loan, you will get less for a loan. This is what you would get from a reverse mortgage.

Again, with the traditional mortgage, you must start making payments immediately; with the reverse mortgage, you do not.

What is a Reverse Mortgage?

It is important to understand a reverse mortgage conceptually. It is a mortgage. The most crucial point of the modern reverse mortgage is that it is a nonrecourse loan; only the house pays the loan back. So, the house, just like a regular mortgage, provides and serves as collateral. But in a reverse mortgage, the house is the sole collateral. Someone’s income or ability to repay is not considered. To do this, actuarial principles apply. Reverse mortgage lenders must know how long people are projected to live to know how much money can be lent.

A reverse mortgage has FHA insurance of about two percent of the home value at the beginning of the mortgage, making the loan nonrecourse. Almost all reverse mortgage borrowers fold the insurance cost into the loan, so they do not have to pay for it out of pocket. Monthly premiums accumulate on the loan balance, totaling half a percentage point per year.

FHA insurance limits the debt for the homeowners and the heirs to the house’s fair market value at the loan’s end, whatever it may be, and it prevents the incursion of any other assets to satisfy the debt. No one can come to the homeowner or the children and have any expectation that anything else will pay the loan back but the house. In research by Dr. Barry Sacks, he points out that FHA insurance allows part of the house to be spent because if they are in the house for a long time, the loan can exceed its value. The house gets used throughout the entire loan term until that maturation event, generally when the last one of the homeowners dies, moves, or sells.

What are the Pros and Cons of Reverse Mortgages?

The cons are that it will cost you some equity because of the FHA insurance component. Also, interest on the loan balance is a bit higher generally than a regular mortgage (but only a little) and will compound if interest payments are not made. There is no expectation that a borrower must make interest payments, but you can make an interest payment.

What are the pros of the modern reverse mortgage?

- It is nonrecourse.

- It is flexible; you can pay interest (or not), pay interest and principal in some years when it suits you, or only in December.

- A reverse mortgage line of credit cannot be canceled, frozen, or reduced. So, if home values drop, interest rates go up, or whatever calamity happens in the greater economy, it cannot affect a reverse mortgage.

- Nor foreclosure is possible for missing payments because no payments are required.

- Credit capacity grows with age; as your longevity shortens, you get more access to your equity.

Regarding costs, Dr. Wade Pfau, who has studied reverse mortgages extensively, says reverse mortgages cannot be viewed in isolation. Their cost can be more than offset by gains elsewhere in the financial plan. And this is the key. If you have other assets, thoughtful use of a reverse mortgage can protect those other assets.

What the Heck is a HECM?

