By Bob Mauterstock, CFP®, ChFC, and CLTC, Eldercare Expert, Speaker, Author, Facilitator

Most of us are not aware of the changing dynamics within our country. The fastest-growing age group in this country is the people over the age of 85. Many retirees could live 30 or more years in retirement, and they may live as many years in retirement as they actively worked. Children born after 2007 can expect to live more than 100 years. This is going to impact and change the whole world of financial planning.

According to the Alzheimer’s Association, the bad news is that over 46 percent of those over age 85 will develop some form of dementia. The most feared condition of later life amongst retirees approaching retirement is dementia, and more than 32 percent are afraid of some form of dementia affecting them. It is more than cancer; it is more than Covid-19, stroke, or heart attack. So, this is something that we as advisors must deal with.

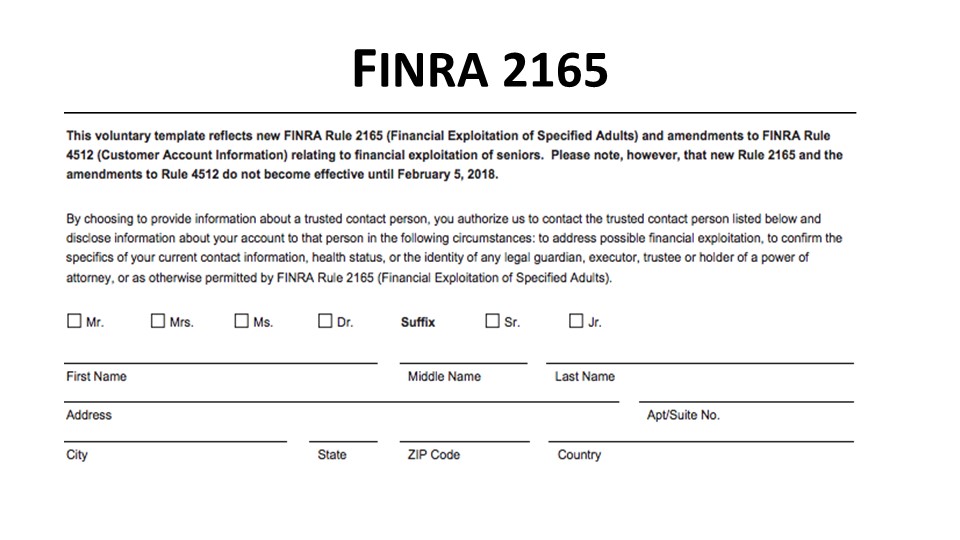

FINRA created this form for those associated with a broker-dealer. It was issued last year to advisors because of an increasing problem and a problem that I had myself.

If you have a client with diminished capacity, how do you relate that to friends and family without breaking their confidence? Do you have the right to pass on to other family members, friends, and so forth that the client is losing their mental capacity? No. So, FINRA created this form, and I suggest that you develop a variation of it for yourself that you can give to clients that will give them the authority to create what we call a “trusted contact person.” It says, “To address possible financial exploitation, confirm specifics of your current contact information, health status, or identity of a legal guardian, executor, trustee, or holder of power.” In other words, giving the advisor the authority to pass on to a trusted contact person their concern that you are having issues with mental capacity.

I had a situation like this before I used this form. I had an aging doctor who was a very good client of mine for over 20 years, and he started calling me every week asking to speak to his accountant. And I told him every time, “Your accountant does not work here, doctor. Let me give you his phone number.” I became increasingly aware that he had a significant mental dementia issue, but I could not tell anyone. I did not have the authority to share that with anyone because he had not given me that authority.

If I had this trusted contact form, I would have been able to share that information with someone else. If there is one thing that you take out of our discussion today, it is developing a version of this form to use yourself with your clients. Especially if you are bringing in new clients who are age 60 or older, you may want to consider having all your clients sign it and just tell them, “Well, this is just a matter of our normal practice in our firm is giving us the authority to contact a trusted contact.” Keep that in mind because that will be an increasingly important issue to deal with if you have any clients that have diminished capacity.

Now let’s address the seven steps to meet a new retiree’s elder planning needs.

Step One: Create a single source recordkeeping document, or in my terms, their life folio.

How often have your clients looked all over the place to find a title for their auto coverage, healthcare proxy, long-term care policy, or life insurance policy? Just imagine what it would be like if, at a point of emergency, they had to find some of those documents; they would not be able to do it.