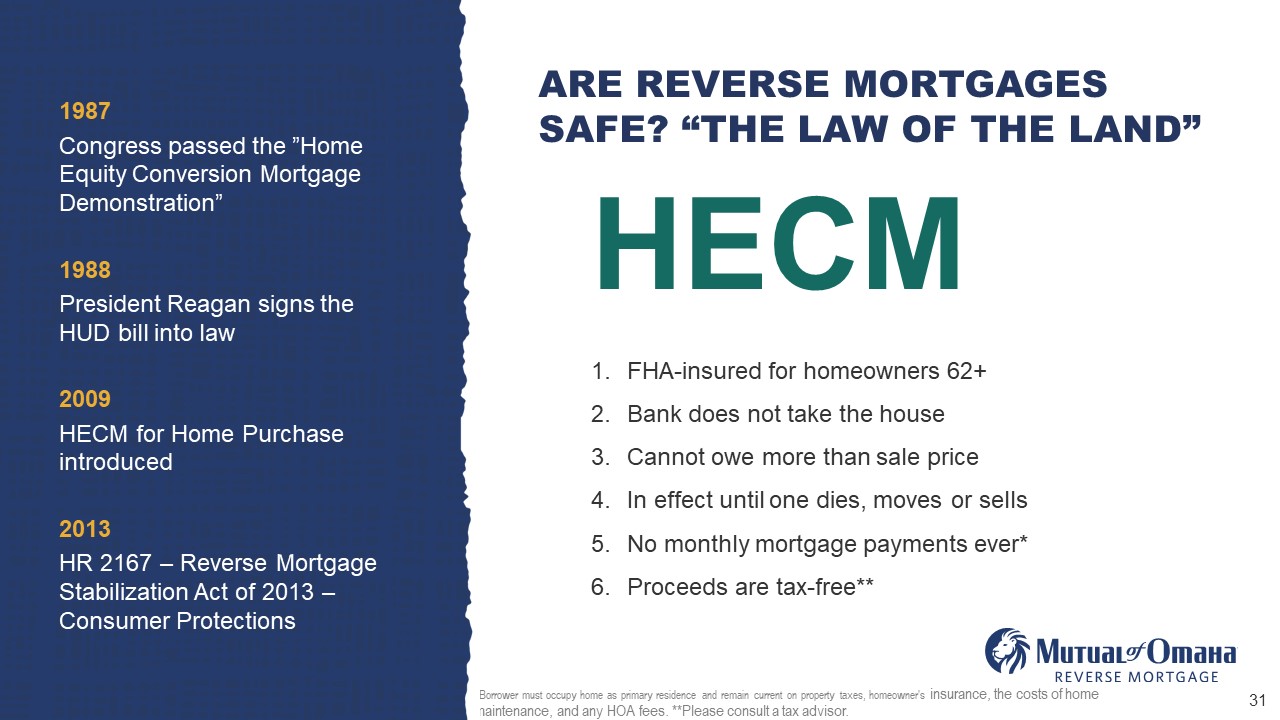

The acronym, HECM, stands for Home Equity Conversion Mortgage. Congress passed the “Home Equity Conversion Mortgage Demonstration” in 1987.

Ninety-five percent of all reverse mortgages in our country are HECMs. Additional consumer protections have been added over time to improve the HECM continually.

A HECM is FHA insured for homeowners aged 62+. Bank does not take the house, and the homeowner cannot owe more than the current value when the last homeowner dies, moves, or sells. There is no monthly mortgage payment ever, and the proceeds are tax-free.

The IRS considers proceeds from a mortgage as debt, not income.

Every client must attend an FHA counseling session and be given the book, “Use Your Home to Stay at Home.” The FHA-approved counselor has nothing to do with the transaction and is there to ensure they understand that it is a mortgage, interest is involved, their home is theirs, and they are not signing it over to the bank. The FHA counselor also ensures they understand they are responsible for their tax, insurance, maintenance, and HOA.

A HECM can be a revolving credit instrument. So, let us look at a regular credit card. Let us say your credit card limit is $10,000, and you spend $9,000, so your credit available goes down to $1,000. In month one, you pay it right back, and your credit available goes back up to $10,000. Next month you spend $8,000, so your credit available goes down to $2,000. Pay it right back, and your credit available is back to $10,000.

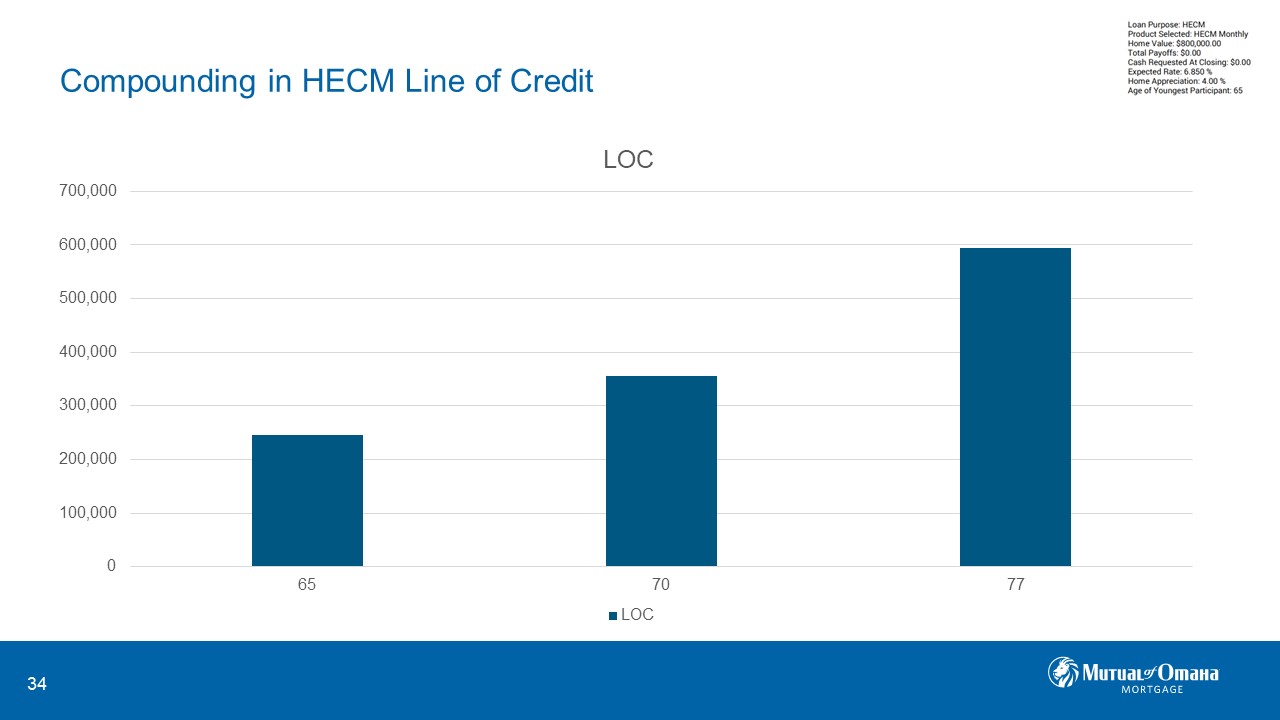

A HECM line of credit works the same way. You can make payments against it, but you are always going to have growth at the same rate that the loan balance is growing. For example, for a $100,000 beginning line of credit at 4% interest, the line of credit will be $104,000 at the end of the first year. At the end of the second year, the HECM line of credit will be $108,000.

The credit limit in a HECM line of credit has to grow. It grows as part of the internal structure of how the HECM works, and it cannot be canceled, frozen, or reduced even if the home value drops. Here is an example of a HECM line of credit growth at age 65 with an expected rate of 6.85%.

A HECM line of credit is going to compound as well.

The growth in the line of credit really interested the original retirement experts. The fact that this line of credit was going to keep pace with what was going on in the market and that it could not be canceled, frozen, or reduced if the overall real estate market or other financial markets collapsed. The growth in the line of credit is backed by the US government’s full faith in and credit.

Would a regular home equity line of credit (HELOC) be less expensive overall? Dr. Wade Pfau points out that if you set up a HELOC, you will not get an increase in your credit capacity as you would with a HECM. With a HELOC, you do not get to borrow from it after ten years. Dr. Pfau also says that opening a HECM line of credit earlier allows for greater availability of future credit relative to waiting until retirement.

Proceeds from a reverse mortgage can be distributed:

- as a lump sum.

- as a monthly tenure payment that will last for as long as you are in the house.

- as a term payment. For example, say you need $12,000 a month so that your husband can have care at home. They can figure out how long paying $12,000 a month would last.

- as a line of credit that the lender cannot cancel, reduce, or freeze, or

- as a combination of these.