So, you need to create a three-hole punch binder in which you can put all these documents or note where they can be found.

- What are your investment accounts? Where are they? Whom are they placed with? Who owns them? Husband, wife, child, or trust?

- Insurance. Do they have life insurance? Do they have long-term care insurance? Do they have annuities, and where are those policies located? I remember talking with one of my clients and saying, “I need to look at your life insurance policies, John.” And he said to me, “Well, Bob. I don’t need to do that. I have had those policies for a long time. There is no problem there.” And so, I asked him to bring in the policies. After I reviewed them, I said, “Who is Mary?” And he said, “Well, Mary is my ex-wife. We have been divorced for more than ten years.” I said, “Well, John, she is the beneficiary of your $100,000 life insurance policy.” He was not even aware of that fact.

So, your clients must determine where their insurance policies are and be able to determine if they’re still in force. If they have insurance policies that are no longer in force, have them throw them out. Do not keep them because if they are deceased and you, as the advisor, are trying to track down the benefits and the policy does not exist, you will waste a lot of your time.

- Legal documents. And we will talk later about the specifics of the legal documents that you need to have. But in this life folio, you need to determine where the documents are and what the documents are. If you hold copies, or does your attorney hold the primary document? You need to find out where the documents are and list them in the life folio

- Advisors. You need to make a list of all of your advisors, your accountant, your attorney, your financial advisor, and your religious advisors so that if anything happens to your client, you and their family can contact those people to let them know that there is a problem or they are deceased.

- Internet accounts. How many internet accounts does your client have? What are their user names and passwords? I don’t keep this on paper in my life folio, but I use something called Keeper, a software program to keep track of all my internet accounts. Some of these accounts will contain digital assets in the future, and they will be worth something./li>

Once that life folio is collected in that three-ring binder, make sure the entire family knows where it is because if Mom or Dad has a problem, you will have to find out where their documents are located, and the children need to know.

Step Two: Learning How to Protect Your clients’ assets.

There are many different programs or avenues that you could use to help protect your client’s assets.

- Medicare is the health insurance for those of us who turned age 65. It includes Sections A, B, and D for hospitals, doctors’ offices, and prescription medications. However, Medicare does not cover custodial care. If you have a client who goes into a hospital and then goes into rehabilitation, they are covered during rehabilitation for up to 100 days. The first 20 days are full coverage, and the 80 days after that are co-pay. After 100 days, the coverage stops.

- Medicaid is a partnership between the states and the Federal government to cover people who have run out of assets. In Massachusetts, to get coverage for Medicaid to be in a long-term care facility, you can only have $2,000 in assets, and your spouse can have up to $137,000 in assets. But that is it. Medicaid is really for those clients who have needed care or had care and ran out of money.

- Veteran’s benefits. Veteran’s benefits can be from a veteran’s nursing home to individual care. There is something called the Aid and Attendance Benefit, which is also known as the veteran’s pension. For any veteran who served during times of war, at least 15 days during any time of war, they are covered for the Aid and Attendance benefit. This benefit will provide them with over $2,000 a month of expense coverage for themselves, and if they are deceased, they will provide over $1,000 for a spouse, but they have to show the need for that care and that their expenses are greater than their income.

- Long-term care insurance. I have long been an advocate for long-term care insurance throughout my career because there is no other program available for individuals that covers the cost of custodial care in a nursing home, assisted living, adult day care, and respite care. Unfortunately, this industry has consolidated considerably over the last several years. When the companies initially came out with their long-term care policies, they expected that a certain percentage of people would surrender those policies. People have not surrendered their policies, so the claims ratio was much larger than insurance companies expected. As a result, long-term insurance carriers have had to increase their rates many times.

The condition is that they cannot discontinue your coverage. However, they can continue to increase your rates. This has happened to several of my clients who have long-term care policies. In many cases, the rates have gone up 50 percent. However, let’s assume you have a long-term care policy that costs you $4,000 or $5,000 a year. Well, guess what? That $5,000 could cover a single 30-day stay in an assisted living or a nursing home, so it is undoubtedly worthwhile.