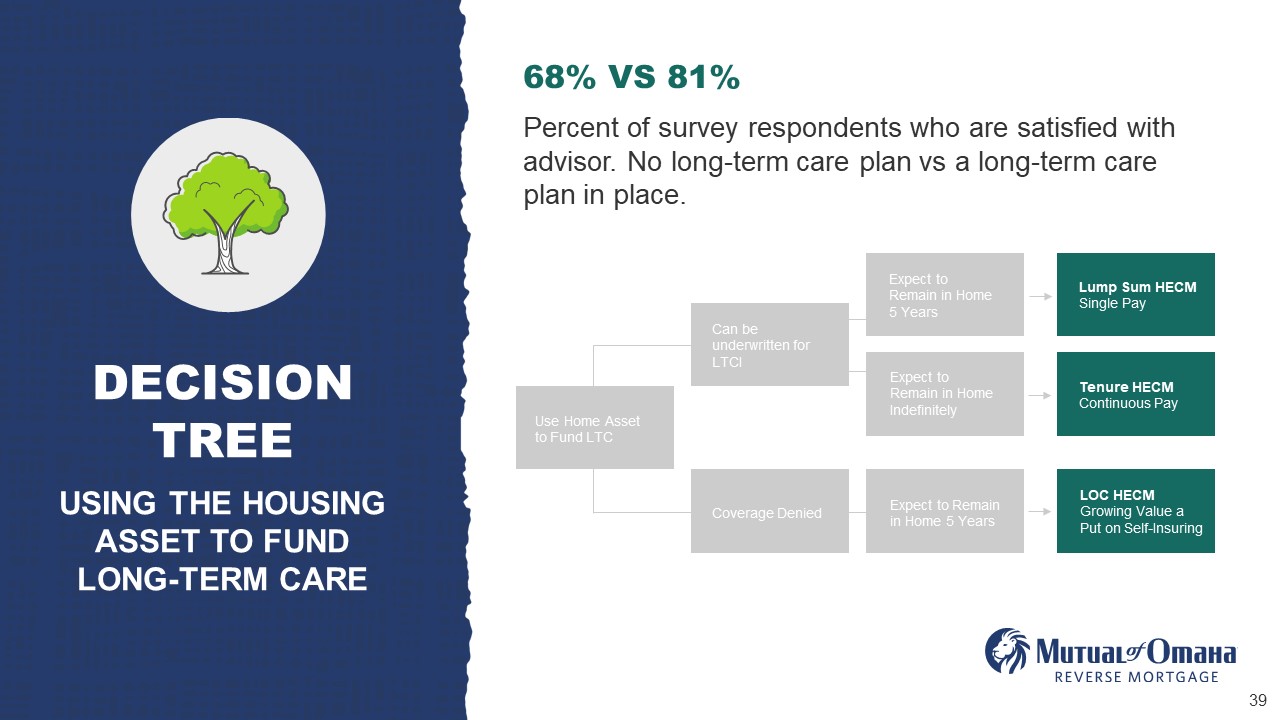

How Can You Use a Reverse Mortgage to Self-fund Long-Term Care?

The availability of long-term care policies has been shrinking and becoming more expensive. People are not buying them.

People who work with an advisor might not have long-term care insurance, but they can create a plan for long-term care. Clients whose advisors talk to them about long-term care needs are more satisfied than those whose advisors put their heads in the sand because it is just such a complex problem to solve if they are not going to get long-term care insurance.

Here is a decision tree for how to use the housing asset to fund longer-term care:

Say you want to use the home asset to fund long-term care. First, you must check to see if the client can be underwritten for long-term care insurance because of the cost of setting up a reverse mortgage. It is generally assumed that you should expect to stay in the home for five years to justify the cost of setting it up. You could then use the lump sum HECM for a single-pay long-term care policy.

If you expect to stay in the home indefinitely, you could use the tenure continuous pay option to pay long-term care premiums. If coverage is denied and you expect to remain in the home for five years, you can set up that line of credit so that it has growing value, which is like a “put” on self-insurance. So, if you do not spend it, the money is just equity that was not spent. But that growing line of credit is there for you should, in the future, you need long-term care in the home.

Again, the HECM line of credit compounds monthly at a contractually established rate. The lender cannot alter it. It cannot be canceled, frozen, or reduced. It grows even if the housing value does not. The line of credit will grow regardless of the rate of home appreciation. HELOC growth is zero.

In addition, using the reverse mortgage line of credit for long-term care expenses instead of taking the funds from your retirement portfolio dramatically increases the amount and longevity of the portfolio over time.

Case Studies

Let’s say Stephanie is 72 years old. She has a yearly principal and interest payment of $13,608. So, by taking out a HECM, she replaces her current mortgage with a reverse mortgage. She will get enough to pay off her current traditional mortgage from her reverse mortgage and keep $80,000 of equity in her growing HECM line of credit. Using Money Guide Pro (a popular planning software used by financial planners), If she had kept her traditional mortgage, she would have had a low probability of retirement success, with $1,100 a month eating up her retirement income or savings. Even if she converted her HECM line of credit into a tenure payment of $463 a month for life, just an extra $463 a month on top of the improved cash flow of not paying $1,100 a month on her traditional mortgage, increases her probability of retirement success to 99%.

Let’s say Carlos and Maria are aged 66. They have an expected monthly retirement income of $6,000. They have retirement savings of $750,000, and their inflation prediction is three percent. And their return during retirement is estimated at six percent. Their home of $500,000 is almost paid off.

After the divorce, they split the retirement funds. Carlos moves out of the house, and he gets something else. Maria gets the $500,000 house, and her cash flow needs are reduced somewhat, but she still has a house.

Say Maria does a reverse mortgage and draws $1,200 monthly, a modest amount, or $14,400 yearly. Her portfolio could be depleted quickly if she did not get a reverse mortgage. But just having that extra $1,200 a month reduces the need to draw on the portfolio and improves her portfolio resilience significantly.

What is a HECM for Purchase Reverse Mortgage?

Now we will talk about buying a house using a reverse mortgage. This is not the most intuitive thing in the world. People don’t think about buying a house using a reverse mortgage; they think I will put a reverse mortgage on my old house and not move from it.

The legacy home is the departure home. It is not used to calculate purchase money funds. It can be the source of the down payment for a new house, but it is not part of the reverse mortgage. The reverse mortgage is placed on the new home, the new principal residence. The new house is used to determine the HECM for purchase funds available.

For example, Ron and Judy are in their 70s. They have been living in the same house in New York together for years, but not as a married couple. Eventually, they sold their home in New York and received net cash of $330,000. They divide their personal property into two moving pods and move to South Carolina. Ron moves into a short-term rental, and Judy lives with her sister while house hunting.

Judy uses $127,740 of her share of the $330,000 they netted from their home in New York as a down payment on a HECM purchase transaction to buy a $305,000 home. She can retain $42,260 from her half of their home’s sale. The remaining difference between the $127,740 down payment and the $305,000 prior home proceeds is financed with a reverse mortgage. She can move in and has no monthly principal and interest payments. Judy uses $20,000 of her remaining home sale to furnish her new retirement home.

Ron did a similar thing. He bought a condo in Myrtle Beach and a membership to a golf course. So, it worked very well for both of them.

In a divorce, a HECM for purchase can make the difference. For example, let us say the wife takes out a reverse mortgage and gives her husband half of the reverse mortgage proceeds. He leverages the money to buy a new house for himself. Or they can sell the family home, and each takes their share, as Ron and Judy did. They can leverage that down payment from the sale of the house and bump up the value of the house that they buy individually and still have no principal and interest payment. It is an equitable solution to housing, which is sometimes not that easy to accomplish in divorce situations.

It is important to recognize that a HECM purchase reverse mortgage is a one-time down payment in cash, usually about 60%. The remaining money comes from a reverse mortgage. The lien on the house is just a reverse mortgage, and no monthly mortgage payment on the principal or the interest is ever due.

How to Use a HECM to Maximize Social Security

Say Elizabeth is 62. She has $84,000 in retirement cash flow needs. She has a pension of $5,000 a month. She has an IRA of $500,000. Her combined tax bracket is 33%.

What happens if she defers her Social Security until age 70? She can draw $2,000 monthly from the reverse mortgage line of credit to help the spending gap until age 68 and withdraw from the portfolio for the remainder. This allows her to protect her portfolio by delaying drawing from her IRA as long as possible to meet her spending needs and save on taxes.