The industry has recognized that people are now more interested in types of plans that will provide them with some benefits whether or not they need long-term care. These are called hybrid policies. Some are connected to a life insurance policy; some are connected to an annuity and provide build-up for life insurance or annuity benefits whether or not a person needs long-term care. As a result, people can have these long-term care policies and still get benefits from them whether or not they need care.

Step Three is Building a Network of Professionals.

As a financial advisor, you do not know everything that is going on with your clients; you do not know all about their care, medical professionals, or insurance. It is very valuable to build a consensus or a council of other professionals to assist you in making these decisions. Certainly, an elder law attorney specializing in elder law is one of those important members of this team. As your clients’ situation gets more and more complex dealing with the issue of aging, the elder law attorney will be an essential part of the team.

Some specialists deal with helping clients downsize from their larger homes into smaller ones and get rid of everything they have collected over the years. Insurance agents are also very important. Have your clients talk to a specialized long-term care insurance agent who understands the whole process of long-term care and also, of course, they need to understand what their Medicare coverage costs and what the benefits are through Medicare.

There are geriatric care managers. They provide care and do assessments of your client’s homes to see if they need care and if they can stay in their current home. They will do assessments for memory care to determine if there are memory care issues that the client has, so these are all factors that enter into their clients’ situation. So, as the advisor, you need to develop a team of other professionals that you can work with that provide the advice you need to meet your clients’ situations.

Step Four is to Make Sure All Your Legal Documents are Up-to-Date

It is very important to make sure these legal documents are all up-to-date.

- The durable power of attorney. This document gives a person the authority to make financial decisions for another person. Now, if your clients are married, both partners need to have a durable power of attorney on the other. In addition, either a child or another advisor needs to have a durable power of attorney on each of them. Why is that important? Suppose a client begins to show diminished mental capacity and their partner does not have the authority to act on their behalf financially. In that case, they cannot make decisions regarding the client’s account. If they do not have a durable power of attorney, they will have to go to the courts to get a conservatorship to act in their partner’s capacity, which can take months. It is also expensive, and the family member must prove their partner is incompetent before a public court.

- The healthcare proxy. This document allows a person to make healthcare decisions for another person. So, if my wife were ill and could not make healthcare decisions for herself, I could make those decisions for her. Our daughter has a healthcare proxy for both my wife and me because you never know when you will need to make healthcare decisions and in what circumstances you will make them. It is essential that whoever has that healthcare proxy understands what things you want to be done.

- A will. When was the last time that you reviewed your will? Who is what we call the personal representative or the executor of your will? Is that person still alive? The job of the executor of a will is to make sure that everything goes according to what you have stated in the will. It needs to be done by a detail-oriented person. Many people will typically name one of their children as their executor. Is that an appropriate job for one of your children to have? Can they do that job? Make sure they understand the executor’s role. Also, if the client has changed states, state rules may vary regarding how wills are transpired.

- Beneficiary statements. You may not consider these legal documents, but they are legal documents. Life insurance, annuities, and IRAs have both primary and contingent beneficiaries. You need to review your beneficiary statements; make sure they still are appropriate. Suppose your primary beneficiary is deceased and you do not have a contingent beneficiary. In that case, the life insurance will be included in your estate and then passed through probate, where it becomes accessible by creditors.

- The HIPAA form. HIPAA was created to protect people’s medical privacy. Say your dad is in the hospital, and you go to the hospital and say, “I would like to find out how my father is doing and if he is still in his room.” According to HIPAA, if you do not have a HIPAA form in place for that particular person, the person behind the desk cannot give you any healthcare information on that individual. In many cases, the HIPAA form is included in the form for the healthcare proxy, but not in every case. So, it is important to have that HIPAA form, especially if your clients are getting older and may end up in a situation where they need medical care.

- The DNR (Do Not Resuscitate) or a POLST (Physicians Order for Life-Sustaining Treatment) form. Initially, the DNR form was issued for terminally ill people who did not want to be resuscitated if they were to stop breathing. The form has been expanded and, in many states, has been added to or replaced by the POLST form. It looks at many areas of medical coverage, and you can indicate in those areas of medical coverage what you want to be done and what you do not want done.

Step Five is to Develop a Long-term Care Plan

One of the things that we have discovered is that almost 70 percent of people who plan to retire in the next ten years have no idea what their healthcare and long-term cost will be in retirement. Looking at most of your retirement projections and the various software programs, how many build-in long-term care, the potential cost for long-term care, and what will be needed for long-term care? Most of these software programs make no provision for this, so you have no idea what the impact is going to be on your client’s situation for the cost of long-term care.