How to Use a HECM to Protect the Portfolio

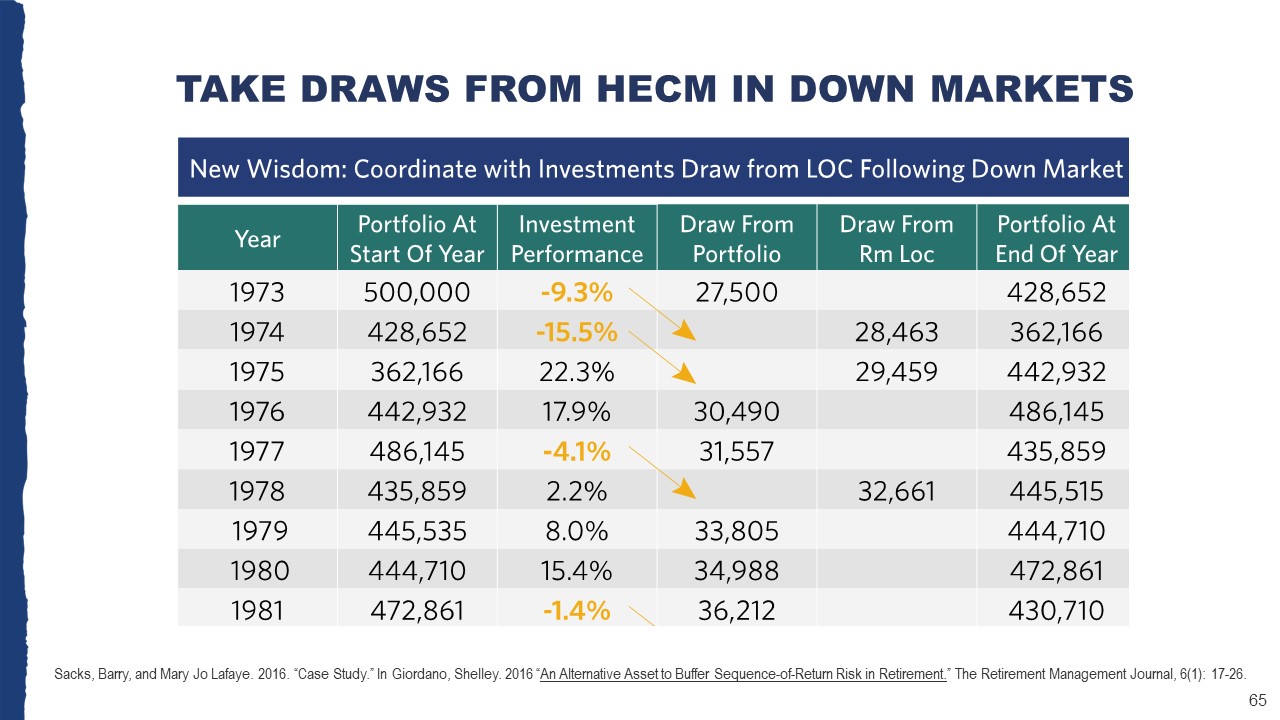

Research by Dr. Barry Sacks and Dr. Stephen Sacks, as well as Dr. John Salter and Harold Evensky, CFP®, demonstrate that taking draws from a HECM instead of from the portfolio in down markets is a way to mitigate sequence of returns risk. The idea here is that if you experience a year of negative return, the following year, do not draw from your portfolio; draw instead from your reverse mortgage line of credit.

Draws here from the portfolio increase over time because of inflation. Say there is another bad year; do not take from the portfolio; draw from the reverse mortgage line of credit. Another bad year, draw from the reverse mortgage line of credit instead of the portfolio. Above, you see that four of the first nine years of a $500,000 retirement portfolio were in negative territory, which is a bad sequence of returns.

Some people plan to use a reverse mortgage as a last resort. In this example, on the left is a $500,000 portfolio where draws are taken as needed without incorporating the use of home equity.

They run out of money in 23 years and must take large draws from their reverse mortgage, resulting in $0 in the portfolio and $583,000 in debt on the reverse mortgage.

On the right side is the coordinated strategy, where you coordinate your portfolio with the reverse mortgage. Those years you drew from the reverse mortgage line of credit have an unbelievably protective effect on the $500,000 portfolio. You actually might have $1 million left in a portfolio. Now, there is a significant ending loan balance. However, the interest on the reverse mortgage could have been mitigated if you wanted to or not.

But the point is that the differential to the estate is $933,764 just by using another asset to protect the portfolio. Without the use of the reverse mortgage, there is only debt on the house. With the use of the reverse mortgage, there is debt on the house, but much money is in the portfolio to offset it.

Who Doesn’t Need a Shock Absorber?

I love considering home equity conversion mortgages as a giant shock absorber.

And what are some of the shocks that come with retirement?

- Hearing aids, $6,000, not covered.

- Dental shocks. I cannot tell you how many clients leave the closing at a reverse mortgage and walk across the street to the dentist. We had a financial advisor who had $50,000 in dental work done as soon as she set up a reverse mortgage. Fifty thousand dollars would take a big chunk out of a portfolio.

- Car repairs can be just devastating to people later in life.

- Housing value shock. With a HECM, it does not matter what the housing value becomes. The appraisal is done at the beginning, which is what you are locking in.

- Health shocks. Anything that can happen to you, your spouse.

- Liquidity shock, not having access to money.

- Inflation shock. We have seen a bit of that, have we not?

- Divorce shock.

- And then, of course, portfolio shock. Anything can happen.

Key Takeaways

- The duty of care and business promotion improves when advisors are sensitive to the unique needs of women clients.

- The modern HECM reverse mortgage is safe for clients.

- The nonrecourse benefit cannot be had anywhere else.

- The reverse mortgage cannot be canceled, frozen, or reduced.

- The reverse mortgage costs are born by the mortgage itself. They are folded into the loan. Again, the differentiating cost between a net and a traditional mortgage is mostly the FHA insurance.

- The compounding interest can be mitigated by voluntary payments when the portfolio is robust. And as Dr. Pfau says, skip the payments if the portfolio is stressed.

The mortgage cost cannot be assessed without evaluating the effect on other assets.