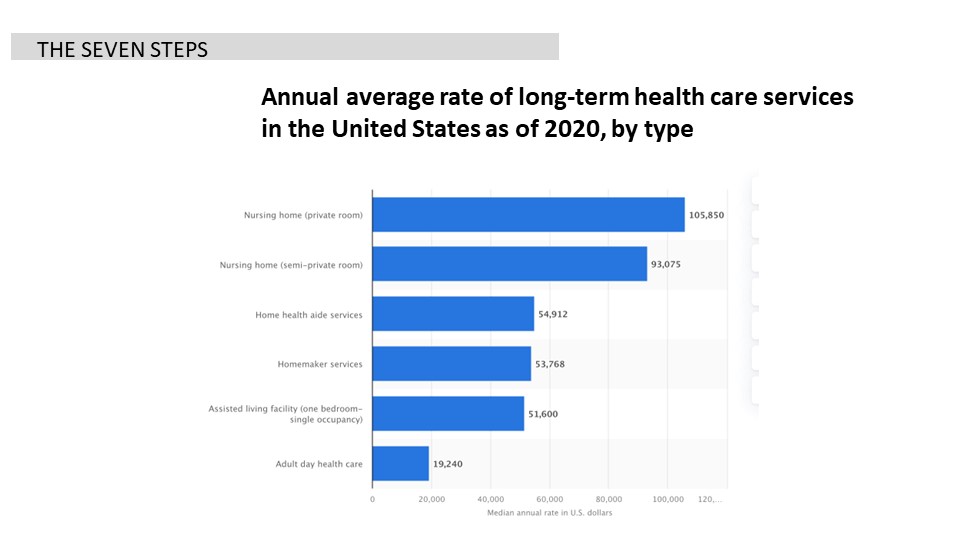

The following are the national long-term care costs as of 2020 by type.

A private room in a nursing home nationwide is over $100,000 a year; a semi-private room in a nursing home is $93,000. Home healthcare aides are more than $50,000; however, there is often up to a six-week wait to get a home care worker, and they are now charging $40 to $50 an hour, which doubles this cost of home healthcare aides.

If you want assisted living, it is essentially less, but over $50,000 a year. But you can see that if you need any of this type of care during your life, how it can impact your retirement, and you as the financial advisor need to put these projections into the long-term care estimate for someone’s retirement.

There are three fundamental questions to plan for:

- Can you stay in your home? Have you looked at your home to determine if it is wheelchair accessible? Are the halls wide enough? Are the bathrooms large enough for wheelchairs? Are there many stairs and people need to go up and down to get into the house or the bedrooms? Under what circumstances can they stay in their home and have no problems getting accessibility around the home?

What are their circumstances, and how will someone unable to walk negotiate them? Can they stay in the home, but what will be their alternatives if they are not? Should they move into a single-floor condo, or should they have one of them go into assisted living?

- Who will provide our care? Situations have become increasingly difficult for dealing with care these days. Many nursing homes are not accepting new patients right now, or they are full, and they are not accepting people until they are tested for Covid. If people want to stay at home, they are also having difficulty getting people who provide home care for them. So, providing care is becoming an increasingly difficult situation.

In many situations, unfortunately, their children will have to provide that care, at least temporarily, until better circumstances are found. Still, it is something that needs to be considered.

- How will we pay for our care? Certainly, if they have long-term care insurance, it is most likely that long-term care will cover a large amount of their costs. But where do the funds come from if they do not have long-term care insurance? Will they come out of retirement accounts, refinancing the home, second mortgages, or other ways to find money from the home? Where will they find the money?

Part of long-term care planning is end-of-life planning. This is probably one of the most challenging areas for most advisors to bring up and discuss because most of us do not want to get into what will happen when we die. There is a program that I have used, and I have found it to be exceptionally good in helping you have this conversation. It is called the Five Wishes. It is approved for healthcare proxy in 43 states, but it is used in over 50 states, and over 200 million people worldwide are using the Five Wishes. You can get a copy of it by contacting Five Wishes at www.fivewishes.org. It addresses:

- Whom do I want to make healthcare decisions for me? Whom do you want to provide decision-making for you if you cannot do it for yourself?

- What kind of medical treatments do I want? Do I want certain medical treatments not included, like intubation and other forms of care? Which ones do I not want?

- How comfortable do I want to be? Do I want to be assisted through various medications to be comfortable? How do I want that to be taken care of?

- How do I want people to treat me? How do I want people to observe me and talk to me? How do I want them to relate to me?

- What do I want my loved ones to know? There are certain circumstances in which individuals do not want their families to know what their needs are.

Complete it for yourself, make these decisions yourself, share it with one of your clients and say, “This is what I have done for my decision-making for end-of-life planning. Take a look at it and tell me what you think of it. What do you think of this program, and what do you think of what I have decided to do?” That will start a conversation with that person right away who can discuss in detail with you and eventually open up the questions they have for themselves and what they need.

Step Six is to Create a Legacy Plan

Much research has been done on older people in the United States, and two things become increasingly important as they age.

The first is maintaining control of their life as long as possible. To be able to continue to drive a car. To be able to live where they want to live and do what they want to do and not be limited in where they can go and what they do.

Number two is when that initial ability to stay as free as possible becomes less and less possible, how do I want to be remembered by my children and grandchildren? That is a legacy question, which becomes increasingly important to us as we get older. Create a Legacy Letter, and in this letter, you share what your values are. What has been important to you during your life? Is it important to you that your family have religious values? Is it important to you that they gather together a certain number of times each year?

These types of things are the values that you state in the Legacy Letter, and you may, in addition, offer various life lessons. What have you learned that either helped or hurt you and share that with your family?

Thirdly, express love and gratitude for those who have been important to you in your life. Express love and thanks to those who have treated you well and taken care of you. And possibly another issue might be giving guidance to trustees as to what you want to be done. You can put these types of things in a Legacy Letter to pass on to your family.

The Seventh Step is Building a Relationship with Your Clients’ Family

Over $40 trillion will pass from Baby Boomers to their children over the next 30 years. Will you understand and know who your client’s family members are? Do you know the first names of each of your top five clients’ children, and if you do, have you had the chance to meet each of their children?

One of the most important things that you can do as a financial advisor is to help to plan a family meeting where your client and their spouse and their adult children get together for a meeting and share all the things that we have discussed previously: the life folio, the legal documents, the leaving legacy, all of those issues can be shared at the family meeting.

So, how do you put together this family meeting? First, identify the Alpha child. The Alpha child in the family is looked up to by the other siblings, is successful, communicates well with their parents, is acknowledged and loved by their parents, and is respected by everyone in the family. The reason to identify the Alpha child is that when Mom and Dad want to get together with the family, some of the children are going to say, “Well, no. I cannot do it, I am too busy,” but the Alpha child will come to the rescue and make sure that everyone gets together. You (as their advisor) should volunteer to become the facilitator or one of the facilitators.

If you are not comfortable managing the meeting yourself, bring on a second person that can help you. Volunteering to facilitate a family meeting with your clients will make you the family’s trusted advisor. In the conversations you have with the family members, they will get to know you, what you can do, and what you can offer to the family.

As the research has shown, over 90 percent of assets will move from one advisor to another when both aging clients have been deceased. Children do not know their parents’ advisors and therefore have not kept the advisors that their parents had. But if you become the entire family’s advisor, they will look to you to provide that service to them.

What is the process of the family meeting? I call it facilitating without prejudice. You should enter the meeting having no predetermined expectation as to what the results should be. It is not your job to determine what the family should do.

The family will decide what they want to be done and how to do it for themselves. Your job is to be objective. You need to designate a scribe, a person who will keep track of the activity and the decisions made in the meeting and make sure that decisions are made through consensus. And what does that mean? You do not vote on decisions in a family meeting.

Once these results are determined, action items need to be assigned to family members, and you as a facilitator should follow up to see how many of those are carried out six months after you have made those decisions. So, the family meeting is an increasingly important part of the family.

The Certified Elder Planning Specialist Program

If you are interested in discussing and learning in more detail the things we have discussed today, inquire about our Certified Elder Planning Specialist program, which is available at our website www.planforlifenow.com. It is a ten-session, completely online program with questions and presenters. We have brought in the best presenters in the various areas of elder planning, allowing you to have a weekly discussion with them online as a group. It is an excellent program, and it is probably the only one that exists today to discuss and deal with the issues you need to know as an elder planning specialist.